Global Data Incident Management Market Size, Share and Analysis Report By Deployment Mode (Cloud-based, On-premises), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises), By Application (Data Quality Incident Response, Data Pipeline Failure Management, Data Breach and Security Incident Response, Compliance and Audit Incident Handling, Others), By End-User Industry (Banking, Financial Services, and Insurance, IT and Telecommunications, Healthcare, Retail and E-commerce, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 177595

- Number of Pages: 381

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaway

- Key Statistics

- Drivers Impact Analysis

- Restraint Impact Analysis

- Investor Type Impact Matrix

- Technology Enablement Analysis

- U.S. Data Incident Management Market Size

- Deployment Mode Analysis

- Organization Size Analysis

- Application Analysis

- End-User Industry Analysis

- Emerging Trends Analysis

- Growth Factors Analysis

- Opportunity Analysis

- Challenge Analysis

- Key Market Segments

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

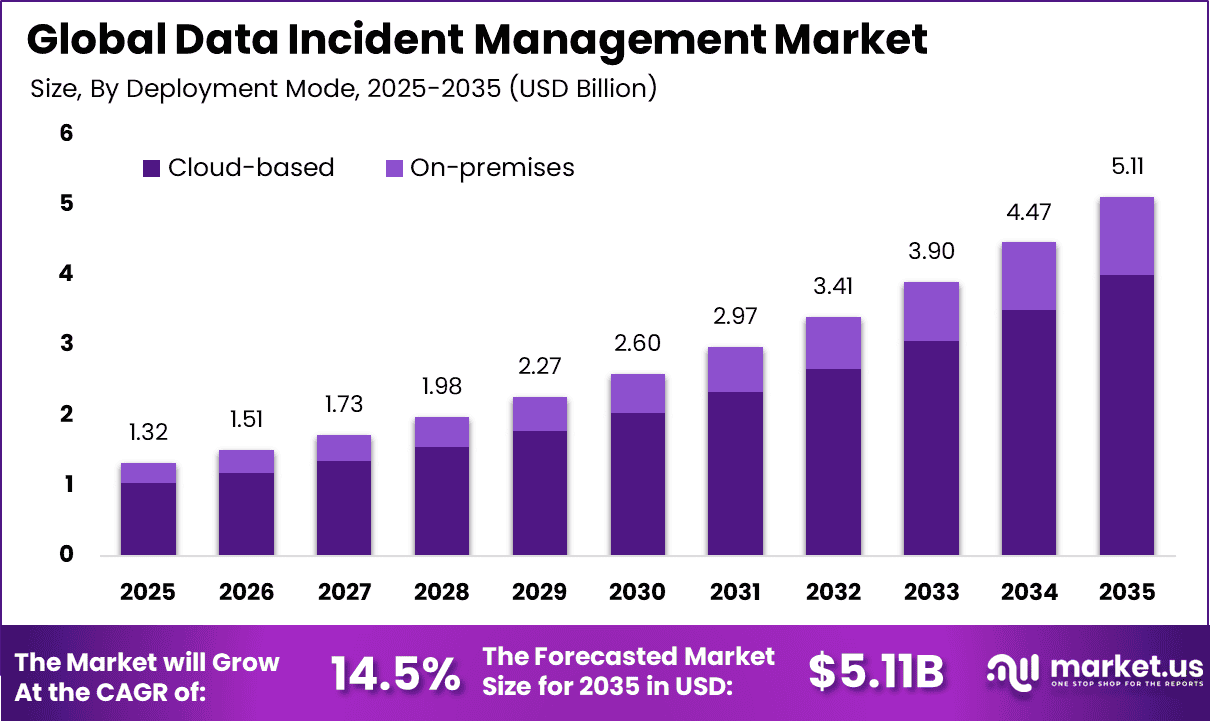

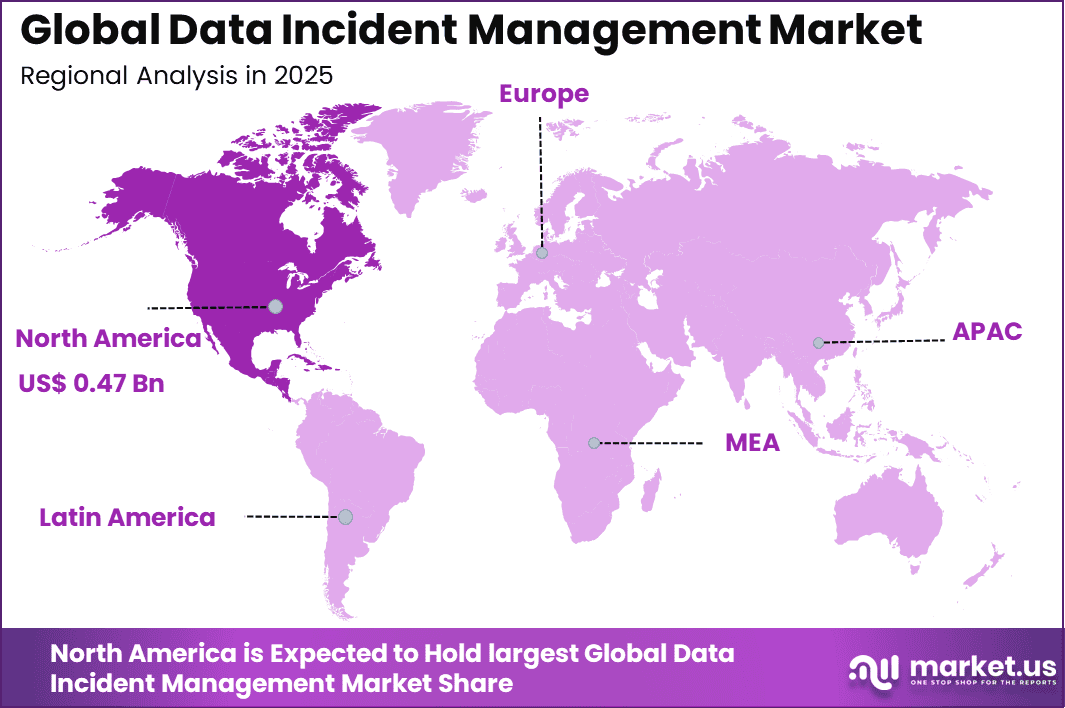

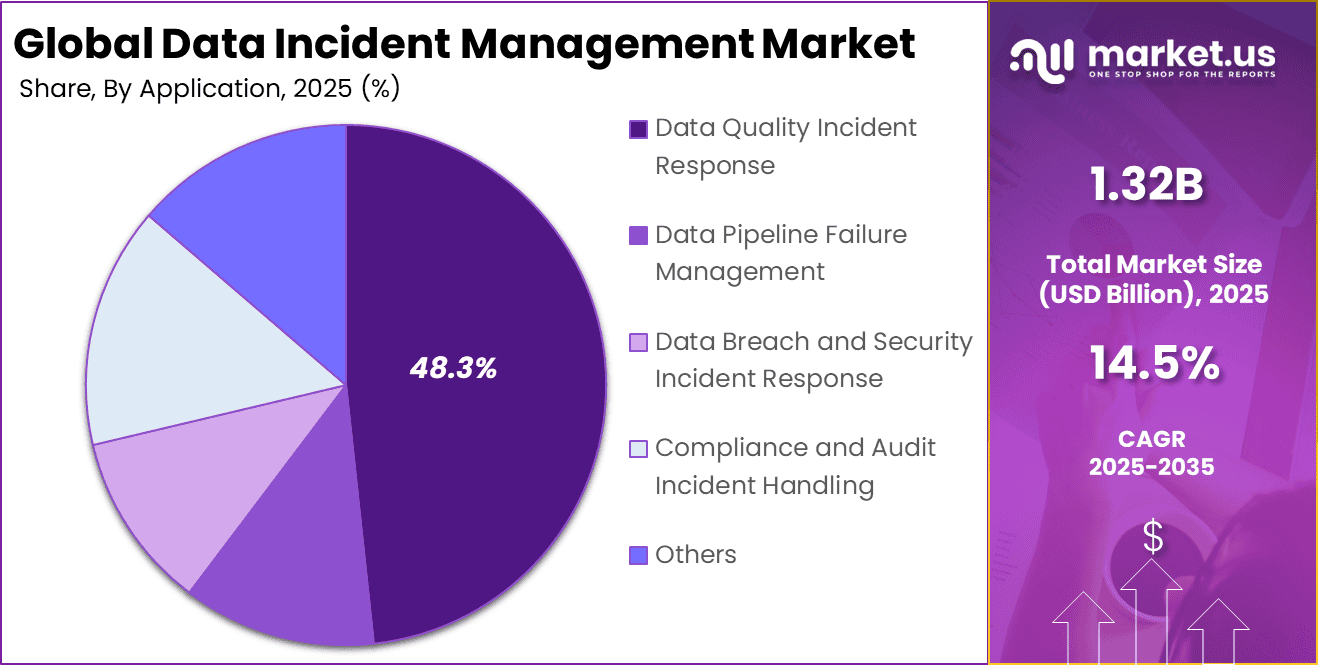

The Global Data Incident Management Market size is expected to be worth around USD 5.11 billion by 2035, from USD 1.32 billion in 2025, growing at a CAGR of 14.5% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 36.14% share, holding USD 0.47 billion in revenue.

The data incident management market focuses on systems that identify, manage, and resolve data related incidents across enterprise environments. These incidents include data quality failures, pipeline disruptions, access issues, and compliance related breaches. As organizations depend heavily on automated data flows, even minor data incidents can create operational and financial impact. Structured incident management has therefore become essential for data reliability and governance.

Top driving factors for the data incident management market are related to the increasing volume and complexity of data estates as enterprises adopt distributed cloud architectures and real time analytics. Organizations face higher operational risk when data issues go undetected, because revenue generating processes and customer experiences are directly linked to data quality and availability.

The rising frequency of cyber incidents, data breaches, and regulatory compliance expectations has made incident handling a board level priority in many sectors, which in turn supports demand for systematic data incident management. These pressures are manifest as greater investment in tools and workflows that enable rapid identification and resolution of data anomalies before they cascade into larger failures.

For instance, in January 2026, Atlassian deepened its incident management leadership through a new Dynatrace integration, embedding real-time production insights into Jira for agentic AI triage. Teams now get instant root cause analysis and business impact visibility, cutting recovery time without tool-switching.

Demand for data incident management is strongest among data driven enterprises operating real time or near real time analytics. Industries such as finance, ecommerce, logistics, and digital services rely on continuous data availability. These organizations experience frequent data issues due to scale and automation. Managing incidents manually becomes unsustainable at this level.

Key Takeaway

- By deployment mode, cloud based solutions led the Data Incident Management Market with a 78.4% share, supported by demand for centralized monitoring and faster incident response.

- By organization size, large enterprises accounted for 82.5% of total adoption, reflecting complex data ecosystems and higher governance requirements.

- By application, data quality incident response held a 48.3% share, driven by the need to quickly identify and resolve data errors.

- By end user industry, Banking, Financial Services, and Insurance represented 41.7% of market demand, supported by strict compliance and operational risk controls.

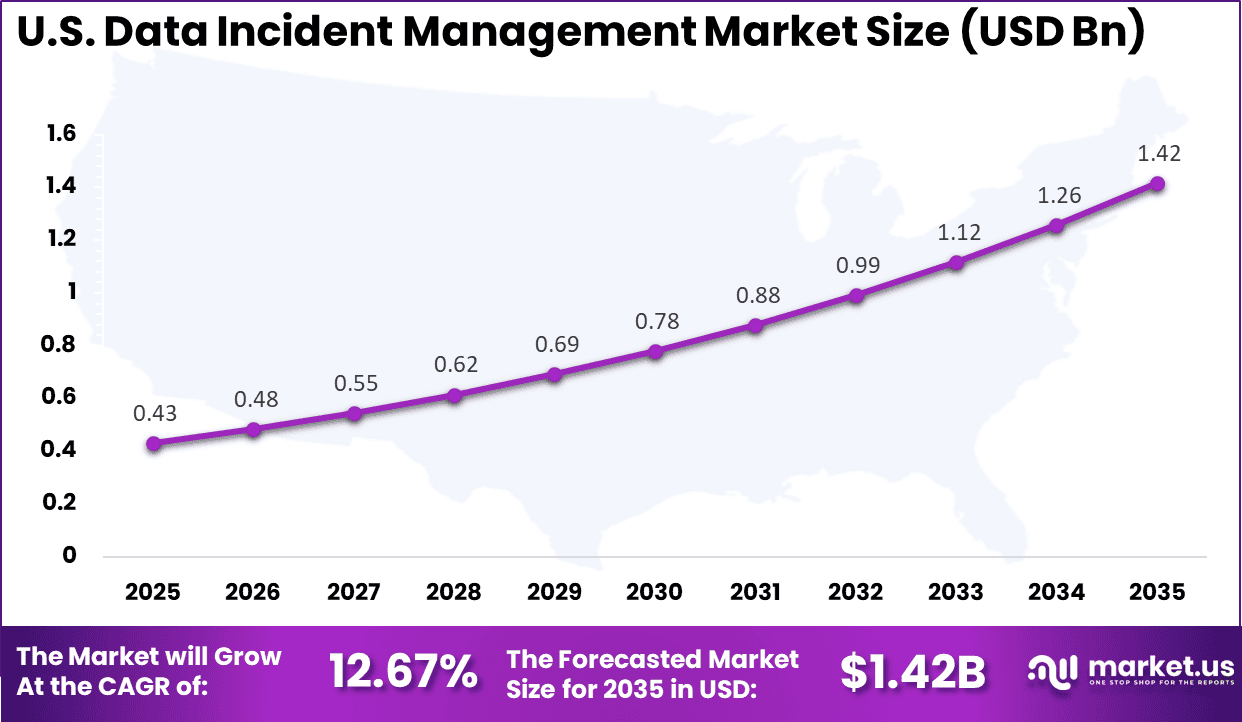

- Regionally, North America held a 36.14% share of the market, with the US valued at USD 0.43 billion and recording a CAGR of 12.67%, reflecting steady investment in data governance and risk management systems.

Key Statistics

- The global average cost of a data breach stood at USD 4.88 million in 2024 and slightly declined to USD 4.44 million in 2025, while the average cost in the US remained significantly higher at USD 10.22 million.

- The average breach lifecycle, from identification to containment, is approximately 241 days, indicating prolonged exposure and recovery periods.

- Human related factors contribute to 68% of breaches, including phishing and operational errors, while 72% of ransomware incidents are linked to software vulnerabilities or absence of multi factor authentication.

- About 99% of organizations report exposure of sensitive data to AI tools, and 16% of breaches in 2025 involved AI driven attack methods.

- Only 45% of companies maintain a formal incident response plan, and just 30% regularly test their response procedures, highlighting preparedness gaps.

Drivers Impact Analysis

Key Driver Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Rising frequency of data breaches and cyber incidents +4.3% Global Short to medium term Increasing regulatory requirements for breach reporting +3.2% Europe, North America Medium term Expansion of cloud and hybrid IT environments +2.9% Global Medium term Growing adoption of DevOps and DataOps frameworks +2.4% North America, Asia Pacific Medium term Enterprise focus on minimizing downtime and reputational risk +1.7% Global Medium to long term Restraint Impact Analysis

Key Restraint Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline High implementation and customization costs -2.8% Emerging Markets Short to medium term Integration complexity across multi-vendor IT stacks -2.4% Global Medium term Limited incident response maturity in mid-sized firms -2.0% Asia Pacific, Latin America Medium term Alert fatigue and workflow inefficiencies -1.7% North America, Europe Medium term Data privacy and governance constraints -1.5% Europe Medium to long term Investor Type Impact Matrix

Investor Type Growth Sensitivity Risk Exposure Geographic Focus Investment Outlook Cybersecurity and incident response platform providers Very High Medium North America, Europe Strong recurring SaaS revenue Cloud and IT infrastructure vendors High Medium Global Integration-led growth Managed security service providers High Low to Medium Global Recurring service contracts Private equity firms Medium Medium North America, Europe Consolidation of response platforms Venture capital investors High High North America Innovation in AI-driven response Technology Enablement Analysis

Technology Enabler Impact on CAGR Forecast (~%) Primary Function Geographic Relevance Adoption Timeline Automated incident detection and response workflows +4.5% Faster remediation Global Short to medium term AI-driven root cause analysis tools +3.8% Accurate issue identification North America, Europe Medium term Cloud-native incident management platforms +3.2% Scalable operations Global Medium term Integration with SIEM and security orchestration systems +2.6% Unified threat visibility Global Medium to long term Real-time reporting and compliance dashboards +2.0% Audit and regulatory readiness Europe, North America Long term U.S. Data Incident Management Market Size

The market for Data Incident Management within the U.S. is growing tremendously and is currently valued at USD 0.43 billion, the market has a projected CAGR of 12.67%. The market is growing due to rising cyber threats, stricter data protection regulations, and increasing digital transformation across industries. Organizations face frequent ransomware attacks, data breaches, and insider risks, prompting higher investment in incident response and monitoring tools.

Regulations such as state-level privacy laws and federal cybersecurity mandates require timely reporting and mitigation of breaches. Additionally, growing cloud adoption, remote work models, and complex IT environments are driving demand for advanced incident detection, response automation, and compliance management solutions.

For instance, in February 2026, ServiceNow enhanced its Security Incident Response (SIR) platform with AI-powered post-incident analysis, NIST-based prioritization, and third-party risk scoring integration. These updates streamline incident triage, reduce duplicate escalations, and improve automation for faster resolution, reinforcing U.S. leadership in data incident management.

In 2025, North America held a dominant market position in the Global Data Incident Management Market, capturing more than a 36.14% share, holding USD 0.47 billion in revenue. This dominance is due to its advanced digital infrastructure, high concentration of large enterprises, and strong regulatory environment. The region experiences a high volume of cyber incidents, prompting organizations to prioritize structured incident response frameworks.

Strict data privacy laws, including state level regulations and federal cybersecurity guidelines, require rapid breach reporting and mitigation. In addition, widespread cloud adoption, strong cybersecurity investments, and the presence of leading technology providers continue to strengthen the region’s leadership in this market.

For instance, in June 2025, IBM Instana introduced Intelligent Incident Investigation powered by agentic AI, enabling rapid root cause analysis and remediation. This preview feature cuts investigation time significantly, highlighting North America’s AI leadership in incident response.

Deployment Mode Analysis

In 2025, cloud based solutions accounted for 78.4% of adoption. Cloud deployment allows centralized monitoring across distributed data environments. Enterprises benefit from faster implementation and easier scalability. This aligns with modern data architecture strategies. Cloud platforms enable real time alerting and collaboration.

Incident response teams can access systems without location constraints. Updates and fixes are deployed without service interruption. This improves response efficiency. Security and reliability improvements have supported confidence in cloud deployment. Data protection standards have matured significantly. As a result, cloud based data incident management has become the preferred model.

For Instance, in February 2026, ServiceNow rolled out updates to its Security Incident Response app, boosting cloud-based handling with better phishing workflows and category tools. This helps teams in cloud setups respond faster to data issues by simplifying detection and triage in distributed environments. Cloud users gain from easier access and auto-scaling during peaks.

Organization Size Analysis

In 2025, large enterprises represented 82.5% of demand. These organizations manage complex data operations across multiple departments and regions. Data incidents can have wide ranging impact. Formal incident management is therefore critical. Large enterprises also face higher compliance and reputational risk. Automated tracking and escalation improve control.

Incident resolution times are reduced through standardized workflows. This supports operational stability. Investment capacity further supports adoption. Large enterprises can integrate incident management with data governance and analytics platforms. This reinforces their dominant position in the market.

For instance, in June 2025, Atlassian enhanced Jira Service Management for enterprises with better role controls and GraphQL APIs for complex workflows. Large firms use it to sync incidents across teams, handling big-scale data events with event-driven automation. It supports enterprise needs for coordinated responses in vast infrastructures.

Application Analysis

In 2025, data quality incident response accounted for 48.3% of usage. Data quality issues directly affect reporting, analytics, and decision making. Incorrect or incomplete data can lead to financial loss and regulatory exposure. Rapid response is therefore a priority. Incident management tools help identify root causes of quality failures.

Automated alerts signal anomalies in data accuracy and completeness. Response teams can act before downstream systems are affected. This reduces business disruption. As data driven decision making increases, quality assurance becomes more critical. Incident response platforms provide structured resolution processes. This has made data quality the leading application area.

For Instance, in January 2026, Splunk On-Call (ex-VictorOps) improved integrations for data quality alerts, adding real-time timelines and runbooks. Users automate triage for quality incidents from logs, reducing manual fixes. This strengthens the response to data flaws in monitoring-heavy apps.

End-User Industry Analysis

In 2025, Banking, financial services, and insurance accounted for 41.7% of adoption due to their reliance on accurate and timely data. Data incidents in these sectors can disrupt transactions, reporting, and customer trust. Strong incident controls are therefore essential. Data incident management supports operational resilience. Regulatory oversight in financial services is strict and ongoing.

Institutions must document incidents and response actions. Automated platforms support compliance and audit requirements. This reduces regulatory risk. Digital transformation has increased data volumes and system complexity in BFSI organizations. Automated incident handling helps manage this scale efficiently. As digital finance expands, BFSI remains a primary end user industry.

For Instance, in December 2025, PagerDuty advanced Opsgenie features for BFSI workflows, with tailored escalations and dashboards for financial alerts. Banks use it for payment API crashes, routing to specialists fast. It ensures compliance in high-stakes data incidents for finance.

Emerging Trends Analysis

An emerging trend in the data incident management market is consolidation of incident response and observability functions. Platforms are increasingly combining monitoring, logging, alerting, incident workflows, and post-incident analysis into unified suites. End-to-end visibility and coordinated response support faster resolution and comprehensive oversight. Unified observability is becoming a standard expectation.

Another trend is the adoption of collaborative incident management workflows. These tools support cross-team communication, centralised case tracking, and shared knowledge bases. Enhanced collaboration reduces response friction and improves institutional learning from incidents.

Growth Factors Analysis

One of the key growth factors for the data incident management market is rising regulatory and compliance requirements. Organisations must demonstrate capability to detect, manage, and report data incidents. Incident management frameworks provide essential compliance artefacts and documentation. Regulatory driven investment continues to support steady demand.

Another growth factor is increasing business reliance on digital systems and data services. Any operational disruption can affect revenue, customer experience, or competitive positioning. Incident management tools reduce downtime and improve recovery confidence. This operational demand reinforces long term adoption.

Opportunity Analysis

A significant opportunity in the data incident management market lies in integration with advanced analytics and machine learning. These capabilities enable proactive detection, automatic classification of incident severity, and predictive insights into potential incident causation. Platforms that incorporate intelligent analytics improve speed and accuracy of detection and response. This enhances value for larger enterprises facing high volumes of data activity.

Another opportunity is the alignment between incident management and broader resilience frameworks. Organisations are increasingly investing in business continuity and disaster recovery planning. Incident management tools that integrate with continuity planning and risk assessment frameworks support unified preparedness and response strategies.

Challenge Analysis

A major challenge for the data incident management market is balancing automation with control. Automated detection and response workflows improve speed but may require careful tuning to avoid unnecessary actions or false positives. Organisations must ensure that automated responses uphold compliance and maintain operational stability. Finding the optimal balance remains a technical and governance challenge.

Another challenge involves clear attribution and root cause analysis. Data incidents can stem from complex interactions between infrastructure faults, software errors, and human action. Accurately tracing causation requires sophisticated tools and skilled analysts. Without clear analysis, corrective actions may be incomplete or ineffective.

Key Market Segments

By Deployment Mode

- Cloud-based

- On-premises

By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises

By Application

- Data Quality Incident Response

- Data Pipeline Failure Management

- Data Breach and Security Incident Response

- Compliance and Audit Incident Handling

- Others

By End-User Industry

- Banking, Financial Services, and Insurance

- IT and Telecommunications

- Healthcare

- Retail and E-commerce

- Others

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Enterprise workflow and service management leaders such as ServiceNow and Atlassian dominate the data incident management market. Their platforms provide structured ticketing, root cause tracking, and automated remediation workflows. IBM and Microsoft integrate incident response within broader cloud and security ecosystems. These vendors benefit from strong enterprise adoption and cross-functional integration.

Observability and monitoring providers such as Splunk, Datadog, and LogicMonitor strengthen incident detection through real-time alerts and anomaly insights. SolarWinds, BMC Software, and Micro Focus enhance visibility across hybrid environments. These tools reduce mean time to detection and resolution. Adoption is strong among enterprises operating complex multi-cloud infrastructures.

Alerting and incident orchestration specialists such as PagerDuty, Opsgenie, BigPanda, VictorOps, and xMatters focus on real-time collaboration and automated escalation. These players emphasize AI-driven event correlation and workflow automation. Other vendors add competitive depth and regional specialization, supporting continuous improvement in enterprise data incident management practices.

Top Key Players in the Market

- ServiceNow

- Atlassian

- IBM

- Microsoft

- Splunk

- Datadog

- PagerDuty

- Opsgenie

- BigPanda

- VictorOps

- xMatters

- LogicMonitor

- BMC Software

- Micro Focus

- SolarWinds

- Others

Recent Developments

- In December 2025, Datadog acquired Metaplane, an ML-powered data observability platform, expanding incident management to data quality across warehouses like Snowflake. The deal unifies app, infra, and data visibility, cutting MTTR for AI/ML pipelines.

- In February 2026, ServiceNow rolled out major updates to its Security Incident Response module, adding AI-driven post-incident analysis and NIST-aligned prioritization. These enhancements cut down triage time by up to 30% for enterprises.

Report Scope

Report Features Description Market Value (2025) USD 1.3 Billion Forecast Revenue (2035) USD 5.1 Billion CAGR(2025-2035) 14.5% Base Year for Estimation 2024 Historic Period 2020-2024 Forecast Period 2025-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Deployment Mode (Cloud-based, On-premises), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises), By Application (Data Quality Incident Response, Data Pipeline Failure Management, Data Breach and Security Incident Response, Compliance and Audit Incident Handling, Others), By End-User Industry (Banking, Financial Services, and Insurance, IT and Telecommunications, Healthcare, Retail and E-commerce, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape ServiceNow, Atlassian, IBM, Microsoft, Splunk, Datadog, PagerDuty, Opsgenie, BigPanda, VictorOps, xMatters, LogicMonitor, BMC Software, Micro Focus, SolarWinds, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Data Incident Management MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample

Data Incident Management MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- ServiceNow

- Atlassian

- IBM

- Microsoft

- Splunk

- Datadog

- PagerDuty

- Opsgenie

- BigPanda

- VictorOps

- xMatters

- LogicMonitor

- BMC Software

- Micro Focus

- SolarWinds

- Others

Our Clients

- 177595

- Feb. 2026