Quick Navigation

Market Overview

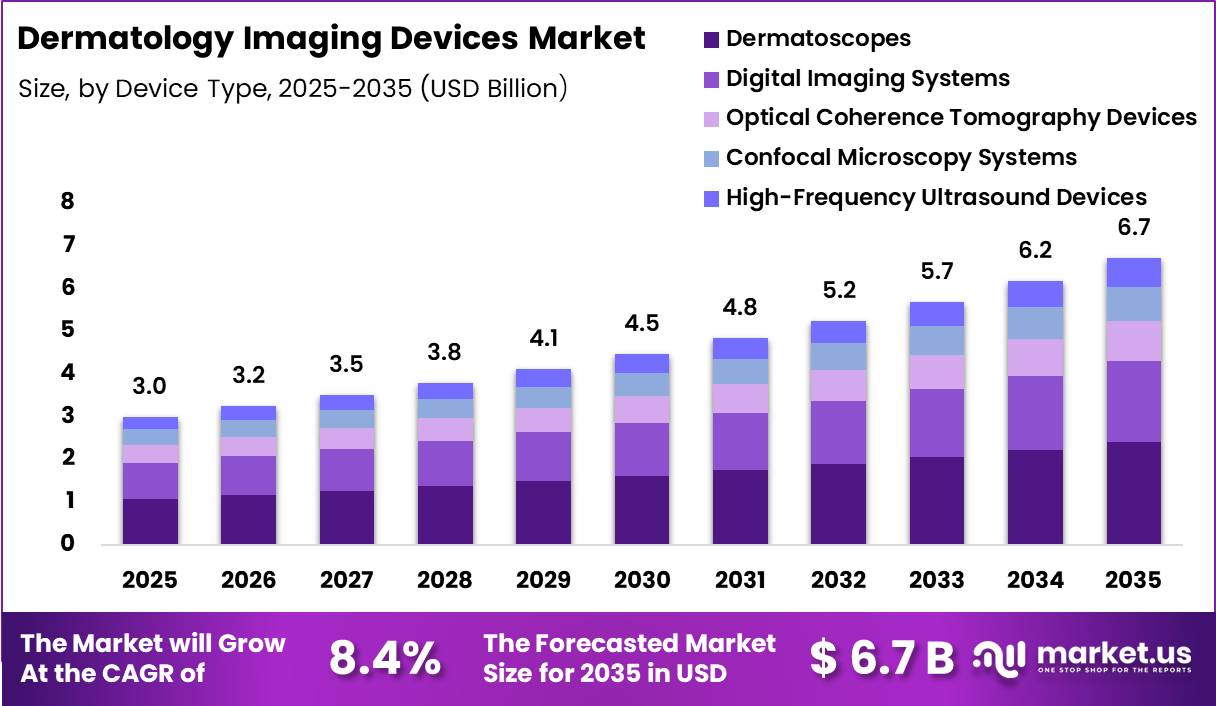

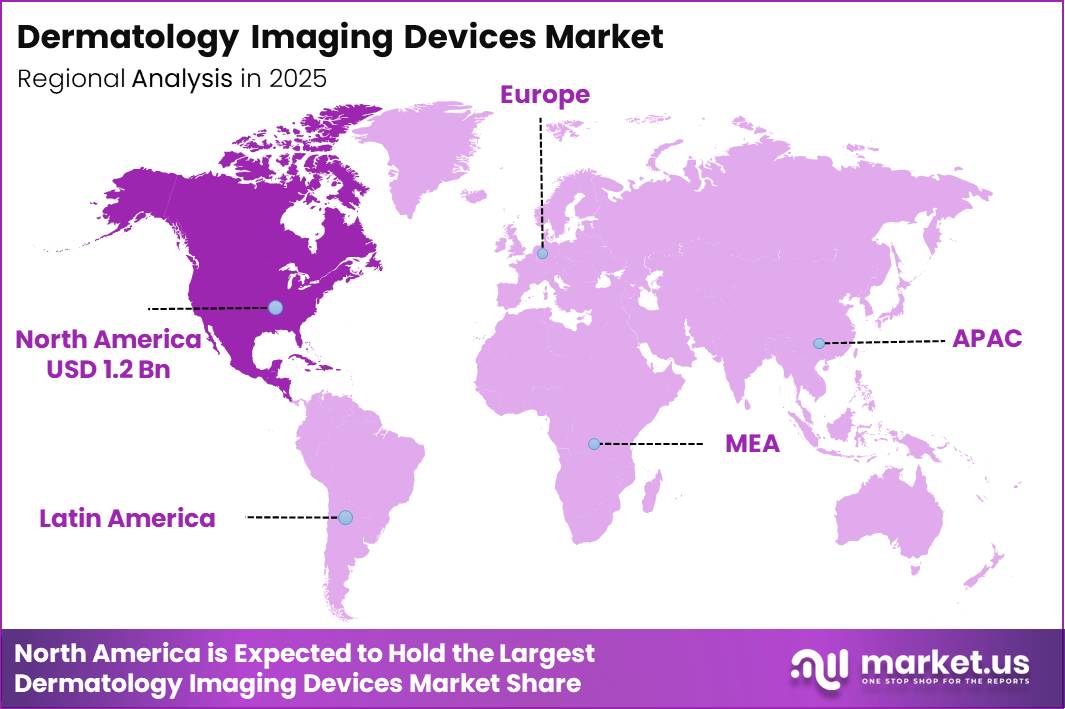

Global Dermatology Imaging Devices Market size is expected to be worth around US$ US$ 6.7 Billion by 2035 from US$ 3.0 Billion in 2025, growing at a CAGR of 8.4% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 40.0% share with a revenue of US$ 1.2 Billion.

Dermatology imaging devices are becoming an increasingly important part of modern skin disease diagnosis and patient management. These technologies, including dermatoscopes, digital imaging systems, optical coherence tomography (OCT), high-frequency ultrasound, confocal microscopy, and AI-assisted imaging platforms, enable clinicians to evaluate skin lesions non-invasively, improve diagnostic accuracy, and monitor treatment outcomes over time. Their adoption is being supported by the growing global burden of skin disorders and continued advances in digital healthcare.

According to the World Health Organization (WHO), skin diseases are among the most common human health conditions worldwide, affecting approximately 1.8 billion people at any given time. In addition, WHO estimates that 2 to 3 million non-melanoma skin cancers and approximately 132,000 melanoma cases occur globally each year, highlighting the importance of early detection and accurate imaging technologies.

The U.S. Food and Drug Administration (FDA) continues to regulate and evaluate innovative medical imaging devices, including advanced optical imaging, diagnostic software, and artificial intelligence-enabled technologies designed to improve dermatological diagnosis while ensuring patient safety and device effectiveness.

Healthcare providers are increasingly integrating digital imaging into routine dermatology practice because it supports earlier identification of suspicious lesions, facilitates longitudinal monitoring, and improves clinical documentation.

Emerging multimodal imaging technologies combine high-resolution visualization with enhanced tissue characterization, enabling more comprehensive skin assessments without invasive procedures. Continued investments in research, regulatory science, and AI-supported diagnostics are expected to accelerate innovation, making dermatology imaging devices an essential component of precision dermatology and future skin cancer screening strategies.

Key Takeaways

- Market Size: Global Dermatology Imaging Devices Market size is expected to be worth around US$ US$ 6.7 Billion by 2035 from US$ 3.0 Billion in 2025

- Market Share: The market is growing at a CAGR of 8.4% during the forecast period from 2026 to 2035.

- Device Type: The Dermatoscopes segment dominated the dermatology imaging devices market in 2025, accounting for 36.00% of the total market share.

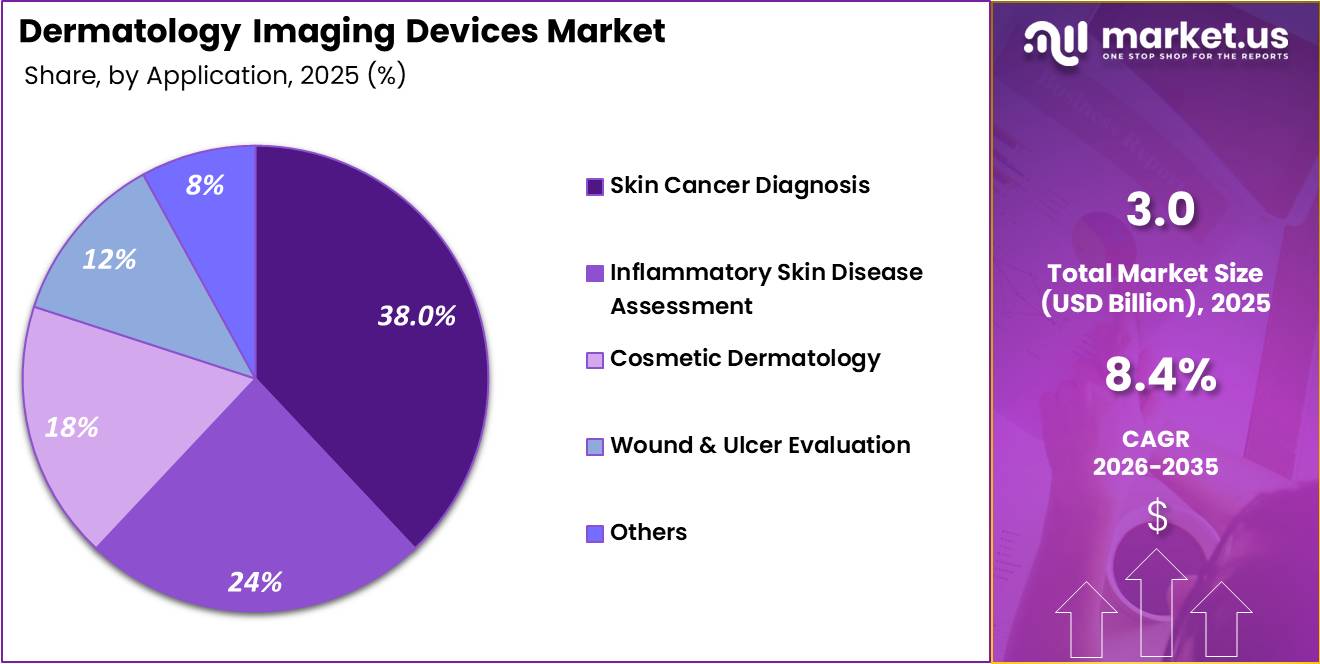

- Application: Skin Cancer Diagnosis leads the application segment with 38.00% market share in 2025.

- Technology: Conventional Imaging dominates the technology segment with 54.00% market share in 2025.

- End User: Hospitals dominate the end-user segment with 41.00% market share in 2025.

- Portability: Standalone systems dominate the portability segment with 62.00% market share in 2025.

- Distribution Channel: Direct sales dominated the dermatology imaging devices market in 2025, capturing 67.00% of the total market share.

- Regional Analysis: In 2025, North America led the market, achieving over 40.0% share with a revenue of US$ 1.2 Billion.

Device Type Analysis

Dermatoscopes Lead Device Type Segment Driven by Early Skin Cancer Detection Demand.

The Device Type segment of the dermatology imaging devices market is led by Dermatoscopes, accounting for 36.00% of the market share in 2025. Their dominance is attributed to widespread clinical adoption for rapid, non-invasive examination of pigmented skin lesions and early melanoma detection.

Dermatoscopes are cost-effective, portable, and easy to integrate into routine dermatology practice, making them indispensable in hospitals, dermatology clinics, and primary care settings. Continuous advancements such as polarized illumination, digital connectivity, and smartphone-compatible dermatoscopes have further improved diagnostic accuracy and accessibility.

Digital Imaging Systems represent 28.00% of the market, driven by increasing demand for high-resolution lesion documentation, treatment monitoring, and teledermatology applications. Optical Coherence Tomography (OCT) Devices, holding 14.00%, are gaining traction for providing cross-sectional skin imaging that supports non-invasive diagnosis of skin cancers and inflammatory disorders.

Confocal Microscopy Systems account for 12.00%, offering near-histological visualization of skin structures and reducing unnecessary biopsies in specialized dermatology centers. High-Frequency Ultrasound Devices, comprising 10.00%, are increasingly utilized for assessing skin thickness, inflammatory conditions, and cosmetic treatment planning.

Growing technological innovations, combined with rising skin disease prevalence and demand for non-invasive diagnostics, continue to drive adoption across all device categories.

Application Analysis

Skin Cancer Diagnosis Dominates Application Segment Due to Rising Incidence and Early Detection Needs.

By application, Skin Cancer Diagnosis dominates the dermatology imaging devices market with 38.00% of the market share in 2025. The segment’s leadership is supported by the increasing incidence of melanoma and non-melanoma skin cancers, alongside growing emphasis on early detection and improved diagnostic precision.

Dermatology imaging technologies enable clinicians to evaluate suspicious lesions non-invasively, reducing unnecessary biopsies while enhancing patient outcomes. Expanding skin cancer screening programs and increasing public awareness further reinforce demand for advanced imaging solutions in oncology-focused dermatology practices.

Inflammatory Skin Disease Assessment accounts for 24.00% of the market, driven by the growing prevalence of chronic conditions such as psoriasis, eczema, and dermatitis that require continuous monitoring and treatment evaluation.

Cosmetic Dermatology contributes 18.00%, supported by rising aesthetic procedures and the need for imaging systems to assess skin texture, pigmentation, wrinkles, and treatment effectiveness. Wound & Ulcer Evaluation, representing 12.00%, is expanding steadily as imaging technologies assist clinicians in monitoring chronic wounds, diabetic ulcers, and tissue healing progression without invasive procedures.

The remaining Others segment, with 8.00%, includes applications such as infectious skin disease assessment, vascular lesion evaluation, and educational research, reflecting the broadening clinical utility of dermatology imaging technologies.

Technology Analysis

Conventional Imaging Holds Leadership in Technology Segment Amid Strong Clinical Adoption.

Based on technology, Conventional Imaging holds the largest share of the dermatology imaging devices market, accounting for 54.00% in 2025. Its dominance is driven by extensive clinical familiarity, affordability, and widespread availability across hospitals and dermatology clinics.

Conventional imaging systems remain the primary choice for routine skin examinations, lesion documentation, and diagnostic evaluations because they provide reliable visualization while requiring relatively low investment compared with advanced technologies. Their established role in daily dermatological practice ensures consistent demand, particularly in healthcare facilities with limited budgets.

Digital Imaging represents the second-largest segment, supported by increasing adoption of high-resolution cameras, image storage capabilities, and teledermatology platforms that facilitate remote consultations and longitudinal monitoring of skin conditions. The ability to capture standardized clinical images significantly improves documentation accuracy and treatment follow-up.

Meanwhile, AI-Assisted Imaging is emerging as the fastest-growing technology segment, fueled by advances in artificial intelligence algorithms capable of supporting lesion classification, melanoma risk assessment, and clinical decision-making.

AI-powered platforms improve diagnostic consistency, reduce interpretation variability, and enhance workflow efficiency. As healthcare providers increasingly adopt digital health technologies, the combination of digital imaging and AI-assisted analysis is expected to accelerate innovation while complementing conventional imaging systems rather than immediately replacing them.

End User Analysis

Hospitals Dominate End User Segment Owing to High Patient Volume and Advanced Infrastructure.

By end user, Hospitals account for the largest share of the dermatology imaging devices market, representing 41.00% in 2025. Their leadership is supported by comprehensive dermatology departments, greater financial capacity to invest in advanced imaging technologies, and increasing patient volumes requiring skin cancer screening, chronic disease management, and surgical planning.

Hospitals also integrate multiple imaging modalities into multidisciplinary care, improving diagnostic accuracy and treatment outcomes. Rising healthcare infrastructure investments and expanding dermatology services continue to strengthen this segment’s market position.

Dermatology Clinics form the second-largest segment, benefiting from growing demand for specialized skin care, cosmetic dermatology procedures, and outpatient diagnostic services. These clinics increasingly adopt portable dermatoscopes, digital imaging systems, and AI-enabled solutions to enhance workflow efficiency and patient satisfaction.

Academic & Research Institutes contribute significantly by utilizing advanced imaging technologies for dermatological research, clinical trials, technology validation, and physician training. Their investments support innovation in non-invasive diagnostic methods and imaging software development.

Diagnostic Centers are also experiencing steady growth as patients seek specialized imaging services without hospital admission. Increasing referrals, expanding preventive skin health programs, and rising awareness of early diagnosis collectively support continued adoption of dermatology imaging devices across all end-user categories.

Portability Analysis

Standalone Systems Dominate Portability Segment Due to High Diagnostic Accuracy and Advanced Imaging Capability.

Based on portability, Standalone Systems dominate the dermatology imaging devices market with 62.00% of the market share in 2025. Their leadership is driven by superior imaging performance, advanced software integration, and the ability to support comprehensive dermatological evaluations within hospitals, specialized clinics, and academic institutions.

Standalone systems often incorporate multiple imaging modalities, high-resolution visualization, and sophisticated image analysis capabilities, making them suitable for complex diagnostic procedures, skin cancer assessment, and research applications. Their compatibility with hospital information systems and electronic medical records further enhances workflow efficiency and long-term patient monitoring.

Portable / Handheld Devices represent the remaining market share and are witnessing rapid adoption due to their convenience, mobility, and expanding role in point-of-care dermatology. Lightweight dermatoscopes, handheld imaging devices, and smartphone-connected systems enable clinicians to perform rapid examinations in outpatient clinics, rural healthcare facilities, and community screening programs.

The increasing popularity of teledermatology, home healthcare services, and mobile diagnostic solutions is further accelerating demand for portable devices. Continuous improvements in image quality, wireless connectivity, cloud-based data management, and artificial intelligence integration are narrowing the performance gap between portable and standalone systems, supporting broader accessibility while complementing established fixed imaging platforms.

Distribution Channel Analysis

Direct Sales Lead Distribution Channel Segment Driven by Strong B2B Healthcare Procurement.

By distribution channel, Direct Sales account for the largest share of the dermatology imaging devices market, representing 67.00% in 2025. Manufacturers primarily utilize direct sales channels to build long-term relationships with hospitals, dermatology clinics, and large healthcare organizations requiring customized product demonstrations, installation, training, and after-sales technical support.

Direct engagement also enables companies to provide integrated service contracts, software updates, and maintenance programs that enhance customer satisfaction and equipment performance throughout the product lifecycle.

Distributors hold 19.00% of the market and play an important role in expanding geographic reach, particularly in emerging economies and regional healthcare markets where manufacturers may have limited direct presence. Their established local networks facilitate product availability, customer support, and regulatory compliance.

Online Procurement, accounting for 14.00%, is steadily expanding as healthcare providers increasingly adopt digital purchasing platforms for standardized medical devices and accessories. Online procurement offers greater pricing transparency, simplified product comparisons, and faster ordering processes, particularly for portable imaging devices and replacement components.

The growing digitalization of healthcare procurement, combined with improvements in e-commerce infrastructure and supply chain efficiency, is expected to strengthen online distribution while direct sales remain the preferred channel for high-value dermatology imaging systems.

Key Market Segments

By Device Type

- Dermatoscopes

- Digital Imaging Systems

- Optical Coherence Tomography (OCT) Devices

- Confocal Microscopy Systems

- High-Frequency Ultrasound Devices

By Application

- Skin Cancer Diagnosis

- Inflammatory Skin Disease Assessment

- Cosmetic Dermatology

- Wound & Ulcer Evaluation

- Others

By Technology

- Conventional Imaging

- Digital Imaging

- AI-Assisted Imaging

By End User

- Hospitals

- Dermatology Clinics

- Academic & Research Institutes

- Diagnostic Centers

By Portability

- Standalone Systems

- Portable / Handheld Devices

By Distribution Channel

- Direct Sales

- Distributors

- Online Procurement

Opportunity

Primary-care AI triage rollout.

This is an opportunity rather than a baseline driver because dermatology imaging is still sold mainly into specialist workflows, while the larger white space sits upstream in primary care where lesion triage volume is materially higher and clinical decision support is only beginning to gain regulatory legitimacy.

The U.S. Food and Drug Administration’s 2024 authorization of DermaSensor for non-dermatologist physicians created a precedent for imaging-assisted triage outside dermatology, and published evidence showed 96% sensitivity across 224 skin cancers plus a reduction in missed skin cancers from 18% to 9%, implying a pathway for imaging vendors to monetize not just hardware but per-scan software, recurring QA subscriptions, and referral-routing integrations.

With 234,680 new melanoma cases projected in the U.S. in 2026 and roughly 9,500 Americans diagnosed with skin cancer each day, even capturing 8% to 10% of first-line suspicious-lesion assessments through reimbursable or capitated triage workflows could add an estimated $180 million to $260 million in annual addressable revenue across devices, software licenses, and consumables in North America alone, while improving clinic throughput by an estimated 15% to 25% through fewer unnecessary dermatology referrals.

Because the category’s current installed base is still disproportionately specialist-centered, this channel expansion represents incremental TAM creation above baseline replacement demand, with the strongest upside accruing to vendors that package handheld imaging, algorithm updates, EHR connectors, and referral analytics into a per-site annual contract model that can lift gross margins by 600 to 900 basis points versus one-time capital sales.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Primary-care AI triage rollout | +2.4% | North America core, EU, Australia | Short term (≤ 2 years) |

| High-risk melanoma monitoring platforms | +1.8% | US, Australia, Nordics, UK | Medium term (2-4 years) |

| Pigmented-lesion imaging for darker skin cohorts | +1.5% | US urban centers, Brazil, GCC, South Africa, India | Medium term (2-4 years) |

| Aesthetic dermatology imaging SaaS | +2.1% | US, EU, South Korea, Japan, GCC | Short term (≤ 2 years) |

| Retail-pharmacy and payer screening channels | +1.7% | US, Canada, UK, Germany | Medium term (2-4 years) |

| Imaging-led oncology pathway integration | +2.0% | US, EU5, Japan | Long term (≥ 4 years) |

Driving Factors

Teledermatology workflow standardization with dermoscopy.

Teledermatology is no longer a temporary access workaround; it is becoming a structured delivery model that depends heavily on image quality.

A 2025 review found diagnostic sensitivity ranging from 41.9% to 100% and specificity from 46% to 90%, but it also concluded that performance depends less on synchronous versus asynchronous format and more on standardized image capture, dermoscopy integration, and protocolized workflows; time to diagnosis was reduced by more than 75% in some programs.

That finding is crucial because it converts imaging devices from optional peripherals into enabling infrastructure for scalable remote triage pathways.From a market standpoint, standardized teledermatology expands demand for portable dermatoscopes, smartphone adapters, secure image-management software, and training bundles.

The value capture is strongest where access gaps are widest rural North America, public European systems under wait-time pressure, and mixed urban-rural networks in emerging markets because the economic benefit comes from reducing unnecessary referrals, compressing time to specialist review, and allowing a higher ratio of triage encounters per dermatologist full-time equivalent. Vendors that package hardware with workflow software, capture protocols, and interoperability support are therefore positioned to outgrow pure device sellers.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skin cancer screening load and lesion volume growth | +2.4% | North America core, Western Europe core, Australia, affluent APAC urban centers | Short term (≤ 2 years) |

| AI-assisted triage moving imaging into frontline care | +2.1% | U.S. core, EU, UK, Nordics, selective APAC corridors | Short term (≤ 2 years) |

| Teledermatology workflow standardization with dermoscopy | +1.7% | North America rural networks, EU public systems, Latin America private chains, India urban-rural hubs | Medium term (2-4 years) |

| 3D total-body photography for high-risk surveillance | +1.5% | U.S. oncology/derm centers, Germany, UK, Netherlands, Australia | Medium term (2-4 years) |

| EU MDR and higher-grade software regulation favoring validated platforms | +1.2% | EU core, UK spill-over, Switzerland, export-oriented manufacturers globally | Medium term (2-4 years) |

| Reimbursement and practice-efficiency pressure favoring earlier digital capture | +1.0% | U.S. core, France, Germany, mixed private-pay Asia | Short term (≤ 2 years) |

Challenge

AI validation burden.

The most persistent operating challenge is not lack of interest in AI-assisted dermatology imaging, but the rising validation workload required to convert image-analysis claims into regulator-ready evidence across changing software versions, care settings, and patient cohorts; the U.S. Food and Drug Administration’s January 2025 draft lifecycle guidance and subsequent 2025–2026.

AI oversight direction push manufacturers toward much heavier documentation around data lineage, bias controls, labeling, postmarket monitoring, and predetermined modification plans, while the U.S. AI-enabled device base has already exceeded 1,250 marketed products, raising the competitive bar for evidence depth and submission quality.

In practical terms, this adds 6 to 12 months to upgrade cycles for lesion-classification or triage software, lifts validation dataset requirements into the tens of thousands of labeled images for multi-phototype robustness, increases cross-site reader study costs by roughly 15% to 25% versus static imaging software programs, and forces firms to maintain parallel clinical, regulatory, and MLOps teams instead of a single premarket project structure.

The resulting friction does not halt current device sales, but it compresses effective innovation velocity, delays feature monetization, and pushes vendors toward longer release calendars, centralized model-governance systems, locked change-control architectures, and earlier regulator engagement as a permanent operating model.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| AI validation burden | -1.4% | North America core, EU regulatory hubs, Japan advanced care systems | Medium term (2-4 years) |

| Dermatologist capacity mismatch | -1.1% | U.S. secondary cities, EU public systems, rural APAC care gaps | Long term (≥ 4 years) |

| Component lead-time volatility | -1.0% | APAC manufacturing bases, North America OEMs, EU device assemblers | Medium term (2-4 years) |

| Cybersecurity lifecycle overload | -0.8% | U.S. connected-device vendors, EU hospital networks, Gulf digital clinics | Medium term (2-4 years) |

| Dataset bias normalization | -0.9% | North America diverse populations, Europe migrant-heavy systems, LATAM mixed-phototype markets | Long term (≥ 4 years) |

| Screening-workflow integration drag | -0.7% | Hospital outpatient chains, multi-site dermatology groups, teledermatology corridors | Short term (≤ 2 years) |

Restraints

Reimbursement compression.

Reimbursement remains a direct constraint because dermatology practices buying imaging systems still underwrite adoption against physician cash flow, lesion documentation throughput, and procedure mix, and those economics tightened after the CY 2025 Medicare Physician Fee Schedule reduced the conversion factor to about $32.35, roughly 2.8 percent below the prior year level under the administration of Centers for Medicare & Medicaid Services.

Even where imaging is bundled into broader visit economics rather than paid as a standalone premium, lower physician fee conversion compresses discretionary capital budgets, weakens ROI thresholds for add-on imaging modules, and makes independent dermatology clinics more likely to stretch refresh cycles from roughly 4 to 6 years toward 6 to 7 years, particularly for high-end digital dermoscopy carts and AI subscription layers.

The commercial effect is most visible in the U.S. outpatient base, where vendors face greater discounting, slower SaaS attach rates, and higher proof-of-value demands tied to biopsy avoidance or workflow savings, justifying a 1.5 percentage point reduction to baseline CAGR in the near term.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI validation burden | -1.8% | North America core, EU, Japan, ANZ | Medium term (2-4 years) |

| Reimbursement compression | -1.5% | U.S. core, selective Canada, private-pay markets | Short term (≤ 2 years) |

| EU compliance overlap | -1.3% | EU, UK-linked compliance chain, EEA | Medium term (2-4 years) |

| Component cost inflation | -1.1% | APAC corridors, U.S. import channels, EU assemblers | Short term (≤ 2 years) |

| Procurement deferral in clinics | -0.9% | North America, Western Europe, urban APAC | Short term (≤ 2 years) |

| Data integration friction | -0.8% | U.S., EU, Gulf hospitals, advanced APAC | Long term (≥ 4 years) |

Regional Analysis

North America Leads Dermatology Imaging Devices Market.

In 2025, North America dominated the Dermatology Imaging Devices Market, accounting for over 40.0% share and generating revenue of US$ 1.2 Billion. The region’s leadership is driven by advanced healthcare infrastructure, early adoption of AI-enabled dermoscopy systems, and high prevalence of skin cancer, particularly melanoma and non-melanoma cases.

Strong reimbursement frameworks and the presence of leading medical imaging manufacturers further support widespread clinical adoption across hospitals, dermatology clinics, and ambulatory surgical centers. Continuous technological innovation and integration of digital imaging with teledermatology platforms also enhance diagnostic efficiency.

Europe held a significant share supported by strong dermatology awareness programs, aging population, and structured skin cancer screening initiatives, particularly in countries such as Germany, the United Kingdom, and France. The region benefits from well-established healthcare systems and increasing adoption of digital imaging solutions in outpatient dermatology practices.

Meanwhile, Asia-Pacific is emerging as the fastest-growing region due to rising healthcare expenditure, expanding hospital infrastructure, growing medical tourism, and increasing awareness of early skin disease detection. Countries like China, Japan, and India are witnessing rapid uptake of advanced imaging devices. Latin America and the Middle East & Africa are gradually adopting dermatology imaging technologies, driven by improving healthcare access and growing private sector investment.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

In 2025, the Dermatology Imaging Devices Market is moderately consolidated, with competition strongly shaped by innovation in AI-assisted diagnostics, high-resolution dermoscopy, and integrated digital workflow solutions. Market players focus on improving early skin disease detection, enhancing imaging precision, and expanding teledermatology capabilities through cloud-based platforms and connected devices.

Strategic R&D investments, collaborations with healthcare providers, and ecosystem-based product development are key competitive approaches. The market is increasingly driven by demand for portable devices, automated lesion analysis, and seamless data integration across dermatology clinics, hospitals, and research centers.

Key players include Canfield Scientific Inc., FotoFinder Systems GmbH, DermLite (3Gen Inc.), Heine Optotechnik GmbH, and Michelson Diagnostics Ltd. Canfield Scientific Inc. leads with advanced total-body imaging systems and AI-powered analytics that support longitudinal patient monitoring and comprehensive skin mapping.

FotoFinder Systems GmbH strengthens its position through AI-assisted mole mapping and teledermatology solutions that enhance remote diagnostics. DermLite (3Gen Inc.) focuses on portable dermatoscopes designed for point-of-care screening, improving accessibility and speed of diagnosis.

Heine Optotechnik GmbH emphasizes high-quality optical dermoscopy instruments known for precision and clinical reliability. Michelson Diagnostics Ltd. advances OCT-based imaging technology, enabling deeper skin layer visualization for complex dermatological assessment. Collectively, these companies drive innovation, strengthen digital integration, and shape the competitive landscape of dermatology imaging worldwide.

Top Key Players

- Canfield Scientific Inc.

- FotoFinder Systems GmbH

- DermLite (3Gen Inc.)

- Heine Optotechnik GmbH

- Michelson Diagnostics Ltd.

- Caliber Imaging & Diagnostics

- GE HealthCare

- Siemens Healthineers

- Leica Microsystems

- Verily Life Sciences

- Cortex Technology

- QuantifiCare S.A.

- Longport Inc.

- Firefly Global

- Dino-Lite (AnMo Electronics Corporation)

Recent Developments

- In April 2025, GE HealthCare announced a multi-year collaboration with Ascension, one of the largest non-profit health systems in the U.S. The agreement focuses on improving diagnostic imaging access, patient safety, workflow efficiency, and quality of care through advanced medical technologies.

- In July 2025, Siemens Healthineers was recognized as the 2025 North America Company of the Year in advanced visualization applications by Frost & Sullivan. The recognition reflects the company’s continued investment in intelligent imaging software, workflow automation, and AI-enabled visualization technologies.

- In October 2025, DermaSensor secured USD 16 million in Series B funding to accelerate commercialization of its FDA-cleared non-invasive skin cancer detection device, bringing total company funding to USD 43 million.

- In July 2025, FotoFinder announced that GHO Capital acquired a majority stake in the company, supporting the expansion of its AI-powered dermoscopy, total body mapping, and skin imaging technologies for dermatology and skin cancer detection.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 3.0 Billion |

| Forecast Revenue (2035) | US$ 6.7 Billion |

| CAGR (2026-2035) | 8.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Device Type (Dermatoscopes, Digital Imaging Systems, Optical Coherence Tomography (OCT) Devices, Confocal Microscopy Systems, High-Frequency Ultrasound Devices), By Application (Skin Cancer Diagnosis, Inflammatory Skin Disease Assessment, Cosmetic Dermatology, Wound & Ulcer Evaluation, Others), By Technology (Conventional Imaging, Digital Imaging, AI-Assisted Imaging), By End User (Hospitals, Dermatology Clinics, Academic & Research Institutes, Diagnostic Centers), By Portability (Standalone Systems, Portable / Handheld Devices), By Distribution Channel (Direct Sales, Distributors, Online Procurement) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Canfield Scientific Inc., FotoFinder Systems GmbH, DermLite (3Gen Inc.), Heine Optotechnik GmbH, Michelson Diagnostics Ltd., Caliber Imaging & Diagnostics, GE HealthCare, Siemens Healthineers, Leica Microsystems, Verily Life Sciences, Cortex Technology, QuantifiCare S.A., Longport Inc., Firefly Global, Dino-Lite (AnMo Electronics Corporation) |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |