Global Demand Response Management System Market Size, Share, And Enhanced Productivity By Technology (Conventional Demand Response, Automated Demand Response), By Services (Curtailment Services, System Integration and Consulting Services, Managed Services, Support and Maintenance), By End-use (Manufacturing, Office and Commercial Buildings, Energy and Power, Agriculture, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: January 2026

- Report ID: 173907

- Number of Pages: 226

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

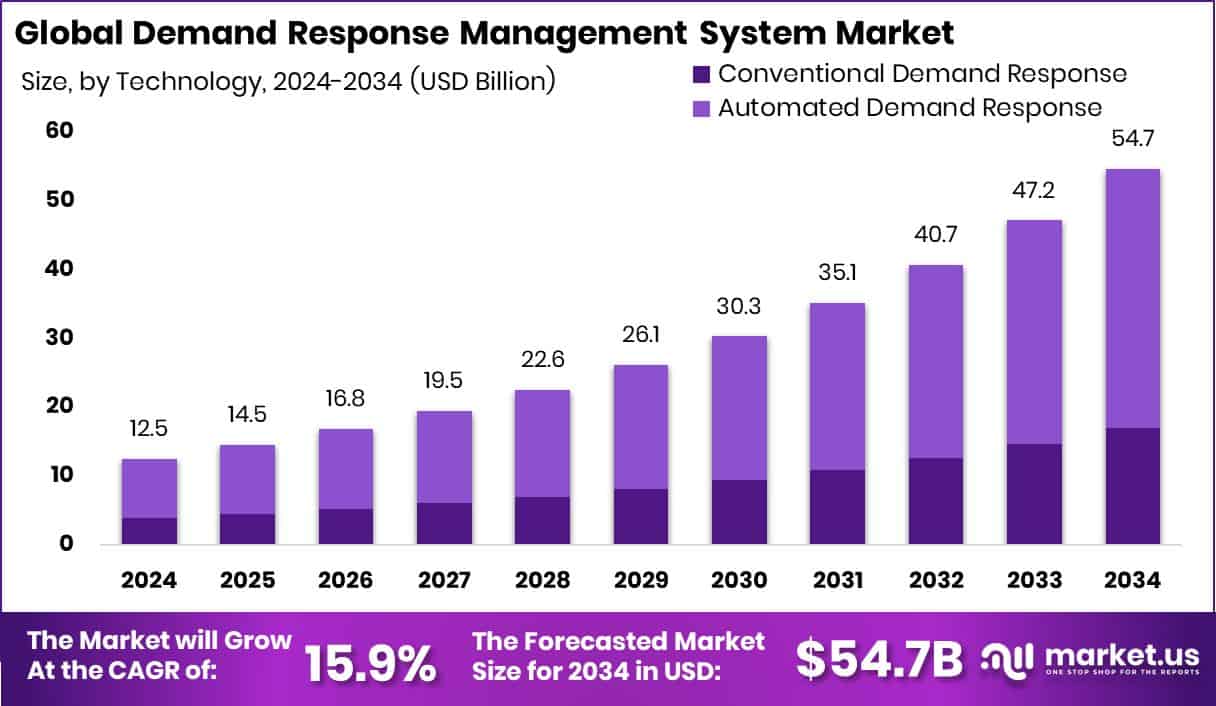

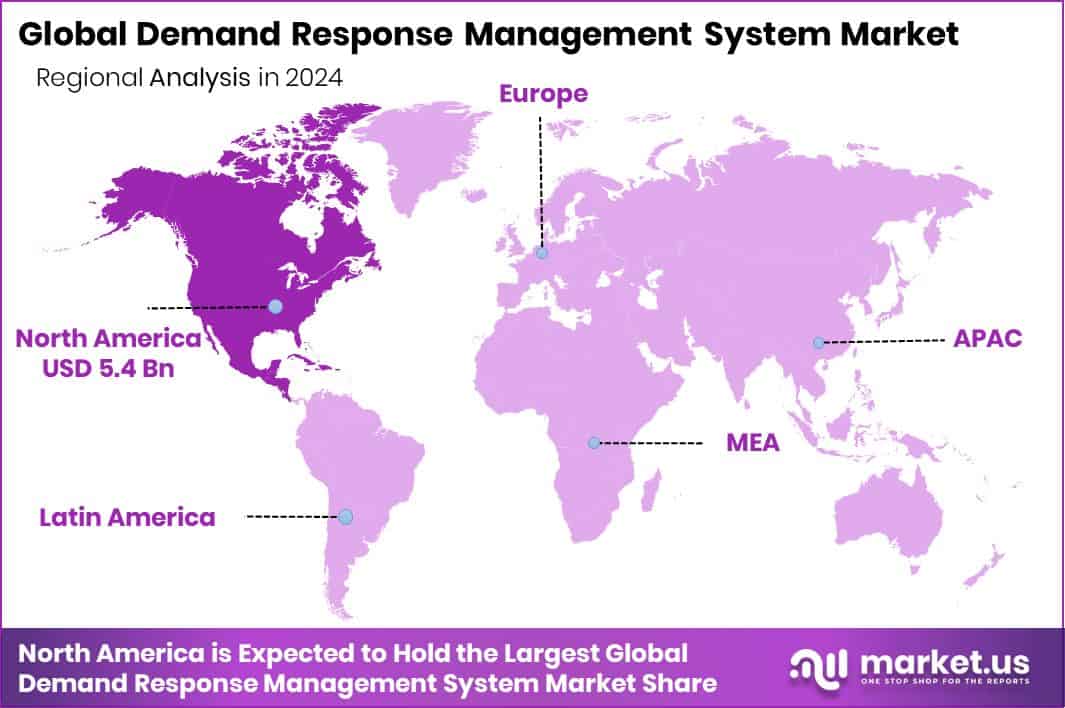

The Global Demand Response Management System Market is expected to be worth around USD 54.7 billion by 2034, up from USD 12.5 billion in 2024, and is projected to grow at a CAGR of 15.9% from 2025 to 2034. Demand Response Management System Market sees North America at 43.5%, USD 5.4 Bn.

A Demand Response Management System is a digital platform that helps utilities and large electricity users manage power consumption during peak demand periods. It works by monitoring real-time electricity use and automatically reducing or shifting non-essential loads when the grid is under stress. This helps prevent outages, lowers energy costs, and improves overall grid reliability without stopping core operations.

The Demand Response Management System Market covers software, control tools, and services that enable organized demand response programs across residential, commercial, and industrial users. As power systems become more complex with renewable energy and storage, these systems play a key role in balancing supply and demand efficiently while supporting grid stability.

Market growth is driven by rising investments in clean energy and grid flexibility. For example, Apraava Energy secured Rs 800-crore funding to strengthen power infrastructure, while Power Capital raised €323M to accelerate renewable energy growth in Ireland. Such investments increase the need for digital tools that can manage variable electricity demand reliably.

Electricity demand is increasing due to urbanization, electrification, and energy-intensive industries. Capital flows such as Nuveen raising $1.3B for energy and power infrastructure and Sharing Energy raising ¥31.5 billion in Series C funding highlight the scale of new energy assets coming online, which require smarter demand control systems.

Future opportunities expand with energy storage and distributed power. The rise of flexible assets is reinforced by Base Power raising $200 million to scale energy storage solutions. As storage, renewables, and digital grids grow together, demand response systems become essential tools for cost control, grid resilience, and sustainable energy management.

Key Takeaways

- The Global Demand Response Management System Market is expected to be worth around USD 54.7 billion by 2034, up from USD 12.5 billion in 2024, and is projected to grow at a CAGR of 15.9% from 2025 to 2034.

- Automated Demand Response led the Demand Response Management System Market with 69.1% share in 2024.

- Managed Services dominated the Demand Response Management System Market, capturing 39.8% share through outsourcing optimization.

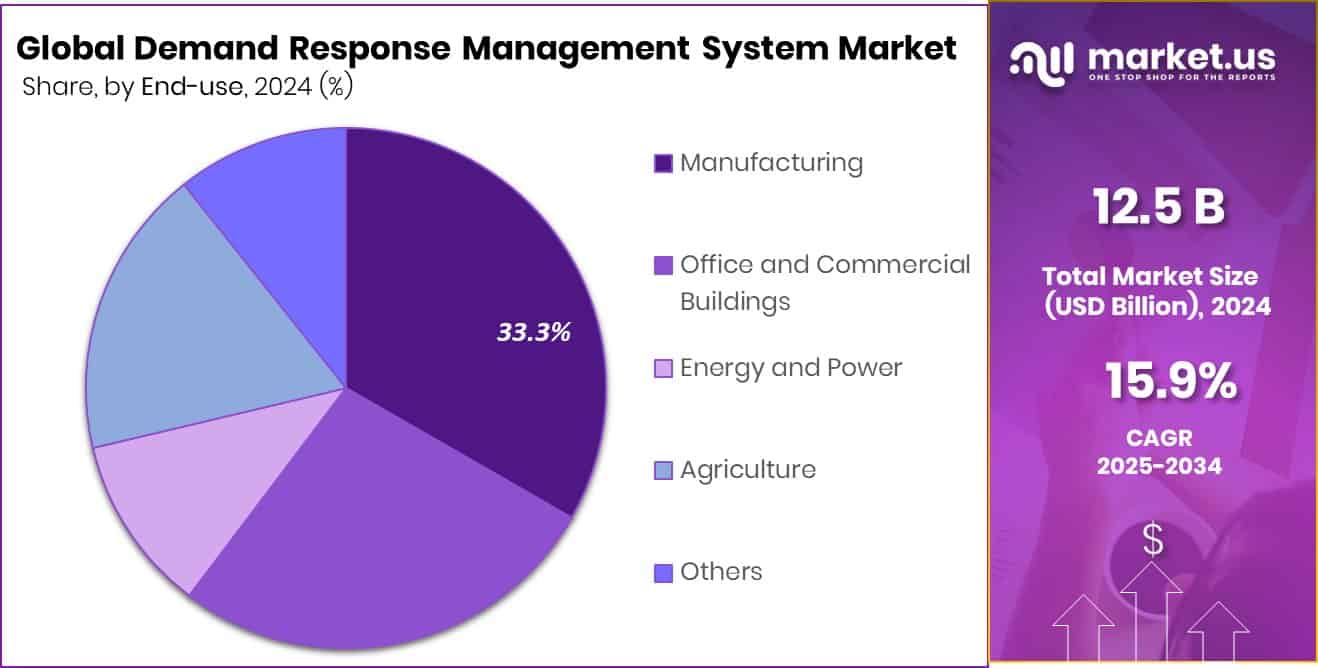

- Manufacturing led end-use adoption in the Demand Response Management System Market with 33.3% share globally.

- North America commands DRMS growth in 2024, holding 43.5% share of USD 5.4 Bn.

By Technology Analysis

Automated Demand Response leads Demand Response Management System Market with 69.1% adoption.

In 2024, Automated Demand Response held a dominant position in the Demand Response Management System Market, capturing 69.1% share as utilities and large energy users moved toward fully automated load control. This technology allows real-time communication between grid operators and connected systems, enabling automatic load reduction or shifting during peak demand periods.

Manufacturing plants, data centers, and commercial buildings increasingly adopted automation to avoid manual intervention, reduce energy costs, and meet grid compliance requirements. The rise of smart meters, IoT-enabled equipment, and AI-based energy platforms further strengthened adoption. Automated systems also improve response accuracy and speed, helping grid operators maintain stability while supporting renewable energy integration and reducing peak-load stress.

By Services Analysis

Managed Services support Demand Response Management System Market, accounting for 39.8% share.

In 2024, Managed Services secured a 39.8% share in the Demand Response Management System Market, reflecting the growing need for expert-led energy management. Many organizations lack in-house expertise to manage complex demand response programs, real-time analytics, and regulatory compliance. Managed service providers handle program enrollment, monitoring, reporting, and optimization, allowing customers to focus on core operations.

Utilities and aggregators increasingly partner with service providers to scale demand response participation across multiple sites. The shift toward outcome-based energy savings, predictable costs, and continuous performance improvement made managed services attractive for commercial and industrial users seeking reliability without heavy upfront investment.

By End-use Analysis

Manufacturing drives Demand Response Management System Market, contributing 33.3% end-use demand globally.

In 2024, the Manufacturing sector accounted for 33.3% of the Demand Response Management System Market, driven by high energy consumption and cost sensitivity. Energy-intensive processes such as metal processing, chemicals, food production, and automotive manufacturing rely heavily on electricity during peak hours. Demand response systems help manufacturers shift non-critical loads, optimize production schedules, and avoid peak tariffs without disrupting output.

Increasing pressure to reduce operating costs and carbon emissions further encouraged adoption. Integration with energy management systems and automation platforms allowed manufacturers to participate in demand response programs seamlessly, turning energy flexibility into a strategic operational advantage.

Key Market Segments

By Technology

- Conventional Demand Response

- Automated Demand Response

By Services

- Curtailment Services

- System Integration and Consulting Services

- Managed Services

- Support and Maintenance

By End-use

- Manufacturing

- Office and Commercial Buildings

- Energy and Power

- Agriculture

- Others

Driving Factors

Building Emissions Rules Drive Smart Energy Control

Stricter building emission regulations are a major driving factor for the Demand Response Management System Market. Cities are pushing commercial and multifamily buildings to actively manage electricity use, especially during peak hours, to cut carbon emissions. This pressure encourages property owners to adopt automated demand response tools that can reduce load without affecting daily operations.

A strong example is when the City of Seattle awarded $17.2 million to implement its Building Emissions Performance Standard, supporting commercial and residential buildings in lowering climate pollution. Such programs push building operators to monitor, control, and optimize energy use more carefully. As compliance deadlines approach, demand response systems become practical solutions to meet emission targets while avoiding high retrofit costs and operational disruptions.

Restraining Factors

High Technology Complexity Slows Market Adoption

System complexity remains a key restraining factor for the Demand Response Management System Market. Many building owners and facility managers struggle with integrating demand response platforms into existing electrical and automation systems. Advanced controls, data analytics, and cybersecurity requirements can raise concerns around cost, skills, and long-term maintenance. This challenge exists even as innovation funding increases.

For instance, the U.S. Department of Energy announced $80 million to support innovative building technologies, aiming to modernize energy systems. While this funding accelerates development, it also highlights the technical gap between new solutions and on-site capabilities. Without skilled operators and simplified platforms, adoption may remain slow in smaller or older facilities.

Growth Opportunity

Empty Offices Create Energy Optimization Opportunities

Changing office usage patterns create a strong growth opportunity for demand response systems. Cities with high office vacancies face economic pressure and inefficient energy use in underutilized buildings. Reports warn that Boston could lose $1.7 billion in tax revenue due to empty offices, pushing stakeholders to rethink how these buildings operate. Demand response systems help owners reduce wasted electricity by adjusting loads based on real occupancy and grid needs.

As offices shift to flexible use or partial occupancy, automated energy control becomes essential. This creates opportunities for demand response solutions to support cost savings, improve grid interaction, and make underused buildings financially and operationally viable again.

Latest Trends

Office To Housing Conversions Shape Energy Trends

Adaptive reuse of commercial buildings is a key trend shaping the Demand Response Management System Market. As cities convert offices into residential spaces, energy demand patterns change from daytime commercial loads to around-the-clock residential use. This shift requires flexible energy management to balance comfort, costs, and grid stability.

A clear example is when the Healey-Driscoll Administration awarded $7.4 million to convert downtown Boston offices into new housing. Such projects increase the need for smart demand response systems that can manage mixed-use energy profiles. As conversions accelerate, demand response tools become central to handling new load behaviors efficiently and sustainably.

Regional Analysis

In 2024, North America leads the DRMS market at 43.5%, valued at USD 5.4 Bn.

In 2024, North America held a dominant position in the Demand Response Management System Market, accounting for 43.5% share and reaching a market value of USD 5.4 Bn. The region benefits from mature grid infrastructure, high penetration of smart meters, and strong participation from utilities and large commercial and industrial users. Widespread adoption of automated demand response platforms supports grid reliability, peak load reduction, and efficient energy pricing mechanisms. Strong regulatory frameworks and well-established energy markets continue to reinforce North America’s leadership.

In Europe, demand response systems are increasingly integrated into broader energy efficiency and grid-balancing strategies. Utilities and industrial users focus on flexibility services to manage variable renewable energy and stabilize power networks. Emphasis on digital energy platforms and cross-border electricity coordination supports steady regional adoption.

The Asia Pacific market is driven by rapid industrialization, urban growth, and rising electricity demand. Large manufacturing bases and expanding commercial infrastructure encourage the use of demand response to manage peak loads and operational costs.

In Middle East & Africa, grid modernization and growing power consumption create opportunities for demand response solutions, particularly in commercial and utility-scale applications.

Latin America shows gradual adoption as utilities seek cost-effective tools to manage grid stress and improve energy efficiency across urban centers.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, ABB continues to play a strategic role in the Demand Response Management System market through its strong capabilities in grid automation, digital substations, and energy management software. The company’s focus on integrating demand response with smart grids and industrial energy systems positions it well among utilities and large industrial users. ABB’s strength lies in connecting demand-side flexibility with grid reliability, helping customers optimize power usage without compromising operational continuity.

Eaton maintains a solid market presence by leveraging its expertise in power distribution, energy storage, and intelligent power management platforms. In demand response applications, Eaton’s solutions support real-time load control and energy optimization across commercial buildings, data centers, and manufacturing facilities. Its end-to-end approach, combining hardware with software-driven insights, allows customers to actively manage peak demand and improve energy resilience.

Enel SpA stands out for its utility-led demand response initiatives and deep operational experience in electricity networks. The company actively uses demand response as a grid-balancing tool, enabling flexible consumption patterns among commercial and industrial users. Enel’s emphasis on digital platforms and consumer participation strengthens its position as a demand response innovator within evolving power systems.

Top Key Players in the Market

- ABB

- Eaton

- Enel Spa

- ALARM.COM HOLDINGS, INC.

- General Electric

- Honeywell International Inc

- Itron Inc.

- Johnson Controls, Inc.

- Schneider Electric SE

- Siemens

Recent Developments

- In May 2024, Honeywell International Inc. teamed up with Enel North America to provide automated demand response and energy management solutions for commercial and industrial facilities. This collaboration helps organizations connect building automation systems with grid demand response programs, enabling automated control of energy loads during peak times for better grid stability and efficiency.

- In February 2024, General Electric’s energy arm (GE Vernova) introduced GridBeats, a portfolio of software-defined automation solutions to help utilities modernize grid operations, boost resilience, and manage complex power networks with digital controls and AI/ML tools. These capabilities support advanced energy management and indirectly enable better demand response and flexibility by giving operators real-time grid intelligence and control.

Report Scope

Report Features Description Market Value (2024) USD 12.5 Billion Forecast Revenue (2034) USD 54.7 Billion CAGR (2025-2034) 15.9% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Technology (Conventional Demand Response, Automated Demand Response), By Services (Curtailment Services, System Integration and Consulting Services, Managed Services, Support and Maintenance), By End-use (Manufacturing, Office and Commercial Buildings, Energy and Power, Agriculture, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape ABB, Eaton, Enel Spa, ALARM.COM HOLDINGS, INC., General Electric, Honeywell International Inc, Itron Inc., Johnson Controls, Inc., Schneider Electric SE, Siemens Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Demand Response Management System MarketPublished date: January 2026add_shopping_cartBuy Now get_appDownload Sample

Demand Response Management System MarketPublished date: January 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- ABB

- Eaton

- Enel Spa

- ALARM.COM HOLDINGS, INC.

- General Electric

- Honeywell International Inc

- Itron Inc.

- Johnson Controls, Inc.

- Schneider Electric SE

- Siemens

Our Clients

- 173907

- January 2026