Quick Navigation

Report Overview

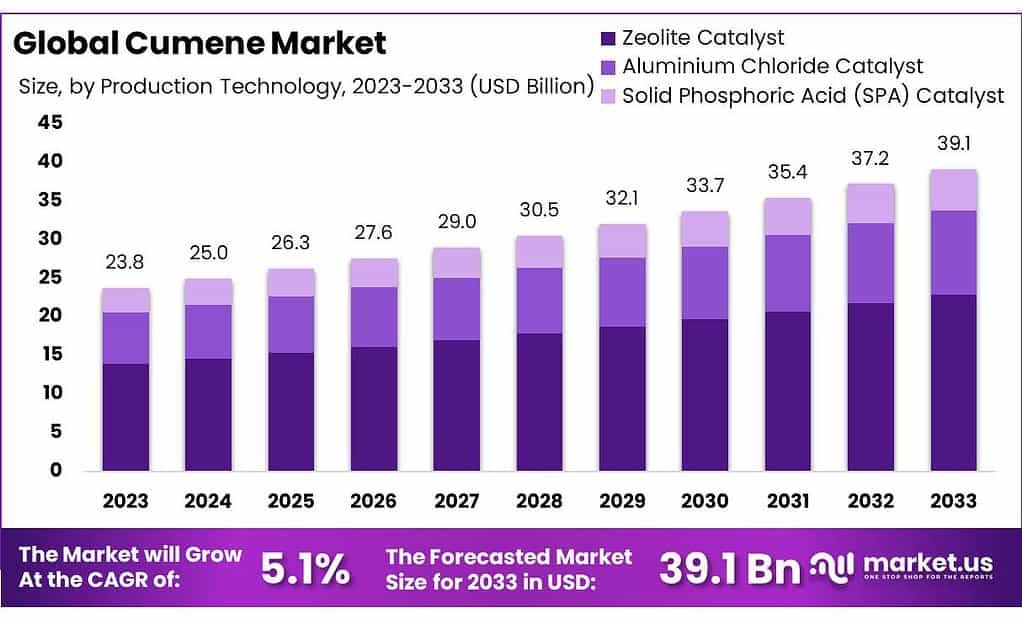

The global Cumene Market size is expected to be worth around USD 39.1 billion by 2033, from USD 23.8 billion in 2023, growing at a CAGR of 5.1% during the forecast period from 2023 to 2033.

Cumene market data is vital for stakeholders across various industries, such as plastics, automotive, and solvents, as it provides extensive information about the market size, growth trends, and forecasts. This data is segmented by application, geographic distribution, competitive landscape, and financial performance of major companies. Given cumene’s role in the production of phenol and acetone—both crucial to numerous industrial applications—the market dynamics of cumene directly impact these sectors.

Market reports on cumene offer deep insights into the factors influencing the market, including technological advancements, regulatory changes, macroeconomic trends, and supply chain developments.

These reports typically perform a SWOT analysis to identify drivers, restraints, opportunities, and threats, offering a comprehensive overview that aids businesses, investors, and policymakers in understanding the potential challenges and opportunities within the market. For instance, a surge in output from the automotive industry could elevate the demand for cumene-derived products, which in turn would influence market growth strategies and decision-making processes in related industries.

Focusing on specific regions, such as Taiwan, the cumene industry showcases significant developments with robust installed plant capacities and cutting-edge production technologies. As of 2023, Taiwan’s commitment to fulfilling both domestic and international demand is evident through its considerable infrastructure geared towards cumene production.

Moreover, strategic investments are prominent within the sector. Notably, INEOS is expanding its production capabilities with a new facility in Germany designed to produce 75 kilotons of cumene annually, reflecting a strategy to cater to future market demands efficiently.

Additionally, the acquisition of Axiall Corporation by INEOS Americas LLC for $62.9 million, which includes a cumene production facility with a capacity of 900,000 tons, highlights significant market expansion and acquisition strategies aimed at bolstering market position and meeting growing consumer demands. These examples illustrate the dynamic nature of the cumene market and its critical impact on related industrial sectors.

Key Takeaways

- The cumene market is projected to grow from USD 23.8 billion in 2023 to USD 39.1 billion by 2033, at a 5.1% CAGR.

- Zeolite Catalyst dominated in 2023, capturing over 58.4% market share due to high efficiency and reduced energy costs.

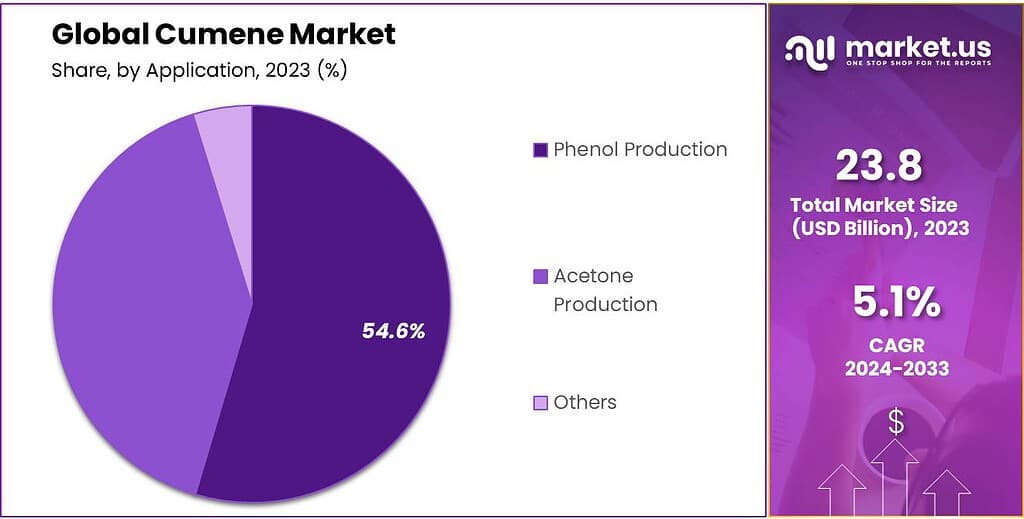

- Phenol production held a 54.6% share in 2023, driven by its use in manufacturing plastics and related compounds.

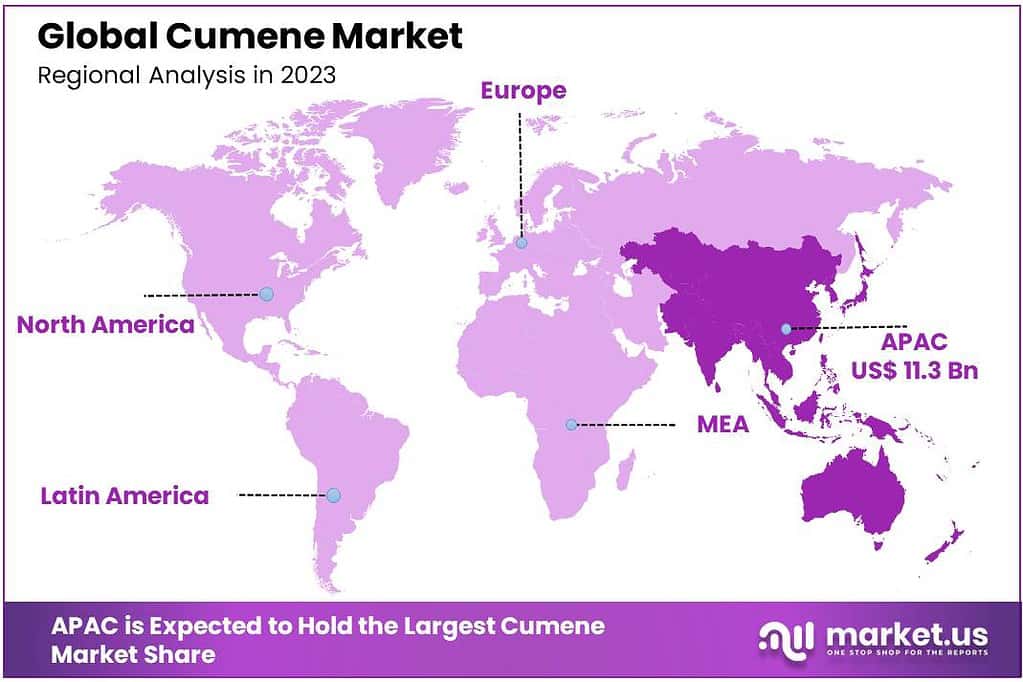

- Asia-Pacific holds a 47.6% market share, valued at USD 11.37 billion, driven by industrial growth in China and India.

By Production Technology

In 2023, the Zeolite Catalyst segment held a dominant position in the cumene market, capturing more than a 58.4% share. This technology is favored due to its high efficiency and selectivity in the cumene production process. Zeolite catalysts are renowned for their durability and ability to facilitate reactions at lower temperatures, which significantly reduces energy costs and enhances overall production sustainability.

The Aluminium Chloride Catalyst segment also plays a crucial role in the cumene market. Although it holds a smaller market share compared to Zeolite Catalysts, it is valued for its effectiveness in specific production environments where high reaction speeds are necessary. This catalyst type is particularly advantageous in setups that prioritize rapid throughput alongside high yield, making it a critical component of the cumene production landscape.

Solid Phosphoric Acid (SPA) Catalysts are another key technology in cumene production. While they command a lesser share of the market, SPA catalysts are essential for their unique properties, such as the ability to produce high-purity cumene, which is crucial for certain high-grade applications. The SPA Catalyst is particularly favored in processes where the control of by-product formation is critical, thus ensuring the quality and purity of the cumene produced.

By Application

In 2023, Phenol Production held a dominant market position within the cumene market, capturing more than a 54.6% share. This segment’s strength stems from the widespread use of phenol in the manufacture of plastics and related compounds, which are essential in industries ranging from automotive to electronics. The demand for phenol significantly influences the cumene market dynamics, as cumene is a primary feedstock in phenol production.

Acetone Production also constitutes a significant application of cumene, though it commands a smaller share compared to Phenol Production. Acetone is utilized extensively as a solvent in the pharmaceutical, cosmetics, and plastics industries. Its production using cumene highlights the versatility and critical role of cumene in meeting various industrial needs.

By End-Use

In 2023, the Petrochemical Industry held a dominant market position in the cumene market. This sector extensively utilizes cumene for the production of essential chemicals like phenol and acetone, which are integral to various manufacturing processes. The reliance on cumene for these derivatives underpins its significant share in the market, highlighting its importance in synthesizing compounds critical to the petrochemical industry’s operations.

The Automotive sector also significantly benefits from cumene, particularly in the production of plastics and resins used in vehicle manufacturing. These materials contribute to the lightweight and durable components that are vital for modern automotive design, underscoring cumene’s role in this industry.

In the Electronics industry, cumene derivatives are used in making components that require precise and durable plastics, such as in computers and mobile devices. The material properties enhanced by cumene derivatives are crucial for the industry’s demand for high-quality, reliable products.

The Construction industry utilizes cumene-related products to produce insulation materials and other construction chemicals that improve the durability and efficiency of building projects. This application highlights the versatility of cumene as a chemical precursor in a variety of construction applications.

Key Market Segments

By Production Technology

- Zeolite Catalyst

- Aluminium Chloride Catalyst

- Solid Phosphoric Acid (SPA) Catalyst

By Application

- Phenol Production

- Acetone Production

- Others

By End-Use

- Petrochemical Industry

- Automotive

- Electronics

- Construction

- Others

Driving Factors

Rising Demand for Phenol and Acetone: A Key Driver in the Cumene Market

A significant driving force in the cumene market is the rising demand for phenol and acetone, two primary derivatives produced from cumene. This increase is anchored by their extensive applications across several critical industries, including plastics, automotive, and electronics. Phenol and acetone are essential in producing polycarbonate plastics, epoxy resins, and other polymers that are integral to modern manufacturing.

The global demand for phenol, which is projected to drive the cumene market further, is supported by its extensive use in the production of bisphenol A—an essential component in polycarbonate plastic production. Polycarbonate plastics are vital for manufacturing various consumer goods, such as electronic devices, automotive components, and construction materials. This growth directly correlates to an increased demand for cumene as a precursor chemical.

Moreover, the market dynamics for acetone are influenced by its role in solvent applications and its use in synthesizing methyl methacrylate and bisphenol A. Acetone’s versatility as a solvent—used in everything from nail polish remover to paint thinner—ensures its steady demand in both industrial and consumer markets.

Furthermore, governmental and regulatory developments also support the cumene market’s growth. Initiatives aimed at reducing environmental impact and promoting sustainable chemical manufacturing processes are prompting the petrochemical industry to innovate and improve the efficiency of cumene production technologies. This includes advancements in catalysis and process optimization to reduce waste and energy consumption, aligning with global sustainability goals.

The expansion of the automotive and electronics sectors, particularly in Asia-Pacific regions such as China and India, where consumer markets are rapidly growing, also bolsters the cumene market. As these economies expand, the demand for consumer goods that rely on cumene derivatives continues to soar. For instance, the automotive industry’s shift towards more sustainable materials and lighter vehicles increases the demand for polycarbonates and phenol-derived resins, pushing the cumene market upward.

Restraining Factors

Health and Environmental Concerns: Major Restraints in the Cumene Market

A significant restraining factor in the cumene market is the health and environmental concerns associated with its production and use. Cumene is recognized as a hazardous chemical, with exposure potentially leading to health issues such as skin irritation, respiratory problems, and other serious health risks. These health concerns are heightened by cumene’s classification as a volatile organic compound (VOC), which contributes to air pollution and has implications for environmental health.

Regulatory bodies across the globe have imposed stringent regulations on the use and handling of hazardous chemicals, including cumene. These regulations often require companies to invest in expensive safety measures and pollution control technologies, which can increase operational costs and limit market growth. For example, compliance with environmental safety standards can lead to increased processing time and reduced efficiency, impacting the overall productivity of cumene production facilities.

Moreover, the public and governmental pressure for more environmentally friendly and sustainable industrial practices continues to grow. This societal shift has prompted industries to explore and adopt greener alternatives to cumene, which could potentially lead to a decline in its market size if viable substitutes are found and become commercially popular. The push for sustainability affects not only regulatory practices but also consumer and industrial end-user preferences, further influencing the global demand dynamics for cumene.

Thus, while cumene remains a critical component in the production of phenol and acetone—widely used in the manufacture of plastics and solvents—the health risks and environmental impact associated with its use are significant factors that could restrain its market growth. Companies operating in the cumene market must navigate these challenges by improving safety standards, reducing emissions, and possibly innovating less harmful production methods to sustain their market positions.

Growth Opportunities

Expanding Use in High-Octane Aviation Fuels: A Growth Opportunity for Cumene

A notable growth opportunity for the cumene market lies in its increasing utilization in the production of high-octane aviation fuels. The aviation industry’s expansion, particularly in regions like Asia-Pacific, drives this demand. As airlines seek more efficient and cleaner-burning fuels to reduce environmental impact and improve engine performance, cumene’s role as a component in gasoline blends used for aviation fuel becomes increasingly critical.

In China, the aviation sector is experiencing significant growth, with forecasts predicting the need for over 8,500 new commercial aircraft by 2040. This surge is expected to increase the demand for aviation fuels, where cumene’s high-octane properties make it a valuable additive. The growth in domestic air travel and the expansion of the civilian aircraft fleet in China, which includes a notable number of general aviation aircraft, further underscores the expanding market for cumene-based aviation fuels.

Moreover, the global push towards more sustainable aviation fuels aligns with environmental goals, adding an impetus to refine fuel compositions to include components like cumene that can enhance fuel efficiency and reduce emissions. This trend presents a significant opportunity for cumene producers to capitalize on the growing aviation sector, particularly in rapidly developing regions.

The strategic expansions by major chemical companies in cumene production capabilities, aimed at meeting the anticipated rise in demand, are indicative of the market’s response to these opportunities. Investments in production facilities and technological advancements in cumene synthesis are poised to boost supply, aligning with the expected increase in demand from the aviation fuel sector.

This alignment of market forces and industrial strategies points to a robust growth trajectory for the cumene market, driven by its critical role in aviation fuel production.

Latest Trends

Expanding Use of Cumene in High-Value Applications: A Key Trend

A major trend in the cumene market is its growing use in high-value applications, such as the production of Bisphenol A (BPA), which is derived from phenol and acetone, both cumene derivatives. BPA is extensively used in manufacturing polycarbonate and epoxy resins, which are crucial for a variety of industries, including automotive, electronics, and construction due to their strength and durability. The demand for these resins is projected to drive significant consumption of cumene.

Additionally, the market sees a substantial influence from the pharmaceutical, cosmetics, and electronics sectors, which utilize acetone derived from cumene. Acetone’s effectiveness in removing nail polish and oil stains and its application in cleaning electronic gadgets further underpin cumene’s utility in domestic and industrial settings. This versatility of acetone enhances the overall demand for cumene.

The Asia-Pacific region, particularly China and India, is experiencing rapid industrialization, leading to increased demand for cumene. These countries are expanding their petrochemical capacities and infrastructure, which is expected to support the cumene market growth. Government initiatives aimed at boosting local chemical production also play a critical role in this trend. For instance, projects like the construction of petrochemical plants in India that include facilities for cumene production are indicative of this strategic focus.

Overall, the cumene market is poised for growth, driven by its critical role in the production of essential chemicals and supported by expanding industrial activities and strategic governmental initiatives in key regions.

Regional Analysis

In the global cumene market, regional dynamics play a pivotal role in shaping production, consumption, and market trends. Asia Pacific (APAC) emerges as the dominant region, commanding a substantial 47.6% market share valued at USD 11.37 billion. This dominance is driven by robust industrialization in countries like China and India, where cumene is extensively used in phenol production for various applications including resins, adhesives, and coatings. The region’s strong economic growth, coupled with expanding manufacturing sectors, fuels the demand for cumene, bolstering its market position.

North America follows closely, characterized by a mature market landscape supported by advanced technologies and stringent environmental regulations. The region accounts for a significant share due to steady demand from end-use industries such as automotive, electronics, and construction. In Europe, cumene demand is influenced by the presence of key chemical manufacturing hubs and stringent regulatory frameworks promoting sustainable practices. The market here is driven by applications in pharmaceuticals, agriculture, and consumer goods, contributing to stable market growth.

The Middle East & Africa region shows promising growth prospects attributed to increasing investments in petrochemical infrastructure and industrial diversification initiatives. The market benefits from abundant feedstock availability and strategic geographical positioning, enhancing production capacities and supply chain efficiencies. Latin America, although smaller in market share, is experiencing gradual expansion driven by rising industrial activities and infrastructure development across key economies like Brazil and Mexico.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Cumene market features a diverse array of key players driving its dynamics and growth. Prasol Chemicals Pvt Ltd., Total S.A., Versalis S.p.A., and Borealis are prominent contributors, leveraging their extensive expertise in chemical production and distribution. These companies play pivotal roles in meeting global demand for cumene, which serves as a crucial intermediate in the manufacturing of phenol and acetone.

Saudi Basic Industries Corporation (SABIC), Royal Dutch Shell plc, and Cepsa also occupy significant positions in the market. Their robust production capabilities and strategic investments bolster the supply chain for cumene, supporting various industries dependent on phenol and acetone derivatives. Additionally, Dow Chemical Company, Sumitomo Chemical Co., LG Chem Ltd., and China Petroleum & Chemical Corporation (Sinopec) are key players known for their substantial contributions to the cumene market, ensuring reliable supply chains and technological advancements.

Further strengthening the market landscape are INEOS, Kumho P&B Chemicals Inc., Dow, and Koch Industries Inc., each bringing unique strengths and capabilities to the production and distribution of cumene. Their strategic initiatives, including capacity expansions and technological innovations, underscore their commitment to meeting global demand while adapting to evolving market trends and regulatory landscapes.

Market Key Players

- Prasol Chemicals Pvt Ltd.

- Total S.A.

- Versalis S.p.A.

- Borealis

- Saudi Basic Industries Corporation

- Royal Dutch Shell plc

- Cepsa

- Dow Chemical Company

- Sumitomo Chemical Co.

- LG Chem Ltd.

- China Petroleum & Chemical Corporation

- INEOS

- Kumho P&B Chemicals Inc.

- Dow

- Koch Industries Inc.

Recent Development

In January 2023 Prasol Chemicals Pvt Ltd. with 5,000 metric tons of cumene produced, which increased to 6,000 tons by April to meet heightened seasonal demand.

In 2023, Total S.A. began the year with a production volume of 20,000 metric tons of cumene in January, steadily increasing to 22,000 tons by March to meet growing market demands.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 23.8 Bn |

| Forecast Revenue (2033) | US$ 39.1 Bn |

| CAGR (2024-2033) | 5.1% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Production Technology(Zeolite Catalyst, Aluminium Chloride Catalyst, Solid Phosphoric Acid (SPA) Catalyst), By Application(Phenol Production, Acetone Production, Others), By End-Use(Petrochemical Industry, Automotive, Electronics, Construction, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Prasol Chemicals Pvt Ltd., Total S.A., Versalis S.p.A., Borealis, Saudi Basic Industries Corporation, Royal Dutch Shell plc, Cepsa, Dow Chemical Company, Sumitomo Chemical Co., LG Chem Ltd., China Petroleum & Chemical Corporation, INEOS, Kumho P&B Chemicals Inc., Dow, Koch Industries Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

Cumene Market size is expected to be worth around USD 39.1 billion by 2033, from USD 23.8 billion in 2023

The Cumene Market is expected to grow at a CAGR of 5.1% during 2023-2032.

Prasol Chemicals Pvt Ltd., Total S.A., Versalis S.p.A., Borealis, Saudi Basic Industries Corporation, Royal Dutch Shell plc, Cepsa, Dow Chemical Company, Sumitomo Chemical Co., LG Chem Ltd., China Petroleum & Chemical Corporation, INEOS, Kumho P&B Chemicals Inc., Dow, Koch Industries Inc.