Global Directed Energy Weapons Market By Technology (High Energy Lasers, High Power Microwaves), By Platform (Airborne, Land, Space And Naval), By Product Type (Lethal And Non-Lethal), By Region and Key Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

- Published date: Dec. 2023

- Report ID: 28278

- Number of Pages: 299

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

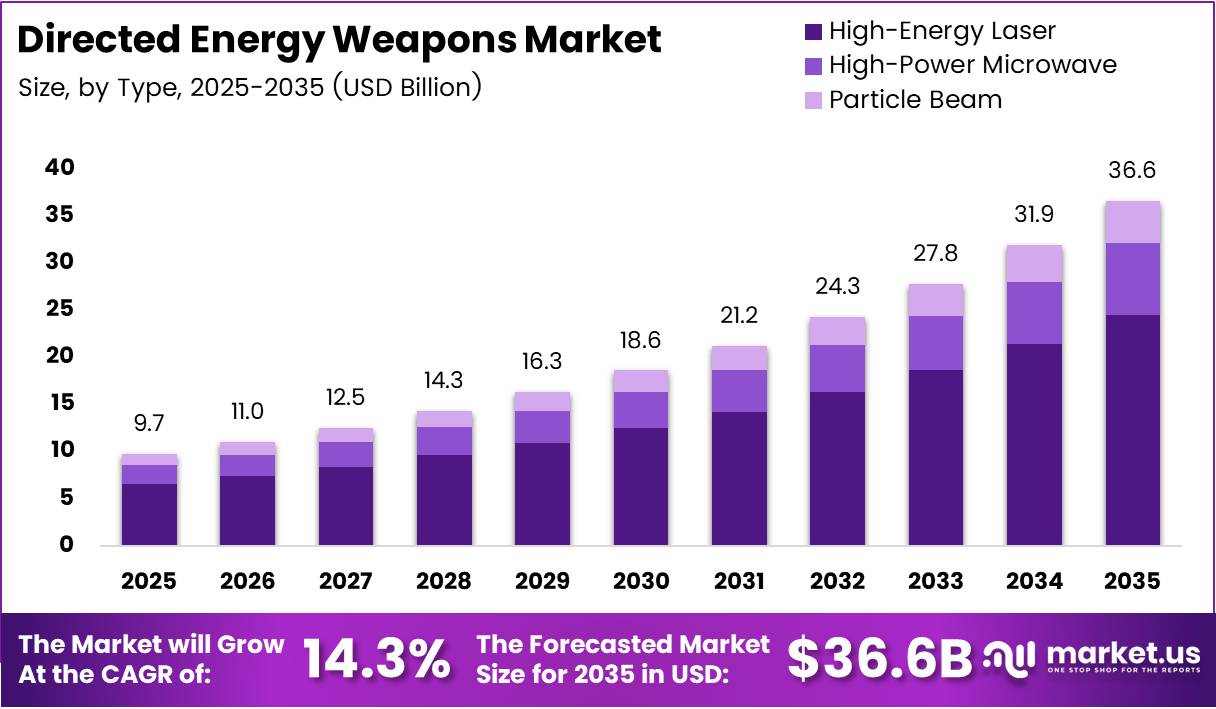

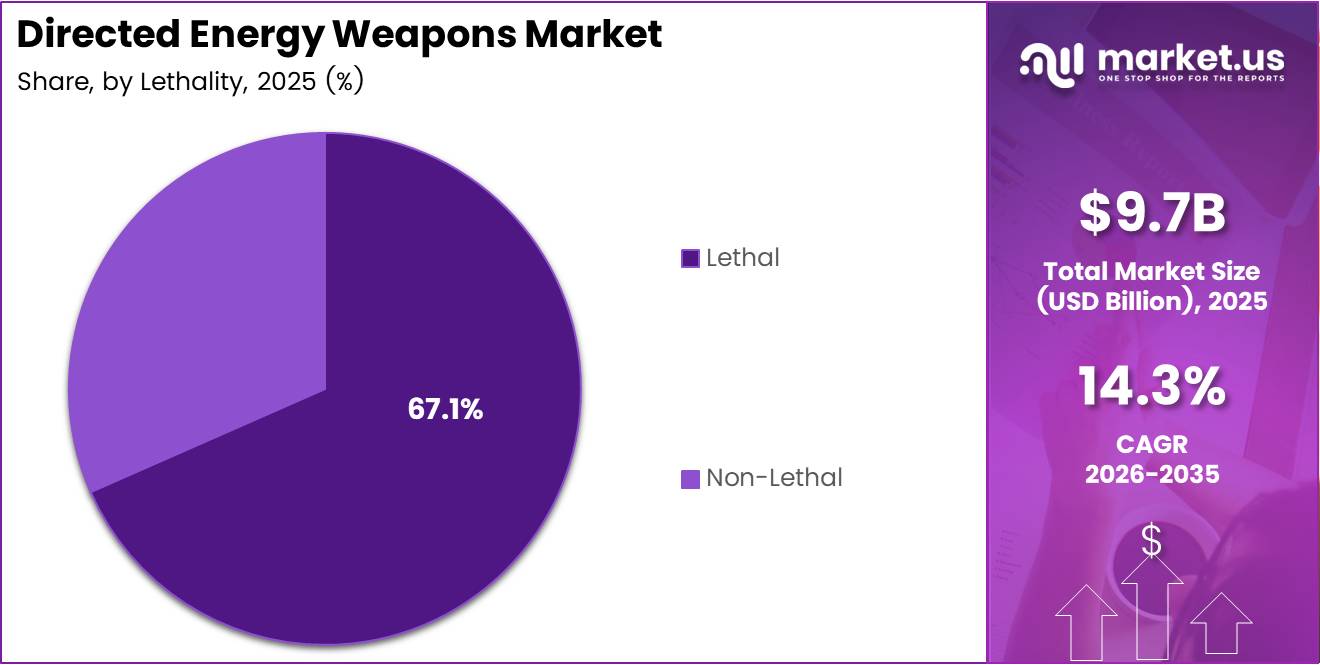

Global Directed Energy Weapons Market size is expected to be worth around USD 36.6 Billion by 2035 from USD 9.7 Billion in 2025, growing at a CAGR of 14.3% during the forecast period 2026 to 2035.

Directed energy weapons use focused electromagnetic energy — high-energy lasers, high-power microwaves, or particle beams — to neutralize targets at the speed of light. Unlike conventional munitions, these systems deliver precision engagement without explosive warheads, reducing collateral risk in contested urban and airspace environments.

The shift from kinetic to directed energy reflects a structural change in modern defense procurement. Militaries worldwide now prioritize systems that can engage multiple threats per power cycle at low cost-per-shot — a capability gap that conventional interceptor-based systems cannot fill at scale against swarm drone threats.

Counter-unmanned aerial system (counter-UAS) requirements have become the primary demand catalyst for this market. Ground forces face an escalating threat from low-cost commercial drones converted for military use, and kinetic interceptors are neither fast enough nor cost-effective enough to counter them at volume. Directed energy fills this operational gap directly.

Defense budget allocations signal sustained government commitment to this technology class. According to a 2025 USI analysis, India’s FY 2025–26 defence budget allocates 149.24 billion rupees specifically for next-generation technologies including directed energy weapons, AI, swarm drones, and hypersonics — within a total defence R&D allocation of 268.16 billion rupees. This concentration of capital in next-generation platforms signals that procurement timelines are compressing, not expanding.

Operational validation is accelerating buyer confidence across allied defense programs. According to a 2025 USI study, India’s Sahastra Shakti Mk-II(A) 30 kW fiber-laser system achieved 100 percent kill probability in April 2025 trials against fixed-wing UAVs, quadcopter swarms, and passive optical surveillance arrays at ranges up to 5 km. Trial results at this confidence level remove the technical uncertainty that previously delayed procurement decisions.

High-energy laser systems lead adoption, with the 51–150 kW power class holding 44.3% of the market by power range. This segment sits at the intersection of engineering feasibility and operational utility — powerful enough to defeat cruise missiles and fast boats, yet compact enough for mobile platform integration.

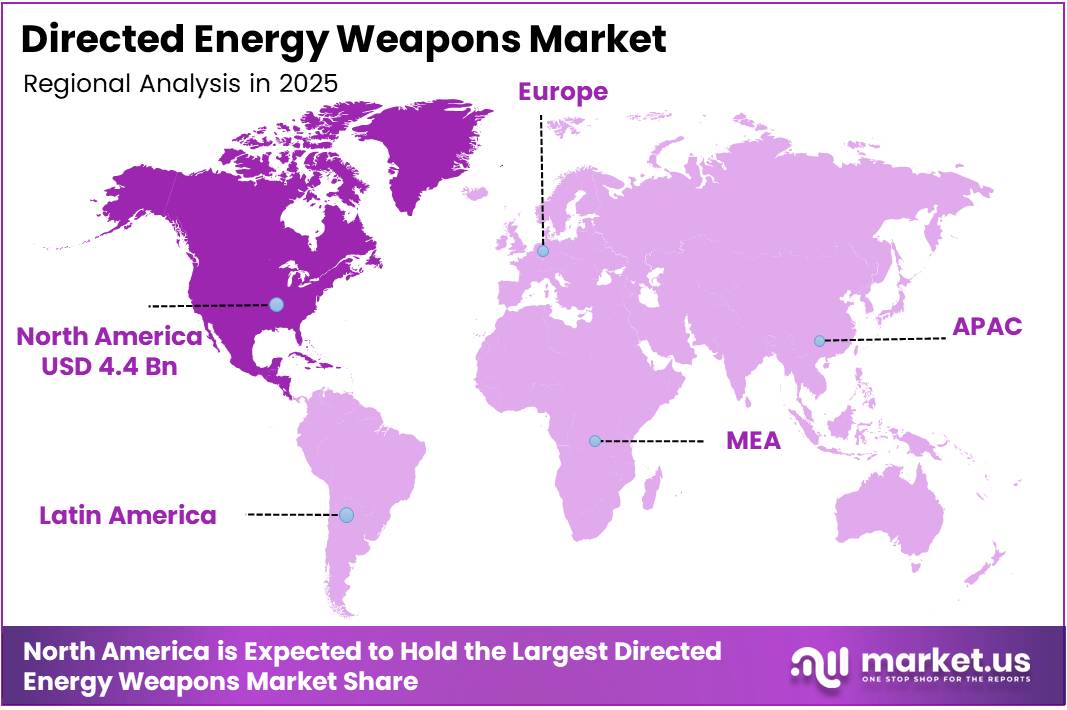

North America holds 45.80% market share at USD 4.4 billion in 2025, supported by the U.S. military’s structured development programs across laser, microwave, and space-based defense applications. As allied nations replicate U.S. procurement frameworks, the technology diffusion path into Europe and the Indo-Pacific is already underway.

Key Takeaways

- The Global Directed Energy Weapons Market was valued at USD 9.7 Billion in 2025 and is forecast to reach USD 36.6 Billion by 2035.

- The market advances at a CAGR of 14.3% during the forecast period 2026 to 2035.

- By Type, High-Energy Laser leads with a 65.8% share, reflecting its dominance in operational and field-tested directed energy applications.

- By Platform, Land-based systems hold 41.6% share, driven by ground force counter-UAS and short-range air defense deployment requirements.

- By Lethality, Lethal systems account for 67.1% of the market, reflecting primary military procurement priorities.

- By Power Class, the 51–150 kW segment holds 44.3% share as the most deployable power range for current operational platforms.

- By End-User, the Army segment leads with 43.2% share, driven by ground-based counter-drone and air defense integration programs.

- North America dominates the regional landscape with a 45.80% share valued at USD 4.4 Billion in 2025.

Type Analysis

High-Energy Laser dominates with 65.8% due to proven combat effectiveness and technology maturity.

In 2025, High-Energy Laser held a dominant market position in the By Type segment of the Directed Energy Weapons Market, with a 65.8% share. Laser systems have advanced from laboratory prototypes to field-deployable weapons, with multiple programs achieving operational status. This maturity makes them the default choice for procurement officers evaluating counter-UAS and missile defense requirements.

High-Power Microwave systems serve a distinct operational role by disrupting electronics rather than physically destroying targets. This non-kinetic mechanism makes microwave weapons especially effective against drone swarms, where a single pulse can disable multiple vehicles simultaneously — an engagement geometry that laser systems cannot replicate at the same cost efficiency. Electronic warfare demand is expanding the addressable market for this segment.

Particle Beam weapons represent the most technically demanding category in this market. These systems accelerate charged particles to near-light speed to deliver damage at molecular level, offering penetration capabilities that photon-based systems cannot match. However, the significant power and infrastructure requirements restrict particle beam development to strategic defense programs and long-horizon R&D investment rather than near-term procurement cycles.

In July 2024, EOS (Electro Optic Systems) unveiled its Apollo high-energy laser system, a roughly 150 kW counter-UAS weapon with 360-degree coverage and battery-powered operation. This product launch illustrates how the laser segment is moving from government R&D into commercial defense catalogs, expanding the buyer base beyond tier-one military programs.

Platform Analysis

Land dominates with 41.6% due to immediate counter-UAS deployment demand from ground forces.

In 2025, Land held a dominant market position in the By Platform segment of the Directed Energy Weapons Market, with a 41.6% share. Ground-based platforms benefit from established power supply infrastructure, lower weight constraints compared to airborne systems, and direct alignment with Army counter-drone priorities. The U.S. Army’s M-SHORAD directed-energy integration program exemplifies the procurement pathway that is pulling land platform spending higher.

Airborne platforms represent the second major deployment environment, where directed energy systems offer persistent area denial without the missile payload limitations of conventional aircraft. Integrating high-energy laser weapons onto aircraft requires overcoming thermal management and power generation constraints at altitude — challenges that current spectral beam-stacking architectures are beginning to resolve. In March 2024, Lockheed Martin received continued funding under the U.S. Missile Defense Agency’s Airborne High Energy Laser program to mature 300 kW-class systems toward deployable airborne configurations.

Naval platforms provide a structurally advantaged environment for directed energy integration. Ships carry dedicated power generation capacity that land vehicles and aircraft cannot match, enabling higher power-class laser and microwave systems to operate sustainably. Naval directed energy systems address anti-ship missile threats and fast-boat swarm scenarios — threat profiles that kinetic close-in weapon systems handle with finite magazine depth.

Space-based directed energy programs occupy the longest development horizon in this market. Orbital platforms would provide global engagement coverage without atmospheric interference, but require solving power generation, pointing accuracy, and treaty compliance challenges simultaneously. Defense agencies in the U.S. and allied nations are funding feasibility studies, signaling intent without near-term procurement commitments.

Lethality Analysis

Lethal dominates with 67.1% due to primary military strike and air defense mission requirements.

In 2025, Lethal systems held a dominant market position in the By Lethality segment of the Directed Energy Weapons Market, with a 67.1% share. Military procurement priorities center on destroying targets — drones, missiles, and fast-attack vehicles — rather than disabling them. The operational requirement for definitive threat neutralization drives lethal system spending to more than two-thirds of total market volume.

Non-Lethal directed energy systems address a different operational requirement: crowd control, perimeter defense, and counter-personnel applications where lethal force carries legal and political costs. These systems find deployment in homeland security, base protection, and peacekeeping roles. However, the procurement volume for non-lethal directed energy remains structurally smaller because military end-users prioritize terminal effectiveness over compliance flexibility.

Power Class Analysis

51 to 150 kW dominates with 44.3% due to optimal balance of lethality and platform integration feasibility.

In 2025, 51 to 150 kW held a dominant market position in the By Power Class segment of the Directed Energy Weapons Market, with a 44.3% share. According to a 2025 USI analysis, systems in the 50–300 kW power range can defeat cruise missiles and swarming fast boats — precisely the threat categories that define current operational requirements. This capability-to-feasibility alignment explains why this power class captures the largest procurement share.

Less than 50 kW systems serve the entry-level tier of directed energy deployment, targeting lightweight UAVs and surveillance assets. The USI 2025 analysis classifies 10–50 kW medium-energy systems as capable of destroying UAVs and disabling warheads. Lower power requirements reduce the thermal and electrical demands on host platforms, making sub-50 kW systems the most accessible entry point for smaller defense forces and mobile tactical units.

Greater than 150 kW systems represent the high-performance tier where missile intercept capability becomes viable. Development in this class focuses on scaling spectral beam-stacking and slab-laser architectures toward continuous-wave output above 300 kW, the threshold identified for higher-end missile defense roles. These programs carry the highest R&D investment per unit and the longest path to operational readiness.

End-User Analysis

Army dominates with 43.2% due to acute short-range drone defense requirements in ground operations.

In 2025, Army held a dominant market position in the By End-User segment of the Directed Energy Weapons Market, with a 43.2% share. Ground forces face the highest frequency of drone threats in active conflict zones, and the Army’s structured directed energy integration programs — including M-SHORAD laser variants — reflect this operational pressure. Army procurement volume signals that land-based counter-UAS is the market’s near-term commercial engine.

Air Force end-users focus directed energy procurement on airborne platforms and fixed-base defense. High-altitude laser integration and runway protection against drone swarms represent the primary Air Force use cases. Development timelines for airborne high-energy laser weapons are longer than ground-based equivalents, but successful integration would create the highest unit-value contracts in this market.

Navy/Coast Guard end-users leverage the power-generation advantages of naval platforms to deploy higher-class laser and microwave systems. Ship-based directed energy provides persistent magazine-depth against missile and fast-boat threats that finite kinetic interceptor supplies cannot guarantee. Naval procurement represents the segment most likely to scale toward greater-than-150 kW deployments within the forecast period.

Homeland Security end-users apply directed energy primarily for perimeter protection, critical infrastructure defense, and counter-UAS at high-value fixed sites. This end-user category favors non-lethal and lower power-class systems that operate within civilian legal frameworks. Budget cycles differ from military procurement, making Homeland Security a slower but structurally growing segment as commercial drone proliferation accelerates threat exposure.

Others encompass research institutions, allied partner defense programs, and emerging national defense forces building directed energy capabilities from the ground up. Bilateral technology transfer agreements and co-development programs increasingly route directed energy procurement through this category, particularly in the Indo-Pacific region where allied force modernization is active.

Key Market Segments

By Type

- High-Energy Laser

- High-Power Microwave

- Particle Beam

By Platform

- Land

- Airborne

- Naval

- Space

By Lethality

- Lethal

- Non-Lethal

By Power Class

- Less than 50 kW

- 51 to 150 kW

- Greater than 150 kW

By End-User

- Army

- Air Force

- Navy/Coast Guard

- Homeland Security

- Others

Drivers

Escalating Drone Threats and Precision Strike Requirements Accelerate Directed Energy Weapons Procurement

Modern militaries face a compound threat environment: low-cost commercial drones converted for weapons delivery, coordinated swarm attacks, and precision guided missiles — all requiring engagement at speed and volume that kinetic interceptors cannot sustain. Directed energy weapons address this gap by delivering engagements at the cost of electrical power rather than expensive munitions.

Counter-UAS demand has reshaped Army procurement priorities. A July 2025 report on U.S. Army live-fire trials confirmed that prototype laser-based M-SHORAD systems engaged alongside kinetic variants to counter swarms of small unmanned aircraft, with the exercise focused on integrating laser weapons into unit procedures including target identification and threat prioritization. This trial confirms that directed energy is transitioning from development to doctrine.

Concurrently, in March 2025, HII’s Mission Technologies division received a contract under an Other Transaction Agreement to develop an open-architecture high-energy laser weapon system prototype for the U.S. Army’s Rapid Capabilities and Critical Technologies Office, targeting counter-UAS protection for Groups 1–3 unmanned aircraft systems. Open-architecture design reduces vendor lock-in, which accelerates procurement timelines by lowering integration risk for procurement officers.

According to a 2025 solid-state laser weapon review, Lockheed Martin’s latest spectral beam-stacking fiber-laser system exceeds 300 kW average power — the highest output the company has delivered to date — with improved efficiency and reduced size and weight. Crossing the 300 kW threshold unlocks missile intercept missions, expanding the addressable market beyond counter-drone into strategic air defense.

Restraints

Power Generation Limits and Environmental Sensitivity Constrain Directed Energy Weapons Operational Readiness

Directed energy systems consume electrical power at rates that exceed the generation capacity of most tactical platforms. Scaling laser output from 50 kW to 300 kW requires not just more powerful generators but also advanced thermal management to prevent beam distortion and hardware degradation — engineering challenges that add cost, weight, and complexity to every deployment configuration.

Atmospheric conditions further limit operational reliability. Fog, dust, smoke, and humidity scatter and absorb laser beams, reducing effective range and kill probability precisely in the contested environments where directed energy systems are most needed. This environmental sensitivity creates performance gaps that procurement planners must account for when designing layered defense architectures.

According to a 2025 USI analysis, typical quick-reaction SAM batteries carry only 6–8 interceptors as first-line ammunition, whereas laser-based directed energy weapons can theoretically fire hundreds of times per power cycle without reloading — provided continuous power and cooling are maintained. That conditional clause — continuous power and cooling — captures the central constraint: the systems that offer the highest tactical advantage are also the most demanding to sustain in the field.

Growth Factors

Ship-Based Laser Programs, Counter-UAS Adoption, and Portable Weapon Development Create Converging Revenue Expansion Paths

Naval directed energy deployments represent one of the highest-value growth vectors in this market. Ships provide dedicated power generation that mobile land platforms cannot match, enabling sustained operation of high-power laser systems above 150 kW. As navies face intensifying anti-ship missile and drone boat threats, ship-based directed energy transitions from experimental capability to operational requirement.

Portable directed energy weapons for tactical ground units open a parallel growth path. Miniaturizing power supplies and thermal management systems to support man-portable or vehicle-portable configurations expands the addressable buyer base from large-platform programs to light infantry and special operations forces. In March 2025, HII detailed that its Army-contracted high-energy laser weapon will be modular, supporting both fixed-site and mobile configurations — a design decision that signals the industry is treating portability as a procurement prerequisite.

According to a 2025 solid-state laser review, U.S. slab-laser prototypes have demonstrated approximately 105 kW output power, with development paths targeting 300 kW-class continuous-wave systems through distributed slab-gain architectures and improved thermal management. Each incremental power milestone unlocks new mission profiles — from disabling UAV electronics at 50 kW to intercepting cruise missiles above 150 kW — structurally expanding the market with each engineering advance.

Emerging Trends

Autonomous Integration, Solid-State Laser Maturation, and Operational Deployment of Air Defense Lasers Define the Market’s Near-Term Direction

Directed energy weapons are entering a new phase where autonomous target acquisition and fire control replace human-in-the-loop engagement. Integrating these systems with autonomous defense platforms reduces response latency to milliseconds — the difference between intercepting and missing a hypersonic or swarm threat. This integration trend shifts competitive advantage toward companies that combine laser hardware with AI-driven battle management software.

Solid-state laser technology is maturing from research programs into deliverable products. Spectral beam stacking — combining multiple wavelength-separated beams into a single high-power output — enables compact architectures that fit on existing military platforms without major structural modifications. This technology path removes one of the primary barriers to widespread adoption: the requirement for purpose-built host platforms.

Operational deployment is now supplanting field testing as the market’s leading indicator. According to a 2025 USI analysis, Israel’s Iron Beam laser neutralized loitering munitions and UAVs within a roughly 10 km engagement envelope during 2024–2025 cross-border operations, demonstrating effectiveness in continuous low-altitude air defense. In March 2025, Rafael Advanced Defense Systems’ CEO confirmed that Iron Beam would achieve operational status during 2025. Combat-proven systems remove procurement hesitation and establish the performance benchmarks that allied programs will now target.

Regional Analysis

North America Dominates the Directed Energy Weapons Market with a Market Share of 45.80%, Valued at USD 4.4 Billion

North America holds 45.80% of the global directed energy weapons market, valued at USD 4.4 billion in 2025. The U.S. military drives this position through structured programs spanning the Army’s M-SHORAD laser integration, the Missile Defense Agency’s airborne high-energy laser initiative, and Navy shipboard directed energy development. Mature procurement infrastructure and dedicated R&D funding streams sustain North America’s lead through the forecast period.

Europe Directed Energy Weapons Market Trends

Europe advances directed energy procurement through national defense modernization programs and NATO interoperability requirements. The continent’s defense industries — particularly in Germany, the UK, and France — invest in laser and high-power microwave systems aligned with counter-drone and base protection missions. European procurement timelines are accelerating as threat assessments from ongoing regional conflicts prioritize short-range air defense investment.

Asia Pacific Directed Energy Weapons Market Trends

Asia Pacific represents the fastest-expanding regional market for directed energy weapons, driven by active development programs in India, China, South Korea, and Japan. India’s FY 2025–26 defence budget allocates 149.24 billion rupees to next-generation technologies including directed energy systems, signaling sovereign capability development rather than import dependence. Regional territorial disputes and drone proliferation create sustained procurement demand across multiple national programs simultaneously.

Middle East and Africa Directed Energy Weapons Market Trends

The Middle East has moved from procurement consideration to operational deployment of directed energy systems. Israel’s Iron Beam program — which achieved combat effectiveness in 2024–2025 operations — represents the region’s leading position in operational directed energy air defense. Gulf states observe these results closely, and procurement interest from Saudi Arabia and the UAE signals that the Middle East will become a structurally significant buyer in the next phase of this market.

Latin America Directed Energy Weapons Market Trends

Latin America remains at an early stage of directed energy weapons adoption, with procurement activity concentrated in Brazil and Mexico where defense modernization programs include surveillance and border protection applications. Budget constraints limit large-scale directed energy acquisitions, but counter-drone requirements at critical infrastructure — ports, energy facilities, and government installations — create a defined entry-level market for lower power-class systems.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Lockheed Martin Corporation occupies the highest-power tier of the directed energy market through its spectral beam-stacking fiber-laser program, which exceeded 300 kW average power output — the threshold required for missile intercept missions. This achievement positions Lockheed as the primary supplier candidate for programs requiring maximum-class laser weapons, creating a structural lead in contracts where power output is the decisive procurement criterion.

RTX Corporation (formerly Raytheon Technologies) applies its integrated defense systems expertise across directed energy, combining high-energy laser development with targeting, fire control, and battle management capabilities. RTX’s strategic advantage lies in offering complete engagement solutions rather than standalone laser hardware — a systems integration approach that aligns with military buyers’ preference for end-to-end platform contracts over component sourcing.

Northrop Grumman Corporation contributes directed energy capabilities through its role in the U.S. Army’s M-SHORAD laser program and related airborne platform integration work. Northrop’s positioning benefits from its existing prime contractor relationships across Army and Air Force platforms, allowing it to insert directed energy components into established program-of-record vehicles rather than competing for standalone laser contracts. This integration pathway reduces procurement friction significantly.

BAE Systems plc develops directed energy weapons within its broader advanced defense electronics portfolio, with particular focus on high-power microwave and laser systems for naval and ground applications. BAE’s cross-Atlantic presence — with operations in the U.S., UK, and Australia — positions it to access procurement programs across multiple allied defense markets simultaneously, providing revenue diversification that pure-play directed energy companies cannot replicate.

Key Players

- Lockheed Martin Corporation

- RTX Corporation

- Northrop Grumman Corporation

- BAE Systems plc

- The Boeing Company

- Rheinmetall AG

- MBDA

- Rafael Advanced Defense Systems Ltd.

- Honeywell International Inc.

- L3Harris Technologies, Inc.

Recent Developments

- April 2025 — India’s Sahastra Shakti Mk-II(A) 30 kW fiber-laser weapon system achieved 100 percent kill probability in live trials against fixed-wing UAVs, quadcopter swarms, and passive optical surveillance arrays at ranges up to 5 km, validating the system for potential operational deployment.

- April 2025 — Lockheed Martin delivered a new 300 kW-class solid-state spectral beam-combined laser as a major technology milestone, positioning its laser product line for transition into next-generation high-energy laser weapon contracts requiring missile-intercept capability.

- March 2025 — Rafael Advanced Defense Systems’ CEO confirmed that the Iron Beam high-energy laser air-defense system would reach operational status during 2025, marking the transition of a combat-tested laser weapon from development program to deployable product.

- July 2025 — U.S. Army live-fire trials confirmed that the Army’s directed energy development focus has shifted from earlier strategic missile-defense concepts toward short-range air defense against low-cost drones, reflecting operational demand for laser and high-power microwave counter-UAS systems.

- April 2024 — Elbit Systems disclosed delivery obligations under the Iron Beam program, committing to truck-mounted high-energy laser units integrated with Rafael’s interceptor-network architecture as part of Israel’s layered air-defense modernization effort.

- December 2025 — EOS marketed its Apollo high-energy laser system as one of the most economical drone-defense solutions available, capable of neutralizing multiple UAVs on a single battery charge — signaling the commercialization of counter-UAS laser technology beyond government R&D programs.

- 2025 (USI Study) — A power classification analysis confirmed that laser systems above 300 kW are being pursued for higher-end missile-defense roles, while 50–300 kW systems can defeat cruise missiles and fast boats, establishing the engineering benchmarks that current procurement specifications are built around.

Report Scope

Report Features Description Market Value (2025) USD 9.7 Billion Forecast Revenue (2035) USD 36.6 Billion CAGR (2026-2035) 14.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (High-Energy Laser, High-Power Microwave, Particle Beam), By Platform (Land, Airborne, Naval, Space), By Lethality (Lethal, Non-Lethal), By Power Class (Less than 50 kW, 51 to 150 kW, Greater than 150 kW), By End-User (Army, Air Force, Navy/Coast Guard, Homeland Security, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Lockheed Martin Corporation, RTX Corporation, Northrop Grumman Corporation, BAE Systems plc, The Boeing Company, Rheinmetall AG, MBDA, Rafael Advanced Defense Systems Ltd., Honeywell International Inc., L3Harris Technologies, Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) Frequently Asked Questions (FAQ)

What are Directed Energy Weapons (DEWs)?Directed Energy Weapons are advanced systems that emit focused energy, such as lasers or microwaves, to target and damage enemy assets. These weapons offer speed-of-light capabilities and are used in various defense applications.

How big is Directed Energy Weapons Market?The Global Directed Energy Weapons Market is likely to secure a valuation of USD 5.8 Billion in 2024, with a CAGR of 19.7% during the forecast period. The global market is anticipated to capture a valuation of USD 12.4 Billion by 2033.

What is driving the growth of the Directed Energy Weapons market?The market is primarily driven by the increasing need for precision and speed in military operations, advancements in technology, and the continuous pursuit of more effective and efficient defense solutions.

What are the key applications of Directed Energy Weapons?DEWs find applications in air and missile defense, counter-drone systems, anti-satellite operations, and other strategic defense initiatives. They are also explored for use in non-lethal capabilities for crowd control and security.

What challenges does the Directed Energy Weapons market face?Challenges include technological hurdles, high development costs, regulatory concerns, and ethical considerations. Integration into existing military infrastructure and addressing potential safety issues are also significant challenges.

Which companies are leading in the Directed Energy Weapons market?Key players in the market include major defense contractors and technology firms such as MBDA, Leonardo S.p.A., RTX, Lockheed Martin Corporation, BAE Systems, Northrop Grumman, Boeing, Rheinmetall AG, QinetiQ, Thales Group

Directed Energy Weapons MarketPublished date: Dec. 2023add_shopping_cartBuy Now get_appDownload Sample

Directed Energy Weapons MarketPublished date: Dec. 2023add_shopping_cartBuy Now get_appDownload Sample -

-

- Lockheed Martin Corporation

- RTX Corporation

- Northrop Grumman Corporation

- BAE Systems plc

- The Boeing Company

- Rheinmetall AG

- MBDA

- Rafael Advanced Defense Systems Ltd.

- Honeywell International Inc.

- L3Harris Technologies, Inc.

Our Clients

- 28278

- Dec. 2023