Quick Navigation

Report Overview

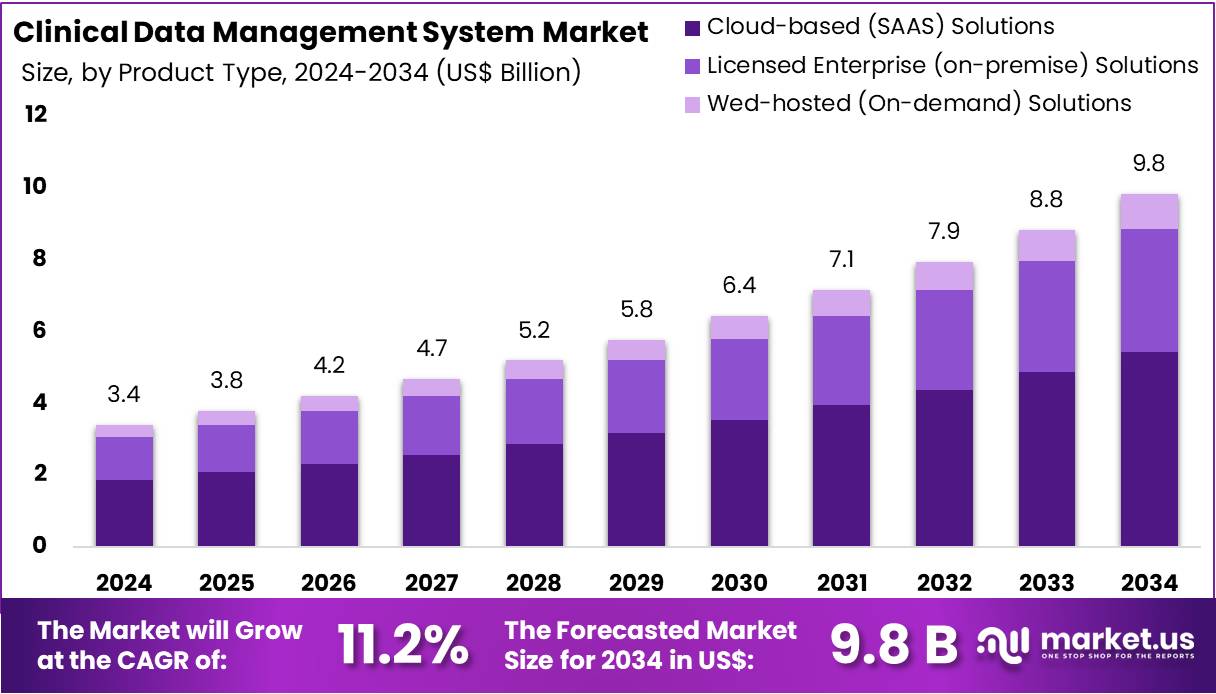

The Global Clinical Data Management System Market size is expected to be worth around US$ 9.8 Billion by 2034, from US$ 3.4 Billion in 2024, growing at a CAGR of 11.2% during the forecast period from 2025 to 2034.

The clinical data management system (CDMS) market is driven by the increasing need for efficient handling of complex clinical trial data, rising regulatory scrutiny, and growing adoption of digital health technologies. Pharmaceutical companies, contract research organizations (CROs), and academic research centers are rapidly transitioning from traditional paper-based methods to sophisticated digital platforms to improve data accuracy, streamline workflows, and reduce the time required for data validation and analysis.

The shift towards decentralized and hybrid clinical trials is significantly influencing demand, as these models rely heavily on real-time data capture and integration across multiple remote sites. The rising number of clinical trials is significantly driving the growth of the global Clinical Data Management System (CDMS) market.

- As of 2024, ClinicalTrials.gov lists over 540,000 studies across 229 countries and territories, highlighting the global expansion of clinical research.

This surge in clinical trials generates vast amounts of data, including patient information, treatment outcomes, and safety assessments, which require efficient management and analysis. CDMS platforms play a crucial role in streamlining data capture, storage, and analysis, ensuring data accuracy, integrity, and compliance with regulatory standards.

Furthermore, the increasing complexity of clinical trials, coupled with stricter regulatory requirements, makes it essential to adopt advanced CDMS solutions for data quality management and real-time access to trial data. With platforms like ClinicalTrials.gov attracting millions of visitors monthly, the demand for reliable and scalable data management systems continues to grow, driving the expansion of the CDMS market.

However, the market faces challenges such as high implementation costs, data interoperability issues, and concerns related to cybersecurity and data privacy. The need for standardization across various platforms and trial phases also remains a key restraint. Nevertheless, strategic collaborations between tech providers, CROs, and life sciences companies are fostering innovation in system architecture and functionality.

As the clinical research landscape becomes more data-intensive and globally interconnected, the role of advanced CDMS platforms is expected to become increasingly central to ensuring the quality, integrity, and efficiency of clinical trial outcomes.

| Location | Number of Registered Studies and Percentage of Total (as of 2025-06-05) |

|---|---|

| U.S. only | 158,436 (29%) |

| Non-U.S. only | 302,217 (56%) |

| Both U.S. and non-U.S. | 24,253 (4%) |

| Not provided | 55,432 (10%) |

| Total | 540,338 (100%) |

Key Takeaways

- The global clinical data management system market was valued at USD 3.4 billion in 2024 and is anticipated to register substantial growth of USD 9.8 billion by 2034, with 11.2% CAGR.

- In 2024, the Cloud-based (SAAS) Solutions segment took the lead in the global market, securing 55.2% of the total revenue share.

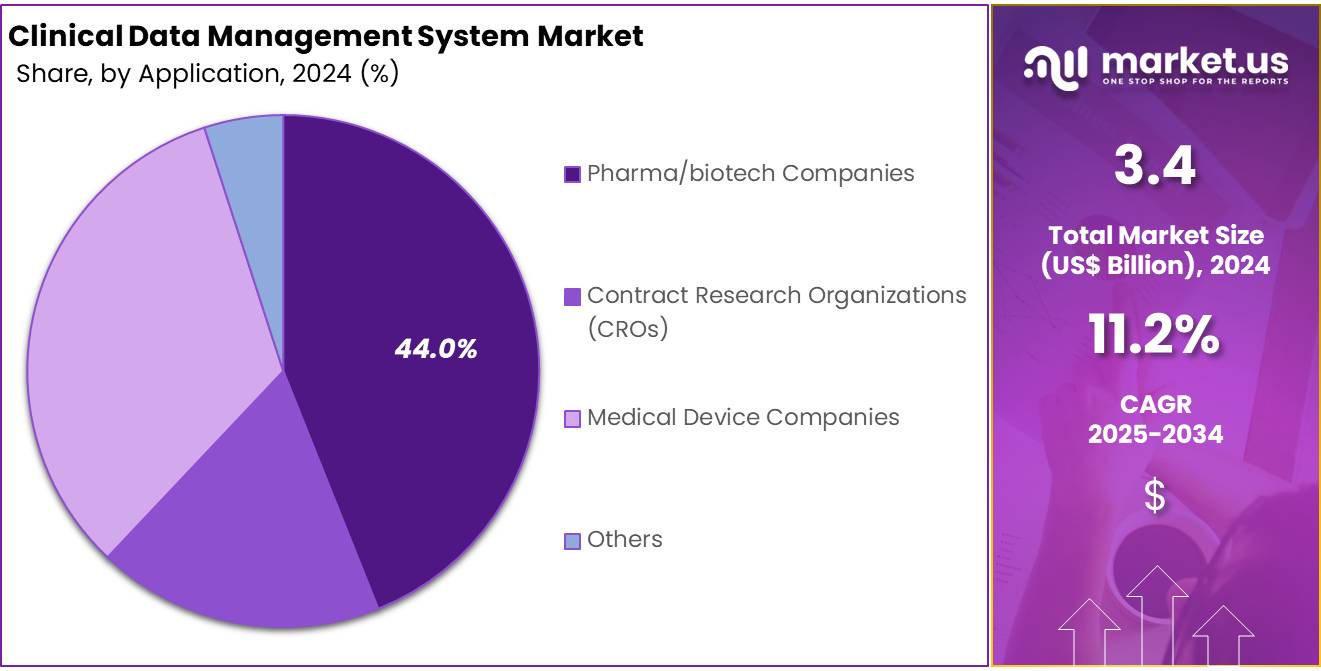

- The Pharma/biotech Companies segment took the lead in the global market, securing 44.0% of the total revenue share.

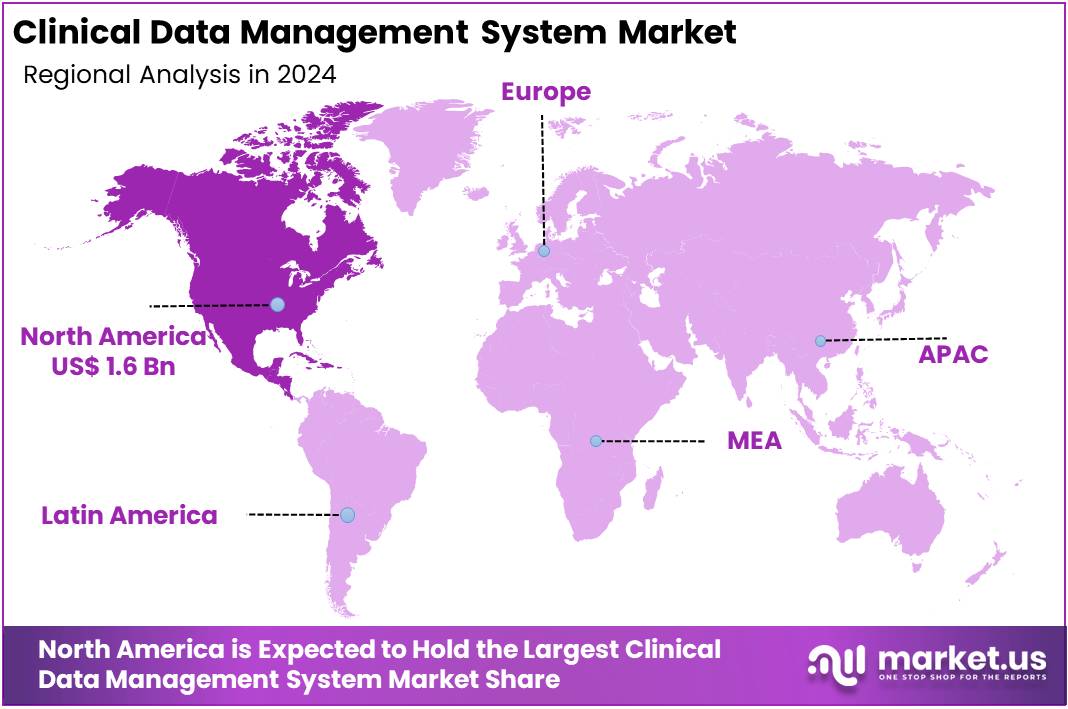

- North America maintained its leading position in the global market with a share of over 48.2% of the total revenue.

Product Type Analysis

Based on product type the market is fragmented into cloud-based (SAAS) solutions, licensed enterprise (on-premise) solutions, and wed-hosted (on-demand) solutions. Amongst these, Cloud-based (SAAS) solutions segment dominated the global clinical data management system market capturing a significant market share of 55.2% in 2024.

The cloud-based (SaaS) solutions segment has emerged as the dominant force in the global Clinical Data Management System (CDMS) market, driven by their scalability, flexibility, and cost-effectiveness. Cloud-based solutions enable seamless data storage, real-time sharing, and collaborative access across multiple stakeholders, such as clinical researchers, investigators, and sponsors, regardless of geographic location. This facilitates faster decision-making and enhances the overall efficiency of clinical trials.

The adoption of cloud-based platforms is particularly attractive due to their ability to scale according to the growing volume of clinical trial data, eliminating the need for significant upfront investments in physical infrastructure. Furthermore, cloud solutions are aligned with the increasing demand for decentralized clinical trials, where remote data collection and real-time monitoring are essential. The continuous development of innovative cloud-based CDMS platforms and the growing preference for SaaS models are propelling the rapid expansion of this segment within the global CDMS market.

- In April 2021, Calyx launched its enhanced Calyx CTMS v15.0 on the Azure cloud platform, aimed at reducing risks and optimizing clinical trial processes. This move underscores the broader trend of companies shifting to cloud-based solutions to streamline operations, ensure compliance, and improve the quality of clinical trial data management.

Application Analysis

The market is fragmented By Application into contract research organizations (CROs), medical device companies, and others. Pharma/biotech Companies dominated the global clinical data management system market capturing a significant market share of 44.0% in 2024. Pharmaceutical and biotechnology segment, driven by their extensive involvement in clinical trials and the increasing complexity of drug development.

These companies are the primary users of CDMS platforms, as they manage large-scale clinical trials that generate massive volumes of data, including patient demographics, treatment outcomes, and safety evaluations. With regulatory requirements becoming more stringent, pharmaceutical and biotech firms rely on CDMS solutions to ensure data accuracy, compliance, and timely submission to regulatory authorities. The need for efficient data management systems is particularly critical as these companies focus on bringing new therapies to market faster and at lower costs.

Moreover, the shift towards personalized medicine and targeted therapies, which require more sophisticated and accurate data handling, further fuels the demand for advanced CDMS platforms. As the pharmaceutical and biotechnology industries continue to innovate and expand, particularly in the fields of rare diseases and oncology, the reliance on robust data management solutions will only increase.

Additionally, the integration of artificial intelligence (AI) and machine learning (ML) into CDMS solutions allows these companies to optimize trial efficiency, mitigate risks, and accelerate drug development timelines, further reinforcing the dominance of pharma and biotech companies in the global CDMS market.

Key Segments Analysis

By Product Type

- Cloud-based (SAAS) Solutions

- Licensed Enterprise (on-premise) Solutions

- Wed-hosted (On-demand) Solutions

By Application

- Pharma/biotech Companies

- Contract Research Organizations (CROs)

- Medical Device Companies

- Others

Drivers

Increased Prevalence of Chronic Disorders

The clinical data management system (CDMS) market is witnessing substantial momentum, largely driven by the growing volume of clinical trials being conducted worldwide. As the pharmaceutical, biotechnology, and healthcare sectors intensify their research and development efforts, there is an escalating need for reliable and efficient data management solutions.

These trials generate vast datasets encompassing patient demographics, treatment responses, and safety metrics—making the role of streamlined data handling increasingly critical. Effective data management ensures the integrity, precision, and regulatory compliance of clinical trial operations. CDMS solutions are central to this process, facilitating accurate data collection, secure storage, and analytical insights, all of which contribute to the overall success of clinical trials. The complexity of modern trials and tightening regulatory frameworks further underscore the importance of adopting advanced digital tools.

- For instance, in January 2023, Tata Consultancy Services (TCS) introduced its Connected Clinical Trials (CCT) platform, a Software as a Service (SaaS) solution aimed at revolutionizing patient engagement and optimizing clinical supply chain management—marking a pivotal step in enhancing trial efficiency and accountability.

Restraints

Lack of Skilled Professionals

The global clinical data management system market is the challenge of data interoperability and integration across diverse platforms. Clinical trials often involve multiple stakeholders, including pharmaceutical companies, contract research organizations (CROs), healthcare providers, and regulatory bodies. These stakeholders frequently rely on various data management systems, software, and platforms, many of which are not fully compatible with each other. This lack of seamless integration can result in inefficiencies, delays, and increased costs, as data needs to be manually transferred or reformatted between systems.

Additionally, clinical data often comes from a variety of sources, including electronic health records (EHRs), laboratory systems, and patient-reported outcomes, all of which may have different formats, standards, and protocols. The inability to integrate this data effectively into a unified system can lead to incomplete or inaccurate datasets, compromising the quality and integrity of clinical trial results. Furthermore, regulatory requirements across different regions and countries add another layer of complexity, as CDMS platforms must be designed to comply with varying standards such as HIPAA, GDPR, and 21 CFR Part 11.

Opportunities

Increasing Adoption of Cloud-based CDMS Solutions

The CDMS market is witnessing a significant shift toward cloud-based solutions, driven by the increasing demand for flexible, scalable, and efficient data infrastructure. Cloud technology has revolutionized data handling in healthcare and clinical research by enabling seamless accessibility, enhanced collaboration, and streamlined operations.

Cloud-based CDMS platforms allow organizations to manage large volumes of clinical trial data without the need for substantial investments in physical infrastructure. These solutions also support real-time data sharing among key stakeholders including researchers, investigators, and sponsors regardless of geographical location, thereby improving coordination and accelerating decision-making processes. The ability to access and analyze data simultaneously from multiple sites enhances the speed and accuracy of clinical research.

- For instance, in July 2023, Eitan Medical, a developer of drug delivery technologies, introduced Eitan Insights a cloud-based infusion management system specifically designed to address the evolving needs of at-home and specialty infusion therapies. This move highlights the broader industry shift toward cloud-enabled platforms to support the growing demands of decentralized and patient-centric clinical models.

Impact of macroeconomic factors / Geopolitical Factors

Macroeconomic and geopolitical factors have a notable impact on the global CDMS market, influencing both the demand for data management solutions and the ability of organizations to adopt them. Economic slowdowns or recessions can lead to reduced funding for research and development, resulting in fewer clinical trials and delayed project timelines. This, in turn, may decrease the demand for CDMS solutions, as pharmaceutical companies and contract research organizations (CROs) may scale back their investments in digital infrastructure.

Conversely, periods of economic growth, particularly in emerging markets, can drive increased healthcare investments, fueling the adoption of CDMS to streamline clinical trials and improve operational efficiency. Geopolitical tensions, trade barriers, and regulatory changes also play a role, as varying compliance requirements across regions can complicate the integration of clinical trial data across borders.

For example, stricter data privacy laws like the General Data Protection Regulation (GDPR) in Europe can create additional challenges for global trials, requiring CDMS providers to adapt their platforms to meet these regulations. Similarly, geopolitical instability or disruptions in supply chains due to factors like pandemics or regional conflicts can delay the rollout of CDMS technologies. As a result, these macroeconomic and geopolitical factors can introduce both challenges and opportunities, shaping the pace of innovation and expansion in the CDMS market.

Latest Trends

The global CDMS market is experiencing significant transformation driven by several key trends. The integration of AI and ML technologies is enhancing data accuracy and predictive analytics, thereby accelerating clinical trial timelines and improving patient outcomes. Additionally, the adoption of cloud-based solutions is increasing due to their scalability, cost-effectiveness, and ability to facilitate real-time data sharing among stakeholders across various locations.

This shift supports the growing trend of decentralized and hybrid clinical trials, which aim to improve patient recruitment and retention by offering more flexible participation options. Furthermore, the emphasis on data interoperability is pushing for standardized data formats and seamless integration across diverse platforms, addressing challenges in data exchange and compliance with global regulations.

The implementation of risk-based monitoring approaches is also gaining traction, focusing on identifying and mitigating potential issues proactively, thus enhancing the quality and efficiency of clinical trials. These trends reflect the industry’s commitment to leveraging technological advancements to streamline clinical data management processes, ensuring more efficient and effective drug development.

Regional Analysis

North America leads the CTMS market, driven by the region’s advanced research institutions, universities, and major pharmaceutical and medical device companies. These organizations are at the forefront of clinical trials, leveraging CTMS for efficient trial planning, monitoring, and regulatory compliance. Additionally, North America benefits from robust healthcare infrastructure, ensuring optimal conditions for conducting clinical trials. Government policies also play a significant role in strengthening the market.

- In January 2023, the Canadian government launched several health-focused initiatives. These included national training platforms, a clinical trial consortium, and multiple research projects aimed at improving public health outcomes. To support this effort, around USD 60.0 million was allocated to fund 22 clinical trial-related projects. The funding emphasized trials that align with Canada’s Biomanufacturing and Life Sciences Strategy (BLSS). These actions reflect a strong push toward strengthening clinical research infrastructure and promoting innovation in healthcare and life sciences across the country.

These investments and initiatives contribute to the growing demand for CTMS solutions in the region, ensuring that North America remains a dominant player in the global market. This supportive environment, combined with technological innovation and government backing, positions North America as the leading market for clinical trials management systems.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The global CDMS market is characterized by a dynamic competitive landscape, featuring a blend of established industry leaders and emerging innovators. Key players such as Oracle Corporation, Medidata Solutions, Veeva Systems, IBM Watson Health, and eClinical Solutions LLC dominate the market, offering comprehensive platforms that support various aspects of clinical trial data management, including data capture, validation, and analysis.

These companies leverage advanced technologies like artificial intelligence (AI), machine learning (ML), and cloud computing to enhance data accuracy, streamline workflows, and ensure regulatory compliance. The market is also witnessing the rise of specialized providers such as CluePoints, which focuses on risk-based quality management and data analytics to improve data quality in clinical trials.

Veeva Systems Inc., is a leading provider of cloud-based software solutions tailored for the global life sciences industry. The company specializes in applications for clinical trials, regulatory compliance, quality management, and commercial operations. Veeva’s offerings, such as Veeva Vault and Veeva Clinical Suite, are designed to streamline processes, enhance collaboration, and ensure compliance with industry standards.

Oracle Corporation, is a multinational technology company renowned for its comprehensive suite of enterprise software solutions. The company specializes in database management systems, cloud applications, and enterprise resource planning (ERP) software. Oracle’s flagship product, Oracle Database, is widely utilized across various industries for data management and analytics.

Top Key Players in the Clinical Data Management System Market

- IBM Watson Health

- Veeva System

- Oracle Corporation

- Ennov

- OpenClinica LLC

- Fortress Medical

- Medidata Solutions (Dassault Systems)

- Perceptive Informatics

- Medidata Rave

- Forte Research Systems

- IBM Watson Health

- Fortress Medical Systems

Recent Developments

- In August 2024: Clinical Ink, a global life sciences technology company, launched EDCXtra, an advanced electronic data capture (EDC) system for clinical trials. The system combines direct data capture (DDC), electronic clinical outcome assessments (eCOAs), and electronic consent (eConsent) solutions into a unified web-based platform. This integrated solution is designed to streamline the data capture process in clinical trials, ensuring compliance with good clinical practice (GCP) standards.

- In April 2025: Veeva Systems introduced Veeva SiteVault CTMS, a clinical trial management system tailored for research sites. The platform integrates SiteVault eISF and SiteVault eConsent, providing research sites with a comprehensive system for managing clinical trials. Integration with Veeva’s Clinical Platform allows seamless bidirectional data flow between sites and sponsors, reducing manual tasks and enhancing overall efficiency.

- In January 2024: BSI Life Sciences announced a new partnership with Ocular Therapeutix, which will utilize BSI’s cloud-based Clinical Trial Management System for its clinical trial needs.

- In November 2024: Medidata, a Dassault Systèmes brand and a leading provider of clinical trial solutions, was recognized as a leader in Everest Group’s inaugural Life Sciences Clinical Trial Management System Products PEAK Matrix® Assessment 2024. The assessment evaluated 13 providers based on their market impact and ability to deliver high-quality, successful offerings.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 3.4 billion |

| Forecast Revenue (2034) | US$ 9.8 billion |

| CAGR (2025-2034) | 11.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Cloud-based (SAAS) Solutions, Licensed Enterprise (on-premise) Solutions, and Wed-hosted (On-demand) Solutions), By Application (Pharma/biotech Companies, Contract Research Organizations (CROs), Medical Device Companies, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | IBM Watson Health, Veeva System, Oracle Corporation, Ennov, OpenClinica, LLC, Fortress Medical, Medidata Solutions (Dassault Systems), Perceptive Informatics, Medidata Rave, Forte Research Systems, IBM Watson Health, and Fortress Medical Systems |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |