Quick Navigation

- Report Overview

- Key Takeaways

- Analyst’s Viewpoint

- U.S. Market Analysis

- Component Analysis

- Type Analysis

- Range Analysis

- Technology Analysis

- Mitigation Analysis

- Defense Analysis

- End Use Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Top Opportunities for Players

- Recent Developments

- Report Scope

Report Overview

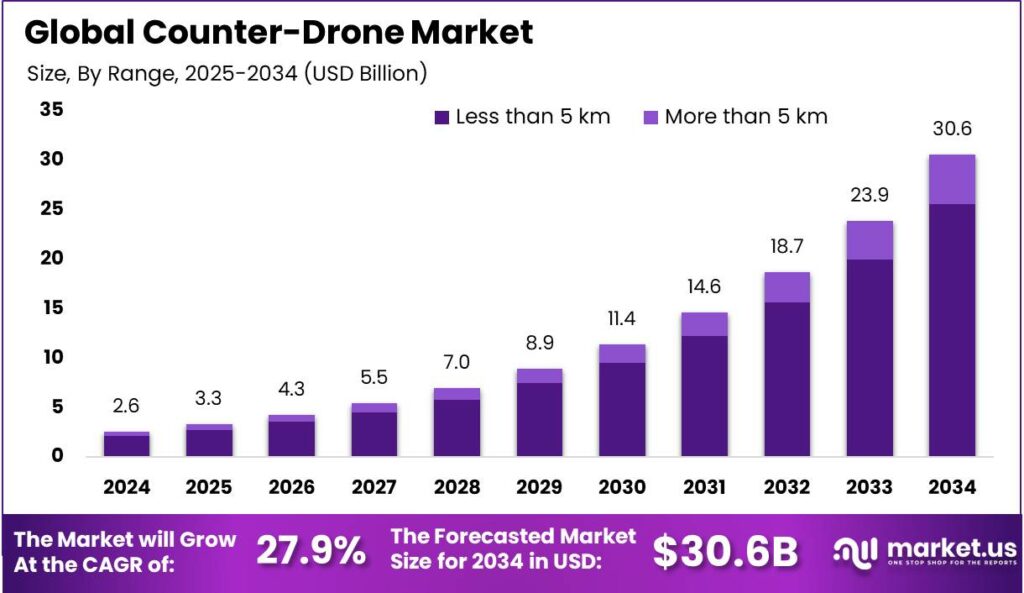

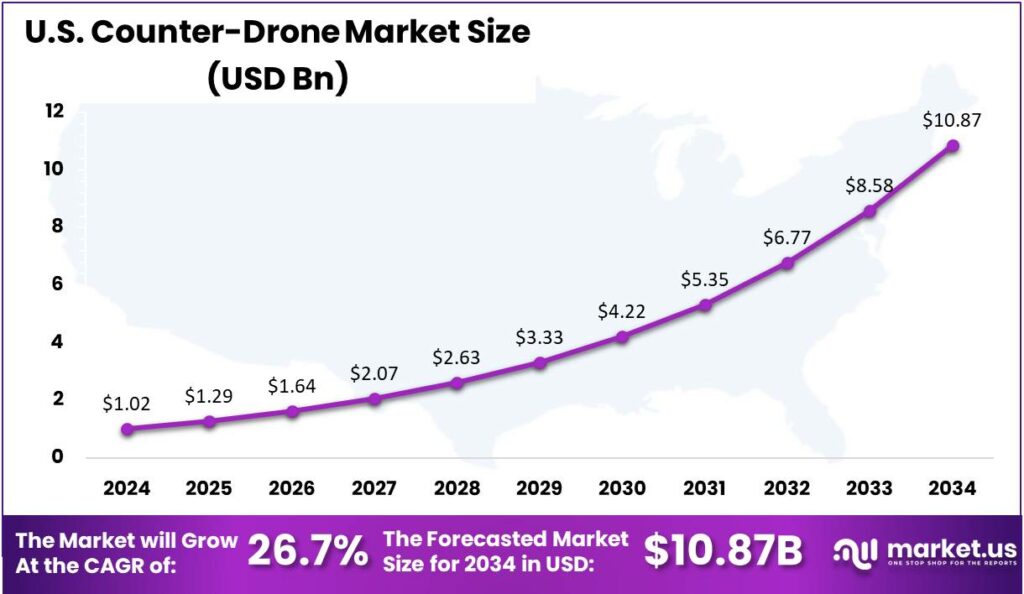

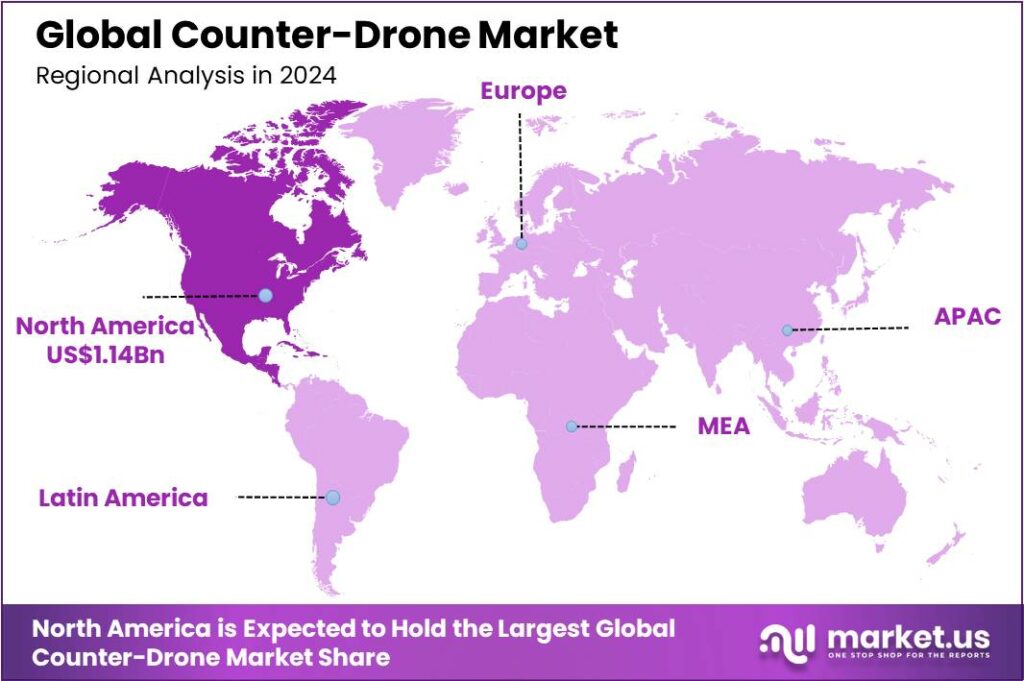

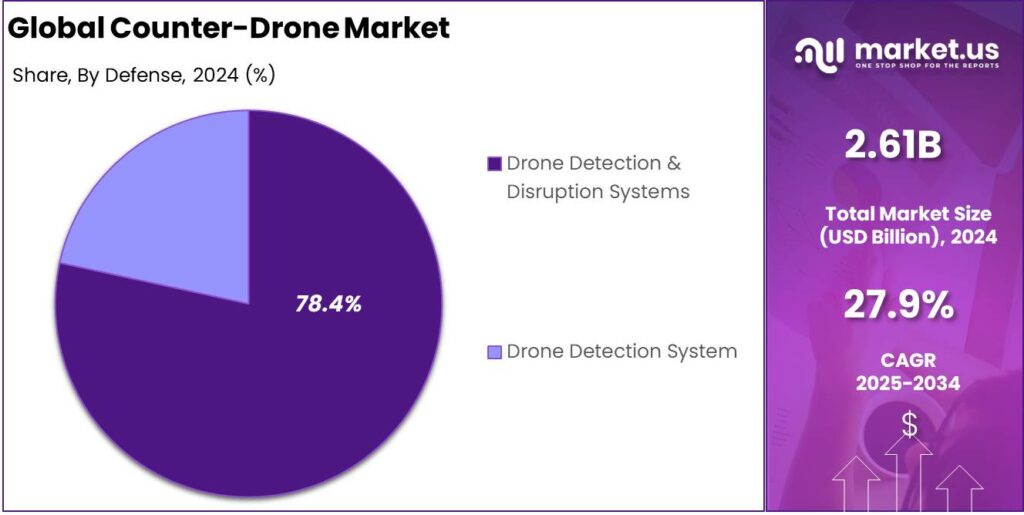

The Global Counter-Drone Market size is expected to be worth around USD 30.6 Billion By 2034, from USD 2.61 Billion in 2024, growing at a CAGR of 27.90% during the forecast period from 2025 to 2034. In 2024, North America led the market with a 43.7% share, generating about USD 1.14 billion. The U.S. market accounted for USD 1.02 billion, highlighting its rising strategic role in defense and security, with a projected CAGR of 26.7%.

Counter-drone technology, often referred to as anti-drone systems, encompasses a range of solutions designed to detect, track, and neutralize unauthorized or malicious drones. These systems are crucial in safeguarding sensitive areas such as airports, military installations, and public events from potential threats posed by unmanned aerial vehicles (UAVs).

Key factors driving the counter-drone market are rapid drone tech advances, rising drone-related threats, and growing airspace security demands. Public safety, stadiums, and corporate sites are adopting drone detection as part of security. Growing drone breaches and awareness among local authorities fuel steady demand for scalable, reliable solutions.

Key Takeaways

- The Global Counter-Drone Market size is expected to grow from USD 2.61 Billion in 2024 to approximately USD 30.6 Billion by 2034, with a CAGR of 27.90% during the forecast period from 2025 to 2034.

- In 2024, the Hardware segment dominated, capturing more than 69.2% share in the global counter-drone market.

- The Ground Based segment held a leading position in 2024, accounting for more than 76.8% of the global counter-drone market.

- The Less than 5 km range segment was dominant in 2024, with over 83.7% share of the global counter-drone market.

- Among technologies in 2024, the Anti-drone Radar segment captured more than 56.1% share of the global counter-drone technology landscape.

- The Destructive System segment led the counter-drone mitigation market in 2024, with a commanding 82.6% share.

- In terms of application, the Drone Detection & Disruption Systems segment dominated, holding more than 78.4% share in the global counter-drone market in 2024.

- The Military & Defense segment was the largest end-user in 2024, capturing over 61.8% of the global counter-drone market.

- Regionally, North America dominated the market in 2024, holding over 43.7% share with revenues of approximately USD 1.14 billion.

- The U.S. Counter-Drone market reached USD 1.02 billion in 2024, emphasizing its growing strategic importance in defense, infrastructure security, and public safety, with a strong projected CAGR of 26.7%.

Analyst’s Viewpoint

Technological advances drive counter-drone evolution, with AI analytics, advanced sensors, and RF detection enhancing accuracy and response. Indigenous micro-missile systems mark a key innovation, enabling mobile, precise UAV neutralization. These developments are vital to tackling evolving drone threats effectively.

The regulatory environment is crucial in shaping the counter-drone market. Governments worldwide are implementing laws to regulate drone use and require anti-drone systems in sensitive areas. These regulations drive investments and establish a standardized framework that supports market growth.

Investments in the counter-drone sector are increasing as public and private entities prioritize airspace security. With applications in defense, commercial, and public safety sectors, the market offers abundant opportunities. Companies are boosting R&D to enhance anti-drone technologies, while rising drone incidents drive governments to allocate resources for effective countermeasures.

Counter-drone systems offer benefits beyond security, ensuring operational continuity by preventing disruptions from unauthorized drones. They safeguard intellectual property, protect privacy, and enhance public safety. In aviation, energy, and defense, these measures are essential for risk management and regulatory compliance.

U.S. Market Analysis

In 2024, the U.S. Counter-Drone market reached a significant valuation of USD 1.02 billion, marking a clear indication of its growing strategic importance in national defense, critical infrastructure protection, and public safety.This market has become vital in security and surveillance due to the growing threat from unauthorized and potentially malicious unmanned aerial systems (UAS).

The market is experiencing remarkable momentum, with a projected CAGR of 26.7%, reflecting the urgency among stakeholders to implement effective drone mitigation systems. Key technologies like radar, RF jamming, electro-optical sensors, and directed energy weapons are driving growth, enabling real-time detection, identification, and neutralization of rogue drones within layered defense systems.

The U.S. counter-drone market is rapidly expanding beyond military use, driven by rising demand from civilian sectors like airports, stadiums, and critical infrastructure. Regulatory efforts by the FAA, along with growing public awareness and increased R&D investment, are positioning the market for significant growth, strengthening national defense against aerial threats.

In 2024, North America held a dominant market position, capturing more than a 43.7% share of the global counter-drone market, with total revenues reaching approximately USD 1.14 billion. This leadership is primarily attributed to the region’s robust defense spending, cutting edge technology infrastructure, and strong governmental support for unmanned aerial system (UAS) countermeasures.

North America’s strong defense infrastructure and R&D investments have driven the rise of advanced counter drone technologies. U.S. based companies like WhiteFox Defense and Dedrone lead in developing detection and mitigation systems, now used beyond the military by law enforcement and private sectors to protect against drone threats.

The region’s strong regulatory environment is key to its counter-drone market leadership. With stringent FAA guidelines and active legislative efforts to improve drone detection and mitigation, North America has built a supportive framework that encourages the widespread adoption of counter-drone technologies across sectors.

North America’s focus on public safety and national security is driving strong demand for counter-drone solutions. Protecting major events, critical infrastructure, and borders requires effective mitigation as drone misuse rises. These factors ensure the region’s continued leadership and growth in the counter-drone market.

Component Analysis

In 2024, the Hardware segment held a dominant market position, capturing more than a 69.2% share in the global counter-drone market. This stronghold can be attributed to the physical necessity of devices like radars, RF detectors, and jamming systems for real-time drone detection and neutralization.

Radars and RF detectors are vital for early drone detection, widely used in defense sites, airports, and large venues requiring rapid response. Their effectiveness in tracking diverse drones makes hardware favored over software in security system upgrades.

Infrared and video surveillance systems are further enhancing the precision of hardware offerings. By integrating thermal imaging and visual tracking, these devices allow operators to visually confirm drone threats even in low-visibility conditions. Their effectiveness in 24/7 monitoring environments, such as national borders and industrial plants, has driven broader adoption among civil and military agencies, solidifying the segment’s growth.

While software plays a supportive and increasingly intelligent role in system coordination and data analysis, the market still largely relies on tangible infrastructure for threat mitigation. Jammers and acoustic sensors, capable of disrupting communication between drones and their operators, continue to be a preferred choice in urban and high-risk zones.

Type Analysis

In 2024, the Ground Based segment held a dominant market position, capturing more than a 76.8% share of the global counter-drone market. This dominance is largely driven by the segment’s wide adaptability across both civilian and defense sectors.

Mobile ground-based systems, a sub-category in this segment, are rapidly gaining traction for their operational flexibility. Mounted on vehicles, they provide temporary protection for convoys, events, and infrastructure in dynamic settings. The U.S. military and law enforcement use these mobile counter-drone platforms for border patrols and large gatherings, valuing their wide coverage and easy repositioning for mission-critical security.

The Handheld segment, though compact and cost-effective, holds a smaller market share. Used mainly by security and law enforcement for short-range drone disruption, these portable devices provide quick responses but are limited by range and manual operation. Despite this, their use is growing for crowd control and localized protection amid rising urban drone threats.

UAV-based counter-drone systems are still in early development. These drones detect, track, and intercept rogue UAVs but face challenges like regulations, limited maturity, and high costs. Currently used mainly in specialized military trials, they hold future potential as autonomous and swarm technologies advance for aerial security.

Range Analysis

In 2024, the Less than 5 km segment held a dominant market position, capturing more than 83.7% share of the global counter-drone market. This dominance is primarily attributed to the widespread deployment of short-range counter-drone systems across critical infrastructures such as airports, government buildings, and stadiums, where threats are most likely to emerge from drones operating within close proximity.

The growing number of drone-related incidents within city environments has increased the demand for localized and precise countermeasures. As most unauthorized or rogue drones operate within a limited range, security agencies and facility managers are increasingly investing in short-range counter-UAV technologies.

The Less than 5 km segment leads due to growing regulatory focus on localized drone mitigation near sensitive areas like airports and public events. Short-range systems using RF jamming, electro-optical detection, and portable radar offer accurate, affordable surveillance and rapid neutralization, appealing to both military and commercial users.

In contrast, systems with ranges beyond 5 km are costly, complex, and suited for battlefield or long-range surveillance, requiring larger infrastructure and power. This limits their use to defense and specialized sectors. Meanwhile, rising urbanization, drone misuse, and demand for quick, deployable solutions keep the Less than 5 km counter-drone segment dominant globally.

Technology Analysis

In 2024, Anti-drone Radar segment held a dominant market position, capturing more than a 56.1% share in the global counter-drone technology landscape. This strong foothold is primarily driven by the radar system’s proven effectiveness in detecting and tracking drones over long distances and under varied weather conditions.

One of the key reasons why anti-drone radar has outpaced other technologies such as RF scanning or thermal imaging lies in its versatility and scalability. These systems are capable of identifying multiple aerial threats simultaneously, whether swarming drones or high-speed UAVs, making them suitable for large-area surveillance.

From a commercial standpoint, radar-based systems are increasingly favored by government and private sector entities due to their reduced false-alarm rate compared to RF-based solutions, which can often be disrupted by crowded signal environments. Their superior ability to differentiate between bird movements and drones adds an extra layer of security, particularly in urban and perimeter-protected zones.

Additionally, regulatory frameworks across regions have started to emphasize the adoption of non-intrusive and accurate detection technologies. Anti-drone radar fits this demand well by providing a passive, non-jamming solution that aligns with aviation and defense compliance standards.

Mitigation Analysis

In 2024, the Destructive System segment held a dominant market position, capturing more than a 82.6% share of the global counter-drone mitigation market. This dominance is largely attributed to the growing need for immediate and decisive neutralization of hostile drones, especially in high-risk zones like military bases, government facilities, and conflict-prone borders.

Laser systems are rapidly gaining popularity for their precise targeting and cost-effective operation. Unlike kinetic methods, lasers can engage multiple threats quickly without ammo reloads. Their silent, non-explosive use makes them ideal for sensitive environments, making them a preferred choice for defense forces in advanced security setups.

Missile effectors provide long-range takedown of high-speed, high-altitude drones, crucial for strategic airspace defense. Electronic countermeasures disrupt drone navigation and communication, grounding threats early. Despite their destructive nature, precision targeting minimizes unintended impacts, reflecting advances in balancing power with control.

The preference for destructive counter-drone systems reflects global security shifts toward hard deterrence. Governments are boosting defense budgets for real-time neutralization capabilities. In tense geopolitical climates, these systems act as strong deterrents, reducing drone incursions. This mix of effectiveness, deterrence, and tech superiority keeps destructive systems dominant in counter-drone efforts.

Defense Analysis

In 2024, Drone Detection & Disruption Systems segment held a dominant market position, capturing more than a 78.4% share in the global counter-drone market. This segment’s leadership is primarily driven by its dual capability to not only identify unauthorized drones but also to neutralize or redirect them in real time.

The rising concern over drone-based surveillance, smuggling, and potential weaponization has compelled governments and enterprises to invest in systems that can actively prevent incidents. Drone Detection & Disruption Systems use a combination of radar, radio frequency analysis, and electro-optical sensors to detect UAVs, while integrated jamming, spoofing, or kinetic countermeasures disable them.

Another key factor driving the dominance of this segment is the increasing number of mandates and security guidelines issued by defense ministries and aviation authorities globally. Countries like the U.S., UK, India, and Israel have accelerated their procurement of integrated counter-UAV systems to safeguard military bases, airports, and VIP convoys.

Moreover, advancements in artificial intelligence and machine learning are enhancing the capabilities of these systems, making them smarter and faster in threat assessment. Real-time decision-making, automated threat prioritization, and the ability to distinguish between friend and foe are significantly improving operational efficiency.

End Use Analysis

In 2024, Military & Defense segment held a dominant market position, capturing more than a 61.8% share in the global counter-drone market. The stronghold of this segment is largely due to the increasing deployment of drones in modern warfare and surveillance missions by adversarial forces. Military operations are now more vulnerable to threats from rogue drones used for spying, delivering explosives, or disrupting communication systems.

One of the key advantages of the Military & Defense segment is the availability of large-scale budgets and government funding, enabling extensive R&D and rapid adoption of cutting-edge solutions. Unlike commercial or civilian use cases, the military’s requirements often include highly specialized systems with the capability to detect, track, and neutralize drones even in complex battlefield scenarios.

Geopolitical tensions and border skirmishes have heightened the demand for strong aerial threat mitigation. Nations like the U.S., China, Russia, and India are increasing investments in military-grade anti-drone tech, from fixed sites to mobile armored units. This urgency makes Military & Defense the leading segment in implementation scale and tech sophistication.

Ongoing innovations in drone warfare push militaries to adopt advanced countermeasures against swarms, autonomous UAVs, and long-range threats. This drives partnerships between defense agencies and tech firms, accelerating AI-powered, automated systems. As drone threats evolve, Military & Defense will continue leading the counter-drone market in demand and influence.

Key Market Segments

By Component

- Hardware

- Radars

- Acoustic Sensors

- Infrared and Video Surveillance Systems

- RF Detectors

- Jammers

- Others

- Software

By Type

- Ground Based

- Fixed

- Mobile

- Handheld

- UAV Based

By Range

- Less than 5 km

- More than 5 km

By Technology

- Anti-drone Radar

- RF Scan

- Thermal Image

- Others

By Mitigation

- Destructive System

- Laser System

- Missile Effector

- Electronic Countermeasure

- Non-destructive System

By Defense

- Drone Detection & Disruption Systems

- Drone Detection System

By End Use

- Military & Defense

- Commercial

- Government

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Rising Security Threats from Drones

Drones have become more affordable and widely used across sectors, but this has also enabled their misuse. In certain border regions, drones are used to smuggle contraband like drugs and weapons, raising serious concerns for local communities and security forces. The constant fear among residents highlights the urgent need for effective counter-drone measures.

To address these threats, innovative solutions are being developed. For instance, Indrajaal, a Hyderabad-based company, has introduced an AI-driven anti-drone system designed to protect critical infrastructure. This system integrates advanced threat detection with tools like sensors and jammers, aiming to secure large areas from drone intrusions. Such advancements highlight the growing need for and investment in counter-drone technologies to ensure public safety and national security.

Restraint

Privacy and Civil Liberties Concerns

While counter-drone technologies are essential for security, they raise significant privacy and civil liberties issues. These systems often involve surveillance measures that can inadvertently infringe upon individuals’ privacy rights. For example, deploying counter-drone solutions may lead to the collection of personal data or interfere with lawful drone operations, such as those used for journalism or recreational purposes .

Moreover, the potential for misuse of these technologies by authorities or private entities adds to public apprehension. There’s a delicate balance between ensuring security and upholding individual freedoms. Without clear regulations and oversight, the deployment of counter-drone systems could lead to unintended consequences, eroding public trust and potentially violating legal standards.

Opportunity

Expanding Commercial Applications

Beyond security, counter-drone technologies offer vast opportunities in the commercial sector. Industries like logistics, agriculture, and entertainment are increasingly integrating drones into their operations. However, the risk of unauthorized drone activities necessitates protective measures. Implementing counter-drone solutions can safeguard assets, ensure operational continuity, and enhance safety protocols .

For instance, in agriculture, drones are used for crop monitoring and spraying. Counter-drone systems can prevent interference from rogue drones, ensuring that operations proceed without disruptions. Similarly, in events and entertainment, these technologies can protect venues from unauthorized aerial recordings or potential threats, enhancing the overall safety and experience for attendees.

Challenge

Technological Limitations and Evolving Threats

One of the significant challenges in counter-drone technology is keeping pace with the rapidly evolving drone landscape. Drones are becoming smaller, faster, and more autonomous, making them harder to detect and neutralize. Traditional detection methods, like radar and radio frequency analysis, often struggle with low-flying or non-communicative drones .

Additionally, mitigation techniques such as jamming or physical interception can have unintended consequences, including collateral damage or interference with other electronic systems . The dynamic nature of drone technology requires continuous innovation and adaptation in counter-drone measures. Developing flexible, multi-layered defense systems that can respond to diverse and sophisticated threats is essential but remains a complex and ongoing endeavor.

Emerging Trends

Counter-drone technology is advancing quickly due to the growing use of drones across industries. AI and machine learning significantly improve these systems by enhancing detection accuracy, predicting drone behavior, and automating responses. AI-driven solutions can analyze patterns to differentiate between harmless and threatening drones, enabling more effective threat assessment and response.

Counter-drone technologies are increasingly integrated into larger security frameworks. Systems like India’s Indrajaal Infra protect extensive areas, such as naval ports, by using AI-driven detection alongside jammers and spoofers to neutralize threats. This approach marks a shift toward proactive, adaptable drone defense.

Drone countermeasures often rely on detection systems like radar, RF analysis, acoustic sensors, and optical cameras. Radar detects drones at long range but struggles with small, low-flying ones. RF analysis works on signal-dependent drones but not autonomous ones. Acoustic sensors detect drone sounds but falter in noisy settings. Optical systems offer visual ID but are limited by lighting and weather.

Business Benefits

Counter-drone technology is increasingly essential, protecting critical facilities like power plants, airports, and ports from threats posed by unauthorized drones. These drones may carry harmful payloads or conduct surveillance, risking safety and operations. Counter-drone systems detect and neutralize these dangers to maintain secure and uninterrupted infrastructure functioning.

Drones equipped with cameras can infringe on personal privacy or corporate confidentiality. They might capture sensitive information without consent. Counter-drone technologies can detect and mitigate such intrusions, protecting individuals’ privacy and organizations’ proprietary data.

Drones are increasingly used for illegal activities like smuggling and unauthorized surveillance. Law enforcement uses counter-drone systems to detect and intercept these threats, supporting crime prevention and border security. These technologies also help manage drone traffic, ensuring safe operation and compliance with regulations.

Key Player Analysis

The Counter-Drone Market is rapidly evolving as security concerns around unauthorized drones increase globally.

Orelia is known for its specialized counter-drone systems that emphasize precision detection and safe neutralization methods. Their approach often integrates multi-sensor technologies, providing comprehensive protection without disrupting other wireless communications nearby.

Prime Consulting and Technologies offers a broad portfolio of counter-drone products with a strong emphasis on software-driven intelligence and analytics. Their systems excel in real-time drone identification and classification, enabling quick decision-making. Prime Consulting stands out for flexible deployment and strong integration with existing security setups, meeting diverse customer needs.

Raytheon Company, a major defense contractor, brings unmatched expertise and scale to the counter-drone market. Leveraging decades of experience in aerospace and defense, Raytheon develops cutting-edge counter-drone solutions that combine advanced radar systems, electronic warfare, and AI-powered tracking.

Top Key Players in the Market

- Lockheed Martin Corporation

- Orelia

- Prime Consulting and technologies

- Raytheon Company

- Saab AB

- Selex Es Inc.

- Thales Group

- The Boeing Company

- Advanced Radar Technologies S.A.

- Airbus SE

- Blighter Surveillance Systems

- Dedrone

- DeTect, Inc.

- Droneshield LLC

- Enterprise Control Systems

- Israel Aerospace Industries Ltd. (IAI)

- Liteye Systems, Inc.

- Others

Top Opportunities for Players

- Expanding Civilian Applications: As drones become more common in everyday life, there’s a growing need to protect public spaces like airports, stadiums, and power plants. This opens up avenues for companies to develop systems that ensure safety without causing disruptions. By focusing on non-intrusive detection and neutralization methods, businesses can cater to a broader market beyond military applications.

- Integration of Artificial Intelligence: Incorporating AI into counter-drone systems allows for quicker and more accurate threat detection. AI can help differentiate between harmless drones and potential threats, reducing false alarms. This technological advancement not only improves efficiency but also builds trust among users in various sectors.

- Development of Portable Solutions: There’s a rising demand for mobile counter-drone units that can be easily deployed in different locations. Portable systems are especially useful for events, temporary installations, or remote areas. Creating lightweight and user-friendly equipment can meet this need and expand market reach.

- Focus on Non-Destructive Technologies: Not all situations call for the destruction of drones. In many cases, safely intercepting or redirecting them is preferable. Developing non-lethal methods, such as signal jamming or controlled landings, can be more acceptable in civilian contexts and open up new business opportunities.

- Collaboration with Regulatory Bodies: Working closely with government agencies to shape policies and standards can position companies as industry leaders. By contributing to the development of regulations, businesses can ensure their technologies are compliant and favored in public sector contracts.

Recent Developments

- In March 2025, Saab AB introduced the “Loke” counter-drone system, developed in just 84 days. It’s a mobile system that detects, tracks, and neutralizes drones, enhancing Sweden’s defense capabilities.

- In March 2025, DroneShield LLC announced significant upgrades to its counter-drone systems at the Avalon Airshow, enhancing protection for critical infrastructure and military sites.

- In February 2025, Blighter Surveillance Systems launched BlighterNexus, an AI-powered hub that simplifies the integration of radar systems with command centers, improving drone detection and response times.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 2.61 Bn |

| Forecast Revenue (2034) | USD 30.6 Bn |

| CAGR (2025-2034) | 27.90% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Hardware (Radars, Acoustic Sensors, Infrared and Video Surveillance Systems, RF Detectors, Jammers, Others), Software), By Type (Ground Based (Fixed, Mobile), Handheld, UAV Based), By Range (Less than 5 km, More than 5 km), By Technology (Anti-drone Radar, RF Scan, Thermal Image, Others), By Mitigation (Destructive System (Laser System, Missile Effector, Electronic Countermeasure), Non-destructive System), By Defense (Drone Detection & Disruption Systems, Drone Detection System), By End Use (Military & Defense, Commercial, Government, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Lockheed Martin Corporation, Orelia, Prime Consulting and technologies, Raytheon Company, Saab AB, Selex Es Inc., Thales Group, The Boeing Company, Advanced Radar Technologies S.A., Airbus SE, Blighter Surveillance Systems, Dedrone, DeTect, Inc., Droneshield LLC, Enterprise Control Systems, Israel Aerospace Industries Ltd. (IAI), Liteye Systems, Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |