Global CNC Controller Market Size, Share, Growth Analysis By Product Type (Industrial OEM CNC Controllers, CNC Retrofit Controllers, PC Based CNC Controller, Others), By Type (2 Axis & 3 Axis, 4 Axis & 5 Axis, Multi-Axis), By End-Use Industry (Automotive, Aerospace & Defense, Industrial Machinery, Electronics & Semiconductor, Medical Devices, Energy & Power, Marine, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181181

- Number of Pages: 281

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

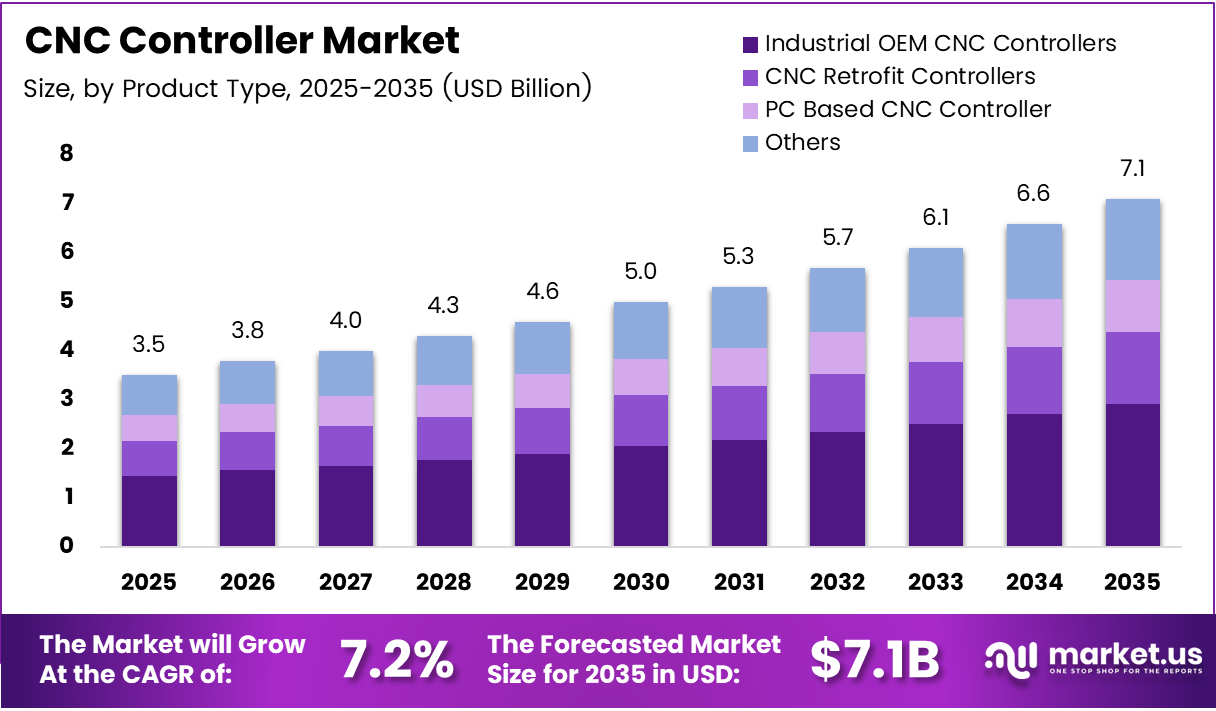

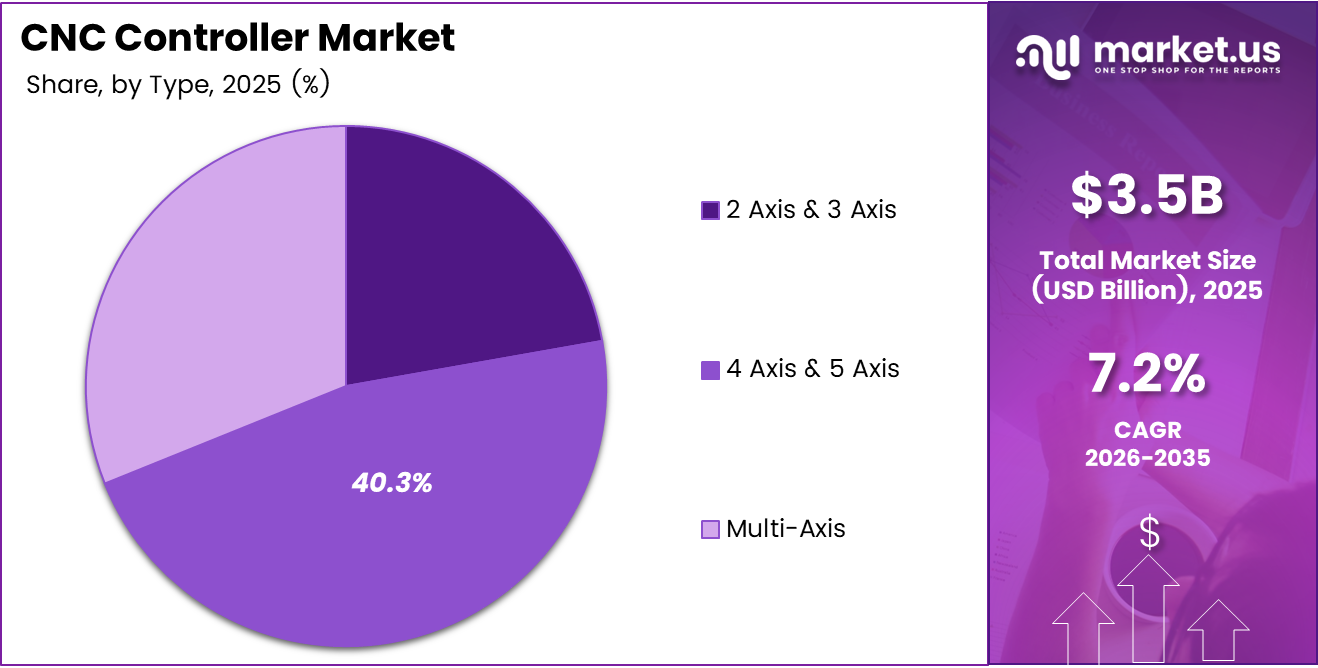

Global CNC Controller Market size is expected to be worth around USD 7.1 Billion by 2035 from USD 3.5 Billion in 2025, growing at a CAGR of 7.2% during the forecast period 2026 to 2035.

CNC controllers are the electronic systems that direct machine tool movements with precision across milling, turning, grinding, and multi-axis machining operations. Manufacturers across automotive, aerospace, and medical device sectors rely on these systems to hold tight tolerances and maintain output consistency at scale. Without capable controllers, high-mix production environments cannot sustain competitive cycle times.

The 7.2% CAGR signals that enterprise buyers are replacing older motion control systems faster than many vendors anticipated. This pace reflects a deliberate shift — manufacturers no longer treat CNC controllers as commodity purchases. They now evaluate them as strategic infrastructure tied directly to throughput, scrap rates, and workforce efficiency.

Smart manufacturing investments are reshaping procurement criteria. Buyers now require controllers that support real-time data exchange, predictive diagnostics, and IIoT connectivity. This shift moves the purchase decision up the organizational hierarchy — from floor-level engineering to operations and capital planning teams — widening the sales cycle but also increasing contract value.

Asia Pacific leads adoption, driven by large-scale industrial expansion across China, Japan, South Korea, and India. Automotive and electronics manufacturing clusters in these countries are modernizing production infrastructure, creating concentrated demand for both new controller installations and retrofit upgrades on existing machine fleets.

Government-backed industrial programs across the United States, Germany, and Japan continue to fund automation upgrades in domestic manufacturing. These programs reduce payback periods for buyers and lower the financial risk of transitioning to advanced multi-axis control systems — effectively compressing the adoption timeline across mid-tier manufacturers.

According to a peer-reviewed study published in Discover Mechanical Engineering, optimized tool pathway strategies in CNC machining deliver up to 67% energy savings for rectangular pocket operations. This finding matters because energy cost now ranks among the top three operational concerns for high-volume machining facilities — making energy-efficient controllers a direct profit lever, not just a sustainability checkbox.

According to machinetoolnews.ai, AI-enabled predictive maintenance systems deployed on CNC installations achieve a 50% reduction in unplanned downtime. For a production floor running three shifts, that figure translates directly into recovered machine hours and avoided expediting costs — which explains why AI-integrated controllers command premium pricing and shorter sales cycles than standard replacements.

Key Takeaways

- The Global CNC Controller Market was valued at USD 3.5 Billion in 2025 and is forecast to reach USD 7.1 Billion by 2035.

- The market advances at a CAGR of 7.2% during the forecast period 2026 to 2035.

- By Product Type, Industrial OEM CNC Controllers lead with a 40.3% share in 2025.

- By Type, the 4 Axis & 5 Axis segment holds a 40.3% share, reflecting demand for complex precision machining.

- By End-Use Industry, Automotive is the dominant vertical with a 25.4% share.

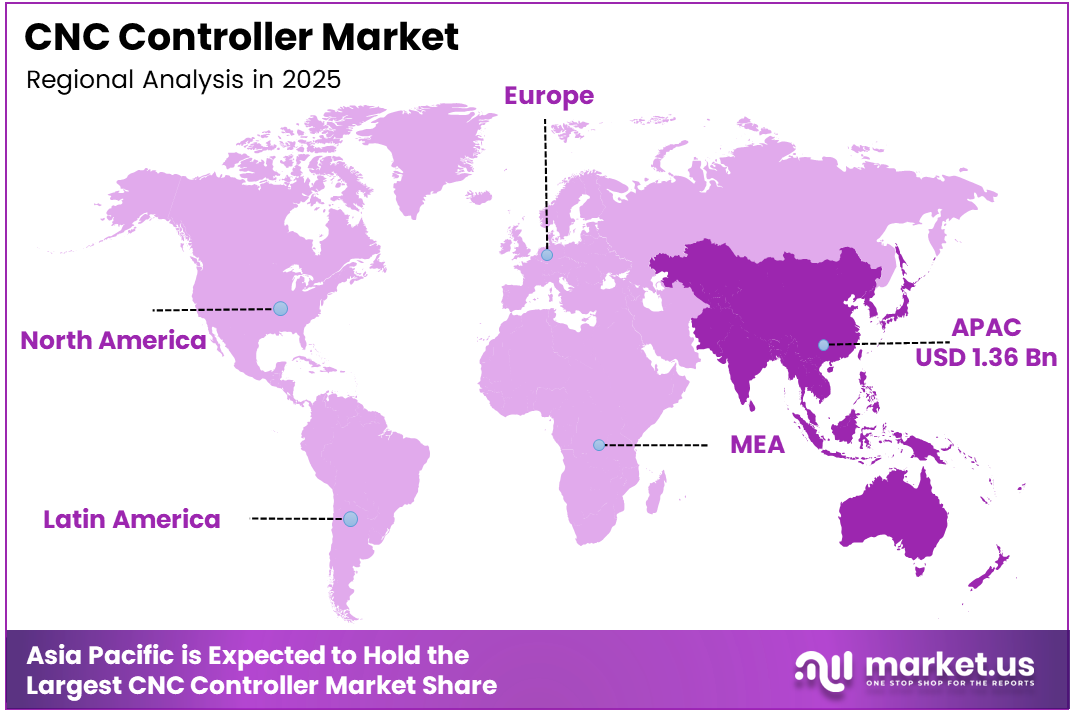

- Asia Pacific dominates regionally with a 38.4% market share, valued at USD 1.36 Billion in 2025.

- Key players include FANUC, Siemens, Mitsubishi Electric, Heidenhain, Haas Automation, and Okuma, among others.

Product Type Analysis

Industrial OEM CNC Controllers dominate with 40.3% due to deep machine builder integration and procurement scale.

In 2025, Industrial OEM CNC Controllers held a dominant market position in the By Product Type segment of the CNC Controller Market, with a 40.3% share. Machine tool builders standardize on OEM controllers to maintain performance warranties and reduce integration risk. This structural lock-in creates high switching costs, reinforcing OEM controller share even as alternative architectures mature.

CNC Retrofit Controllers serve as the cost-effective entry point for manufacturers upgrading aging machine fleets without full capital replacement. Retrofit solutions allow mid-tier facilities to extend asset life while gaining modern control capabilities. This segment benefits directly from constrained capital budgets — when new machine purchases are deferred, retrofit controller demand fills the gap.

PC-Based CNC Controllers differentiate through open software architecture and compatibility with third-party applications. These systems attract high-mix, low-volume manufacturers and research-oriented facilities that require frequent reprogramming flexibility. In August 2024, FANUC Corporation launched the new Series 500i-A controller featuring 2.7 times higher CPU performance, underscoring how even OEM leaders are pushing computational capability to meet rising software demands.

Others in the product type segment covers specialized and application-specific controllers used in niche machining environments. These include dedicated systems for grinding, EDM, and laser cutting platforms. Although volume is limited, this sub-segment carries above-average margin due to custom engineering requirements and limited competitive alternatives.

Type Analysis

4 Axis & 5 Axis controllers dominate with 40.3% due to aerospace and complex part manufacturing requirements.

In 2025, 4 Axis & 5 Axis controllers held a dominant market position in the By Type segment of the CNC Controller Market, with a 40.3% share. Complex aerospace components, turbine blades, and orthopedic implants require simultaneous multi-axis interpolation that two- or three-axis systems cannot deliver. This technical necessity — not preference — anchors the segment’s leading position.

2 Axis & 3 Axis controllers represent the broadest installed base across general machining, turning centers, and job shops. These systems handle the majority of standard part geometries and remain the default choice for price-sensitive buyers. However, as part complexity rises across automotive and electronics supply chains, buyers increasingly specify higher-axis controllers even for traditionally simple operations.

Multi-Axis controllers address the most demanding simultaneous machining requirements — including nine-axis and beyond — used in aerospace structural components and complex die and mold applications. This segment carries the highest per-unit revenue and the longest integration timeline. Buyers in this tier evaluate controller vendors on software capability and post-sale engineering support as much as hardware specification.

End-Use Industry Analysis

Automotive dominates with 25.4% due to high-volume precision part production at scale.

In 2025, Automotive held a dominant position in the By End-Use Industry segment of the CNC Controller Market, with a 25.4% share. Engine blocks, transmission housings, and brake components require machined tolerances that only CNC-controlled systems can sustain at production volumes. Electric vehicle platform shifts are now triggering additional controller upgrades as new powertrain geometries replace established tooling setups.

Aerospace & Defense sets the performance ceiling for CNC controller capability. Structural airframe parts and rotating components demand five-axis simultaneous machining with real-time error compensation. Regulatory certification requirements for aerospace-grade parts also make controller software validation a procurement prerequisite — creating a high barrier that established controller vendors are better positioned to clear.

Industrial Machinery spans press tools, hydraulic components, and heavy equipment parts. This segment provides consistent baseline demand because capital goods manufacturers continuously refresh tooling and upgrade machining lines. Controller vendors targeting this vertical benefit from repeat purchase cycles tied to production line capacity expansions.

Electronics & Semiconductor manufacturing uses CNC controllers for precision drilling, milling, and cutting of PCBs, housings, and semiconductor packaging components. Miniaturization trends push tolerance requirements tighter each product generation — directly raising the performance bar for controllers deployed in this vertical.

Medical Devices represent one of the fastest-expanding application areas for high-precision CNC machining. Implants, surgical instruments, and diagnostic equipment housings require validated, traceable machining processes. Regulatory traceability requirements push buyers toward controller platforms with integrated data logging and process documentation.

Energy & Power applications include turbine components, valve bodies, and heat exchanger parts machined to tight specifications. This segment benefits from infrastructure investment cycles in both conventional and renewable energy projects. Controller upgrades in this vertical often run in parallel with broader plant modernization programs.

Marine manufacturing uses CNC machining for propeller shafts, hull components, and engine parts. Although smaller in volume than automotive or aerospace, marine applications require corrosion-resistant material machinability — a technically demanding environment that favors controllers with adaptive feed rate control.

Others captures emerging applications including construction equipment, rail, and consumer goods manufacturing. As CNC machining penetrates smaller production environments, this segment grows in breadth if not in unit value — representing the long tail of controller adoption across diverse industrial categories.

Key Market Segment

By Product Type

- Industrial OEM CNC Controllers

- CNC Retrofit Controllers

- PC Based CNC Controller

- Others

By Type

- 2 Axis & 3 Axis

- 4 Axis & 5 Axis

- Multi-Axis

By End-Use Industry

- Automotive

- Aerospace & Defense

- Industrial Machinery

- Electronics & Semiconductor

- Medical Devices

- Energy & Power

- Marine

- Others

Regional Analysis

Asia Pacific Dominates the CNC Controller Market with a Market Share of 38.4%, Valued at USD 1.36 Billion

Asia Pacific commands 38.4% of the global CNC Controller Market, valued at USD 1.36 Billion in 2025. China, Japan, South Korea, and India collectively drive this position through massive automotive and electronics manufacturing clusters. Government-backed industrial modernization programs across these economies accelerate machine tool investments, creating concentrated and recurring controller demand unavailable at this scale elsewhere.

North America CNC Controller Market Trends

North America maintains a strong share anchored by aerospace, defense, and medical device manufacturing requirements. The United States drives most regional volume, where reshoring initiatives and defense procurement programs sustain capital expenditure on advanced machining infrastructure. Buyers in this region prioritize controller platforms with certified software, cybersecurity features, and domestic technical support networks.

Europe CNC Controller Market Trends

Europe holds a mature but technically demanding position in the global market. Germany leads regional demand through its machine tool manufacturing base — one of the largest globally — where domestic builders integrate controllers directly into export equipment. Precision engineering standards and strict energy efficiency regulations push European buyers toward high-performance, energy-optimized controller architectures ahead of other regions.

Latin America CNC Controller Market Trends

Latin America represents an earlier-stage adoption environment, with Brazil and Mexico anchoring regional activity through automotive assembly and parts manufacturing. Foreign direct investment in both countries brings modern production standards that require capable CNC infrastructure. However, import dependency for advanced controllers and limited local technical support constrain adoption velocity.

Middle East and Africa CNC Controller Market Trends

Middle East and Africa show early-stage but directionally positive market activity, driven by energy sector machining, defense equipment manufacturing, and economic diversification programs. GCC countries, particularly Saudi Arabia and the UAE, are investing in domestic manufacturing capacity as part of national industrial strategies — creating a foundation for CNC controller demand that was not present a decade ago.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Market Segments

By Product Type

- Industrial OEM CNC Controllers

- CNC Retrofit Controllers

- PC Based CNC Controller

- Others

By Type

- 2 Axis & 3 Axis

- 4 Axis & 5 Axis

- Multi-Axis

By End-Use Industry

- Automotive

- Aerospace & Defense

- Industrial Machinery

- Electronics & Semiconductor

- Medical Devices

- Energy & Power

- Marine

- Others

Drivers

Smart Manufacturing Mandates and Precision Requirements Drive Rapid CNC Controller Upgrades Across Global Industries

Industry 4.0 adoption forces manufacturers to replace isolated machine tools with networked, data-generating production systems. CNC controllers sit at the center of this transition — they are the interface between physical machining and digital production management. Facilities that cannot connect controller data to enterprise systems face measurable throughput and quality disadvantages against competitors that can.

Aerospace, automotive, and medical device manufacturers drive precision machining requirements beyond what legacy two- and three-axis controllers support. Turbine components, structural airframe parts, and surgical implants now require simultaneous five-axis interpolation with real-time compensation. According to machinetoolnews.ai, AI-enabled predictive maintenance on CNC systems delivers a 30% improvement in overall equipment effectiveness — a direct productivity gain that justifies the premium cost of advanced controller platforms.

Electronics and semiconductor manufacturing add another structural pull. Board-level miniaturization and packaging complexity push machining tolerances tighter each product generation. Automated production lines in this sector run continuously and cannot absorb the schedule disruption of unplanned controller failures — creating strong commercial logic for investing in higher-capability, diagnostics-rich control systems from the outset.

Restraints

High Capital Costs and Operator Skill Gaps Limit CNC Controller Adoption Among Mid-Tier Manufacturers

Advanced CNC controllers carry significant upfront costs that extend well beyond hardware procurement. System integration, software configuration, machine recalibration, and staff retraining all add to the total implementation cost. For small and mid-sized manufacturers operating on thin margins, this cumulative investment frequently pushes controller upgrades into multi-year deferral cycles.

Skilled CNC programmers and operators remain scarce across major manufacturing economies. Modern multi-axis controllers require proficiency in CAM software, G-code programming, and increasingly in IIoT data interpretation. According to a peer-reviewed study published in Discover Mechanical Engineering, optimized CNC tool pathway strategies achieve up to 33% energy savings for circular pocket operations — but realizing those savings requires operator expertise that many facilities currently lack.

The skills gap compounds the capital constraint. Manufacturers that invest in advanced controllers but cannot staff them effectively see slower productivity gains, longer payback periods, and increased risk of costly programming errors. This double constraint — financial and human — slows adoption velocity most severely among the mid-market manufacturer segment that represents the largest volume opportunity for controller vendors.

Growth Factors

AI-Enabled Maintenance, Cloud Connectivity, and SME Expansion Create New Revenue Layers for CNC Controller Vendors

AI-integrated predictive maintenance transforms the commercial proposition for next-generation CNC controllers. Rather than selling hardware, vendors now offer measurable operational outcomes — reduced downtime, avoided repair costs, and extended asset life. According to machinetoolnews.ai, CNC users report a 10x return on investment within weeks of deploying AI-enabled monitoring systems. That payback speed fundamentally changes the CFO conversation around controller upgrade budgets.

Small and medium-sized manufacturers represent the largest underpenetrated segment in the CNC controller market. These facilities historically deferred advanced controllers due to cost and complexity. However, compact, lower-cost controller platforms — combined with cloud-based configuration and remote support — now make sophisticated control accessible to job shops and contract manufacturers that previously relied on basic two-axis systems. In November 2025, Onefinity CNC released the Redline Controller upgrade kits for all Elite series machines, demonstrating direct product response to this SME upgrade demand.

Cloud-connected CNC controllers open a recurring revenue model that hardware-only controller sales cannot support. Remote monitoring, over-the-air software updates, and centralized analytics give vendors post-sale engagement that deepens customer relationships and raises switching costs. Asia-Pacific manufacturing hubs, where new facilities are built with digital infrastructure from the ground up, are the fastest adoption environment for cloud-native controller architectures.

Emerging Trends

Open Architecture, IIoT Integration, and Digital Twin Adoption Redefine CNC Controller Functionality Expectations

Open-architecture CNC controllers remove the proprietary lock-in that has historically constrained machine builders and end-users alike. By supporting standardized communication protocols and third-party software integration, open platforms allow manufacturers to combine best-in-class motion control with specialized CAM, simulation, and analytics tools. This flexibility directly lowers total system cost and shortens time-to-production for new machining programs.

IIoT connectivity turns CNC controllers into active production intelligence nodes rather than passive motion executors. Real-time spindle load, tool wear, thermal drift, and cycle time data feed into plant-level dashboards and ERP systems. According to machinetoolnews.ai, AI-enabled monitoring systems achieve 75% faster troubleshooting for maintenance technicians — a gain that compounds across multi-machine facilities and directly reduces the skilled labor hours consumed by reactive maintenance.

Digital twin technology enables manufacturers to simulate and validate CNC programs before cutting a single part. Collision detection, cycle time prediction, and toolpath optimization happen in software, not on the machine. In March 2025, AI-driven startup LimitlessCNC raised USD 4.1 Million in seed funding to develop AI agent technology that automates CNC programming workflows — signaling that venture capital now views intelligent CNC software as a distinct, investable category separate from the controller hardware itself.

Key Company Insights

FANUC Corporation holds a structurally advantaged position through its deep OEM integration with machine tool builders globally. Its proprietary servo systems, motors, and controllers operate as a closed ecosystem — creating high switching costs that protect installed base revenue. FANUC’s multi-decade relationships with Japanese and international machine builders give it first-mover access to new platform decisions before competitors are even considered.

Siemens competes on the strength of its SINUMERIK platform, which integrates CNC control with broader factory automation, drives, and digital enterprise software. This end-to-end positioning allows Siemens to sell controller upgrades as part of larger digital transformation contracts — moving the conversation from unit price to total value of the production system. European manufacturing’s preference for integrated automation stacks plays directly to this strategy.

Mitsubishi Electric leverages its combined strength in servo technology, programmable controllers, and CNC systems to serve automotive and electronics manufacturers requiring tightly coordinated motion and process control. Its MELDAS and M8 series platforms are embedded across Asian manufacturing supply chains, giving Mitsubishi Electric durable installed base density in the region with the highest near-term growth rate.

Heidenhain differentiates through precision measurement integration — combining linear encoders, angle encoders, and CNC control into systems optimized for die-and-mold, aerospace, and medical machining. This vertical focus commands premium pricing in applications where measurement accuracy is non-negotiable. Heidenhain’s engineering reputation creates a defensible niche that broad-line competitors find difficult to displace on technical grounds alone.

Key Players

- FANUC Corporation

- Siemens

- Mitsubishi Electric

- Heidenhain

- Haas Automation

- Okuma

- GSK CNC Equipment

- Fagor Automation

- NUM Controls

- Allen-Bradley (Rockwell Automation)

- Hurco Companies

- DMG MORI

- B&R Industrial Automation

- Delta Electronics

- Schneider Electric

- Other Key Players

Recent Developments

- August 2024 — FANUC Corporation launched the Series 500i-A CNC controller featuring dual-engine architecture with 2.7 times higher CPU performance and integrated 5-axis technology. The platform also introduced enhanced cybersecurity features and optimized energy efficiency, positioning it as FANUC’s flagship solution for advanced machining centers requiring next-generation computational capability.

- November 2025 — Onefinity CNC officially released the Redline CNC Controller upgrade kits for all Elite series machines during Launch Week 2025, following a summer preview at AWFS. The kits deliver a complete ground-up redesign of motion control architecture, targeting precision, responsiveness, and user experience improvements for professional woodworking and fabrication applications.

- March 2025 — Israeli AI startup LimitlessCNC emerged from stealth mode and closed a USD 4.1 Million seed round led by Grove Ventures and Meron Capital. The company develops AI agent technology that automates CNC programming and machining workflows, directly targeting the skilled programmer shortage that constrains adoption of advanced CNC systems across mid-tier manufacturers.

Report Scope

Report Features Description Market Value (2025) USD 3.5 Billion Forecast Revenue (2035) USD 7.1 Billion CAGR (2026-2035) 7.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Industrial OEM CNC Controllers, CNC Retrofit Controllers, PC Based CNC Controller, Others), By Type (2 Axis & 3 Axis, 4 Axis & 5 Axis, Multi-Axis), By End-Use Industry (Automotive, Aerospace & Defense, Industrial Machinery, Electronics & Semiconductor, Medical Devices, Energy & Power, Marine, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape FANUC, Siemens, Mitsubishi Electric, Heidenhain, Haas Automation, Okuma, GSK CNC Equipment, Fagor Automation, NUM Controls, Allen-Bradley (Rockwell Automation), Hurco Companies, DMG MORI, B&R Industrial Automation, Delta Electronics, Schneider Electric, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- FANUC Corporation

- Siemens

- Mitsubishi Electric

- Heidenhain

- Haas Automation

- Okuma

- GSK CNC Equipment

- Fagor Automation

- NUM Controls

- Allen-Bradley (Rockwell Automation)

- Hurco Companies

- DMG MORI

- B&R Industrial Automation

- Delta Electronics

- Schneider Electric

- Other Key Players

Our Clients

- 181181

- Mar 2026