Global DIY And Household Adhesives And Sealants Market Size, Share, And Industry Analysis Report By Product Type (Pressure-sensitive Adhesives, Anaerobic Adhesives and Sealants, Epoxy Adhesives and Sealants, Polyurethane Adhesives and Sealants, Acrylic Adhesives and Sealants), By Substrate (Wood, Metal, Plastic, Glass, Ceramic, Paper, Concrete), By Application (Bonding and Assembly, Sealing and Gasketing, Repair and Maintenance, Sound and Vibration Damping, Decorating and Finishing), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: February 2026

- Report ID: 179690

- Number of Pages: 397

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

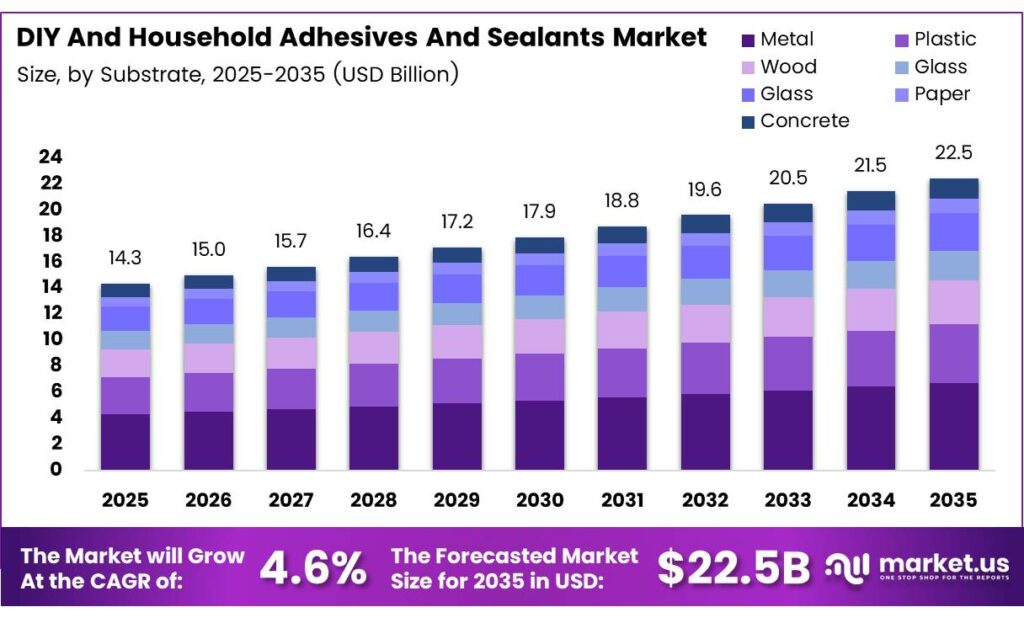

The Global DIY and Household Adhesives and Sealants Market size is expected to be worth around USD 22.5 billion by 2035 from USD 14.3 billion in 2025, growing at a CAGR of 4.6% during the forecast period 2026 to 2035.

The DIY and household adhesives and sealants market covers a broad range of bonding and sealing products used by homeowners, hobbyists, and contractors. These products include pressure-sensitive adhesives, epoxy formulations, polyurethane sealants, and acrylic-based solutions. Moreover, they serve applications from basic repairs to complex construction tasks.

Household adhesives and sealants perform critical roles in bonding diverse substrates such as wood, metal, glass, plastic, and concrete. Consumers increasingly rely on these products for home maintenance, decoration, and energy-efficient building improvements. Consequently, demand spans both urban and rural markets across developed and emerging economies.

- The U.S. Census Bureau reported that residential construction spending reached $848.9 billion, reflecting robust demand for adhesives and sealants in construction and DIY applications. This level of spending highlights the direct connection between housing activity and consumption of bonding products across residential markets.

Government investments in residential infrastructure and energy-efficient building programs create sustained demand for high-performance sealants. Regulatory frameworks promoting low-VOC and environmentally safe formulations push manufacturers to innovate. Additionally, public sector housing initiatives across the Asia Pacific and North America strengthen long-term market prospects for water-based and sustainable products.

- Henkel Adhesive Technologies division generated sales of 10,970 million euros in fiscal 2024, representing 51% of Henkel Group’s total sales. This figure reflects the scale and commercial significance of adhesive products globally, underscoring the sector’s maturity and growth potential for both industrial and consumer-facing segments.

Home renovation trends accelerate the adoption of multi-purpose adhesives and sealants among DIY enthusiasts. E-commerce platforms expand product accessibility, enabling consumers in remote areas to purchase specialized formulations. Therefore, digital retail channels become a significant growth lever for adhesive brands targeting cost-conscious homeowners seeking professional-grade results.

Key Takeaways

- The Global DIY and Household Adhesives and Sealants Market is valued at USD 14.3 billion in 2025 to reach USD 22.5 billion by 2035, growing at a CAGR of 4.6%.

- Pressure-sensitive Adhesives hold the leading share at 29.5%.

- Wood leads with a market share of 31.6%.

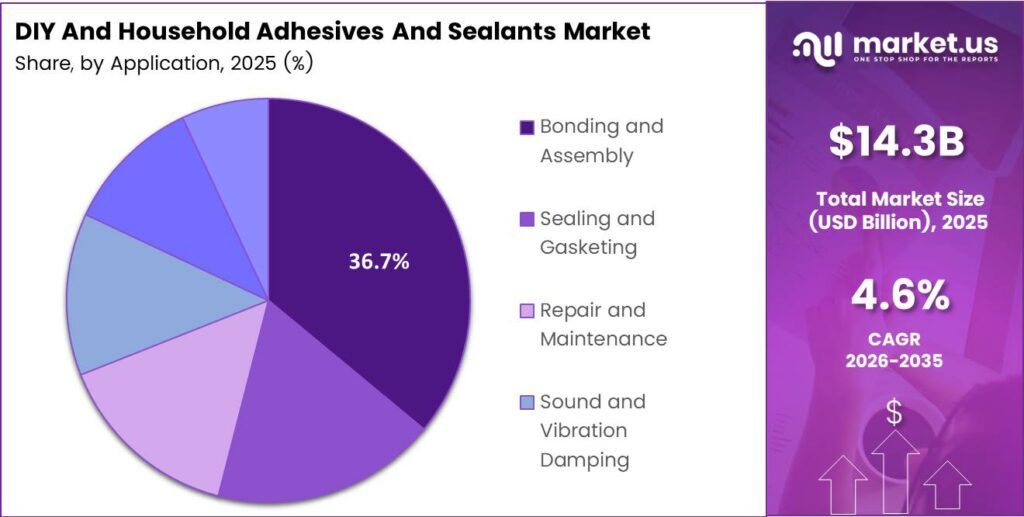

- Bonding and assembly account for the largest share at 36.7%.

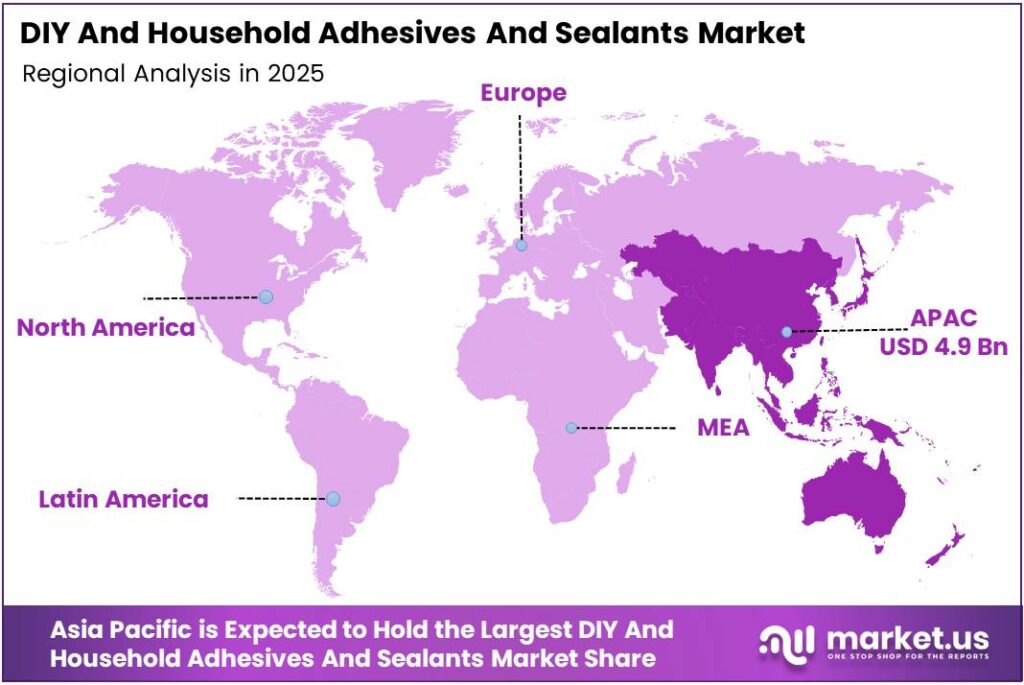

- Asia Pacific dominates the market with a share of 34.5%, valued at USD 4.9 billion.

By Product Type Analysis

Pressure-sensitive adhesives dominate with 29.5% due to ease of application and wide substrate compatibility.

In 2025, Pressure-sensitive Adhesives held a dominant market position in the by-product type segment of the DIY and Household Adhesives and Sealants Market, with a 29.5% share. These adhesives require no heat or solvent activation, making them highly convenient for household users. Moreover, their versatility across labels, tapes, and mounting applications drives consistent retail demand.

Anaerobic Adhesives and Sealants serve niche but important functions in threadlocking, pipe sealing, and metal bonding applications. Their performance in confined spaces without air exposure makes them preferred for maintenance tasks. However, their specialized nature limits broader DIY adoption compared to more universal product types in the household segment.

Epoxy Adhesives and Sealants deliver exceptional bond strength on metals, ceramics, and rigid plastics. DIY users choose them for structural repairs requiring high durability. Additionally, two-part epoxy systems are increasingly available in user-friendly packaging formats, expanding their accessibility for home repair and hobby applications.

Polyurethane Adhesives and Sealants offer flexibility, weather resistance, and strong adhesion across multiple substrates. They are widely used in window sealing, flooring, and outdoor applications. Consequently, their ability to handle movement and temperature variation makes them a practical choice for residential construction and renovation projects.

Acrylic Adhesives and Sealants combine paintability, UV resistance, and fast curing properties for interior and exterior use. Homeowners and contractors use them for caulking, filling, and decorative finishing. Therefore, acrylic formulations remain a staple product in the DIY segment due to their ease of use and broad application range.

By Substrate Analysis

Wood dominates with 31.6% due to its widespread use in residential furniture, flooring, and construction.

In 2025, Wood held a dominant market position in the By Substrate segment of the DIY and Household Adhesives and Sealants Market, with a 31.6% share. Wood bonding applications span furniture assembly, flooring installation, cabinetry, and structural repairs. Moreover, the global rise in wooden home construction and renovation activity sustains strong demand for wood-compatible adhesive formulations.

Metal substrates require adhesives with high shear strength and corrosion resistance for automotive, appliance, and industrial repair tasks. Homeowners and maintenance professionals increasingly use metal-compatible bonding products. Additionally, epoxy and cyanoacrylate formulations designed for metal applications are gaining popularity in the retail DIY segment for plumbing and hardware repairs.

Plastic bonding presents unique challenges due to surface energy variability across polymer types. Specialized adhesives for plastic include cyanoacrylates, UV-curing formulations, and structural acrylics. Consequently, the rising use of plastic in consumer goods, packaging, and home fixtures continues to expand the plastic substrate segment within household adhesive categories.

Glass bonding adhesives deliver optical clarity, chemical resistance, and flexibility for windows, mirrors, and decorative fixtures. Silicone and UV-curing formulations dominate glass bonding applications. Therefore, renovation projects involving glass installations and repairs create consistent demand from both professional contractors and DIY homeowners seeking reliable bonding solutions.

Ceramic, Paper, and Concrete substrates represent additional application areas with distinct adhesive requirements. Ceramic tile adhesives support bathroom and kitchen renovation projects. Paper adhesives serve crafting and stationery needs. Concrete bonding agents address structural repair and finishing tasks, making these substrates collectively important across residential and light commercial applications.

By Application Analysis

Bonding and assembly dominate with 36.7% due to its broad use across furniture, fixtures, and home construction.

In 2025, Bonding and Assembly held a dominant market position in the By Application segment of the DIY and Household Adhesives and Sealants Market, with a 36.7% share. This application covers furniture assembly, appliance mounting, and structural joining tasks in residential settings. Moreover, increased home renovation activity directly supports demand for high-strength bonding solutions across wood, metal, and plastic substrates.

Sealing and Gasketing applications address weatherproofing, water resistance, and air sealing in residential construction. Silicone, polyurethane, and acrylic sealants serve bathroom, kitchen, window, and door sealing tasks. Additionally, growing focus on energy-efficient building envelopes strengthens demand for high-performance sealants in both new construction and retrofit applications.

Repair and Maintenance represents a high-frequency application driven by ongoing household upkeep needs. Consumers use adhesives and sealants for crack filling, leak repair, surface restoration, and hardware fixes. Consequently, the accessibility of retail adhesive products through e-commerce and hardware stores supports consistent demand from cost-conscious homeowners performing their own maintenance tasks.

Sound and vibration-damping applications use specialized adhesive films and compounds to reduce noise transmission in walls, floors, and automotive interiors. This segment benefits from growing consumer awareness of acoustic comfort in residential spaces. Therefore, adhesive manufacturers develop targeted damping solutions to address noise control requirements in modern home construction projects.

Decorating and Finishing and Others round out the application landscape with crafting, hobby, and specialty bonding needs. Decorative adhesives support tiling, wallpaper, and ornamental installations. However, this segment remains fragmented, with demand driven by seasonal trends, social media DIY inspiration, and the growing popularity of home improvement culture among younger consumers.

Key Market Segments

By Product Type

- Pressure-sensitive Adhesives

- Anaerobic Adhesives and Sealants

- Epoxy Adhesives and Sealants

- Polyurethane Adhesives and Sealants

- Acrylic Adhesives and Sealants

By Substrate

- Wood

- Metal

- Plastic

- Glass

- Ceramic

- Paper

- Concrete

By Application

- Bonding and Assembly

- Sealing and Gasketing

- Repair and Maintenance

- Sound and Vibration Damping

- Decorating and Finishing

- Others

Emerging Trends

Water-Based Formulations and Multi-Purpose Solutions Reshape Household Adhesive Demand

Regulatory pressure on solvent-based products accelerates the shift toward water-based adhesive formulations across global markets. Consumer preferences for safer indoor products further reinforce this transition toward low-emission bonding solutions for DIY applications. Bostik generated €2.7 billion in total revenue in 2024, reflecting the commercial scale of adhesive innovation in construction and consumer markets.

Multi-purpose adhesives gain traction among DIY users who prefer single products capable of bonding multiple substrate types. Brands respond by developing versatile formulations that bond wood, plastic, metal, and ceramic without specialized primers. Additionally, these products reduce the need for consumers to stock multiple adhesive types, simplifying home repair supply management.

Health and safety awareness drives rising demand for low-toxicity adhesive and sealant products in residential markets. Consumers increasingly examine product labels for hazardous chemical content before purchasing. Consequently, manufacturers invest in reformulation to eliminate harmful components while maintaining bond performance, positioning non-toxic solutions as a key product differentiation strategy.

Drivers

Rising Home Renovation Activity and Sustainable Product Demand Drive Adhesives and Sealants Market Growth

Home renovation activity surges globally as homeowners invest in upgrades to increase property value and reduce maintenance costs. E-commerce platforms make professional-grade adhesives and sealants accessible to a broader consumer base. Moreover, cost savings from DIY repairs versus professional services encourage more households to purchase bonding products for independent use.

- Demand for sustainable and low-VOC adhesives grows as environmental awareness influences purchasing decisions among DIY consumers. Homeowners prioritize eco-friendly formulations for interior projects to protect indoor air quality. 3M reported full-year revenue of $24.6 billion in 2024, with its Safety and Industrial segment, including adhesives, contributing approximately 44.76% of consolidated revenues.

Urbanization drives household maintenance and decoration needs across developing markets in Asia, Africa, and Latin America. Rising urban populations increase the number of residential units requiring regular upkeep and periodic renovation. Therefore, expanding middle-class consumer bases in emerging economies represents a significant and growing demand source for household adhesive and sealant products.

Restraints

Raw Material Volatility and Environmental Regulations Create Challenges for Adhesive Manufacturers

Fluctuating prices of key raw materials such as petrochemicals, resins, and specialty polymers directly impact manufacturing costs for adhesive and sealant producers. Price volatility reduces profit margins and complicates cost planning for both large manufacturers and smaller regional producers. Moreover, supply chain disruptions amplify these pressures, making consistent pricing and product availability difficult to maintain.

Stringent environmental regulations in Europe, North America, and parts of Asia restrict the use of specific chemicals in adhesive formulations. Compliance with VOC limits, REACH standards, and hazardous substance directives requires significant reformulation investment. Consequently, smaller manufacturers face disproportionate compliance costs, potentially limiting their ability to compete against well-resourced global adhesive brands.

Consumer awareness of chemical hazards occasionally triggers hesitation toward adhesive products perceived as unsafe or toxic. Negative perceptions around solvent-based formulations slow adoption in health-conscious households. However, manufacturers actively address this challenge through transparent labeling, safety certifications, and the development of low-toxicity product lines designed to rebuild consumer confidence in household bonding solutions.

Growth Factors

Bio-Based Innovation, Emerging Market Expansion, and Smart Packaging Accelerate Adhesives Market Development

Bio-based adhesive development gains momentum as eco-conscious consumers and sustainability mandates shape product innovation strategies. Bio-based products attract premium pricing among environmentally aware buyers, improving revenue quality for innovating brands. Sika AG generated CHF 11,763.1 million in total revenue in fiscal 2024, demonstrating the financial scale of companies driving adhesive technology advancement.

- Emerging markets in Southeast Asia, Latin America, and Sub-Saharan Africa present high-growth opportunities for household adhesive expansion. Rising disposable incomes and growing DIY culture fuel demand for consumer-grade bonding solutions in these regions. Additionally, Pidilite Industries reported revenue of approximately ₹139.26 billion in 2025, illustrating the commercial potential of adhesive markets in fast-growing economies.

Portable and user-friendly packaging innovations make adhesive products more convenient for occasional DIY users. Single-use cartridges, precision-tip applicators, and pre-measured dispensing formats reduce waste and improve application accuracy. Therefore, packaging innovation acts as a growth lever by lowering the skill barrier for household consumers attempting repairs and improvement projects independently.

Regional Analysis

Asia Pacific Dominates the DIY and Household Adhesives and Sealants Market with a Market Share of 34.5%, Valued at USD 4.9 Billion

Asia Pacific leads the global DIY and household adhesives and sealants market with a dominant share of 34.5%, valued at USD 4.9 billion. Rapid urbanization, a large construction base, and expanding middle-class populations in China, India, and Southeast Asia fuel strong regional demand. Moreover, rising DIY culture and growing retail infrastructure across the region sustain robust consumption of household bonding and sealing products.

North America represents a mature and innovation-driven market for adhesives and sealants, anchored by high residential renovation spending and strong retail distribution networks. The United States leads regional demand, supported by an active home improvement culture and widespread DIY participation. Additionally, demand for low-VOC and sustainable formulations accelerates product development across consumer and professional segments in the region.

Europe maintains a significant share in the global adhesives and sealants market, driven by stringent environmental regulations and strong demand for high-performance, compliant formulations. Germany, France, and the UK lead regional consumption, particularly for construction-grade sealants and renovation adhesives. Consequently, regulatory frameworks continue shaping product innovation toward safer, greener, and more sustainable bonding solutions across European markets.

Latin America presents growing opportunities for household adhesives and sealants, supported by rising homeownership rates and expanding DIY product distribution in Brazil and Mexico. Urban population growth increases demand for residential maintenance and repair products across the region. Therefore, multinational adhesive brands increasingly focus on affordable product lines designed to capture price-sensitive consumers in Latin American emerging markets.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Henkel holds a leading position in the global adhesives and sealants industry through its Adhesive Technologies division. The company serves construction, automotive, electronics, and consumer DIY markets with a broad portfolio of branded solutions. Moreover, Henkel’s strong distribution network and continuous investment in sustainable formulation technology reinforce its competitive advantage across developed and emerging markets worldwide.

3M operates across multiple adhesive and sealant categories through its Safety and Industrial segment, serving professional and consumer markets globally. The company’s strength lies in advanced material science capabilities and a diversified product portfolio spanning tapes, structural adhesives, and specialty sealants. Additionally, 3M’s innovation pipeline consistently delivers differentiated solutions that address evolving end-user performance and sustainability requirements.

Sika focuses on construction-grade adhesives, sealants, and chemical systems for residential and commercial building applications. The company maintains a strong global footprint through local production and distribution across more than 100 countries. Furthermore, Sika’s acquisition strategy expands its product range and geographic coverage, strengthening its position in the high-growth Asia Pacific and emerging market segments.

Bostik specializes in smart adhesive technologies for construction, industrial, and consumer markets, operating as part of the Arkema Group. The company invests in innovation across pressure-sensitive adhesives, elastic bonding, and waterproofing sealant systems. Consequently, Bostik’s focus on high-performance and sustainable product development positions it competitively within the growing DIY and professional construction adhesives market globally.

Top Key Players in the Market

- Henkel

- 3M

- Sika

- Bostik

- Loctite

- Gorilla Glue

- Dap

- Titebond

- Elmer’s

Recent Developments

- In 2025, Henkel will focus on sustainability, product innovation, and facility expansions in the adhesives and sealants sector. Henkel introduced next-generation cardboard cartridges for improved user experience and sustainability, starting with a roll-out in Europe for sanitary and multi-purpose silicone sealants.

- In 2025, 3M updated and launched several epoxy adhesives and tapes for DIY and household applications, emphasizing versatility for bonding materials like metals, plastics, and wood. Updated Scotch-Weld Epoxy Adhesive DP125 series (translucent variants in various sizes), suitable for bonding wood, metal, glass, stone, and plastics in home construction and repairs.

Report Scope

Report Features Description Market Value (2025) USD 14.3 Billion Forecast Revenue (2035) USD 22.5 Billion CAGR (2026-2035) 4.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Pressure-sensitive Adhesives, Anaerobic Adhesives and Sealants, Epoxy Adhesives and Sealants, Polyurethane Adhesives and Sealants, Acrylic Adhesives and Sealants), By Substrate (Wood, Metal, Plastic, Glass, Ceramic, Paper, Concrete), By Application (Bonding and Assembly, Sealing and Gasketing, Repair and Maintenance, Sound and Vibration Damping, Decorating and Finishing, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Henkel, 3M, Sika, Bostik, Loctite, Gorilla Glue, Dap, Titebond, Elmer’s Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  DIY And Household Adhesives And Sealants MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

DIY And Household Adhesives And Sealants MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Henkel

- 3M

- Sika

- Bostik

- Loctite

- Gorilla Glue

- Dap

- Titebond

- Elmer's

Our Clients

- 179690

- February 2026