Quick Navigation

Report Overview

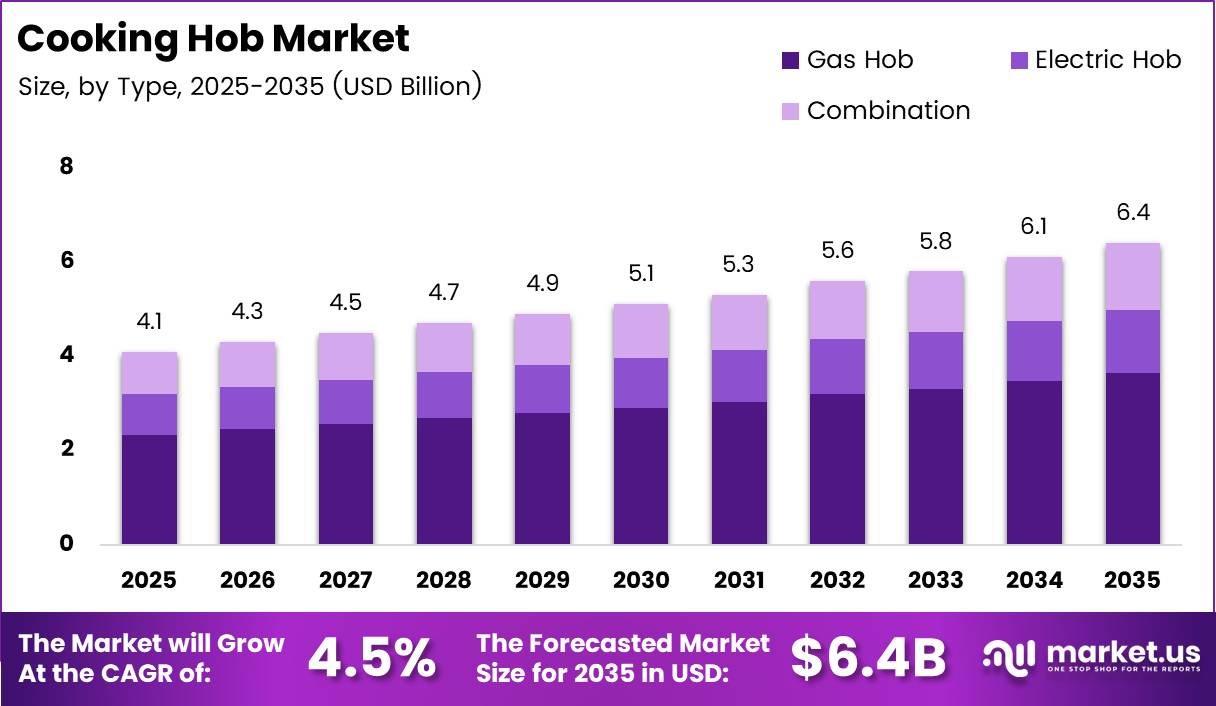

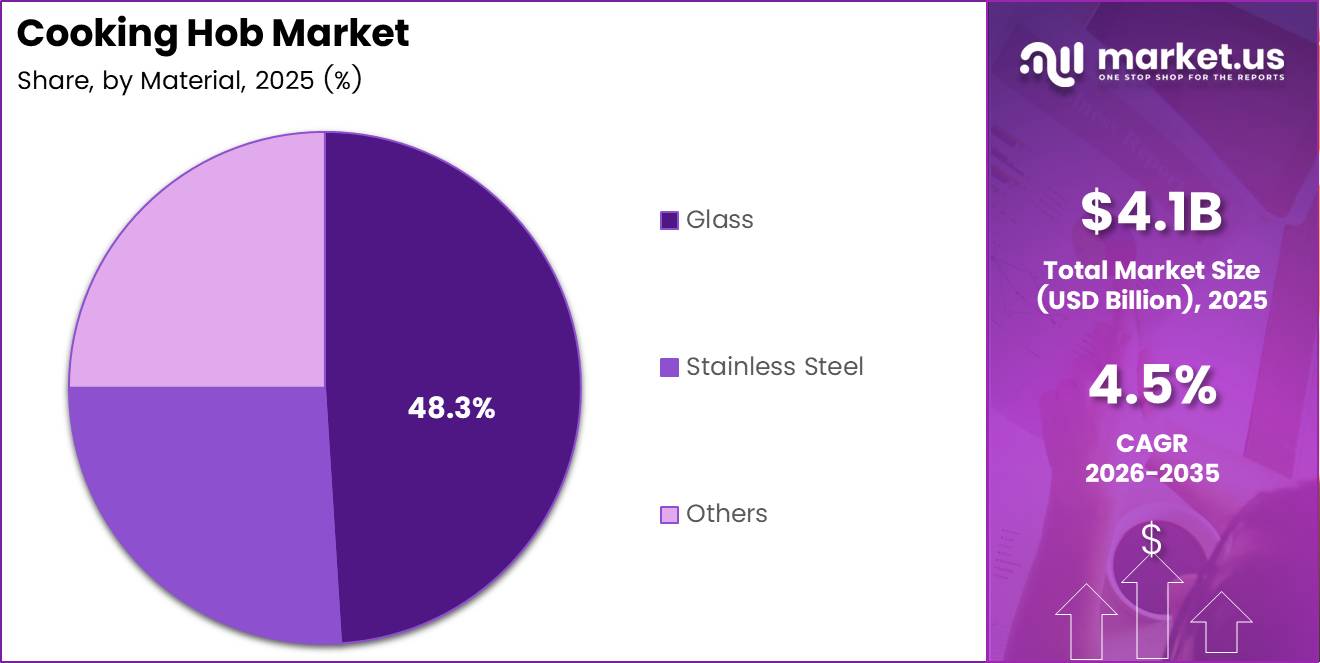

Global Cooking Hob Market size is expected to be worth around USD 6.4 Billion by 2035 from USD 4.1 Billion in 2025, growing at a CAGR of 4.5% during the forecast period 2026 to 2035.

Cooking hobs have shifted from basic kitchen fixtures to central components of modern home design. Urban households across emerging economies are rebuilding kitchens around built-in appliances. This structural shift benefits hob manufacturers selling into both new construction and renovation channels simultaneously.

Gas hobs continue to anchor the market, holding a 56.9% type share. Residential buyers remain the dominant end-user group at 76.4%. These figures confirm that household cooking remains the primary demand engine, and product development priorities should reflect this concentration.

Premium kitchen formats are expanding across Asia, Europe, and the Middle East. Developers integrate hobs directly into modular kitchen designs, which reduces the post-purchase decision cycle. This channel shift favors brands with strong contractor and builder relationships over those relying solely on retail shelf presence.

In August 2025, Samsung Electronics showcased a new lineup of premium built-in kitchen appliances including the Extractor Induction Hob at IFA 2025 for the European market. This move signals that tier-one appliance brands view Europe as the test bed for integrated hob-ventilation systems before broader rollouts.

According to the U.S. Department of Energy, induction cooking systems deliver energy-transfer efficiency of 85% to 95%. Conventional electric cooktops operate at approximately 50% to 80%. This efficiency gap is not marginal. It gives induction hob vendors a measurable, quantifiable argument when targeting cost-sensitive residential buyers.

According to the IEA Energy Efficiency 2025 report, more than 250 new or updated energy-efficiency policies were introduced globally in 2025, covering countries representing 85% of global energy demand. For hob manufacturers, this policy wave creates mandatory upgrade cycles. Markets with stringent appliance efficiency rules will replace older cooktops faster than markets without such frameworks.

Key Takeaways

- The global Cooking Hob Market was valued at USD 4.1 Billion in 2025 and is forecast to reach USD 6.4 Billion by 2035.

- The market grows at a CAGR of 4.5% between 2026 and 2035.

- Gas Hob leads the By Type segment with a 56.9% share in 2025.

