Global Digital Shipyard Market Size, Share, Growth Analysis Type (Commercial Shipyards, Military Shipyards), Process (Design & Planning, Construction, Maintenance & Repair), Capacity (Large Shipyards, Medium Shipyards, Small Shipyards), Digitalization Level (Fully Digital Shipyard, Semi-Digital Shipyard), Technology (Automation & Robotics, Internet of Things (IoT), Data Analytics & Big Data, Digital Twin Technology, Others), End Use (Shipbuilders & Shipyards, Defense & Military, Ship Owners & Operators, Others), Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 178525

- Number of Pages: 261

- Format:

-

keyboard_arrow_up

Quick Navigation

- Digital Shipyard Market Overview

- Key Takeaways

- Type Analysis

- Process Analysis

- Capacity Analysis

- Digitalization Level Analysis

- Technology Analysis

- End Use Analysis

- Key Market Segments

- Drivers

- Restraints

- Growth Factors

- Emerging Trends

- Regional Analysis

- Key Regions and Countries

- Key Company Insights

- Recent Developments

- Report Scope

Digital Shipyard Market Overview

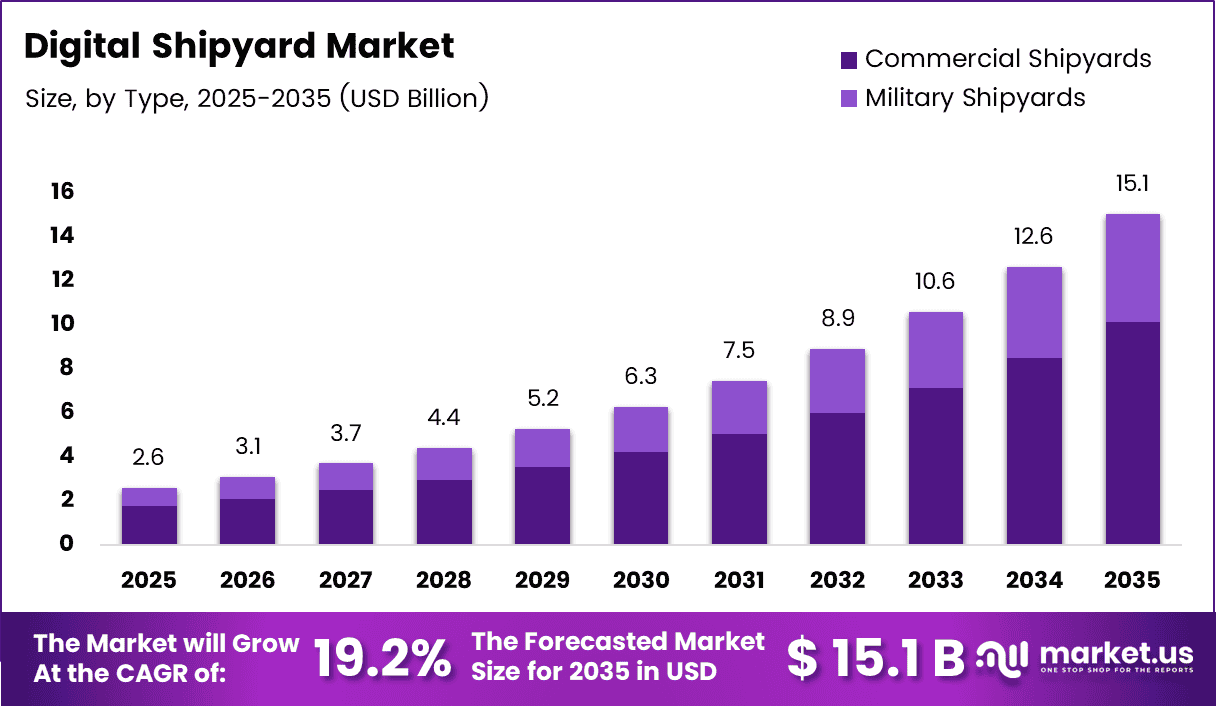

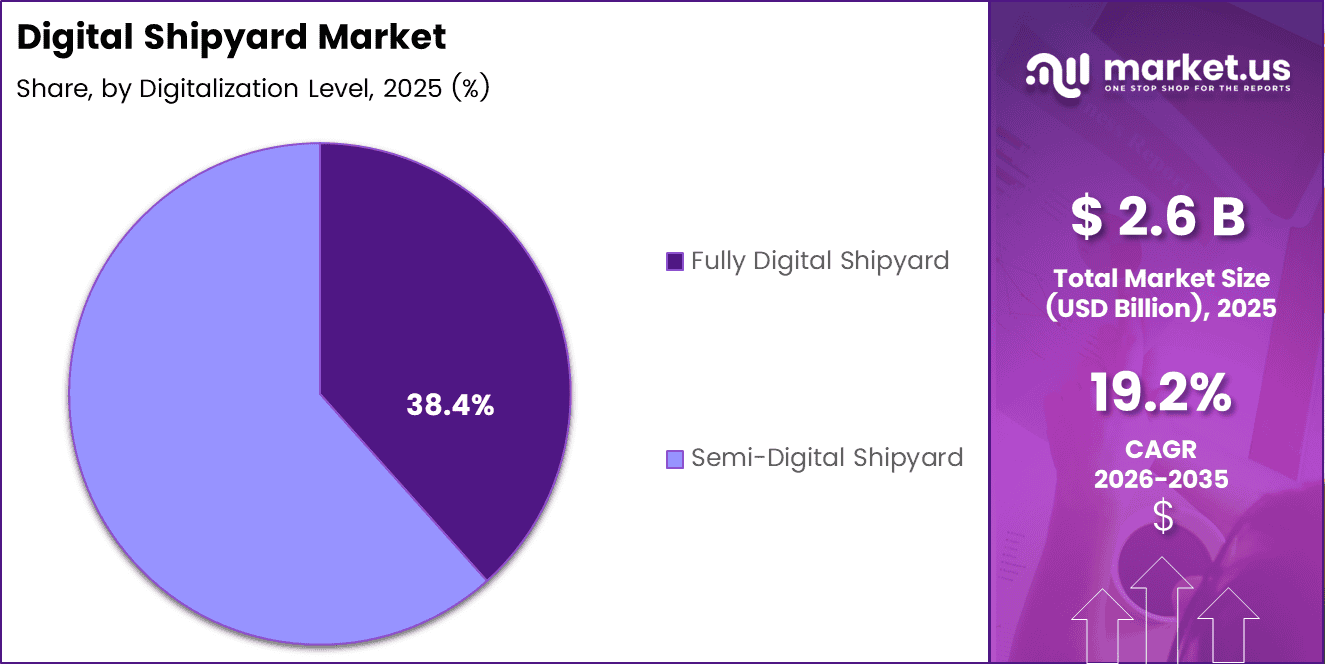

Global Digital Shipyard Market size is expected to be worth around USD 15.1 Billion by 2035 from USD 2.6 Billion in 2025, growing at a CAGR of 19.2% during the forecast period 2026 to 2035.

The digital shipyard market refers to the integration of advanced digital technologies into shipbuilding and repair operations. This includes digital twins, automation, IoT, and data analytics applied across vessel design, construction, and maintenance. Consequently, shipyards are transitioning from traditional workflows to fully connected, data-driven production environments.

Digital shipyards enable real-time monitoring, reduced production errors, and improved lifecycle management of vessels. Moreover, they support better collaboration between engineering teams, suppliers, and clients. This shift is fundamentally changing how both commercial and naval vessels are designed, built, and maintained globally.

Government investment is playing a key role in accelerating market growth. Several maritime nations are funding smart shipbuilding programs and naval modernization initiatives. Additionally, regulatory bodies are encouraging the adoption of digital infrastructure to meet environmental and operational efficiency standards across the global shipping industry.

The market is also driven by rising demand for cost-efficient vessel construction and growing complexity in naval ship design. Defense sectors worldwide are increasing budgets for digital transformation. Therefore, shipyards serving both commercial and military clients are under growing pressure to modernize their production and maintenance capabilities.

Modern warship programs highlight the true scale of digital integration required in today’s shipbuilding environment. According to BAE Systems, a typical warship design involves over 1,800 digital models shared across more than 1,000 engineers and supply chain partners. These models span everything from initial concept and hull design to propulsion simulations and electronic architecture planning.

Moreover, more than 60% of most ship’s components are sourced from the supply chain, covering systems ranging from guns and engines to advanced digital radar platforms. Consequently, digital shipyard platforms must support seamless collaboration across large, geographically distributed teams while maintaining full data integrity and configuration control throughout the vessel lifecycle.

Key Takeaways

- The Global Digital Shipyard Market was valued at USD 2.6 Billion in 2025.

- The market is projected to reach USD 15.1 Billion by 2035, growing at a CAGR of 19.2%.

- By Type, Commercial Shipyards dominated with a 67.3% market share in 2025.

- By Process, Design & Planning led the segment with a 49.6% share.

- By Capacity, Large Shipyards held a dominant position with 49.7% share.

- By Digitalization Level, Fully Digital Shipyard accounted for 38.4% of the market.

- By Technology, Automation & Robotics was the leading segment with a 31.8% share.

- By End Use, Shipbuilders & Shipyards held the largest share at 59.2%.

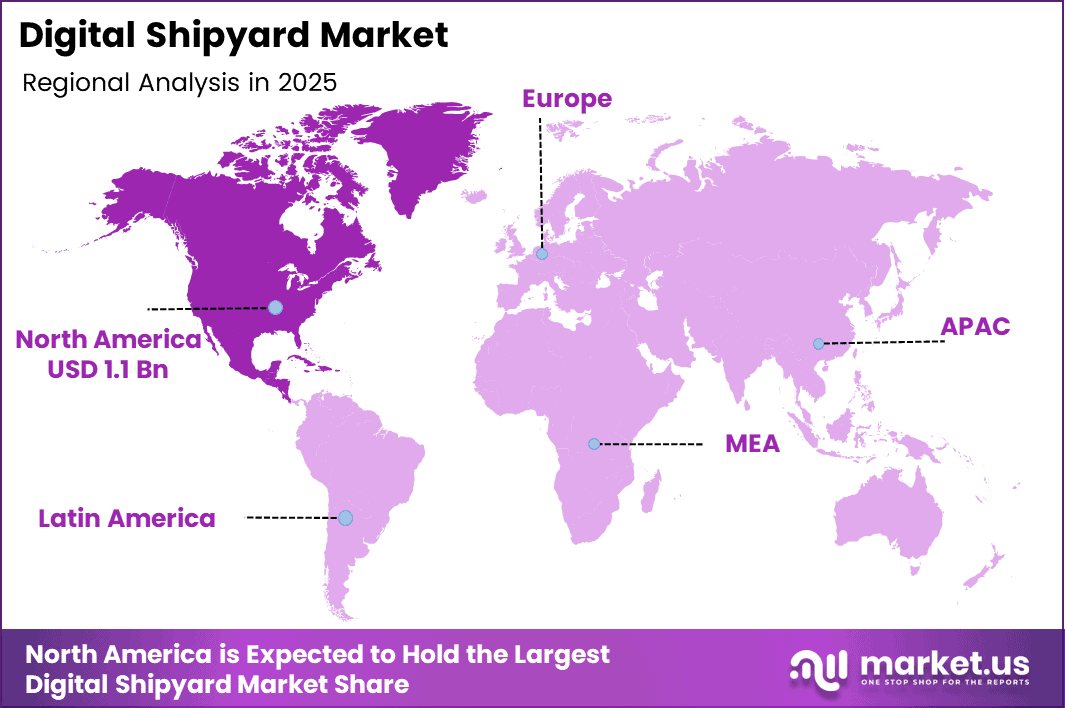

- North America dominated the regional landscape with a 43.70% share, valued at USD 1.1 Billion.

Type Analysis

Commercial Shipyards dominate with 67.3% due to high global vessel production volume and sustained demand for cost-efficient shipbuilding solutions.

In 2025, ‘Commercial Shipyards’ held a dominant market position in the ‘Type’ segment of the Digital Shipyard Market, with a 67.3% share. Commercial shipyards are rapidly adopting digital tools to streamline vessel construction, reduce costs, and meet tight delivery schedules. Consequently, investments in digital twin platforms and automation are highest in this sub-segment.

Military Shipyards represent the remaining share and are growing steadily. Defense modernization programs across North America, Europe, and Asia are driving demand for digital infrastructure in naval facilities. Moreover, military shipyards require highly precise digital tools to manage complex, classified vessel programs with strict lifecycle requirements.

Process Analysis

Design & Planning dominates with 49.6% due to early-stage digital adoption and the critical role of simulation in vessel engineering.

In 2025, ‘Design & Planning’ held a dominant market position in the ‘Process’ segment of the Digital Shipyard Market, with a 49.6% share. Digital tools in this phase enable shipyards to run simulations, reduce design errors, and improve collaboration across engineering teams. Therefore, this segment sees the highest rate of digital twin and CAD software deployment.

Construction is the second key process sub-segment, driven by automation and robotics integration. Shipyards are increasingly using robotic welding and assembly systems to improve precision and speed. Additionally, real-time IoT monitoring during construction is reducing rework and improving overall production efficiency across major shipbuilding facilities.

Maintenance & Repair is gaining traction as ship owners seek to extend vessel lifespans and reduce dry-dock time. Digital platforms enable predictive maintenance scheduling and remote diagnostics. Moreover, lifecycle data integration is allowing operators to manage fleet health more proactively, reducing unplanned downtime and overall operational costs.

Capacity Analysis

Large Shipyards dominate with 49.7% due to higher capital availability and greater need for end-to-end digital process management.

In 2025, ‘Large Shipyards’ held a dominant market position in the ‘Capacity’ segment of the Digital Shipyard Market, with a 49.7% share. Large facilities build complex naval and commercial vessels requiring advanced digital coordination across multiple departments. Consequently, they lead in adopting digital twin platforms, ERP integration, and automated production systems.

Medium Shipyards are the second largest capacity sub-segment and are increasingly investing in digital tools. These yards are adopting cloud-based design and planning software to remain competitive. Moreover, government-backed smart shipbuilding programs in several countries are offering financial incentives to support digitalization in medium-scale operations.

Small Shipyards face higher barriers to adoption but represent a growing opportunity. As software costs decline and cloud solutions become more accessible, smaller facilities are beginning to integrate IoT and analytics tools. Additionally, modular digital solutions designed for limited budgets are helping small yards gradually improve their operational efficiency.

Digitalization Level Analysis

Fully Digital Shipyard dominates with 38.4% due to greater efficiency gains and long-term cost savings from complete digital integration.

In 2025, ‘Fully Digital Shipyard’ held a dominant market position in the ‘Digitalization Level’ segment of the Digital Shipyard Market, with a 38.4% share. Fully digital facilities operate with integrated platforms covering design, production, maintenance, and supply chain. Therefore, they deliver higher throughput, lower error rates, and better lifecycle visibility compared to partially digitized operations.

Semi-Digital Shipyard facilities represent the majority of current global capacity and are transitioning toward full digitalization. Many of these yards have adopted digital tools in select departments while legacy systems remain in others. Consequently, they present a significant near-term upgrade opportunity and are expected to drive sustained market growth through the forecast period.

Technology Analysis

Automation & Robotics dominates with 31.8% due to its direct impact on production speed, safety, and output precision.

In 2025, ‘Automation & Robotics’ held a dominant market position in the ‘Technology’ segment of the Digital Shipyard Market, with a 31.8% share. Robotic welding, material handling, and inspection systems are reducing manual labor requirements while improving accuracy. Consequently, shipyards with high automation rates are achieving significantly better throughput and quality benchmarks.

Internet of Things (IoT) is the second most widely deployed technology in digital shipyards. IoT sensors enable real-time monitoring of equipment, environmental conditions, and production workflows. Moreover, yard-wide connectivity allows operations teams to respond faster to issues and optimize resource utilization across facilities.

Data Analytics & Big Data tools are enabling shipyards to derive actionable insights from large production datasets. These platforms support quality control, scheduling optimization, and predictive maintenance planning. Additionally, integration with ERP systems allows shipyard managers to align production data with procurement and delivery timelines more effectively.

Digital Twin Technology allows shipyards to create virtual replicas of vessels and facilities for simulation and planning. This reduces design-to-build cycle times and enables early identification of engineering issues. Furthermore, digital twins are increasingly used throughout the vessel lifecycle for maintenance forecasting and operational optimization.

Others in this segment include augmented reality, cloud platforms, and AI-based planning tools. These emerging technologies are being piloted by leading shipyards globally. Moreover, their growing maturity is expected to contribute meaningfully to market expansion during the forecast period.

End Use Analysis

Shipbuilders & Shipyards dominate with 59.2% due to direct adoption of digital platforms within core shipbuilding operations.

In 2025, ‘Shipbuilders & Shipyards’ held a dominant market position in the ‘End Use’ segment of the Digital Shipyard Market, with a 59.2% share. As primary adopters, shipbuilders are deploying digital tools across every phase of the production lifecycle. Consequently, this segment drives the highest technology investment and leads overall market demand.

Defense & Military end users are increasing digital infrastructure spending as part of broader naval modernization programs. Governments are prioritizing secure, integrated digital platforms for managing classified shipbuilding projects. Moreover, rising geopolitical tensions are accelerating procurement of next-generation naval vessels, further boosting demand in this sub-segment.

Ship Owners & Operators are adopting digital tools primarily for maintenance, repair, and fleet performance monitoring. Remote diagnostics and predictive analytics help operators minimize downtime and optimize fuel consumption. Additionally, lifecycle data platforms are improving long-term asset management and reducing unplanned maintenance costs across global fleets.

Others in this segment include port authorities, classification societies, and maritime technology vendors. These stakeholders are integrating digital shipyard data into broader maritime logistics and compliance frameworks. Furthermore, collaboration between shipyards and these entities is enabling more seamless digital information exchange across the entire maritime value chain.

Key Market Segments

By Type

- Commercial Shipyards

- Military Shipyards

By Process

- Design & Planning

- Construction

- Maintenance & Repair

By Capacity

- Large Shipyards

- Medium Shipyards

- Small Shipyards

By Digitalization Level

- Fully Digital Shipyard

- Semi-Digital Shipyard

By Technology

- Automation & Robotics

- Internet of Things (IoT)

- Data Analytics & Big Data

- Digital Twin Technology

- Others

By End Use

- Shipbuilders & Shipyards

- Defense & Military

- Ship Owners & Operators

- Others

Drivers

Rising Demand for End-to-End Digital Integration Drives Digital Shipyard Market Growth

The accelerated adoption of digital twin platforms is a primary growth driver for the digital shipyard market. Shipbuilders are using these tools to simulate entire vessel builds before physical production begins. Consequently, errors are reduced significantly, and production timelines are compressed, making digital twin technology a core investment priority for leading shipyards.

Rising demand for cost-efficient and time-bound vessel construction is pushing shipyards to automate and digitize operations. Commercial clients expect faster delivery and lower build costs. Moreover, increasing complexity in both naval and commercial ship designs requires digital tools that can manage thousands of interdependent engineering variables simultaneously and accurately.

Growing focus on lifecycle data integration is further supporting market expansion. Ship owners and operators require complete asset visibility from build to decommission. Therefore, shipyards are investing in platforms that capture and maintain digital records throughout a vessel’s operational life, improving maintenance planning, regulatory compliance, and long-term operational performance.

Restraints

High Capital Investment and Workforce Gaps Restrain Digital Shipyard Market Adoption

High initial capital investment remains one of the most significant barriers to digital shipyard adoption. Deploying advanced digital infrastructure including IoT networks, robotics, and integrated software platforms requires substantial upfront expenditure. Consequently, smaller and mid-sized shipyards often delay or limit digitalization investments due to budget constraints and uncertain return timelines.

The shortage of skilled workers capable of operating and maintaining advanced digital shipyard technologies is a serious restraint. Many existing shipyard workforces are trained in traditional methods and lack expertise in data analytics, automation systems, or digital twin platforms. Moreover, retraining programs are costly and time-consuming, slowing the pace of transformation.

Additionally, the gap between technology availability and workforce readiness creates operational risks during transition periods. Shipyards that invest in digital tools without adequate training programs may face productivity losses. Therefore, addressing the human capital dimension is essential for shipyards seeking to realize the full benefits of digital infrastructure investments.

Growth Factors

Smart Shipbuilding Programs and AI Integration Accelerate Digital Shipyard Market Expansion

The expansion of smart shipbuilding programs in emerging maritime economies presents a major growth opportunity. Countries in Southeast Asia, the Middle East, and Latin America are developing national shipbuilding strategies that prioritize digital infrastructure. Consequently, government-backed initiatives are creating new demand for digital shipyard technologies across previously underpenetrated regional markets.

Integration of AI-driven predictive analytics into ship production planning is improving scheduling, resource allocation, and quality control. Agentic AI tools can identify production bottlenecks and optimize workflows in real time. Moreover, rising defense modernization initiatives globally are directing significant funding toward digital shipyard capabilities, particularly in naval vessel construction and maintenance.

Adoption of cloud-based collaboration tools is enabling shipyards to coordinate design, procurement, and construction activities across geographically dispersed teams. Cloud platforms reduce infrastructure costs and improve data accessibility. Additionally, these tools are supporting better integration between shipyards and their supplier networks, accelerating project timelines and reducing coordination-related delays.

Emerging Trends

IoT Monitoring, Augmented Reality, and Data-Driven Operations Reshape the Digital Shipyard Market

The increasing use of Industrial IoT for real-time yard operations monitoring is one of the most prominent trends in the digital shipyard market. Connected sensors across facilities provide continuous data on equipment status, environmental conditions, and production progress. Consequently, shipyard managers can make faster, more informed decisions that improve both safety and operational efficiency.

Growing implementation of augmented reality for assembly and inspection tasks is transforming how workers interact with complex vessel components. AR overlays provide technicians with real-time guidance, reducing errors and training time. Moreover, the shift toward modular and digitally simulated ship construction is enabling shipyards to pre-build and test vessel sections virtually before physical assembly begins.

Rising adoption of data-driven decision-making is reshaping management practices across global shipyard operations. Analytics platforms are allowing leadership teams to track key performance indicators in real time and respond proactively to production issues. Therefore, shipyards that embed data culture into their operational workflows are achieving measurable improvements in productivity, cost control, and delivery reliability.

Regional Analysis

North America Dominates the Digital Shipyard Market with a Market Share of 43.70%, Valued at USD 1.1 Billion

North America leads the global digital shipyard market, accounting for 43.70% of total market revenue and valued at USD 1.1 Billion in 2025. The region benefits from strong defense spending, advanced manufacturing capabilities, and a well-established base of maritime technology providers. Moreover, U.S. naval modernization programs are directly driving investment in fully integrated digital shipyard platforms.

Europe Digital Shipyard Market Trends

Europe holds a strong position in the digital shipyard market, supported by advanced shipbuilding industries in Germany, France, and Scandinavia. The region’s focus on green shipping regulations and vessel lifecycle management is accelerating digital tool adoption. Additionally, European defense procurement programs are generating steady demand for digitally enabled naval shipbuilding solutions.

Asia Pacific Digital Shipyard Market Trends

Asia Pacific is the fastest-growing regional market, driven by the shipbuilding dominance of South Korea, China, and Japan. These countries collectively account for a large share of global vessel output. Furthermore, investments in automation and digital twin technology at major yards in the region are setting new benchmarks for production efficiency and quality.

Middle East and Africa Digital Shipyard Market Trends

The Middle East and Africa region is at an early but growing stage of digital shipyard adoption. Several Gulf nations are developing maritime infrastructure as part of broader economic diversification strategies. Consequently, new shipyard projects in the UAE and Saudi Arabia are being designed with digital capabilities integrated from the outset.

Latin America Digital Shipyard Market Trends

Latin America presents a moderate growth opportunity in the digital shipyard market. Brazil leads the region due to its offshore oil and gas robotic sector, which drives demand for specialized vessel construction and maintenance services. Moreover, government-backed shipbuilding programs in the region are beginning to incorporate digital infrastructure requirements into new facility development plans.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

ABB is a global leader in electrification, automation, and digital solutions for the maritime and shipbuilding industries. The company provides integrated digital platforms that support vessel design, power management, and yard automation. Moreover, ABB’s expertise in industrial robotics and IoT connectivity makes it a key technology partner for shipyards pursuing end-to-end digital transformation programs worldwide.

Altair Engineering offers advanced simulation and data analytics platforms widely used in ship design and structural analysis. Its software enables shipbuilders to optimize vessel performance and reduce material waste during the design phase. Additionally, Altair’s AI-driven tools support predictive maintenance and lifecycle modeling, helping shipyards improve asset management efficiency across complex, multi-vessel programs.

Aras provides enterprise product lifecycle management software that supports complex engineering workflows in shipbuilding environments. Its platform enables digital thread management, connecting design, production, and maintenance data in a unified system. Consequently, Aras helps shipyards maintain full traceability and configuration control throughout the vessel lifecycle, supporting both commercial and naval program requirements effectively.

BAE Systems is a prominent player in defense-focused digital shipyard solutions, particularly in naval vessel construction and systems integration. The company applies advanced digital engineering, simulation, and virtual testing capabilities to reduce program risk in complex warship builds. Furthermore, BAE Systems’ investments in automation and digital infrastructure position it as a leading contributor to naval shipyard modernization efforts globally.

Key Players

- ABB

- Altair Engineering

- Aras

- BAE Systems

- Dassault Systèmes

- Hexagon

- Honeywell International

- iBase-t

- Schneider Electric (AVEVA)

- Siemens

Recent Developments

- February 2026 – The Shipyard announced a strategic investment in FancyAI, a Generative Engine Optimization platform designed to strengthen brand visibility across AI-powered discovery environments. This makes The Shipyard the first agency to bring patent-pending GEO technology directly to its clients.

- June 2024 – Hanwha completed the acquisition of Philly Shipyard, significantly expanding its global shipbuilding footprint and enhancing its capabilities in the deployment of advanced naval systems across international markets.

- February 2026 – Hapag-Lloyd signed an agreement to acquire ZIM Integrated Shipping Services in a transaction valued at more than USD 4 billion. This deal is expected to reshape the upper ranks of the container shipping sector and reinforce Hapag-Lloyd’s global network reach.

Report Scope

Report Features Description Market Value (2025) USD 2.6 Billion Forecast Revenue (2035) USD 15.1 Billion CAGR (2026-2035) 19.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered Type (Commercial Shipyards, Military Shipyards), Process (Design & Planning, Construction, Maintenance & Repair), Capacity (Large Shipyards, Medium Shipyards, Small Shipyards), Digitalization Level (Fully Digital Shipyard, Semi-Digital Shipyard), Technology (Automation & Robotics, Internet of Things (IoT), Data Analytics & Big Data, Digital Twin Technology, Others), End Use (Shipbuilders & Shipyards, Defense & Military, Ship Owners & Operators, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape ABB, Altair Engineering, Aras, BAE Systems, Dassault Systèmes, Hexagon, Honeywell International, iBase-t, Schneider Electric (AVEVA), Siemens Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- ABB

- Altair Engineering

- Aras

- BAE Systems

- Dassault Systèmes

- Hexagon

- Honeywell International

- iBase-t

- Schneider Electric (AVEVA)

- Siemens

Our Clients

- 178525

- Feb 2026