Global Clinical Trials Management System Market By Solution (Enterprise CTMS and Site-Based CTMS), By Component (Software and Services), By Deployment Mode (Cloud-based, Web-based and On-Premises), By End User (Pharmaceutical & Biotech Companies, Contract Research Organizations (CROs), Medical Device Manufacturers and Academic & Research Institutions), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 178582

- Number of Pages: 371

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

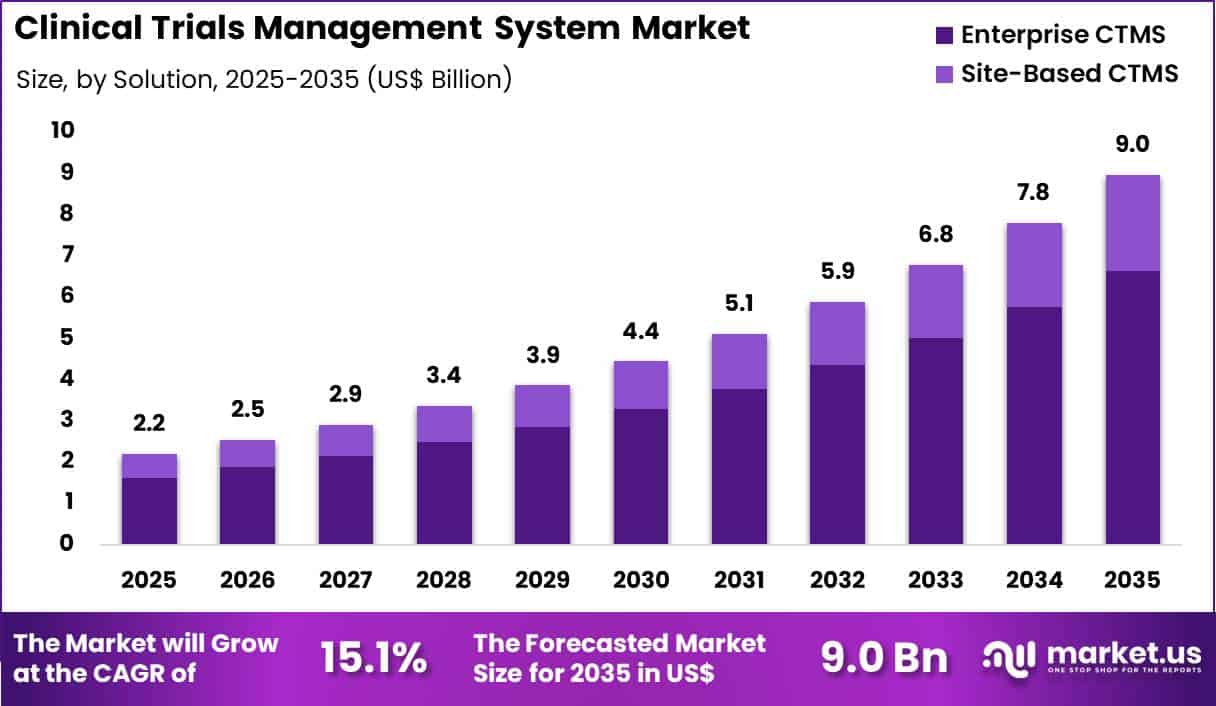

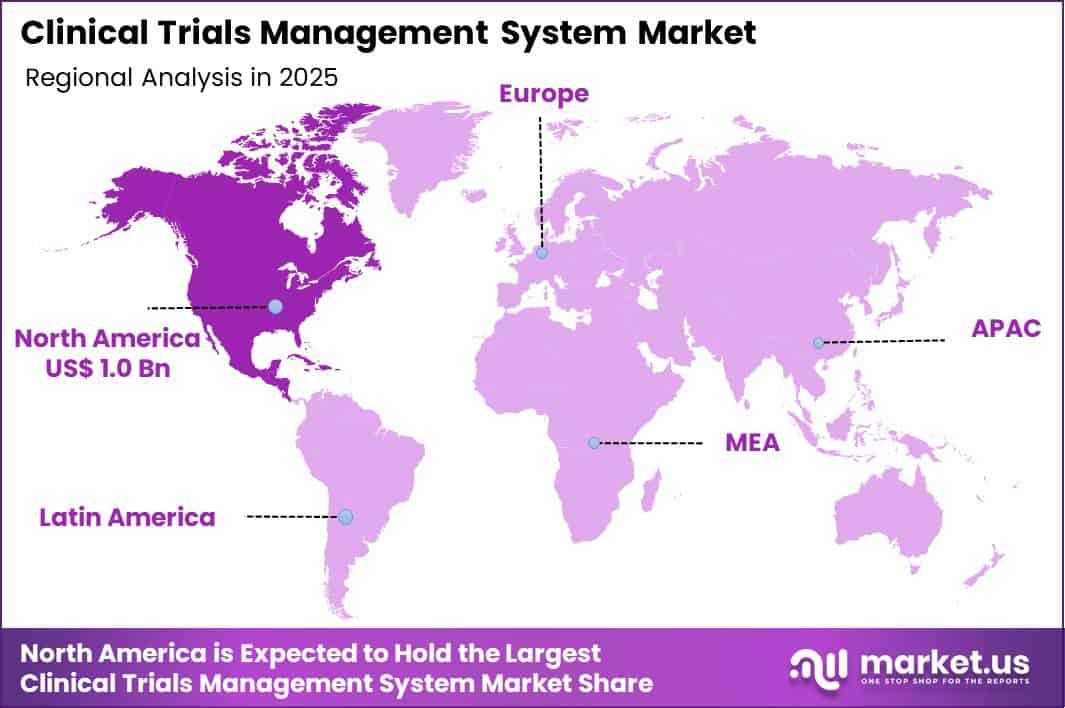

The Global Clinical Trials Management System Market size is expected to be worth around US$ 9.0 billion by 2035 from US$ 2.2 billion in 2025, growing at a CAGR of 15.1 during the forecast period 2026-2035. In 2025, North America led the market, achieving over 46.3% share with a revenue of US$ 1.0 Billion.

Increasing complexity of clinical trials and stringent regulatory demands drive the Clinical Trials Management System market as pharmaceutical companies and research organizations seek integrated platforms that streamline operations and ensure compliance. These systems enable efficient patient recruitment by automating screening processes and matching eligibility criteria across diverse trial phases, from oncology to rare disease studies.

Researchers utilize them for real-time data collection and management, capturing electronic case report forms and adverse event reports to accelerate analysis in multi-site global trials. Sponsors apply these tools to oversee site performance, tracking enrollment rates and protocol adherence in cardiovascular and neurology investigations.

Contract research organizations leverage the systems for budget and timeline management, optimizing resource allocation in vaccine development and Phase III efficacy trials. Clinical teams also employ them for regulatory submissions, generating compliant documentation that expedites approvals for biologics and device-combination studies.

Manufacturers pursue opportunities to incorporate artificial intelligence for predictive analytics, expanding applications in risk-based monitoring that identifies deviations early in adaptive trial designs. Developers advance cloud-based integrations with wearable devices, broadening utility in decentralized trials where remote data capture supports patient-centric endpoints in chronic disease management.

These innovations facilitate seamless collaboration among stakeholders, enhancing protocol optimization in immunotherapy and gene therapy protocols. Opportunities emerge in blockchain-enabled systems that ensure data integrity and traceability for multi-center studies.

Companies invest in user-friendly interfaces that support mobile access, improving investigator engagement in long-term follow-up trials. Recent trends emphasize interoperability with electronic health records and real-time dashboards, positioning the market for growth in value-driven research focused on efficiency, data quality, and accelerated therapeutic advancements.

Key Takeaways

- In 2025, the market generated a revenue of US$ 2.2 Billion, with a CAGR of 15.1, and is expected to reach US$ 9.0 Billion by the year 2035.

- The solution segment is divided into enterprise CTMS and site-based CTMS, with enterprise ctms taking the lead with a market share of 74.0%.

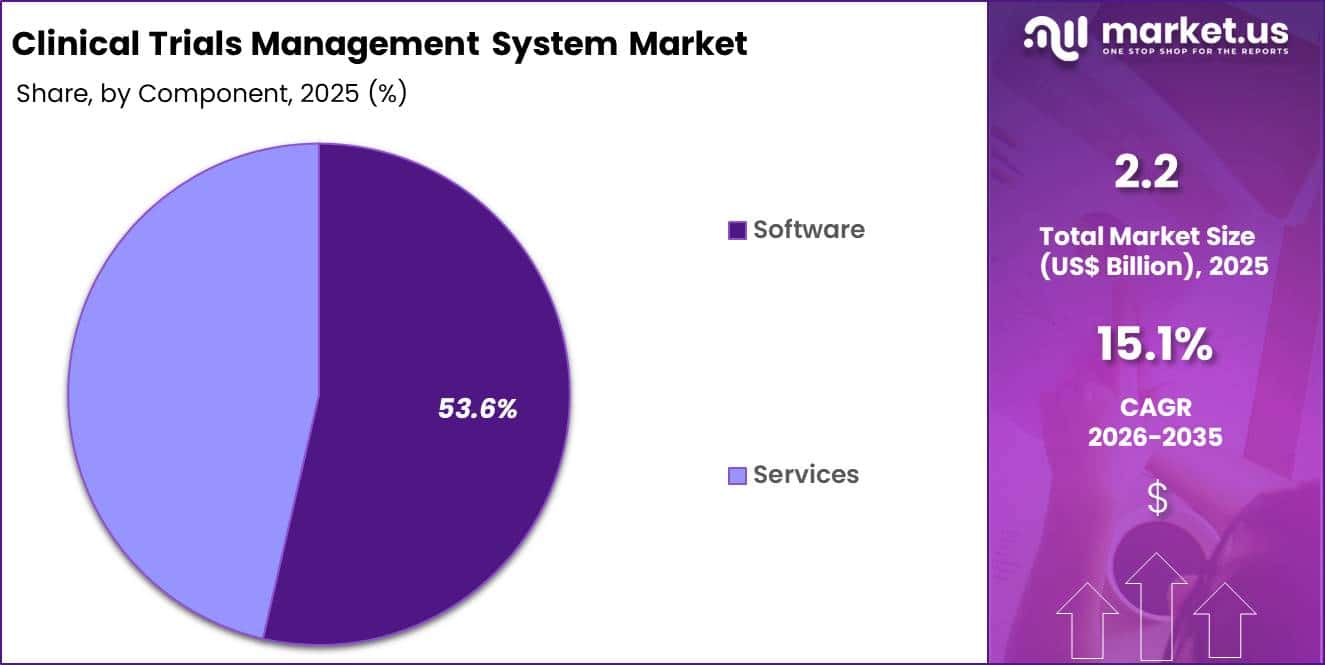

- Considering component, the market is divided into software and services. Among these, software held a significant share of 53.6%.

- Furthermore, concerning the deployment mode segment, the market is segregated into cloud-based, web-based and on-premises. The web-based sector stands out as the dominant player, holding the largest revenue share of 44.1% in the market.

- The end user segment is segregated into pharmaceutical & biotech companies, contract research organizations (CROs), medical device manufacturers and academic & research institutions, with the pharmaceutical & biotech companies segment leading the market, holding a revenue share of 31.7%.

- North America led the market by securing a market share of 46.3%.

Solution Analysis

Enterprise CTMS accounted for 74.0% of growth within solution and dominated the clinical trials management system market due to the need for centralized oversight across multi-country trials. Large sponsors manage complex study portfolios that require integrated budgeting, site monitoring, and regulatory tracking.

Enterprise platforms unify data streams from multiple regions, which improves operational transparency and compliance control. Growing trial complexity increases demand for scalable and standardized management systems.

Growth strengthens as global trials expand across diverse geographies and therapeutic areas. Sponsors prioritize risk-based monitoring and real-time reporting to maintain regulatory alignment. Integration with electronic data capture and safety systems enhances operational efficiency.

Portfolio-level analytics further support strategic planning. The segment is expected to remain dominant as pharmaceutical pipelines continue to globalize and diversify.

Component Analysis

Software generated 53.6% of growth within component and emerged as the leading segment due to its role as the core engine of trial management functionality. Organizations invest in configurable software modules that automate site payments, milestone tracking, and document management. Increased digitalization across research operations drives direct investment in platform capabilities. Sponsors prioritize system interoperability to streamline clinical workflows.

Growth accelerates as artificial intelligence and advanced analytics enhance study forecasting and resource allocation. Continuous software upgrades improve usability and regulatory reporting features. Subscription-based licensing models increase recurring revenue streams.

Demand for cybersecurity and audit readiness further strengthens software adoption. The segment is anticipated to maintain leadership as digital transformation remains central to clinical trial efficiency.

Deployment Mode Analysis

Web-based deployment contributed 44.1% of growth within deployment mode and led the clinical trials management system market due to ease of access and simplified implementation. Research teams value browser-based platforms that allow remote collaboration without extensive infrastructure investment.

Global study teams rely on web interfaces to coordinate site activities and monitor progress in real time. Rapid onboarding capabilities improve operational agility.

Growth continues as hybrid work models increase demand for accessible trial management tools. Web-based systems reduce local IT maintenance burdens and support faster updates. Integration with external data systems enhances workflow continuity. Security enhancements improve user confidence in remote access environments. The segment is projected to remain dominant as organizations seek flexible and widely accessible trial management solutions.

End-User Analysis

Pharmaceutical and biotech companies accounted for 31.7% of growth within end user and dominated the clinical trials management system market due to their extensive research pipelines. These organizations manage multiple concurrent trials across various phases, which increases demand for structured oversight platforms. Regulatory complexity and global expansion require centralized data coordination. High R&D expenditure further supports investment in advanced management systems.

Growth strengthens as personalized medicine and biologics development increase trial volume and complexity. Sponsors seek real-time visibility into recruitment and site performance metrics.

Strategic partnerships with CROs reinforce the need for interoperable systems. Digital compliance frameworks further elevate system utilization. The segment is expected to remain a primary growth driver as pharmaceutical and biotech innovation continues to expand globally.

Key Market Segments

By Solution

- Enterprise CTMS

- Site-Based CTMS

By Component

- Software

- Services

By Deployment Mode

- Cloud-based

- Web-based

- On-Premises

By End User

- Pharmaceutical & Biotech Companies

- Contract Research Organizations (CROs)

- Medical Device Manufacturers

- Academic & Research Institutions

Drivers

Increasing number of clinical trials is driving the market.

The global surge in clinical trial registrations has significantly boosted the demand for efficient management systems to handle complex data and regulatory requirements. Enhanced collaboration between pharmaceutical companies and research organizations has led to more trials in diverse therapeutic areas.

Healthcare regulators are encouraging digital solutions to streamline trial oversight and compliance. The correlation between rising R&D investments and trial volume underscores the need for scalable CTMS platforms. Government-funded initiatives in oncology and infectious diseases contribute to this growth.

Clinical trial management systems enable real-time tracking of patient recruitment and data collection, improving efficiency. National databases show consistent yearly increases in trial initiations.

Key providers are upgrading systems to support decentralized trial models. This driver fosters innovation in data integration and analytics features. The World Health Organization’s International Clinical Trials Registry Platform reported over 500,000 trials registered globally as of 2024, with steady annual growth from 2022 to 2024.

Restraints

High implementation costs are restraining the market.

The substantial upfront expenses for deploying clinical trial management systems, including software licenses and integration with existing IT infrastructure, limit adoption in smaller research organizations. Complex customization requirements for multi-site trials add to the financial burden during setup. Healthcare facilities in developing regions often face budget constraints that delay system upgrades.

Regulatory compliance for data security further increases validation and training costs. In academic institutions, limited grants restrict investments in premium CTMS solutions. Providers may opt for manual processes or basic tools to control spending. This restraint is particularly acute in non-profit and government-funded trials.

Industry reports highlight ongoing maintenance fees as a ongoing challenge. Despite long-term efficiency gains, initial capital outlays hinder market penetration. According to company reports, implementation costs for enterprise CTMS can range from $300,000 to $500,000 for mid-sized organizations in 2022-2024.

Opportunities

Growth in emerging markets is creating growth opportunities.

The rapid expansion of clinical research in Asia-Pacific and Latin America presents significant potential for CTMS adoption in underserved regions. Governmental incentives for foreign investment in biotechnology support the establishment of new trial sites requiring management systems. Increasing outsourcing of trials to low-cost locations amplifies demand for scalable CTMS platforms.

Partnerships with local CROs facilitate regulatory alignment and system deployment. The large patient pools in populous countries like India and China magnify prospects for multi-center trial management. Educational initiatives for local researchers promote standardized CTMS use in emerging economies. This opportunity enables global vendors to diversify beyond saturated Western markets.

Key companies are establishing regional offices to provide customized support. Overall, emerging market growth aligns with efforts to globalize clinical research. Veeva Systems reported a 15% revenue increase in Asia-Pacific for fiscal year 2024, driven by CTMS demand.

Impact of Macroeconomic / Geopolitical Factors

Broader economic cycles affect the clinical trials management system market by shaping sponsor cash flow, site budgets, and technology investment priorities. When inflation remains elevated and borrowing costs stay high, emerging biotech firms delay trial launches and defer enterprise software upgrades.

Geopolitical uncertainty complicates multinational studies through shifting data localization rules, cross border contracting limits, and travel restrictions for monitoring teams. Current US tariffs on imported servers, networking hardware, and certain electronic components increase infrastructure expenses for platform providers and research organizations, which tightens operating margins and extends procurement timelines.

These pressures slow expansion plans and create additional scrutiny around return on investment. At the same time, cost intensity pushes sponsors toward centralized, cloud based systems that reduce manual effort and improve oversight.

Rising trial complexity and regulatory expectations continue to require structured data management and real time visibility. With disciplined budgeting, scalable platforms, and global collaboration models, the market maintains a stable path toward long term growth.

Latest Trends

Integration of artificial intelligence is a recent trend in the market.

In 2024, the incorporation of AI algorithms in CTMS platforms has advanced predictive analytics for trial risk assessment and patient recruitment. These systems use machine learning to optimize protocol design and identify potential delays early.

Manufacturers have focused on seamless integration with electronic data capture tools for real-time insights. Clinical studies demonstrated improved efficiency in site selection through AI-driven data analysis. Medidata launched an AI-enhanced CTMS module in 2024 for automated compliance monitoring. This innovation addresses challenges in handling large datasets from decentralized trials.

The trend emphasizes user-friendly dashboards for non-technical staff. Regulatory guidance in 2024 supported AI use in trial management with validation requirements. Industry collaborations refine algorithms for accurate forecasting of enrollment rates. These developments aim to reduce timelines while maintaining data integrity in complex studies.

Regional Analysis

North America is leading the Clinical Trials Management System Market

North America held a 46.3% share of the Clinical Trials Management System market in 2024, reflecting strong digitization across pharmaceutical sponsors, CROs, and academic research centers. Organizations expanded cloud-based platforms to manage site performance, patient enrollment, regulatory documentation, and financial tracking in real time. Rising protocol complexity and decentralized trial models increased the need for integrated data oversight tools.

Sponsors prioritized compliance with stringent reporting standards, which strengthened investment in centralized trial management software. Growth in oncology, rare disease, and advanced therapy pipelines further elevated operational demands. Academic medical centers also upgraded legacy systems to support multi-site collaborations.

A clear supporting indicator comes from the National Institutes of Health, which reported a budget of USD 47.5 billion for fiscal year 2023, underscoring sustained funding for clinical research activities that require structured digital management infrastructure.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

The Clinical Trials Management System market in Asia Pacific is expected to expand steadily during the forecast period as regional trial activity accelerates and regulatory frameworks modernize. Governments encourage local participation in global studies to strengthen domestic drug development capabilities.

Sponsors increase site numbers across countries such as China, India, South Korea, and Australia, which raises coordination complexity and drives software adoption. Research institutions invest in centralized digital platforms to streamline ethics approvals, budgeting, and monitoring workflows.

Growing patient pools and faster recruitment timelines make the region attractive for multinational trials. Digital transformation initiatives improve interoperability between hospitals and research sponsors.

A verifiable signal of expanding activity appears in 2023 data from China’s National Medical Products Administration, which continues to report rising numbers of clinical trial registrations annually, highlighting strong momentum that supports structured trial management system growth across Asia Pacific.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the clinical trials management system market grow by enhancing platform interoperability, advanced analytics, and real-time visualization tools that help sponsors and research organizations streamline study planning, execution, and oversight. They also broaden service offerings with e-consent, patient engagement modules, and risk-based monitoring capabilities that improve participant retention and operational efficiency.

Firms pursue strategic partnerships with electronic data capture, safety reporting, and site network providers to create integrated ecosystems that reduce data silos and accelerate decision-making. Geographic expansion into North America, Europe, and fast-growing Asia Pacific captures rising clinical research investments and diversifies revenue streams.

Medidata Solutions, a Dassault Systèmes company, exemplifies a specialized life sciences technology provider with a comprehensive suite of trial planning and execution tools, strong global presence, and coordinated commercialization strategy that aligns product innovation with evolving regulatory and operational needs.

The company drives its competitive agenda through disciplined R&D investment, targeted collaborations with biopharma innovators, and a customer-centric approach that translates technical capability into measurable study performance improvements.

Top Key Players

- IQVIA, Inc.

- Medidata (Dassault Systèmes)

- Veeva Systems

- Wipro Limited

- SimpleTrials

- Oracle

- ICON, plc

- Advarra Inc.

- Clinion

- Clario

- Mednet

- Merative

Recent Developments

- In July 2025, PHARMASEAL entered into a technical collaboration with Viedoc to integrate its Engility Clinical Trial Management System with Viedoc’s Electronic Data Capture platform. The combined cloud-based framework is designed to centralize trial management and data collection, enabling improved study coordination, stronger data integrity, and more efficient regulatory alignment for life sciences organizations conducting global clinical programs.

- In March 2025, Jeeva Clinical Trials introduced a CRO Partnership Program centered on its AI-enabled Clinical Trial Management System. The initiative focuses on specialized contract research organizations operating in areas such as obesity, dermatology, oncology, and rare diseases. By providing a shared, real-time digital environment, the program aims to streamline operational workflows, strengthen patient engagement and compliance, and reduce overall study costs through automation and scalable global infrastructure.

Report Scope

Report Features Description Market Value (2025) US$ 2.2 Billion Forecast Revenue (2035) US$ 9.0 Billion CAGR (2026-2035) 15.1 Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Solution (Enterprise CTMS and Site-Based CTMS), By Component (Software and Services), By Deployment Mode (Cloud-based, Web-based and On-Premises), By End User (Pharmaceutical & Biotech Companies, Contract Research Organizations (CROs), Medical Device Manufacturers and Academic & Research Institutions) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape IQVIA, Medidata, Veeva Systems, Wipro, SimpleTrials, Oracle, ICON, Advarra, Clinion, Clario, Mednet, Merative Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Clinical Trials Management System MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Clinical Trials Management System MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- IQVIA, Inc.

- Medidata (Dassault Systèmes)

- Veeva Systems

- Wipro Limited

- SimpleTrials

- Oracle

- ICON, plc

- Advarra Inc.

- Clinion

- Clario

- Mednet

- Merative

Our Clients

- 178582

- Feb 2026