- Glass leads the By Material segment with a 48.3% share in 2025.

- Residential leads the By Application segment with a 76.4% share in 2025.

- Retail Outlets/Offline leads the By Distribution Channel segment with a 67.3% share in 2025.

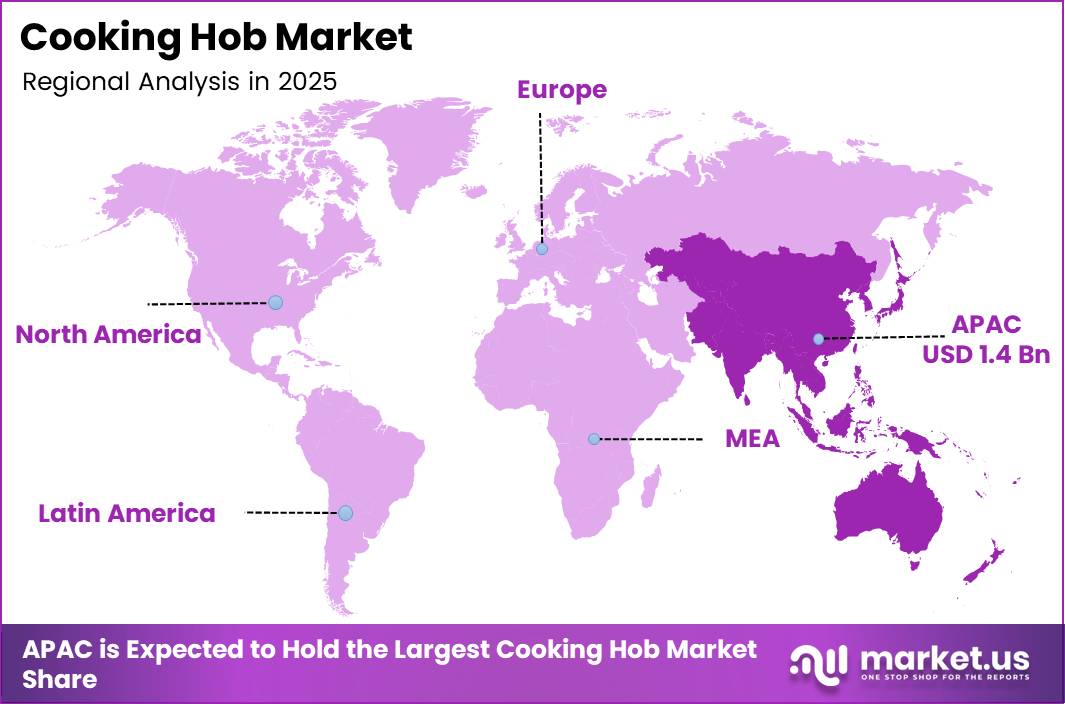

- Asia Pacific leads all regions with a 34.80% share, valued at USD 1.4 Billion.

Type Analysis

Gas Hob dominates with 56.9% due to widespread grid infrastructure and lower unit cost.

In 2025, Gas Hob held a dominant market position in the By Type segment of the Cooking Hob Market, with a 56.9% share. Gas hobs remain the preferred choice in markets where natural gas infrastructure is established. Residential buyers favor them for precise flame control and lower upfront costs compared to induction alternatives.

Electric Hob adoption is accelerating in markets with strong grid reliability and active energy-efficiency mandates. Induction variants within this category deliver 85% to 95% energy-transfer efficiency, a measurable advantage over gas. Buyers in Europe and Japan are leading this shift, supported by appliance replacement subsidies and tightening emissions rules.

Combination Hob products target households transitioning between fuel types. These units pair gas burners with induction zones on a single surface. This format appeals to renovation-led buyers who want flexibility without a full system overhaul, and they command a price premium that supports higher margin per unit for manufacturers.

Material Analysis

Glass dominates with 48.3% due to premium aesthetic appeal and easy-clean surface demand.

In 2025, Glass held a dominant market position in the By Material segment of the Cooking Hob Market, with a 48.3% share. Glass ceramic surfaces align with the visual standards of modern modular kitchens. Developers and interior designers specify glass hobs by default, which drives volume through the construction and renovation channel.

Stainless Steel hobs retain a strong foothold in commercial kitchens and mid-range residential segments. They offer durability under heavy daily use and require less careful handling than glass surfaces. However, the premium kitchen trend is gradually pressuring stainless steel’s residential share as buyers prioritize visual integration over material robustness.

Others in this segment include cast iron and enamel-finished surfaces. According to the IEA, global energy-efficiency improvement rates increased from 1.0% in 2024 to 1.8% in 2025. This policy momentum is nudging buyers toward materials compatible with induction and low-emission cooking formats, gradually reducing demand for older surface types.

In December 2025, Crompton Greaves Consumer Electricals launched the Viona Hobs Series. This product line targets the glass-finish residential segment in India, confirming that domestic manufacturers are directly entering the premium material category to compete with imported brands.

Application Analysis

Residential dominates with 76.4% due to household formation growth and kitchen renovation activity.

In 2025, Residential held a dominant market position in the By Application segment of the Cooking Hob Market, with a 76.4% share. Rising urbanization and new housing completions in Asia Pacific and the Middle East are the structural drivers. Each new residential unit represents a direct sales event for built-in hob vendors.

Commercial applications include hotels, restaurants, catering facilities, and institutional kitchens. This segment prioritizes durability and multi-burner performance over aesthetics. Commercial buyers replace equipment on maintenance cycles rather than design trends, creating a predictable but slower-moving demand base for professional-grade cooking hob products.

Distribution Channel Analysis

Retail Outlets/Offline dominates with 67.3% due to tactile purchasing behavior in high-value appliance buying.

In 2025, Retail Outlets/Offline held a dominant market position in the By Distribution Channel segment of the Cooking Hob Market, with a 67.3% share. Consumers purchasing high-ticket kitchen appliances prefer in-store evaluation. Physical retail allows buyers to assess build quality and surface finish before committing. This preference sustains brick-and-mortar volume despite e-commerce expansion.

E-commerce/Online channels are taking share faster in cooking hobs than in most large appliance categories. Improved product visualization tools, customer review systems, and same-day delivery networks are reducing the friction in online hob purchases. Brands without a strong direct-to-consumer digital presence risk ceding margin to platform intermediaries as this channel grows.

Key Market Segments

By Type

- Gas Hob

- Electric Hob

- Combination

By Material

- Glass

- Stainless Steel

- Others

By Application

- Residential

- Commercial

By Distribution Channel

- Retail Outlets/Offline

- E-commerce/Online

Drivers

Modular Kitchen Expansion and Smart Built-In Appliance Adoption Are Reshaping Residential Hob Demand

Urban housing projects across Asia, the Middle East, and Europe now include pre-fitted modular kitchens as standard. Builders source hobs at the construction stage, bypassing retail entirely. This shifts the purchase decision upstream to architects and kitchen designers, giving brands with specification teams a structural advantage over those relying on consumer pull.

Consumer preference for energy-efficient cooking solutions is also reinforcing hob upgrades. Induction and gas-hybrid systems deliver measurable fuel savings over standalone gas rings. Buyers in premium residential segments are replacing conventional cooktops not because they have failed, but because newer hob formats offer lower running costs and better kitchen aesthetics simultaneously.

According to a 2025 combustion study published in ScienceDirect, a swirl burner with a 49° cap angle achieved 54.1% thermal efficiency and 75.2% combustion efficiency. These figures demonstrate that gas burner engineering is advancing beyond incremental improvements. In October 2025, Hafele introduced the Cronus Digi-Step Hobs featuring advanced gas hob technology and premium kitchen design integration, bringing these engineering gains directly to market.

Restraints

High Installation Costs and Low Rural Penetration Cap Market Reach Beyond Premium Urban Segments

Advanced multi-burner cooking hob systems carry high initial installation costs. Professional fitting, gas line extensions, or electrical panel upgrades add substantially to the product price. This cost structure prices out a large portion of middle-income households and makes volume growth in lower-tier cities structurally difficult for manufacturers targeting scale.

Rural markets across South Asia and Sub-Saharan Africa show low penetration of built-in kitchen appliances. The absence of modular kitchen culture and lower average kitchen renovation budgets limit addressable demand. Without infrastructure investment or targeted financing programs from governments, this segment remains largely outside the formal cooking hob market.

Regulatory timelines compound the challenge. India’s 2026 induction hob energy-labeling policy delayed mandatory compliance by 6 months, shifting the deadline from 1 July 2026 to 1 January 2027. This delay signals that compliance infrastructure in high-potential markets like India is still maturing. Manufacturers face an uneven regulatory landscape that slows product standardization and complicates launch planning.

Growth Factors

IoT Integration, E-Commerce Expansion, and Replacement Demand Are Opening New Revenue Channels for Hob Manufacturers

IoT-enabled cooking hobs with app-based temperature and safety controls are creating a new premium tier. Buyers in smart home segments pay a meaningful price premium for connectivity features. This opens a margin expansion opportunity for manufacturers who can integrate reliable software platforms alongside hardware, rather than treating connectivity as a spec-sheet addition.

According to a 2025 study, a porous PNG cooking burner achieved 73.5% thermal efficiency for PNG and 82.2% for LPG at 0.2 bar operating pressure. These results confirm that burner-level innovation is still producing meaningful efficiency gains. Manufacturers investing in advanced combustion R&D can translate these gains into product differentiation and premium pricing across both residential and commercial segments.

In May 2024, Elica entered a strategic partnership with ILVE to expand into the home cooking market with new hobs and induction ovens. This move illustrates the broader trend of ventilation and cooking appliance brands converging into integrated kitchen solutions. Brands that bundle hob and extraction products together can capture a larger share of the kitchen renovation budget per household.

Emerging Trends

Hydrogen-Compatible Burners, AI Auto-Cooking, and Designer Surface Finishes Are Redefining the Premium Hob Segment

Touch-control and sensor-based induction technologies are becoming baseline features in mid-to-premium hob products. Buyers in Europe and East Asia now expect touch interfaces as standard. Brands still selling dial-controlled models in these markets face a perception gap that directly affects shelf positioning and retail sell-through rates.

According to a 2025 hydrogen cooking burner assessment, burner efficiency improved from 37% to 72% using heat recovery optimization. This near-doubling of efficiency through engineering redesign signals that hydrogen-compatible hob technology is approaching commercial viability. Manufacturers who develop hydrogen-ready burner platforms now will hold a compliance advantage as hydrogen gas networks expand in Europe and parts of Asia.

AI-based auto-cooking features and flame failure safety systems are moving from flagship products into mid-range lines. Consumer expectations are resetting upward. The integration of multi-functional smart connectivity into hobs is no longer a differentiator in premium categories. It is fast becoming a baseline requirement that mid-market manufacturers must meet to stay competitive.

Regional Analysis

Asia Pacific Dominates the Cooking Hob Market with a Market Share of 34.80%, Valued at USD 1.4 Billion

Asia Pacific leads all regions with a 34.80% share, valued at USD 1.4 Billion in 2025. China, India, and South Korea are the primary volume drivers. High urban housing construction rates, a deep-rooted modular kitchen culture in China, and India’s rapidly expanding middle-income housing segment all contribute to the region’s structural dominance in this market.

North America Cooking Hob Market Trends

North America represents a mature but high-value market for cooking hobs. Premium induction and gas-hybrid models are gaining traction as kitchen renovation activity remains elevated among homeowners aged 35 to 55. The U.S. market is also responding to federal energy efficiency directives, which are accelerating the replacement of older cooktop formats with compliant built-in hob systems.

Europe Cooking Hob Market Trends

Europe ranks as the most policy-driven cooking hob market globally. The EU’s energy efficiency directives have created mandatory replacement cycles for non-compliant appliances across member states. Germany, France, and the UK lead induction hob adoption, with glass ceramic surfaces dominating new kitchen installations. OEM and built-in appliance brands compete directly through builder and developer specification programs.

Latin America Cooking Hob Market Trends

Latin America offers mid-term volume potential, concentrated primarily in Brazil and Mexico. Gas hob penetration remains high due to natural gas grid availability and established cooking habits. However, rising disposable incomes in urban Brazil are creating demand for mid-range glass ceramic and combination hob formats among younger households undergoing first-time kitchen upgrades.

Middle East & Africa Cooking Hob Market Trends

The Middle East and Africa region shows bifurcated demand. GCC countries, particularly the UAE and Saudi Arabia, are active buyers of premium built-in hob products through hospitality and luxury residential channels. Sub-Saharan Africa remains largely underpenetrated for formal cooking hob products, with market activity concentrated in South Africa’s mid-to-upper residential segment.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

BSH Home Appliances Group operates Bosch and Siemens as distinct brands with separate market positioning. In October 2024, BSH expanded both portfolios with advanced induction hobs featuring AI-assisted cooking technology. This dual-brand strategy allows BSH to cover mid-premium and luxury segments simultaneously, reducing the risk of ceding share at either price tier to single-brand competitors.

Whirlpool Corporation executed a structural realignment in April 2024 by completing its transaction with Arçelik to create Beko Europe B.V. This move consolidates Whirlpool’s European kitchen appliance operations under a larger, cost-efficient entity. For the hob market specifically, the combined operation gives Whirlpool stronger distribution access across Eastern Europe, where built-in kitchen appliance penetration is still growing.

Electrolux AB maintains competitive positioning through its integrated kitchen ecosystem strategy. The company targets premium European residential buyers who purchase hobs as part of coordinated kitchen installations rather than as standalone products. This bundling approach supports higher average transaction values and creates switching costs that benefit Electrolux in the replacement cycle.

Haier Group Corporation uses its scale in Asia Pacific to compete on product breadth and price agility. Haier covers entry-level, mid-range, and smart-connected hob formats across a single brand architecture. This portfolio depth gives Haier an advantage in markets like India and Southeast Asia, where income stratification demands multiple price points within a single product category.

Key Players

- BSH Home Appliances Group

- Whirlpool Corporation

- Electrolux AB

- Haier Group Corporation

- LG Electronics Inc.

- Samsung Electronics Co., Ltd

- Miele & Cie. KG

- Smeg S.p.A

- Arcelik A.S.

- Faber S.p.A.

Recent Developments

- September 2025 – Miele introduced the KM 8000 induction hob at IFA 2025, featuring the M Sense automatic temperature control system and a modular outdoor kitchen concept called “Dreams.”

- April 2026 – Samsung Electronics unveiled its 2026 Bespoke AI appliance lineup featuring a new Extractor Induction Hob with integrated ventilation and Flex Zone Plus technology.

- July 2025 – Falmec launched the Zero induction hob, focused on energy-efficient cooking and simplified usability for residential buyers.

- March 2025 – Havells India announced expansion into kitchen appliances with new cooktops, hobs, chimneys, and built-in cooking products targeting the domestic market.

- October 2024 – BSH Hausgeräte expanded its Bosch and Siemens portfolios with advanced induction hobs featuring AI-assisted cooking technology across European markets.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.1 Billion |

| Forecast Revenue (2035) | USD 6.4 Billion |

| CAGR (2026-2035) | 4.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Gas Hob, Electric Hob, Combination), By Material (Glass, Stainless Steel, Others), By Application (Residential, Commercial), By Distribution Channel (Retail Outlets/Offline, E-commerce/Online) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | BSH Home Appliances Group, Whirlpool Corporation, Electrolux AB, Haier Group Corporation, LG Electronics Inc., Samsung Electronics Co. Ltd, Miele & Cie. KG, Smeg S.p.A, Arcelik A.S., Faber S.p.A. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |