Global Cotton Seed Treatment Market Size, Share, And Industry Analysis Report By Chemical Origin (Synthetic, Biological), By Product Type (Insecticides, Fungicides, Others), By Application (On-farm, Commercial), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180850

- Number of Pages: 228

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

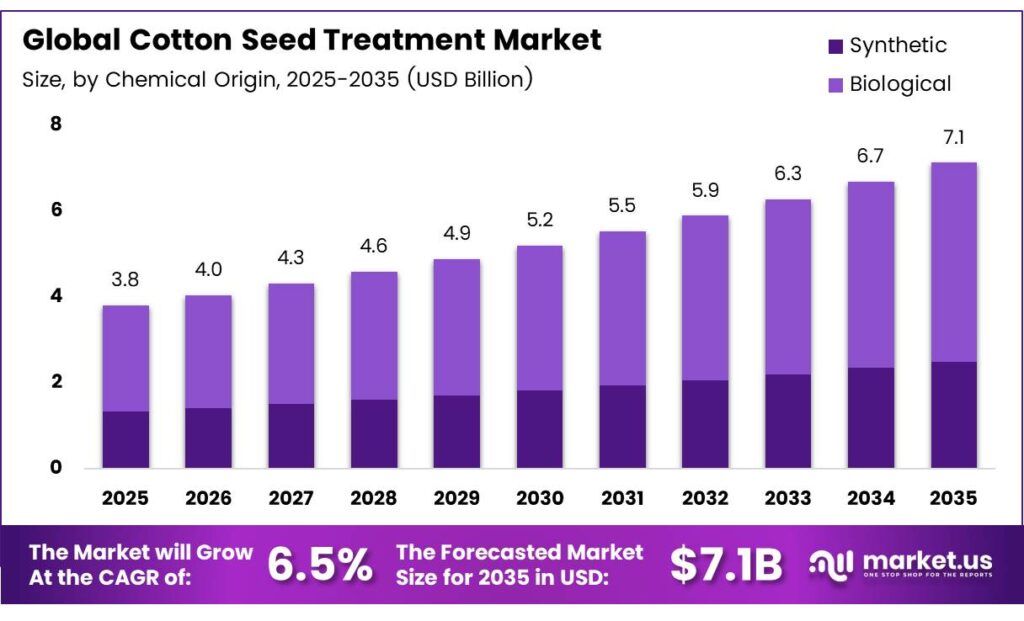

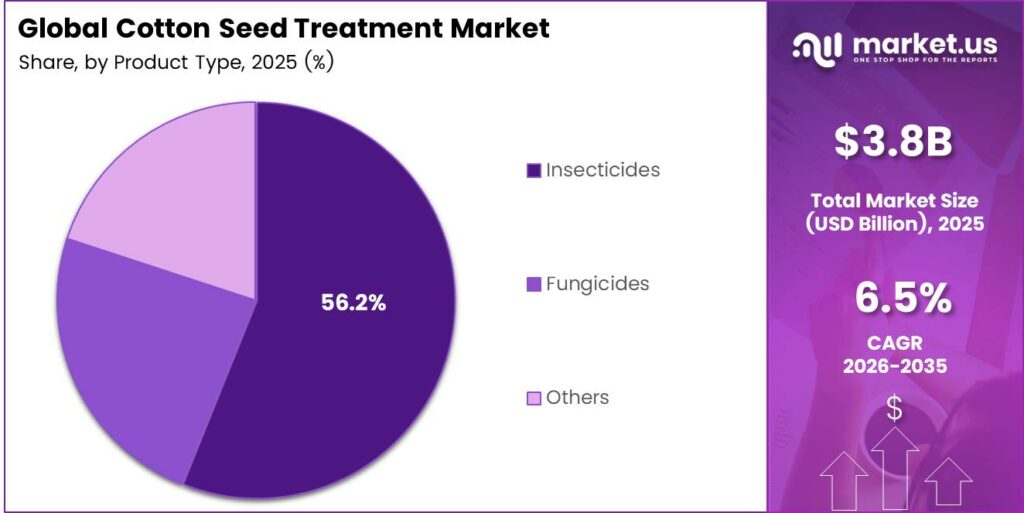

The Global Cotton Seed Treatment Market size is expected to be worth around USD 7.1 billion by 2035 from USD 3.8 billion in 2025, growing at a CAGR of 6.5% during the forecast period 2026 to 2035.

The cottonseed treatment market covers agrochemical and biological products applied directly to cotton seeds before planting. These treatments protect seeds from soil-borne pathogens, early-season insects, and environmental stresses. Consequently, treated seeds deliver better germination rates and stronger crop stands across diverse growing conditions.

Seed treatment products include fungicides, insecticides, and biological agents used in both on-farm and commercial application settings. Growers increasingly rely on these solutions to improve seedling vigor and reduce early crop losses. Moreover, seed treatment reduces the need for broader field applications of pesticides, making it a more targeted and cost-effective approach.

- Bayer recorded a €510 million impairment loss for its Cotton Seed cash-generating unit in 2024, tied to weaker anticipated business prospects. This reflects the competitive pressure reshaping seed treatment portfolios and signals the industry’s strategic shift toward higher-margin biological and combination products.

Government regulations across major cotton-producing regions are driving adoption of safer, bio-based treatment alternatives. Authorities in the US, India, and the European Union enforce strict guidelines on approved active ingredients for seed coatings. Therefore, manufacturers continue to innovate formulations that meet evolving regulatory standards while maintaining agronomic effectiveness.

- India’s output stands at 24.5 million 480-lb bales in MY2025/26 across 11.2 million hectares, confirming the country’s central role in global cotton supply chains. This large production base generates substantial demand for high-performance seed treatment solutions that protect yields at scale.

Investment in agricultural research and development supports the expansion of combination products that blend chemical and biological components. Seed companies and agrochemical firms actively collaborate to develop proprietary treatment technologies. Additionally, the growing organic cotton segment creates new demand for certified biopesticides and micronutrient-based seed treatments.

Key Takeaways

- The Global Cotton Seed Treatment Market is valued at USD 3.8 billion in 2025 and is projected to reach USD 7.1 billion by 2035 at a CAGR of 6.5% during the forecast period 2026 to 2035.

- The Synthetic segment dominates with a 76.9% market share in 2025.

- Insecticides hold the leading position with a 56.2% share in 2025.

- The On-farm segment leads with a 59.6% share in 2025.

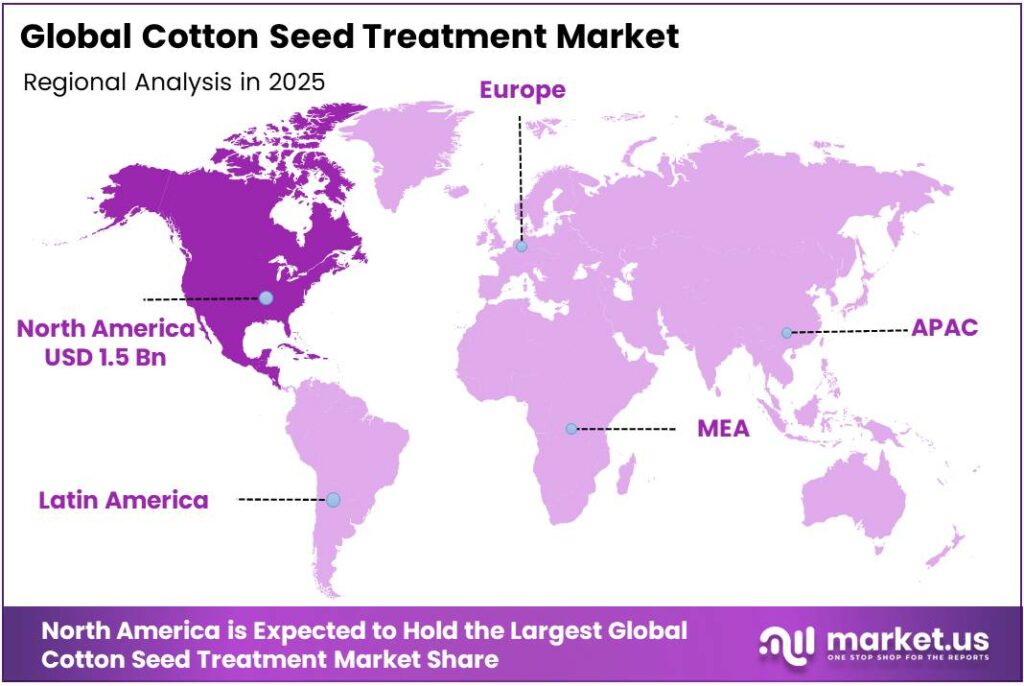

- North America is the dominant region, accounting for a 38.9% market share valued at USD 1.5 billion in 2025.

By Chemical Origin Analysis

Synthetic dominates with 76.9% due to broad-spectrum efficacy and established supply chains.

In 2025, Synthetic held a dominant market position in the By Chemical Origin segment of the Cotton Seed Treatment Market, with a 76.9% share. Synthetic treatments offer proven, broad-spectrum protection against a wide range of soil-borne pathogens and early-season pests. Moreover, their well-established manufacturing infrastructure and competitive pricing make them the preferred choice for large-scale commercial growers.

The Biological segment is growing steadily as growers seek environmentally safer treatment options. Bio-based seed treatments using microbial agents and plant-derived compounds reduce chemical residue concerns. Additionally, stricter government regulations on synthetic active ingredients are prompting agrochemical companies to expand their biological product portfolios for cotton applications.

By Product Type Analysis

Insecticides dominate with 56.2% due to the high threat of soil-borne pest damage at germination.

In 2025, Insecticides held a dominant market position in the by-product type segment of the Cotton Seed Treatment Market, with a 56.2% share. Early-season insect pressure, including thrips, aphids, and wireworms, significantly threatens cotton seedling survival. Therefore, insecticide-treated seeds remain the primary defense tool for cotton farmers aiming to protect crop establishment.

Fungicides represent a critical secondary segment, protecting seeds from damping-off pathogens and soil fungi. Fungicide seed coatings improve seedling emergence rates and overall stand uniformity. Consequently, growers frequently combine fungicide and insecticide treatments in a single application to address multiple early-season threats simultaneously.

The Others sub-segment includes nematicides, plant growth regulators, and micronutrient coatings. These products enhance root development and improve stress tolerance in challenging growing environments. Additionally, the rising demand for combination formulations integrating micronutrients with biologicals is expanding the scope of this sub-segment.

By Application Analysis

On-farm dominates with 59.6% due to grower preference for site-specific and flexible treatment options.

In 2025, On-farm held a dominant market position in the By Application segment of the Cotton Seed Treatment Market, with a 59.6% share. On-farm treatment allows growers to customize seed coating products based on local pest pressure, soil conditions, and regulatory requirements. Moreover, smallholder farmers in India and Sub-Saharan Africa favor on-farm methods due to their lower equipment costs.

The Commercial application segment benefits from centralized, precision-controlled treatment facilities that ensure consistent product coverage. Commercial treaters apply standardized formulations with minimal dust-off and high retention quality. However, the higher cost of commercial treatment equipment limits adoption among smallholder farmers and smaller seed distributors in developing markets.

Key Market Segments

By Chemical Origin

- Synthetic

- Biological

By Product Type

- Insecticides

- Fungicides

- Others

By Application

- On-farm

- Commercial

Emerging Trends

Polymer Coatings, Digital Tools, and Service Models Reshape the Cotton Seed Treatment Landscape

Polymer-based seed coating technologies are gaining traction across cotton-producing regions. These advanced coatings improve active ingredient adhesion to the seed surface and significantly reduce dust-off during planting. Consequently, growers and equipment manufacturers benefit from safer, more precise application processes with lower chemical wastage in the field.

- Digital monitoring tools now allow agronomists to track treated seed performance and field emergence rates in real time. Precision agriculture platforms integrate treatment data with soil health information to optimize planting decisions. Greece accounts for more than 80% of total European cotton output, with MY2025/26 production forecast at 1.02 million bales, demonstrating why digital tracking solutions are vital for high-output regional markets.

The seed treatment as a service model is growing among smallholder cotton farmers who lack access to treatment equipment. Service providers offer mobile or centralized treatment facilities on demand. Additionally, rising adoption of pheromone-based and semiochemical treatments introduces highly targeted pest control methods that complement conventional seed coating programs.

Drivers

Rising Pest Pressure and Global Demand for Quality Cotton Drive Seed Treatment Adoption

Escalating prevalence of soil-borne pathogens and early-season pests in major cotton-producing regions pushes growers toward proactive seed protection strategies. Organisms such as Rhizoctonia, Pythium, and Fusarium threaten seedling survival in warm, humid soils. Therefore, seed treatment products serve as the most cost-effective first line of defense before in-field interventions become necessary.

- Mexico’s cotton imports are expected to rise 25% to 0.75 million bales in MY2025/26 as domestic supply tightens. This import dependence reflects stronger demand for high-quality cotton fiber globally, which drives the need for treated seeds that ensure uniform crop stand establishment and consistent fiber quality output.

Mandatory government regulations across key markets are banning harmful chemical pesticides and mandating safer treatment formulations. Regulatory agencies in the European Union and South Asia enforce approved active ingredient lists for seed coatings. Moreover, precision agriculture expansion demands high-vigor seeds that withstand mechanical planting stresses common in automated farming systems.

Restraints

High Equipment Costs and Environmental Regulations Challenge Cotton Seed Treatment Market Growth

High capital investment and operational costs associated with advanced seed treatment application equipment present a significant barrier for small and mid-scale seed companies. Industrial drum treaters and precision coating machines require substantial upfront expenditure. Consequently, many smaller market participants continue to rely on outdated manual application methods that deliver inconsistent product coverage quality.

- Bayer Crop Science EBITDA before special items fell to €4,325 million in 2024 from €5,038 million in 2023, reflecting lower crop protection pricing and higher operational costs. This margin pressure illustrates how cost challenges affect even major industry players, limiting their capacity to reinvest in next-generation treatment formulation development.

Stringent environmental and safety regulations govern the disposal and runoff management of treated cotton seeds. Regulatory agencies require manufacturers to demonstrate that treatment coatings do not leach harmful substances into soil or water systems. Moreover, compliance with labeling, storage, and transport requirements increases operational complexity and raises costs for both manufacturers and distributors in regulated markets.

Growth Factors

Combination Formulations, Organic Cotton Demand, and Strategic Partnerships Accelerate Market Expansion

Development of combination product formulations integrating biologicals with micronutrients creates a new generation of cotton seed treatments with superior plant health benefits. These multi-mode products address soil nutrition and pest protection simultaneously. Therefore, growers in intensive cotton production regions increasingly adopt them to maximize returns per hectare while reducing the number of separate input applications required.

- Asia Pacific generated Corteva Seed sales of $453 million in FY2025, up 11% from $408 million in FY2024, making it the fastest-growing Corteva Seed region by reported growth. This strong performance reflects rising demand for high-performance treated seed products across Asia Pacific cotton markets, confirming the region’s growth potential.

Côte d’Ivoire’s cotton fiber production is forecast at 745,000 bales in MY2025/26, supported by improved farming practices and stronger pest control campaigns. Untapped market potential in developing nations like Côte d’Ivoire grows as farmer education programs communicate the economic benefits of treated seeds. Additionally, strategic collaborations between seed manufacturers and agrochemical companies continue to generate proprietary treatment technologies that create competitive differentiation.

Regional Analysis

North America Dominates the Cotton Seed Treatment Market with a Market Share of 38.9%, Valued at USD 1.5 Billion

North America leads the global cottonseed treatment market with a 38.9% share valued at USD 1.5 billion in 2025. The United States represents the largest single national market, driven by large-scale commercial cotton farming in Texas, Georgia, and the Mississippi Delta. Moreover, strong regulatory frameworks and widespread adoption of precision agriculture technologies support consistent demand for high-performance seed treatment products across the region.

Europe holds a notable share of the global cottonseed treatment market, with production concentrated in Greece, Spain, and Turkey. Greece alone accounts for more than 80% of total European cotton output, creating a concentrated demand hub for fungicide and insecticide seed treatments. Additionally, Spain’s cotton production is projected to recover in MY2025/26 despite planted area falling to its lowest level in nearly three decades.

The Middle East and Africa region presents growing opportunities, particularly in Sub-Saharan Africa, where cotton serves as a major cash crop for smallholder farmers. Countries such as Côte d’Ivoire, Mali, and Burkina Faso expand cotton acreage annually with support from government and development agency programs. Consequently, demand for affordable, accessible seed treatment products that improve crop establishment continues to rise across this region.

Latin America, led by Brazil, represents one of the most dynamic cottonseed treatment markets in the world. Brazil’s Cerrado region drives intensive commercial cotton production that depends heavily on fungicide and insecticide seed coatings to manage its complex soil pathogen environment. Moreover, Mexico’s domestic cotton supply constraints and rising import volumes signal opportunities for treated seed varieties that improve local production efficiency.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE holds a strong position in the cottonseed treatment market through its Agricultural Solutions division. BASF offers a comprehensive portfolio spanning fungicides, insecticides, and biological seed treatments for cotton. The company’s global R&D network drives continuous formulation improvements, positioning it as a leader in combination treatment technologies that address both soil pathogens and early-season pest threats.

Bayer Crop Science AG is one of the most established players in the global cottonseed treatment sector. Bayer’s seed treatment portfolio integrates systemic fungicides and neonicotinoid-class insecticides designed for large-scale commercial cotton operations. The company continues to invest in next-generation biological treatments as market pressures and regulatory changes reshape its product strategy.

Syngenta AG applies its global crop protection expertise to deliver seed treatment solutions tailored for cotton production systems. The company focuses on developing active ingredients with strong residual activity against soil-borne pathogens and key early-season insects. Moreover, Syngenta’s distribution network across major cotton-producing regions in Asia, Africa, and the Americas gives it a significant reach advantage in both commercial and smallholder farmer segments.

Nufarm specializes in crop protection products, including seed treatment, fungicides, and insecticides for cotton. The company serves both commercial seed treatment operations and on-farm customers across Australia, Latin America, and North America. Additionally, Nufarm actively pursues product development partnerships to expand its biologicals and micronutrient treatment lineup, targeting growers seeking reduced-chemistry farming approaches.

Top Key Players in the Market

- BASF SE

- Bayer Crop Science AG

- Syngenta AG

- Nufarm

- UPL Limited

- FMC Corporation

- Corteva Agriscience

- Incotec Group BV

- Valent BioSciences

Recent Developments

- In 2025, BASF developed two new herbicide-tolerant cotton traits. Axant Flex is the first “four-way” trait stack in the U.S. market, offering tolerance to HPPD inhibitors, glyphosate, glufosinate, and dicamba. Seletio TP is a technology designed specifically for Brazilian growers to control grass weeds. These traits are being integrated into their FiberMax and Stoneville cottonseed brands.

- In 2025, Bayer introduced new cotton varieties with enhanced disease and pest resistance. New FiberMax and Stoneville varieties offer bacterial blight resistance, weed control traits (GlyTol, LibertyLink), and lepidopteran pest protection through TwinLink and TwinLink Plus Bt traits.

Report Scope

Report Features Description Market Value (2025) USD 3.8 Billion Forecast Revenue (2035) USD 7.1 Billion CAGR (2026-2035) 6.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Chemical Origin (Synthetic, Biological), By Product Type (Insecticides, Fungicides, Others), By Application (On-farm, Commercial) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape BASF SE, Bayer Crop Science AG, Syngenta AG, Nufarm, UPL Limited, FMC Corporation, Corteva Agriscience, Incotec Group BV, Valent BioSciences Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Cotton Seed Treatment MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Cotton Seed Treatment MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BASF SE

- Bayer Crop Science AG

- Syngenta AG

- Nufarm

- UPL Limited

- FMC Corporation

- Corteva Agriscience

- Incotec Group BV

- Valent BioSciences

Our Clients

- 180850

- March 2026