Quick Navigation

- Report Overview

- Key Takeaways

- China Size and Growth (2025-2034)

- Packaging Type Analysis

- Testing Type Analysis

- End-User Industry Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Regions and Countries

- Key Player Analysis

- Recent Developments

- Report Scope

Report Overview

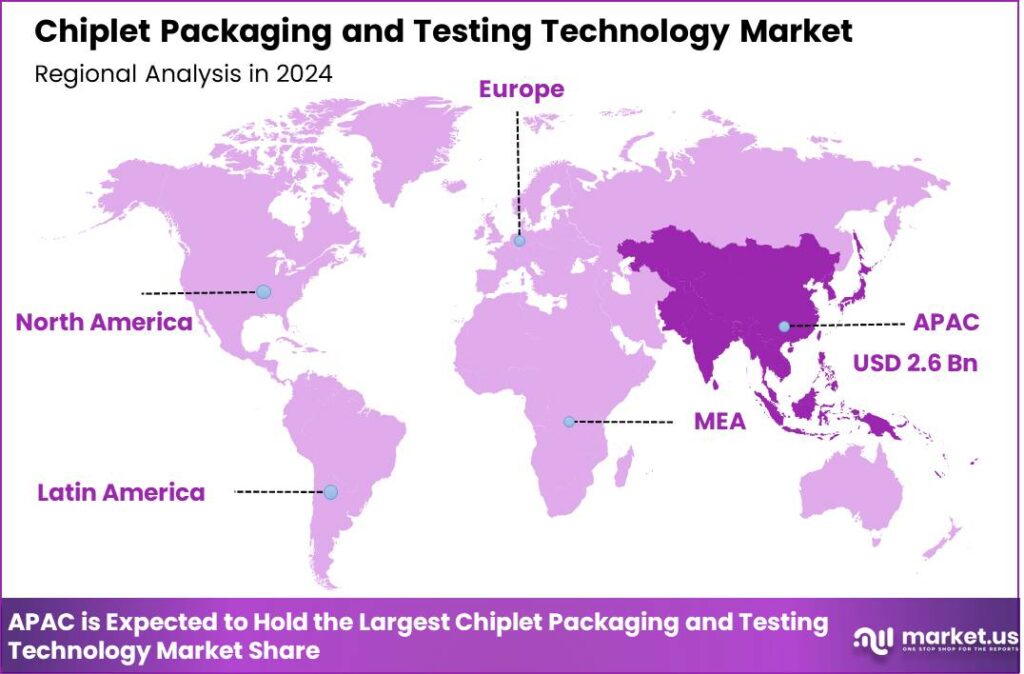

The Chiplet Packaging and Testing Technology Market size is expected to be worth around USD 431.8 Bn By 2034, from USD 5.5 bn in 2024, growing at a CAGR of 54.7% during the forecast period. In 2024, the APAC region led the market, accounting for over 48.6% of the global market share and generating revenue of USD 2.6 bn. Within this region, China’s market size stood at USD 1.38 bn, experiencing a robust annual growth rate of 56%.

Chiplet packaging and testing technology represents an innovative approach to semiconductor design and assembly. Instead of manufacturing a single, large chip, chiplet technology involves integrating multiple smaller chips, or chiplets, into a single package. These chiplets can be optimized for specific functions, which, when combined, deliver the performance of a monolithic chip but with greater flexibility and efficiency.

The market for chiplet packaging and testing technology is expanding, driven by the need for more efficient and powerful semiconductor solutions. This market addresses a broad range of applications, from consumer electronics to high-performance computing systems. As industries increasingly demand smaller, faster, and more energy-efficient electronic devices, the role of chiplet technology grows, positioning it as a critical component in the next generation of semiconductor manufacturing.

Several factors drive the growth of the chiplet packaging and testing technology market. First, the increasing complexity of semiconductor devices necessitates more adaptable and scalable manufacturing methods. Chiplets offer a way to meet this complexity without the exponential costs associated with developing larger, more integrated chips.

Additionally, the push towards artificial intelligence, machine learning, and big data analytics requires high-performance computing capabilities that chiplet technology can provide. This technology enables the rapid deployment of specialized processors tailored to specific computational tasks, thereby enhancing overall system efficiency.

Market demand for chiplet packaging and testing technology is primarily fueled by the consumer electronics, automotive, and telecommunications sectors. Each of these industries requires high-performance computing capabilities that are both cost-effective and energy-efficient. The flexibility of chiplets allows manufacturers to quickly adapt to changing market needs and technological standards, further stimulating demand.

As electronic devices become more integrated into daily life and the Internet of Things (IoT) expands, the demand for chiplets is expected to continue rising. The chiplet packaging and testing technology market presents numerous opportunities, particularly in the development of products for emerging technologies such as 5G, IoT, and autonomous vehicles.

These technologies require high data processing capabilities and low power consumption, which chiplets can provide. Additionally, the ongoing miniaturization of electronic devices offers another significant opportunity for the application of chiplet technology, as it supports the development of smaller, more powerful components.

According to Market.us Analysts, The global chiplets market is set for explosive growth, projected to reach USD 107.0 billion by 2033, up from USD 3.1 billion in 2023, with a remarkable CAGR of 42.5% from 2024 to 2033. In 2023, the Asia-Pacific (APAC) region emerged as a key player, claiming over 40% of the global market share. APAC’s chiplets revenue was valued at approximately USD 1.2 billion, driven by strong demand from industries like consumer electronics and data centers.

Technological advancements in chiplet packaging and testing are continually reshaping the market landscape. Innovations such as improved interconnect technologies that enhance communication between chiplets and more sophisticated testing methods to ensure reliability are pivotal. These advancements not only improve the performance and flexibility of chiplet-based assemblies but also reduce manufacturing costs and time-to-market.

Key Takeaways

- The Chiplet Packaging and Testing Technology Market is on track for explosive growth. Valued at just USD 5.5 billion in 2024, the market is projected to reach a staggering USD 431.8 billion by 2034, expanding at a CAGR of 54.7% during the forecast period.

- The Asia-Pacific (APAC) region emerged as the top market in 2024, accounting for 48.6% of the global revenue and generating USD 2.6 billion.

- Within APAC, China stood out as a key contributor. The country’s market size hit USD 1.38 billion in 2024, driven by the strong adoption of chiplet-based solutions in electronics and semiconductor manufacturing

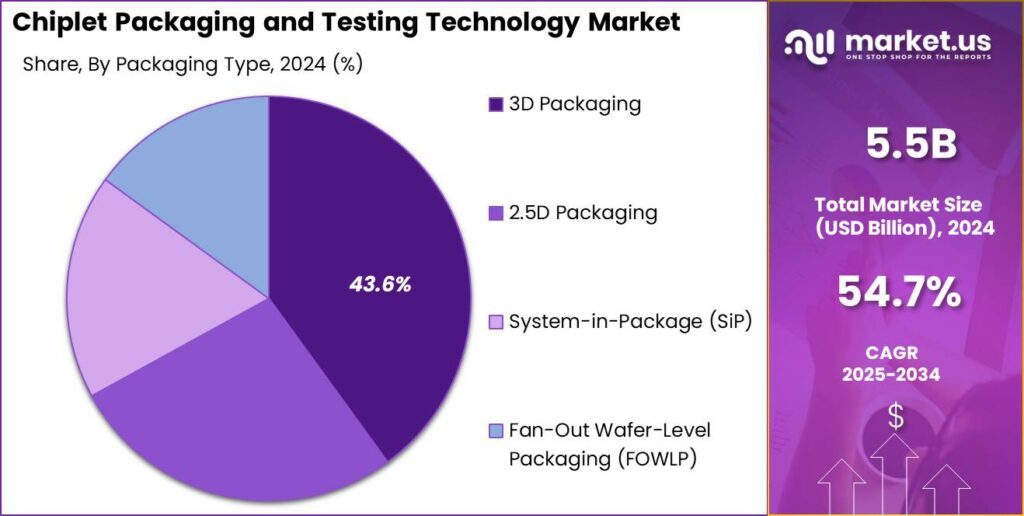

- Among various packaging methods, 3D Packaging took the lead in 2024. This segment captured 43.6% of the total market share, reflecting the growing demand for higher-performance, space-saving packaging solutions across industries like automotive, healthcare, and data centers.

- On the testing front, Pre-Packaging Testing remained the dominant segment in 2024, accounting for 55.7% of the market.

- The Consumer Electronics sector continues to be a major driver of growth for chiplet packaging and testing technology. In 2024, this segment accounted for 34.9% of the total market share.

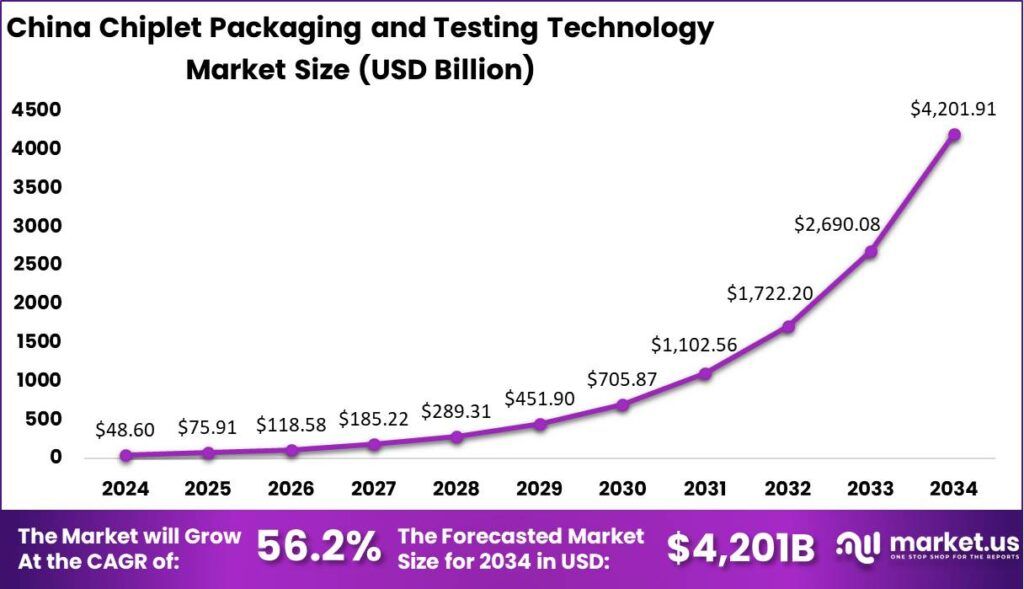

China Size and Growth (2025-2034)

China is rapidly advancing in the field of Chiplet Packaging and Testing Technology, leveraging several strategic advantages that position it at the forefront of this market segment. The Chinese market exhibited a size of USD 1.38 billion in 2024 and is expected to grow at a CAGR of 56.2% due to multiple converging factors.

- Government Support and Infrastructure Investments: The Chinese government has prioritized semiconductor development as a key area for advancement, providing substantial financial and policy support. This initiative is part of a broader strategy to achieve technological self-reliance and leadership. Investments in state-of-the-art facilities and research institutions have enabled rapid advancements in chiplet technologies and their applications.

- Integrated Supply Chains and Manufacturing Capabilities: China benefits from robust, integrated supply chains that enhance the efficiency of chiplet manufacturing. The presence of leading foundries and packaging companies within the country reduces logistical hurdles and speeds up the development cycle for new technologies. This integration facilitates the rapid scaling of chiplet production capabilities to meet both domestic and international demand.

- Focus on Innovation and R&D: Chinese companies are increasingly focusing on research and development to drive innovation in chiplet technology. This includes enhancements in 2.5D/3D packaging technologies and system-in-package solutions, which are critical for the high-performance computing demands of today’s chiplet applications. The commitment to R&D helps in refining the technologies that underpin chiplet designs, making them more efficient and adaptable to various computing needs.

- Partnerships and Global Collaboration: To foster growth and stay ahead of technological trends, Chinese firms are actively engaging in partnerships and collaborations with global tech giants. These collaborations help in the exchange of ideas, sharing of resources, and alignment of strategic interests, which are essential for sustaining innovation and managing the complexities associated with advanced chiplet packaging.

In 2024, APAC held a dominant market position in the Chiplet Packaging and Testing Technology market, capturing more than a 48.6% share with a revenue of USD 2.6 billion. This significant market share is attributed to several key factors that position APAC as the leader in this technology segment.

- Rapid Industrial Growth and Technology Adoption: APAC has been at the forefront of adopting and integrating new technologies across various sectors, including consumer electronics, automotive, and industrial automation. The region’s rapid industrial growth, coupled with a strong emphasis on technological advancement, drives the demand for sophisticated chiplet packaging and testing solutions. This is particularly evident in countries like China, South Korea, and Taiwan, which have substantial semiconductor manufacturing capabilities.

- Government Initiatives and Investments: Governments across the APAC region have launched numerous initiatives and made substantial investments to bolster their domestic semiconductor industries. These initiatives often include subsidies for technology companies, improvements in intellectual property protections, and significant funding for research and development. Such policies have encouraged both domestic and foreign firms to invest in chiplet technology research and development, contributing to the regional market’s growth.

- Strategic Collaborations and Innovation: APAC’s leadership in the chiplet market is also bolstered by strategic collaborations between regional tech giants and global semiconductor players. These partnerships focus on innovation in chiplet designs and packaging techniques, aiming to address the growing needs for high-performance computing and connectivity solutions. The collaborative efforts also extend to academic and research institutions, furthering the development of cutting-edge chiplet technologies.

- Skilled Workforce and Advanced Manufacturing Capabilities: The region benefits from a highly skilled technical workforce, capable of managing advanced manufacturing processes required for chiplet production. The availability of such talent, coupled with advanced manufacturing infrastructures, enables APAC to maintain high standards in chiplet technology production and testing, ensuring continued growth and dominance in the global market.

Packaging Type Analysis

In 2024, the 3D Packaging segment exhibited a dominant position in the chiplet packaging and testing technology market, capturing a significant market share of over 43.6%. This leadership can be attributed to several technological and market-driven factors that underline the essential role of 3D Packaging in modern semiconductor applications.

3D Packaging has become increasingly pivotal due to its ability to provide high-performance solutions in a compact form. By stacking chiplets vertically, 3D Packaging techniques achieve superior die-to-die interconnect density and minimize the footprint on the silicon, which is crucial for applications requiring high bandwidth and low latency.

This architectural advantage facilitates better performance and energy efficiency, making it ideal for high-end computing environments like data centers and advanced consumer electronics. The market’s gravitation towards 3D Packaging is also driven by the evolving needs of electronic devices that demand higher computational power and smaller sizes.

In sectors like healthcare, consumer electronics, and automotive, where advanced features such as wireless connectivity, 3D visualization, and circuit miniaturization are required, 3D Packaging provides a viable solution that supports these complex functionalities. This adoption is amplified by the continuous push for more powerful processing capabilities in smaller and more efficient form factors.

Furthermore, the integration capabilities of 3D Packaging, where multiple functions are encapsulated within a single unit, align with the industry’s trend towards system-level enhancements. This not only simplifies the design and manufacturing processes but also improves the overall system reliability and speed by reducing the interconnect lengths between different components.

The cost-effectiveness of 3D Packaging, combined with its technical benefits, makes it a preferred choice among manufacturers, driving its growth and predominance in the market. Overall, the 3D Packaging segment continues to lead due to its alignment with industry demands for miniaturization, high performance, and integration, marking it as a cornerstone technology that will likely maintain its market prominence in the foreseeable future.

Testing Type Analysis

In 2024, the Pre-Packaging Testing segment in the chiplet packaging and testing technology market held a dominant market position, capturing more than a 55.7% share. This leadership is underpinned by several key factors that highlight its critical role in the semiconductor manufacturing process.

Pre-Packaging Testing is essential in ensuring the reliability and functionality of chiplets before they are assembled into the final semiconductor package. This stage of testing allows manufacturers to identify and address defects or failures in individual chiplets, which is crucial in avoiding costly reworks post-packaging and ensuring high yields in production.

The increasing complexity of chiplet-based designs, which often incorporate multiple integrated circuits (ICs) and advanced materials, further necessitates rigorous pre-packaging testing to meet quality standards and functional specifications. The segment’s prominence is also driven by the growing demand for high-performance computing applications, where the reliability of each component is critical.

In these settings, the failure of a single chiplet can compromise the entire system’s performance, making thorough pre-packaging testing indispensable. Additionally, the expansion of industries such as artificial intelligence and automotive electronics, which require high reliability in semiconductor components, contributes significantly to the growth of this segment.

Economic efficiency also plays a vital role. Pre-Packaging Testing helps in mitigating the financial risk associated with chiplet integration by ensuring only fully functional chiplets proceed to the costly final assembly stages. This efficiency is crucial for maintaining profitability in the highly competitive semiconductor industry, where the optimization of testing processes can lead to significant cost savings and faster time-to-market for new technologies.

Overall, the Pre-Packaging Testing segment’s dominance is attributed to its critical role in enhancing chiplet reliability, ensuring economic efficiency, and meeting the rigorous demands of advanced technological applications. These factors collectively drive its substantial share in the chiplet packaging and testing technology market.

End-User Industry Analysis

In 2024, the Consumer Electronics segment held a dominant market position in the chiplet packaging and testing technology market, capturing more than a 34.9% share. This leadership is largely due to the rapid integration of chiplet technology across a wide range of consumer electronic devices, from smartphones to advanced computing systems, which demand higher performance and more efficient power consumption.

The preeminence of the Consumer Electronics segment is propelled by the ongoing miniaturization trend in electronics, requiring compact yet powerful semiconductor solutions. Chiplets, being small and modular, enable the design of sophisticated electronics that are not only powerful but also space-efficient. This is particularly important in devices like wearable technology, mobile phones, and portable gaming consoles, where space is at a premium but performance demands are high.

Further fueling the growth of this segment is the increasing deployment of technologies such as augmented reality (AR), virtual reality (VR), and high-performance gaming, which require substantial processing power and advanced graphics capabilities. Chiplets facilitate the high-speed analysis and processing needed for these technologies by allowing more versatile and powerful GPU and CPU configurations within smaller device footprints.

Moreover, the rise of the Internet of Things (IoT) and smart devices has expanded the application of chiplets in consumer electronics. By enabling more efficient interconnectivity and faster processing within devices, chiplets are crucial in meeting the performance requirements of connected device ecosystems, enhancing user experiences and device functionality across the consumer electronics landscape.

Overall, the significant market share of the Consumer Electronics segment is driven by the critical role chiplets play in advancing technology in everyday devices, aligning with consumer expectations for functionality, connectivity, and portability in electronics.

Key Market Segments

By Packaging Type

- 2.5D Packaging

- 3D Packaging

- System-in-Package (SiP)

- Fan-Out Wafer-Level Packaging (FOWLP)

By Testing Type

- Pre-Packaging Testing

- Post-Packaging Testing

By End-User Industry

- Consumer Electronics

- Automotive

- Telecommunications

- Industrial

- Healthcare

- Others

Driver

Increasing Demand for High-Performance Computing (HPC)

The chiplet packaging and testing technology market is driven significantly by the escalating need for high-performance computing across various sectors, including cloud computing, data centers, and artificial intelligence. As technological advancements continue to demand more powerful and energy-efficient computing solutions, chiplets have emerged as a crucial component.

They enable more complex and compact designs by allowing multiple chips to function as a single entity, thus providing superior performance compared to traditional monolithic chips. This modular approach not only enhances the computational power but also optimizes energy efficiency, which is critical in large-scale data operations and sophisticated computing tasks.

Restraint

High Costs and Complexity in Manufacturing

One of the primary restraints in the chiplet packaging market is the complexity and high costs associated with advanced packaging technologies, particularly 3D packaging. The intricate processes involved in 3D packaging demand specialized equipment and expertise, leading to higher production costs.

Additionally, issues such as thermal management and signal integrity in densely packed configurations pose significant engineering challenges. These factors can deter adoption, especially in cost-sensitive sectors, limiting the broader application of chiplet technologies in emerging markets and for smaller-scale operations.

Opportunity

Advancements in Semiconductor Manufacturing

The chiplet market is poised for growth with continuous advancements in semiconductor manufacturing processes. Innovations in material science, lithography, and packaging techniques are opening new avenues for chiplet applications.

These technological strides are expected to enhance the integration capabilities of chiplets, allowing for more functionalities within smaller footprints and fostering the development of next-generation electronic devices.

As sectors such as telecommunications and consumer electronics continue to evolve, the demand for compact, high-performance chip solutions will drive significant opportunities in the chiplet technology market.

Challenge

Integration and Interoperability Issues

Despite the advantages, the integration of different chiplets from various manufacturers poses significant challenges, primarily due to compatibility and interoperability issues. Ensuring that chiplets effectively communicate and operate in harmony within a single package requires rigorous standards and testing.

The lack of unified industry standards for chiplet interfaces and interconnects can lead to increased development times and costs, hindering rapid innovation and adoption. Addressing these challenges is crucial for the chiplet industry to realize its full potential, necessitating collaboration and standardization efforts across the semiconductor ecosystem.

Growth Factors

Advancements in High-Performance Computing

The chiplet packaging and testing technology market is experiencing substantial growth, driven by the rising demand for high-performance computing across various sectors, including data centers and artificial intelligence.

This growth is propelled by the need for more efficient, high-speed processing capabilities that chiplets provide, allowing for the integration of diverse functionalities within compact spaces without compromising performance. The versatility of chiplets in combining different technological components into one system enhances their applicability across a broad range of advanced computing tasks, thereby fueling the market expansion.

Emerging Trends

Integration of AI and IoT Technologies

Emerging trends in the chiplet market include the integration of artificial intelligence (AI) and the Internet of Things (IoT). As devices become smarter and more connected, the need for chiplets that can process vast amounts of data quickly and efficiently has become crucial.

This trend is seeing a significant shift towards deploying chiplet architectures in sectors such as consumer electronics and automotive systems, where enhanced data processing capabilities are essential. Furthermore, the development of AI-specific chiplets is set to transform various applications, from cloud computing to edge devices, offering tailored processing capabilities that boost operational efficiency and performance.

Business Benefits

Cost Efficiency and Performance Enhancement

The adoption of chiplet technology in semiconductor manufacturing brings numerous business benefits, primarily cost efficiency and enhanced performance. Chiplets allow for the use of defective dies by integrating them with other functional dies, significantly reducing waste and manufacturing costs.

Moreover, chiplets provide a pathway to circumvent the limitations of Moore’s Law by enabling manufacturers to enhance processor performance through heterogeneous integration rather than traditional scaling. This method not only improves the computational power of devices but also reduces the time and cost associated with developing new full-scale integrated circuits, thereby offering a competitive edge in the fast-evolving tech landscape.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

Intel Corporation continues to advance the chiplet packaging market with its Co-EMIB technology, introduced in 2024, which integrates EMIB and Foveros for superior chiplet integration and performance. Collaborations, such as its June 2024 partnership with Rapidus Corporation, aim to transition chiplet technologies from research to mass production, cementing Intel’s leadership.

Advanced Micro Devices (AMD) leverages chiplet technology to enhance computing efficiency, exemplified by its February 2024 launch of multi-core processors for desktop and server markets. AMD’s focus on strategic acquisitions further strengthens its chiplet packaging capabilities, highlighting its commitment to innovation.

Taiwan Semiconductor Manufacturing Company (TSMC) maintains its leadership with the December 2024 upgrade to its CoWoS technology, delivering higher bandwidth and energy efficiency. TSMC’s collaboration with major chip designers enables optimized packaging solutions, ensuring its cutting-edge position in chiplet technology.

Top Key Players in the Market

- Advanced Semiconductor Engineering Inc. (ASE Group)

- Amkor Technology Inc.

- Intel Corporation

- TSMC (Taiwan Semiconductor Manufacturing Company)

- NVIDIA Corporation

- Samsung Electronics

- Broadcom Inc.

- Qualcomm Incorporated

- Advanced Micro Devices Inc.

- ASE Group

- Others

Recent Developments

- In January 2025: ASE Group announced its new S-SWIFT™ and S-Connect™ package technologies, designed to enhance chiplet integration for high-performance computing applications.

- In January 2025: Amkor presented at the Chiplet Summit 2025, showcasing their latest advancements in chiplet packaging and testing methods.

- December 2024: TSMC introduced an enhanced version of its CoWoS (Chip on Wafer on Substrate) technology, enabling higher bandwidth and more efficient chiplet interconnects.

- September 2024: NVIDIA unveiled a new GPU architecture leveraging advanced chiplet packaging for improved AI and graphics performance.

- July 2024: Samsung announced its Interposer-Cube4 (I-Cube4) technology, a 2.5D packaging solution for high-bandwidth memory (HBM) integration with system-on-chip (SoC) designs.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 5.5 Bn |

| Forecast Revenue (2034) | USD 431.8 Bn |

| CAGR (2025-2034) | 54.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Packaging Type (2.5D Packaging, 3D Packaging, System-in-Package (SiP), Fan-Out Wafer-Level Packaging (FOWLP)), By Testing Type (Pre-Packaging Testing, Post-Packaging Testing), By End-User Industry (Consumer Electronics, Automotive, Telecommunications, Industrial, Healthcare, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Advanced Semiconductor Engineering, Inc. (ASE Group), Amkor Technology Inc., Intel Corporation, TSMC (Taiwan Semiconductor Manufacturing Company), NVIDIA Corporation, Samsung Electronics, Broadcom Inc., Qualcomm Incorporated, Advanced Micro Devices Inc., ASE Group, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |