Quick Navigation

Report Overview

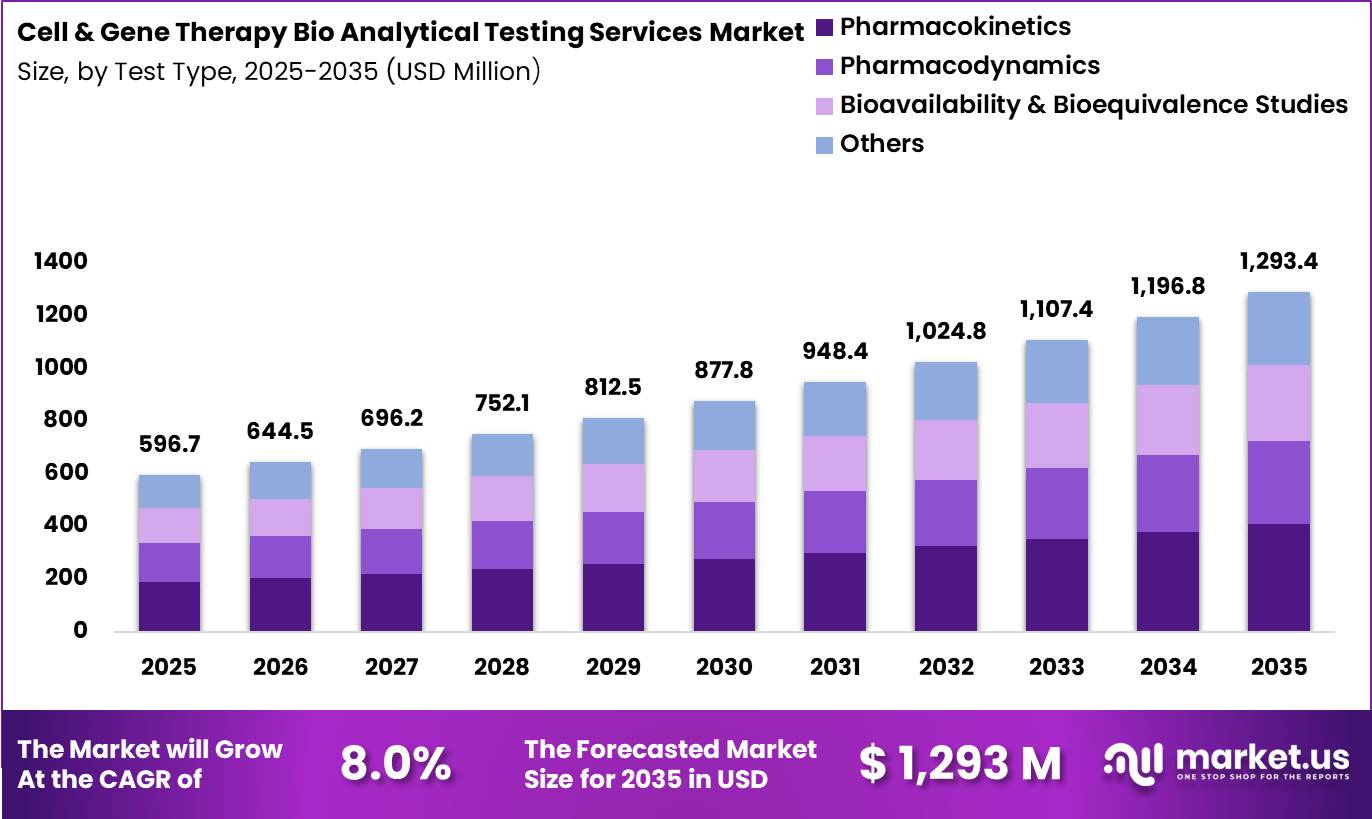

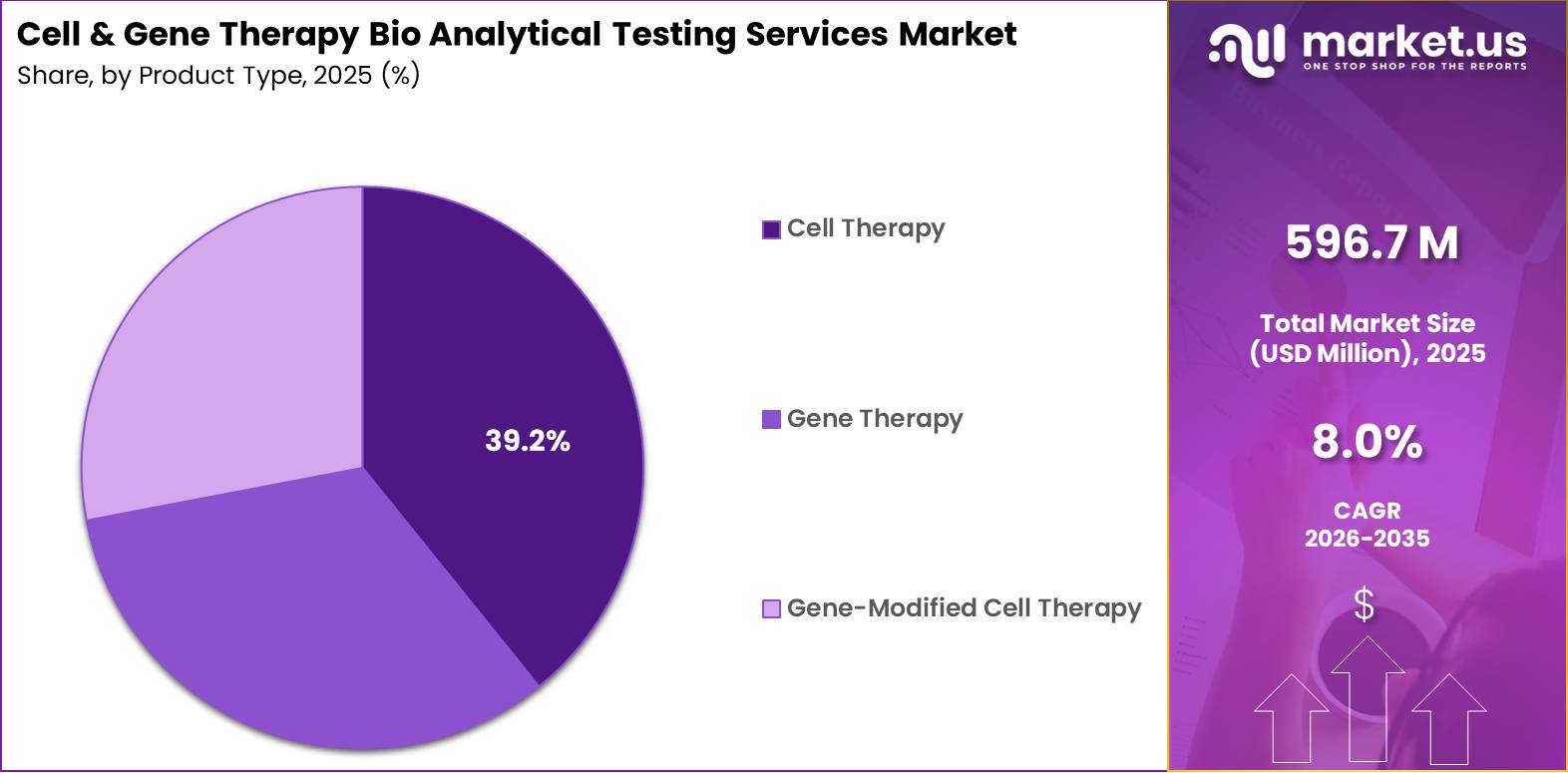

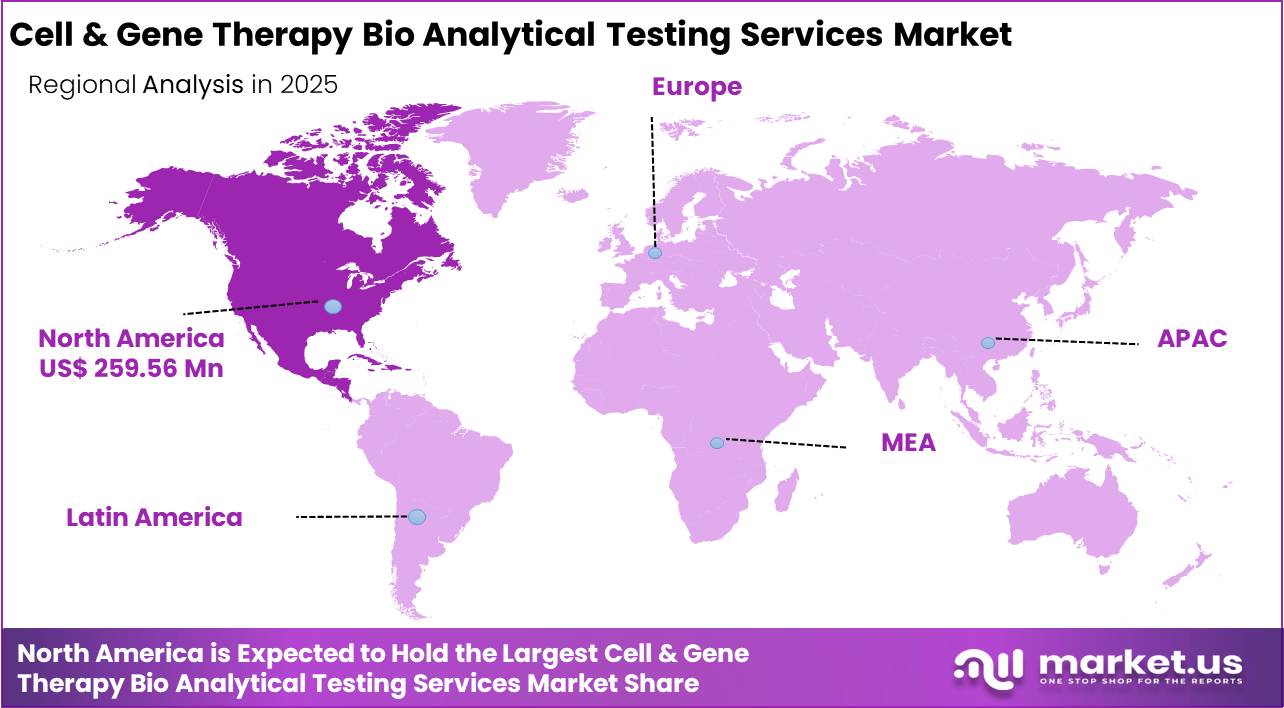

Global Cell & Gene Therapy Bio Analytical Testing Services Market size is expected to be worth around US$ 1,293.4 Million by 2035 from US$ 596.7 Million in 2025, growing at a CAGR of 8.0% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 43.5% share, holding USD 259.56 Million revenue.

Cell & Gene Therapy Bioanalytical Testing Services form a key segment within the field of advanced therapy development, which entails testing services for advanced therapies for the purpose of analyzing, ensuring safety, and evaluating the effectiveness of such products. The demand within the market space is highly dependent on the increasing pipeline of gene therapies, cell therapies, and regenerative medicines that are being developed and tested in various clinical trials.

The industry is regulated, with regulatory guidance on cell and gene therapy products continually growing due to their increasing complexity. This growth has resulted in the U.S. Food and Drug Administration’s continuous efforts toward expanding its regulations to cover gene editing, CAR-T cells, manufacturing, and post-marketing activities. Additionally, the European Medicines Agency oversees the regulation of ATMPs, namely gene therapy products, somatic cell therapies, and tissue engineering products.

Innovation is now directed towards sophisticated bioanalytical techniques in order to characterize vectors, assess potency and biomarkers, detect immunogenicity, and monitor long-term safety. The approved range of cellular and gene therapies by the FDA keeps growing, while new technical guidelines are introduced by regulatory authorities of the United States and Europe.

Key Takeaways

- Market Size: Global Cell & Gene Therapy Bio Analytical Testing Services Market size is expected to be worth around US$ 1,293.4 Million by 2035 from US$ 596.7 Million in 2025.

- Market Share: The market is growing at a CAGR of 8.0% during the forecast period from 2026 to 2035.

- Test Type Analysis: The Pharmacokinetics category was valued at 31.7%, indicating the dominance of assessing vector distribution, transgene expression, persistence, clearance, and dose response for advanced therapy drugs.

- Stage Analysis: Clinical stage is the segment with the highest market share of 63.9% in 2025.

- Product Type Analysis: The Cell Therapy segment will dominate the market, holding 39.2% of the market share in 2025.

- Indication Analysis: Oncology segment dominates the global Cell & Gene Therapy Bioanalytical Testing Services market with its share amounting to 41.5% in 2025

- Regional Analysis: In 2025, North America held a dominant market position, capturing more than a 43.5% share, holding USD 259.56 Million revenue.

Test Type Analysis

Pharmacokinetics Cell & gene therapy bio analytical testing services represents dominant Segment in the Market.

The Pharmacokinetics category was valued at 31.7%, indicating the dominance of assessing vector distribution, transgene expression, persistence, clearance, and dose response for advanced therapy drugs. There is immense importance accorded by regulatory bodies in pharmacokinetic and bio distribution studies while developing a cell and gene-based treatment.

For instance, in 2025 according to U.S. FDA’s guidelines on developing gene therapy, bio distribution tests play an essential role in nonclinical testing of gene therapy products. This indicates that more programs being developed for clinical investigation increase the importance of pharmacokinetic service testing.

Pharmacodynamics is increasingly becoming an essential area of cell and gene therapy services Increasing importance being placed on the demonstration of biological activity, drug effect, and mechanism of action has led to increased use of pharmacodynamics testing.

In 2025, the Food and Drug Administration’s (FDA’s) regulatory guidelines have continued to underscore the need for strong evidence about the safety and effectiveness of such treatments, increasing demand for biomarkers and potency tests. An expanding pipeline of gene editing, CAR-T, and other cellular therapies in government-registered clinical trials further drives demand for pharmacodynamics services.

Stage Analysis

Clinical a significant Stage.

Clinical stage is the segment with the highest market share of 63.9% in 2025 because there will be substantial bioanalytical demands during the clinical stages for evaluating safety, efficacy, immunogenicity, bio distribution, and therapeutic response in patients using the treatments.

As per the U.S. National Institutes of Health (NIH) ClinicalTrials.gov database, in 2025, more than 3,000 active studies on gene therapy have been registered worldwide, indicating considerable clinical development efforts in the industry and increased bioanalytical testing service demand.

The U.S. FDA was developing regulations and guidelines for monitoring cell and gene therapies in clinical development and the post-market phases in 2025, further augmenting bioanalytical test demand at the clinical stage.

Non-clinical stage is the other market segment capturing 36.1% market share in 2025 and exhibiting significant growth due to an increase in investment in safety studies, bio distribution assessment, toxicology studies, and proof of concept by gene therapy product developers.

The U.S. FDA continued to issue nonclinical guidelines and regulations that included the requirement of bio distribution and toxicology evaluation in gene therapies before proceeding to the clinical stage in 2025. Increased gene editing, viral vector, and cell-based therapeutics entering the preclinical stage of development will also boost non-clinical testing services demand.

Product Type Analysis

Cell Therapy is the Most Widely Used Types.

The Cell Therapy segment will dominate the market, holding 39.2% of the market share in 2025. The growth can be attributed to the rising number of approved cell-based therapies and cell therapies under investigation, which need substantial bioanalytical testing for safety, potency, identity, and efficacy.

The development and commercialization of cell therapies necessitate thorough bioanalytical tests such as CAR-T cells and other immune cell therapies. The U.S. Food and Drug Administration (FDA) has approved many cellular therapy products by 2025 and oversees an ever-increasing pipeline of regenerative medicine and cell-based therapies via its Office of Therapeutic Products.

The Gene Therapy segment is the fastest-growing category in the industry owing to the development of new viral vector-based, gene-editing, and genetic medicine platforms. The FDA noted that there was an ongoing increase in gene therapy applications and approvals. Additionally, the National Institute of Health (NIH) maintains an online database for clinical trial research studies, and more gene therapy studies are being listed.

Indication Analysis

Oncology Held a Major Share of the Cell & gene therapy bio analytical testing services Market.

Oncology segment dominates the global Cell & Gene Therapy Bioanalytical Testing Services market with its share amounting to 41.5% in 2025 due to the numerous developments of cellular and gene therapies targeting cancer diseases. Bioanalytical testing helps determine efficacy and efficiency of therapy application, monitor immune response to the therapy, and assess biomarkers in oncology cell and gene therapy.

According to the data provided by NCI, an institute belonging to the NIH, more than 2.04 million new cancer diagnoses are predicted to be made in the USA in 2025. This will ensure the continuous interest in innovative treatment methods, which will stimulate increased clinical activity concerning the development of advanced oncology therapies.

Infectious Diseases segment in 2025 is currently a promising area where companies are increasingly developing gene-based and cell-based approaches to prevent and cure diseases caused by infectious factors. As reported by NIH, continuous government-funded investigations are aimed at advancing technologies to detect and eliminate infectious agents using cell and gene therapies.

Key Market Segments

By Test Type

- Pharmacokinetics

- Pharmacodynamics

- Bioavailability & Bioequivalence Studies

- Others

By Stage

- Clinical

- Non‑Clinical

By Product Type

- Cell Therapy

- Gene Therapy

- Gene-Modified Cell Therapy

By Indication

- Oncology

- Infectious Diseases

- Neurological disorders

- Ophthalmology

- Cardiovascular & Metabolic Diseases

- Rare Genetic Diseases

- Others

Driver

Regulatory intensification in CGT CMC, release, and long term follow up testing

FDA’s current cell and gene therapy guidance set has become materially broader by 2025–2026, covering development planning, product characterization, quality attributes, nonclinical package design, and postapproval safety and efficacy data capture, while also reinforcing the distinction between characterization testing and release testing that must support INDs, BLAs, and certificates of analysis.

FDA’s 2024–2025 CGT Q&A draft guidance stresses that release testing must address safety, purity, and potency, sponsors should test both drug substance and drug product for characterization, and long term follow up can extend up to 15 years depending on modality; in parallel, the 2025 postapproval draft guidance points sponsors toward registries, EHRs, claims data, and auditable compliant real world evidence infrastructure.

EMA has simultaneously advanced a draft guideline for investigational ATMPs covering exploratory and confirmatory trials with explicit quality control and multidisciplinary data expectations, which increases assay validation burden earlier in development.

For bioanalytical testing providers, this converts demand from project based method execution into recurring, compliance linked service lines spanning potency assays, vector copy number, biodistribution, immunogenicity, residual impurity detection, and long duration sample tracking, with the strongest monetization in North America and Europe where filing rigor and inspection readiness are highest.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory intensification in CGT CMC, release, and long-term follow-up testing | +2.4% | North America core, EU core, UK, Japan spill-over | Short term |

| Expanding approval and late-stage pipeline requiring lot release and comparability support | +2.1% | North America core, China, EU, South Korea | Short term |

| Shift toward high-complexity analytical stacks such as ddPCR, flow cytometry, and NGS | +1.9% | U.S., EU, APAC innovation hubs | Medium term |

| Outcomes-based reimbursement and evidence generation increasing post-treatment assay demand | +1.5% | U.S. core, EU selective, GCC and APAC spill-over | Medium term |

| Manufacturing platform reuse and process changes driving comparability and stability programs | +1.3% | U.S. core, EU, China, Japan | Medium term |

| Financing discipline and outsourcing bias favoring specialized testing partners | +1.1% | U.S. core, EU, APAC corridors | Short term |

Challenge

Specialist Talent Shortage In Advanced Bioanalytics

The market faces a persistent talent bottleneck because high value bioanalytical testing requires a narrow labor pool that can combine regulated assay development, cell biology, vector characterization, statistical method validation, and GMP data integrity, while the available workforce pipeline remains materially smaller than demand growth in CGT development and commercialization.

The existence of dedicated ISCT hands on analytical training and specialized workforce courses indicates that standard academic output is still insufficient for immediate deployment, and this translates operationally into 4 to 8 month hiring cycles for experienced assay scientists, wage premiums of roughly 15% to 20% over adjacent biologics analytics roles, and 6 to 12 month ramp periods before independent ownership of complex methods is realistic, creating a modeled 1.2% point CAGR friction and forcing providers to offset scarcity through training academies, automation of repetitive workflows, and concentration of critical functions in talent dense bioclusters.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Potency Assay Variability | -1.6% | North America core; EU ATMP hubs; Japan | Medium term (2-4 years) |

| Specialist Talent Bottleneck | -1.2% | U.S. bioclusters; UK-EU corridors; Singapore | Long term (≥ 4 years) |

| Cryogenic Sample Logistics | -0.9% | APAC export lanes; North America trial networks; EU cross-border flows | Medium term (2-4 years) |

| Regulatory Evidence Creep | -1.4% | U.S. FDA pathway; EU regulatory hubs; global multi-region filings | Medium term (2-4 years) |

| Data Integration Fragmentation | -0.8% | Global CRO networks; multi-site sponsors; CDMO-linked labs | Short term (≤ 2 years) |

| Raw Material Reference Instability | -0.7% | U.S. and EU vector ecosystems; APAC scale-up centers | Medium term (2-4 years) |

Restraints

Assay standardization gaps inflate cost and delay throughput

Assay standardization remains a primary drag because cell and gene therapy testing workflows still require product specific potency, biodistribution, vector copy number, immunogenicity, and identity methods, preventing the service market from achieving the throughput economics seen in monoclonal or small molecule bioanalysis; even with regulators showing more flexibility, FDA still expects lifecycle validation and comparability support.

while the EMA guideline continues to emphasize detailed quality documentation, characterization, specifications, and analytical controls for investigational ATMPs, which means laboratories must often run 3 to 6 major method builds per client program, spend 6 to 12 months on fit for purpose qualification before pivotal readiness, and absorb repeat bridging when sponsors alter vectors, plasmids, cell source, transduction conditions, or release criteria.

In practical terms, this can raise assay development and transfer cost per program by roughly 25% to 40%, depress lab utilization by 10% to 15% because instruments and scientific staff are tied up in bespoke validation cycles rather than revenue dense routine sample analysis, and extend sponsor decision gates by 2 to 3 quarters, ultimately trimming sector growth by about 2.4 percentage points versus a cleaner standard platform adoption curve.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Assay standardization gaps | -2.4% | North America core, EU, Japan, South Korea | Medium term (2-4 years) |

| Regulatory documentation burden | -2.1% | US, EU, UK | Short term (≤ 2 years) |

| Skilled labor scarcity | -1.9% | US biotech hubs, EU clusters, Singapore | Medium term (2-4 years) |

| Vector and reference material bottlenecks | -2.7% | US, EU, APAC corridors | Short term (≤ 2 years) |

| Cryogenic logistics volatility | -1.6% | North America, EU, cross-border APAC | Short term (≤ 2 years) |

| Client funding and program attrition | -3.0% | US-heavy, EU venture markets | Medium term (2-4 years) |

Opportunity

Building Postapproval Long-Term Follow-Up Bioanalytical Platforms

A major white space is the shift from project based preapproval testing into annuity style postapproval bioanalytical monitoring platforms, because the current baseline market still monetizes mostly IND to BLA assay work while FDA guidance for some human gene therapy products contemplates follow up periods of up to 15 years and newer postapproval guidance increasingly points sponsors toward registries, EHR linked evidence generation, and decentralized data capture rather than isolated site visits.

This is an opportunity rather than a current driver because most testing providers have not yet industrialized a recurring software plus services model that bundles immunogenicity, vector persistence, transgene expression, shedding, and longitudinal safety biomarker panels into multi year contracts.

strategically, that can convert a one time 1.5 million to 4 million dollar development testing relationship into a lifecycle account worth 8 million to 20 million dollars over 10 to 15 years, raise revenue visibility by 20% to 30%, and lift EBITDA margins by 300 to 600 basis points through centralized data operations, remote sampling logistics, and lower reacquisition costs.

The upside is strongest in the U.S. first, where the approved product base and late stage pipeline are deepest, but EU and Japan become relevant as more ATMPs move into commercial surveillance and pediatric durability tracking, making this a realistic 2.4 percentage point CAGR uplift for providers that build compliant registry, biostatistics, and bioanalytical interpretation layers before the market standardizes around a few scaled vendors.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Postapproval LTFU platforms | +2.4% | North America core, EU, Japan | Short term (≤ 2 years) |

| Integrated CMC-release analytics | +1.9% | U.S., EU, South Korea | Short term (≤ 2 years) |

| APAC sponsor localization | +2.1% | China, South Korea, Singapore, Australia | Medium term (2-4 years) |

| Solid-tumor assay expansion | +1.6% | U.S., EU, China | Medium term (2-4 years) |

| Companion diagnostics tie-ups | +1.3% | U.S., EU, Japan | Medium term (2-4 years) |

| Platform M&A roll-up | +2.0% | North America, EU | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Geopolitical Realignment and Supply Chain Fragmentation Reshaping Cell & gene therapy bio analytical testing services Manufacturing.

Geopolitical realignment is creating changes within the Cell & Gene Therapy Bioanalytical Testing Services market by impacting biotechnology supply chains, manufacturing trends, and research activities. Countries’ interest in strengthening their biotechnology capabilities has resulted in increased investments in regional bio manufacturing and life sciences capabilities. In 2025, the United States continued implementing the National Biotechnology and Bio Manufacturing Initiative aimed at boosting the nation’s biotechnology capabilities and supply chain resilience.

The initiative created an incentive for making investments into testing services, laboratory capabilities, and quality management systems that are needed to develop and commercialize innovative cell and gene therapies.

In addition, the ongoing diversification of biotechnology supply chains is stimulating demand for specialized testing services from companies involved in biotechnology. Based on information presented in the CBER 2024 Director Report by the FDA, activity within the cell and gene therapy development market continued growing in 2024 and 2025. During the year, there was a rise in the number of therapies being developed and advancing through regulatory approval processes. In order to boost the resilience of the network used for developing cell and gene therapies, the need for regional bioanalytical testing services is rising.

Regional Analysis

North America Held the Largest Share of the Global Cell & gene therapy bio analytical testing services Market.

In 2025, North America had a share of 43.5% in the Cell & Gene Therapy Bioanalytical Testing Services market. This high share is driven by the large number of cell and gene therapies under development, which require analysis and evaluation at all preclinical and clinical trial stages.

According to the U.S. FDA CBER 2024 Director Report, FDA supervised the largest number of cell and gene therapy programs and approved new products among cell and gene therapy drugs in 2024-2025. Besides, the ClinicalTrials.gov website run by the U.S. National Institutes of Health (NIH) recorded more than 5,000 gene therapy-related clinical trials worldwide in 2025, which is indicative of a significant number of research projects necessitating analytical testing, biomarker profiling, and other testing services.

In 2025, Asia Pacific region is expected to be a rapidly growing market owing to rising biotechnology research capabilities and an increasing number of cell and gene therapies under clinical development in the region. The increasing government initiatives to support innovations in biotechnologies, regenerative medicine, and advanced therapies are expected to increase the demand for bioanalytical testing services in the region.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Cell & Gene Therapy Bioanalytical Testing Services Providers’ key objective remains enhancing their capabilities through analytical strength, regulatory experience, and technology advantage. The adoption of next-generation sequencing, digital PCR, flow cytometry, cell-based assays for assessing potency, and biomarker testing technologies that are vital in the production of advanced cell and gene therapies remain a key priority for these companies. In addition, there have been developments by the service providers aimed at improving the provision of vector characterization, bio distribution, immunogenicity testing, and long-term safety analysis services.

Laboratory expansion, process improvement through automation, and development of data management systems have been critical aspects of service provider operations. Through strategic alliances with biotechnology and pharmaceutical companies, CDMOs, and research institutes, service providers aim to diversify their service portfolios and secure pipeline projects.

Other areas that have received attention from providers include quality assurance, regulatory services, and advanced analytical experience. In terms of geographical diversification, the expansion of laboratory networks, digital analytical solutions, and standardized testing methods have been significant drivers of growth.

Major Key Players

- BioAgilytix Labs

- KCAS Bioanalytical Services

- IQVIA, Inc.

- Laboratory Corporation of America Holdings

- Pharmaceutical Product Development, Inc. (Thermo Fisher Scientific Inc.)

- Prolytix

- Pharmaron

- Charles River Laboratories

- Syneos Health

- SGS SA

- Intertek Group Plc

Recent Development

- In March 2025, Charles River Laboratories announced the inaugural cohort of its Advanced Therapy Incubator Program. The initiative provides emerging biotechnology developers with access to scientific, regulatory, quality, development, and manufacturing expertise, supporting the advancement of cell and gene therapy programs. The development reflects continued demand for integrated service capabilities across advanced therapy development.

- In October 2024, IQVIA Laboratories expanded and relocated its Central Laboratories facility in Valencia, California. The facility expansion supports IQVIA’s broader clinical laboratory network and its ability to provide central laboratory, biomarker, genomics, flow cytometry, and bioanalytical services for clinical research programs.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 596.7 Million |

| Forecast Revenue (2035) | US$ 1,293.4 Million |

| CAGR (2026-2035) | 8.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Test Type (Pharmacokinetics, Pharmacodynamics, Bioavailability & Bioequivalence Studies, Others), By Stage (Clinical, Non‑Clinical), By Product Type (Gene Therapy, Gene-Modified Cell Therapy, Cell Therapy), By Indication (Oncology, Infectious Diseases, Neurological disorders, Ophthalmology , Cardiovascular & Metabolic Diseases, Rare Genetic Diseases, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | BioAgilytix Labs, KCAS Bioanalytical Services, IQVIA, Inc., Laboratory Corporation of America Holdings, Pharmaceutical Product Development, Inc. (Thermo Fisher Scientific Inc.), Prolytix, Pharmaron, Charles River Laboratories, Syneos Health, SGS SA, Intertek Group Plc |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |