Quick Navigation

Report Overview

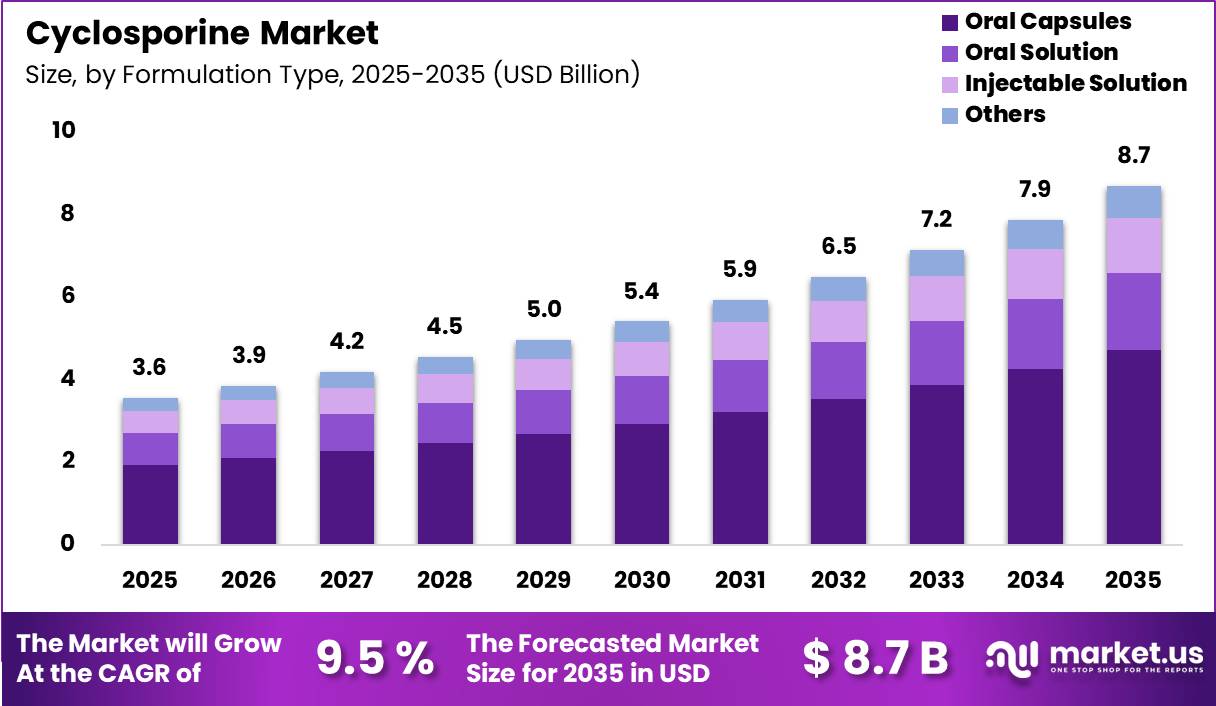

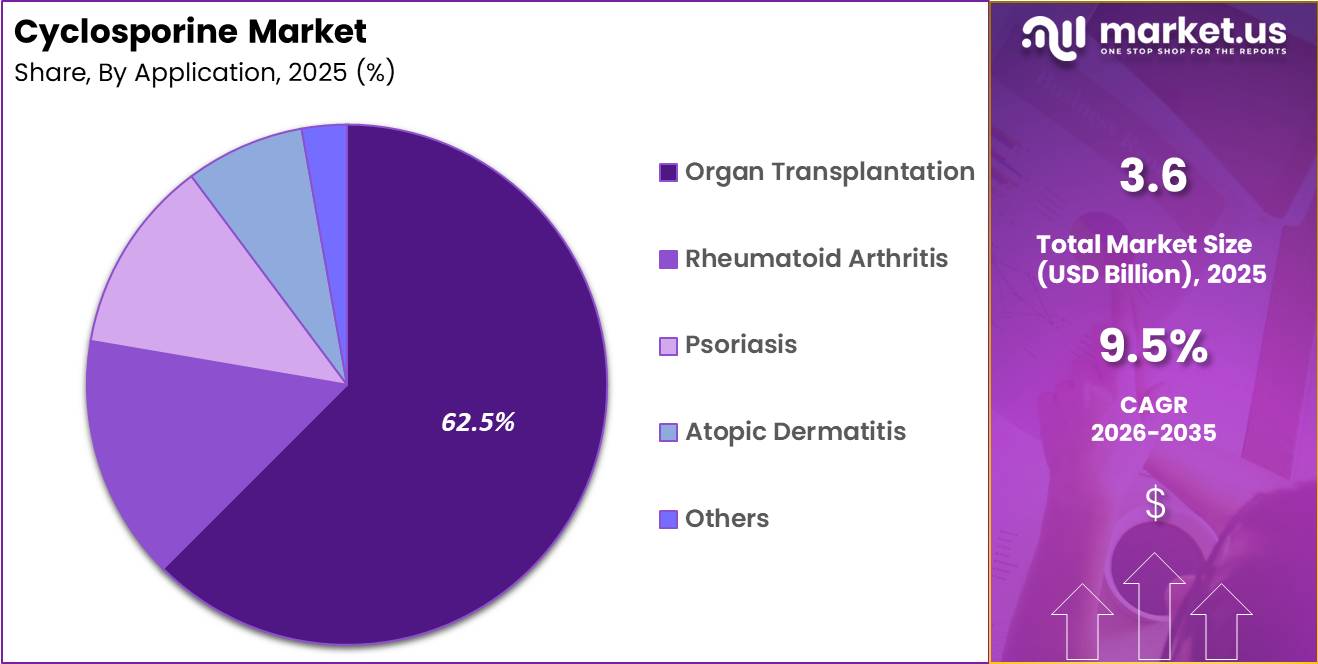

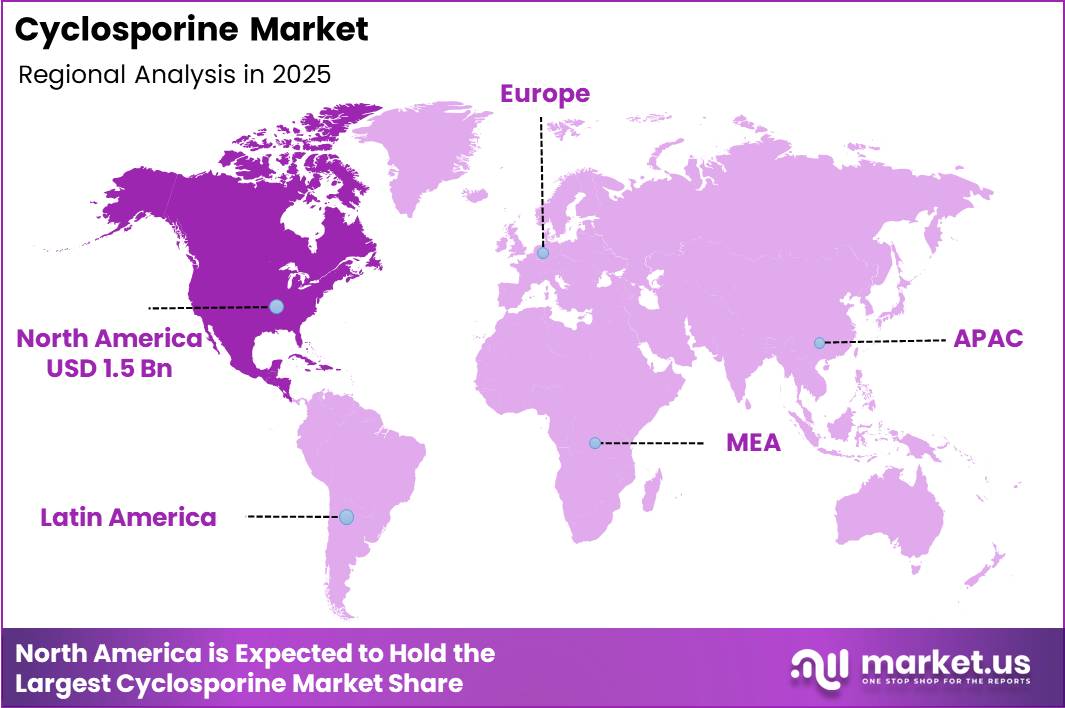

Global Cyclosporine Market size is expected to be worth around US$ 8.7 Billion by 2035 from US$ 3.6 Billion in 2025, growing at a CAGR of 9.5% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 42.5% share with a revenue of US$ 1.5 Billion.

The global cyclosporine market is witnessing steady growth due to the increasing number of organ transplantation procedures and the rising prevalence of autoimmune diseases worldwide. Cyclosporine is a calcineurin inhibitor widely used as an immunosuppressive therapy to prevent organ rejection following kidney, liver, heart, and lung transplantation.

It is also extensively prescribed for autoimmune disorders such as rheumatoid arthritis, psoriasis, nephrotic syndrome, and dry eye disease. The drug plays a critical role in suppressing T-lymphocyte activity, thereby reducing immune-mediated damage and improving transplant success rates.

The growing demand for organ transplantation remains a primary growth driver for the market. According to the United Network for Organ Sharing (UNOS) and the Organ Procurement and Transplantation Network (OPTN), approximately 48,149 organ transplants were performed in the United States in 2024, representing a 3.3% increase compared with 2023. In 2023, around 46,632 organ transplants were conducted in the country, while more than 109,000 patients remained on the national transplant waiting list. The increasing number of transplant procedures directly supports the demand for cyclosporine-based immunosuppressive therapies.

Additionally, the growing burden of autoimmune diseases is contributing significantly to market expansion. According to the National Institutes of Health (NIH), autoimmune diseases affect nearly 8% of the global population, with rising incidence rates observed across both developed and emerging economies. Increasing healthcare expenditure, expanding access to specialty treatments, and improvements in drug delivery technologies are further supporting market growth.

Pharmaceutical manufacturers are also focusing on generic formulations, improved bioavailability, and strategic distribution partnerships to expand patient access. Furthermore, advancements in transplant technologies, growing awareness regarding organ donation, and supportive healthcare infrastructure development are expected to strengthen the long-term growth outlook of the cyclosporine market globally.

Key Takeaways

- Market Size: Global Cyclosporine Market size is expected to be worth around US$ 8.7 Billion by 2035 from US$ 3.6 Billion in 2025.

- Market Share: The market growing at a CAGR of 9.5% during the forecast period from 2026 to 2035.

- Formulation Type Analysis: Oral Capsules are projected to dominate the market, accounting for 54.2% of the global market share in 2025.

- Application Analysis: Organ Transplantation is expected to remain the leading application segment, accounting for 62.5% of the market share in 2025.

- End User Analysis: Hospitals are anticipated to dominate the market with a 48.6% share in 2025.

- Distribution Channel Analysis: Hospital Pharmacies are expected to lead the market with a 45.8% share in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 42.5% share with a revenue of US$ 1.5 Billion.

Formulation Type Analysis

The formulation type segment of the Cyclosporine market is categorized into Oral Capsules, Oral Solution, Injectable Solution, and Others. Among these, Oral Capsules are projected to dominate the market, accounting for 54.2% of the global market share in 2025. The dominance of this segment is primarily attributed to the high adoption of capsule formulations in long-term immunosuppressive therapy following organ transplantation.

Oral capsules offer improved patient compliance, convenient dosing, enhanced bioavailability, and ease of administration, which have supported their widespread utilization across hospital and outpatient settings. In addition, the growing prevalence of autoimmune disorders and chronic inflammatory conditions has further accelerated the demand for oral cyclosporine formulations.

The Oral Solution segment is also witnessing stable growth due to its suitability for pediatric and geriatric patients who experience swallowing difficulties. Injectable Solutions are mainly utilized in acute care and transplant procedures where rapid therapeutic action is required, particularly in hospital environments. Meanwhile, the Others segment, including topical and specialty formulations, is expected to expand steadily owing to ongoing product innovations and increasing therapeutic applications in dermatology and ophthalmology.

Application Analysis

Based on application, the Cyclosporine market is segmented into Organ Transplantation, Rheumatoid Arthritis, Psoriasis, Atopic Dermatitis, and Others. Organ Transplantation is expected to remain the leading application segment, accounting for 62.5% of the market share in 2025.

The segment’s dominance is driven by the critical role of cyclosporine in preventing organ rejection following kidney, liver, heart, and lung transplantation procedures. The increasing number of transplant surgeries globally, coupled with the rising burden of chronic organ failure, continues to support sustained demand for cyclosporine-based immunosuppressive therapies.

The Rheumatoid Arthritis segment is experiencing moderate growth due to the increasing prevalence of autoimmune diseases and the growing use of immunomodulatory therapies in severe inflammatory conditions. Psoriasis remains another significant application area, supported by rising dermatological consultations and increasing awareness regarding advanced treatment options for chronic skin disorders.

The Atopic Dermatitis segment is projected to witness notable expansion owing to the increasing incidence of allergic skin diseases and growing preference for targeted immunosuppressive therapies. The Others category includes ophthalmic and off-label applications, which are anticipated to contribute steadily to market growth due to expanding clinical research and therapeutic advancements.

End User Analysis

Based on end user, the Cyclosporine market is segmented into Hospitals, Specialty Clinics, Transplant Centers, Retail Pharmacies, and Others. Hospitals are anticipated to dominate the market with a 48.6% share in 2025.

The strong position of hospitals is attributed to the high volume of organ transplant procedures, inpatient immunosuppressive treatments, and the availability of advanced healthcare infrastructure. Hospitals remain the primary point of care for patients requiring intensive monitoring and administration of cyclosporine therapies, particularly in transplant and autoimmune disease management.

Transplant Centers represent a significant segment due to the growing number of specialized organ transplant facilities worldwide and increasing success rates of transplantation procedures. Specialty Clinics are also gaining traction as they provide focused treatment for autoimmune and dermatological disorders such as rheumatoid arthritis and psoriasis, thereby supporting higher prescription volumes of cyclosporine.

Retail Pharmacies continue to play an important role in improving patient access to maintenance therapies and chronic disease medications, particularly in developed healthcare markets. Meanwhile, the Others segment, including ambulatory care centers and home healthcare settings, is expected to witness gradual growth driven by the increasing preference for outpatient treatment and long-term disease management solutions.

Distribution Channel Analysis

Based on distribution channel, the Cyclosporine market is segmented into Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, and Others. Hospital Pharmacies are expected to lead the market with a 45.8% share in 2025.

The dominance of this segment is primarily associated with the high consumption of cyclosporine in hospital-based organ transplantation procedures and inpatient autoimmune disease treatments. Hospital pharmacies ensure the availability of specialized immunosuppressive medications, proper dosage monitoring, and controlled dispensing practices, which are critical for patient safety and therapeutic effectiveness.

Retail Pharmacies account for a considerable market share due to the increasing number of patients requiring long-term maintenance therapy for chronic autoimmune disorders. The accessibility and widespread presence of retail pharmacy networks have contributed significantly to the growth of this segment. Online Pharmacies are witnessing rapid expansion owing to the growing adoption of digital healthcare platforms, rising internet penetration, and increasing consumer preference for convenient medicine purchasing options.

Furthermore, the availability of home delivery services and discounted pricing strategies is supporting the adoption of online pharmaceutical distribution channels. The Others segment, including specialty distributors and direct supply channels, is expected to experience steady growth driven by evolving pharmaceutical supply chain models and expanding healthcare access globally.

Key Market Segments

By Formulation Type

- Oral Capsules

- Oral Solution

- Injectable Solution

- Others

By Application

- Organ Transplantation

- Rheumatoid Arthritis

- Psoriasis

- Atopic Dermatitis

- Others

By End User

- Hospitals

- Specialty Clinics

- Transplant Centers

- Retail Pharmacies

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Others

Driving Factors

The growth of the Cyclosporine market is primarily driven by the increasing number of organ transplantation procedures and the rising prevalence of autoimmune disorders globally. Cyclosporine is a calcineurin inhibitor widely used to prevent organ rejection following kidney, liver, and heart transplantation. According to the World Health Organization, cyclosporine is included in the WHO Model List of Essential Medicines because of its critical role in transplantation and immune suppression.

The increasing burden of chronic kidney disease and end-stage renal disease has significantly raised the demand for transplant-related immunosuppressive therapies. Data published by the National Center for Biotechnology Information (NCBI) indicates that cyclosporine remains extensively used in kidney, liver, and heart transplant procedures due to its ability to suppress T-cell activation effectively.

Clinical studies published in the New England Journal of Medicine (NEJM) reported graft survival rates of approximately 78% among renal transplant recipients treated with cyclosporine during a median follow-up period of 36 months. Additionally, increasing incidences of rheumatoid arthritis, psoriasis, and nephrotic syndrome are contributing to long-term prescription demand globally.

Trending Factors

A major trend observed in the Cyclosporine market is the increasing adoption of modified and targeted cyclosporine formulations designed to improve bioavailability and reduce nephrotoxicity risks. Healthcare providers are increasingly focusing on therapeutic drug monitoring and personalized dosing strategies to optimize transplant outcomes. According to the NCBI StatPearls Database, the therapeutic range of cyclosporine in kidney transplant patients varies between 200–400 ng/mL during the first week after transplantation and gradually declines to 75–160 ng/mL after one year, demonstrating the growing importance of individualized treatment protocols.

In addition, pharmaceutical manufacturers are developing microemulsion formulations that provide improved absorption consistency compared to traditional formulations. Another important trend is the growing use of cyclosporine in autoimmune disease management beyond transplantation applications. The Mayo Clinic reports that cyclosporine is increasingly prescribed for severe rheumatoid arthritis and plaque psoriasis in patients unresponsive to conventional therapies.

Furthermore, ongoing pharmacokinetic studies are supporting dose optimization approaches. Research data analyzing 3,674 cyclosporine blood concentration samples showed significant variability in drug clearance depending on postoperative conditions and hematocrit levels, reinforcing the industry trend toward precision medicine and patient-specific monitoring.

Restraining Factors

The Cyclosporine market faces substantial restraints due to the drug’s narrow therapeutic index and its association with severe adverse effects, particularly nephrotoxicity and hypertension. Long-term administration of cyclosporine requires continuous monitoring because small deviations in blood concentration can lead to organ rejection or toxic complications.

According to the NCBI Bookshelf the therapeutic window of cyclosporine is relatively narrow, requiring regular blood concentration monitoring to avoid toxicity. Patients undergoing long-term treatment often experience adverse reactions including kidney dysfunction, elevated blood pressure, tremors, infections, and liver toxicity.

Clinical evidence published in the New England Journal of Medicine (NEJM) found that among 1,663 renal transplant recipients treated with cyclosporine, graft losses occurred in 17% of patients, partly due to chronic graft dysfunction and complications associated with therapy management. In addition, high treatment costs and the need for lifelong immunosuppressive therapy create affordability challenges, especially in low- and middle-income countries.

The World Health Organization (WHO) reported that medicines account for 20–60% of healthcare spending in developing countries, while up to 90% of patients purchase medicines through out-of-pocket expenditures. These financial burdens and safety concerns continue to limit wider market expansion in several healthcare systems globally.

Opportunity

Significant opportunities are emerging in the Cyclosporine market due to the increasing global focus on organ transplantation infrastructure, expansion of healthcare access, and development of advanced immunosuppressive therapies. Governments and healthcare organizations are increasingly investing in transplant programs and specialty treatment centers, particularly in emerging economies.

According to the World Health Organization (WHO), more than 150 countries have adopted national essential medicines lists based on the WHO Essential Medicines List, supporting broader availability of critical drugs including cyclosporine. The increasing prevalence of chronic diseases such as kidney failure, autoimmune disorders, and severe inflammatory diseases is expected to strengthen long-term demand for immunosuppressive medications.

Furthermore, advances in pharmacokinetic monitoring and therapeutic drug management present opportunities for pharmaceutical innovation and safer treatment approaches. Research studies published through PubMed demonstrated that cyclosporine-based immunosuppressive regimens improved renal graft survival to 75% at one year compared with 55% among patients not receiving cyclosporine therapy.

Additionally, increasing research into combination immunosuppressive regimens and steroid-sparing therapies is expected to create opportunities for improved treatment outcomes and reduced side effects. The growing adoption of personalized medicine, biosimilar development, and improved transplant survival rates are expected to support future market expansion across both developed and emerging healthcare markets.

Regional Analysis

North America dominated the global Cyclosporine Market in 2025, accounting for over 42.5% of the total market share and generating revenue of approximately US$ 1.5 Billion. The regional market growth is primarily supported by the high prevalence of autoimmune disorders, increasing organ transplantation procedures, and strong adoption of advanced immunosuppressive therapies across the United States and Canada.

The presence of well-established healthcare infrastructure, favorable reimbursement frameworks, and extensive availability of branded as well as generic cyclosporine products has further strengthened market expansion in the region. In addition, growing awareness regarding early diagnosis and treatment of chronic inflammatory diseases such as rheumatoid arthritis, psoriasis, and nephrotic syndrome continues to support product demand.

The United States represents the largest contributor within North America due to rising healthcare expenditure, continuous pharmaceutical innovation, and the strong presence of leading biotechnology and pharmaceutical companies involved in immunosuppressive drug development.

Furthermore, increasing investments in transplant research and supportive government initiatives aimed at improving patient access to specialty therapies are expected to sustain market growth over the forecast period. The rising adoption of oral and ophthalmic cyclosporine formulations for long-term disease management also contributes significantly to regional revenue generation.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The Cyclosporine Market is characterized by the presence of several global pharmaceutical and biotechnology companies focusing on product innovation, generic drug development, and strategic collaborations to strengthen their market position.

Major players are actively investing in research and development activities to enhance formulation efficacy, improve patient compliance, and expand therapeutic applications in autoimmune diseases and organ transplantation. Companies are also emphasizing the development of ophthalmic and oral cyclosporine formulations to address the growing demand for long-term immunosuppressive treatment.

Leading market participants include Novartis AG, Teva Pharmaceutical Industries Ltd., AbbVie Inc., Sun Pharmaceutical Industries Ltd., and Viatris Inc.. These companies compete based on product portfolio, pricing strategies, regulatory approvals, and geographic expansion.

Additionally, increasing partnerships with healthcare providers and distributors are supporting wider product accessibility across emerging and developed markets. The competitive landscape remains moderately consolidated, with established players focusing on strengthening their global distribution networks and market presence.

Market Key Players

- Novartis AG

- AbbVie Inc.

- Allergan plc (AbbVie)

- Sun Pharmaceutical Industries Ltd.

- Mylan N.V.

- Teva Pharmaceutical Industries Ltd.

- Akorn, Inc.

- Cipla Inc.

- Dr. Reddy’s Laboratories Ltd.

- Intas Pharmaceuticals Ltd.

- Glenmark Pharmaceuticals Ltd.

- Apotex Inc.

- Bausch Health Companies Inc.

- Panacea Biotec Ltd.

- Zydus Lifesciences Limited

- Others

Recent Developments

- Novartis (February 2025): Novartis announced the acquisition of Anthos Therapeutics for about 925 million dollars, part of a broader strategy to deepen its cardiovascular and immunology pipeline; while not cyclosporine‑specific, this signals sustained capital allocation into immune‑modulating therapies that keeps Novartis well‑placed in transplant and autoimmune care where cyclosporine remains a backbone option.

- Dr. Reddy’s Laboratories Ltd. (March 2025): Introduced a new cyclosporine microemulsion formulation designed to improve bioavailability in transplant patients. The development reflects the company’s continued focus on specialty immunosuppressant formulations and value-added generics within the transplant care segment.

- Sun Pharmaceutical Industries Ltd. (2025): Expanded the commercial reach of its Cequa portfolio through a broader distribution agreement focused on cyclosporine ophthalmic therapies. The strategic expansion continued to support the company’s positioning in the chronic dry eye treatment market during 2025.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 3.6 Billion |

| Forecast Revenue (2035) | US$ 8.7 Billion |

| CAGR (2026-2035) | 9.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Formulation Type (Oral Capsules, Oral Solution, Injectable Solution, Others) By Application (Organ Transplantation, Rheumatoid Arthritis, Psoriasis, Atopic Dermatitis, Others) By End User (Hospitals, Specialty Clinics, Transplant Centers, Retail Pharmacies, Others) By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Novartis AG, AbbVie Inc., Allergan plc (AbbVie), Sun Pharmaceutical Industries Ltd., Mylan N.V., Teva Pharmaceutical Industries Ltd., Akorn, Inc., Cipla Inc., Dr. Reddy’s Laboratories Ltd., Intas Pharmaceuticals Ltd., Glenmark Pharmaceuticals Ltd., Apotex Inc., Bausch Health Companies Inc., Panacea Biotec Ltd., Zydus Lifesciences Limited, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |