Global CDN Security Market Size, Share and Analysis Report By Organization Size (Small and Medium-Sized Businesses (SMBs), Large Enterprises), By Security Type (DDoS Protection, Web Application Firewall (WAF), Bot Mitigation and Screen-Scraping Protection, Data Security and Content Integrity, Others), By End-user Industry (Media and Entertainment, Retail and E-commerce, BFSI, IT and Telecom, Healthcare and Life Sciences, Government and Public Sector, Education, Others), By Deployment Mode (Cloud, On-Premise), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 178697

- Number of Pages: 205

- Format:

-

keyboard_arrow_up

Quick Navigation

- CDN Security Market size

- Top Market Takeaways

- Report Overview

- Drivers Impact Analysis

- Restraint Impact Analysis

- By Organization Size: Large Enterprises

- By Security Type: DDoS Protection

- By End-User Industry: Media and Entertainment

- By Deployment Mode: On-Premise

- Regional Overview: North America

- Emerging Trends Analysis

- Opportunity Analysis

- Challenge Analysis

- Key Market Segments

- Investor Type Impact Matrix

- Technology Enablement Analysis

- Competitive Analysis

- Recent Developments

- Report Scope

CDN Security Market size

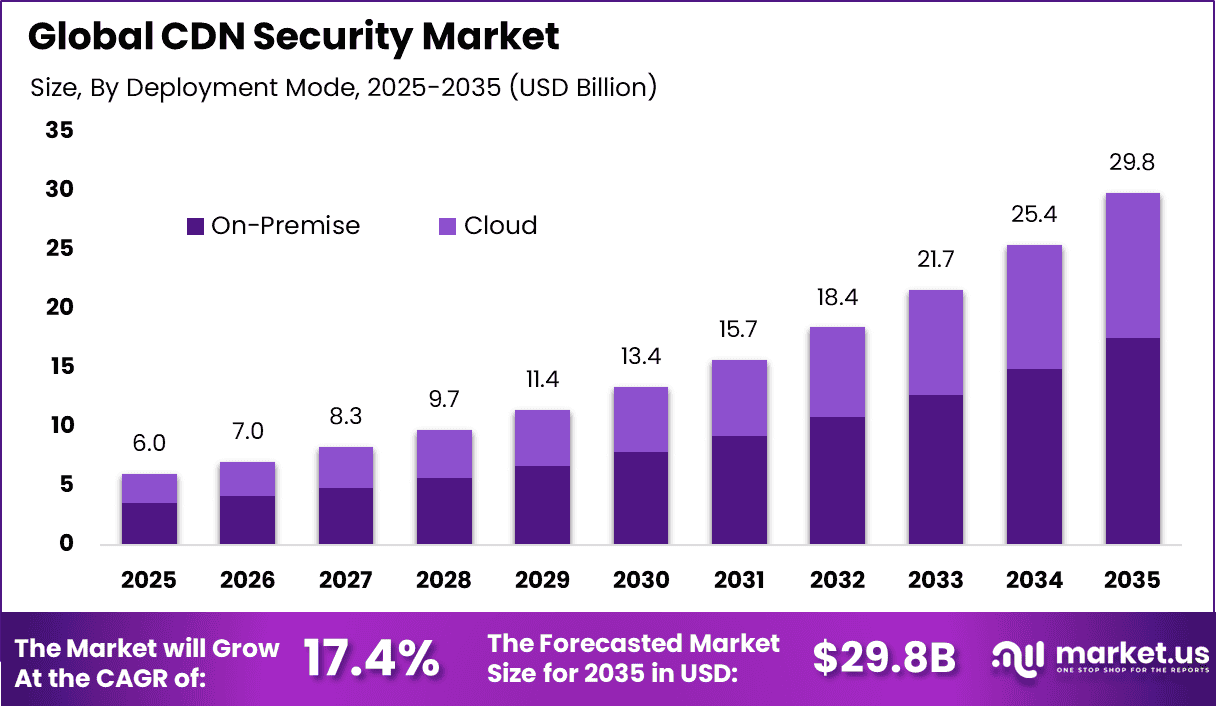

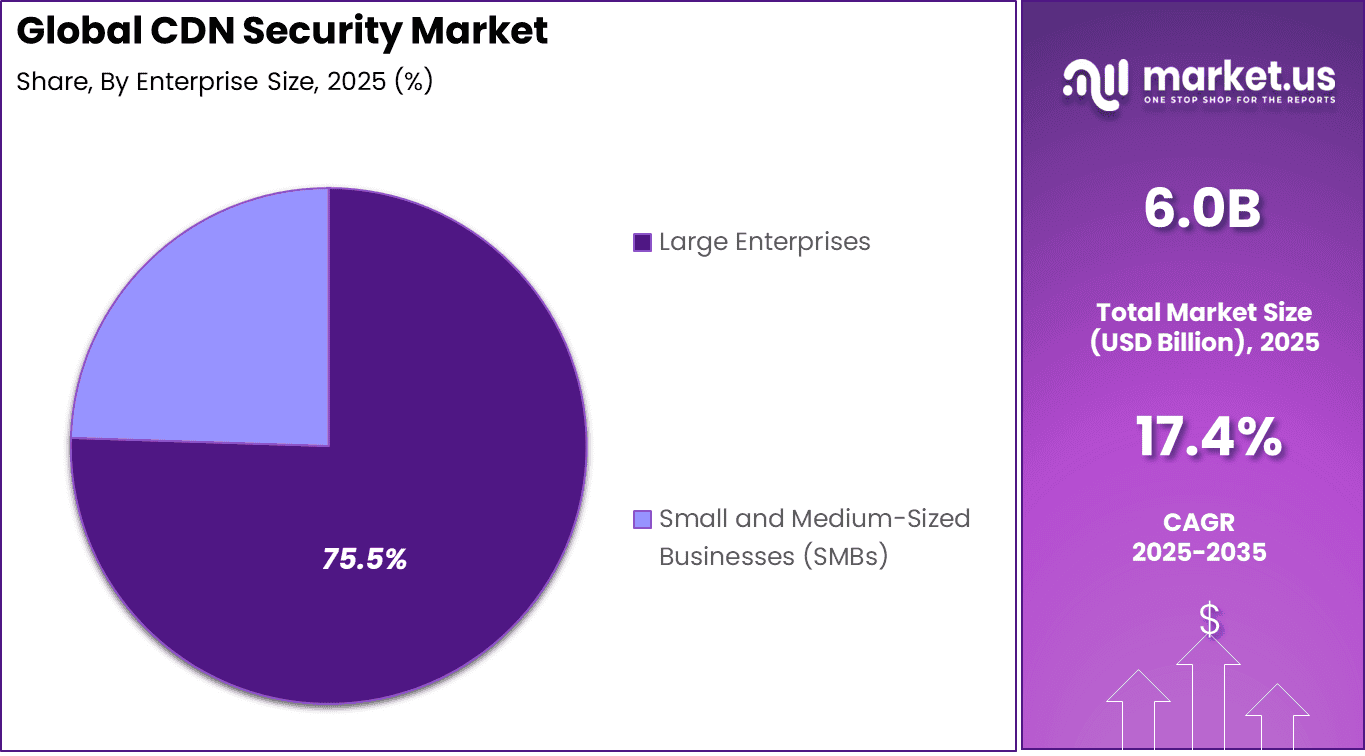

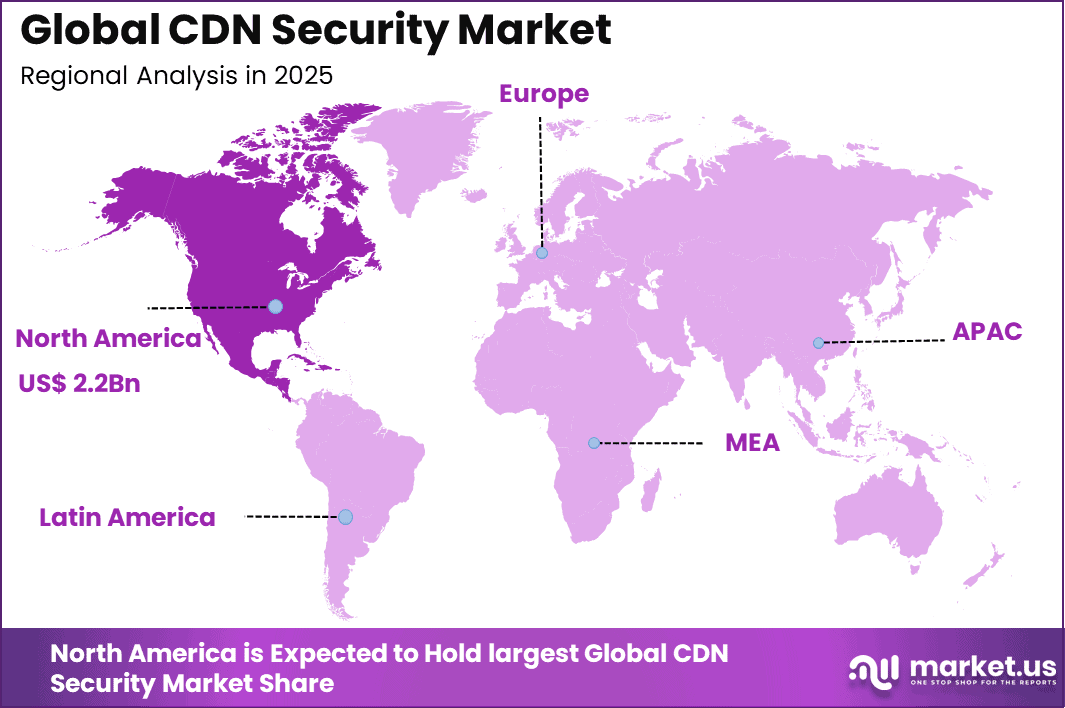

The Global CDN Security Market size is expected to be worth around USD 29.8 Billion By 2035, from USD 6.0 billion in 2025, growing at a CAGR of 17.4% during the forecast period from 2026 to 2035. North America held a dominant Market position, capturing more than a 37.8% share, holding USD 2.2 Billion revenue.

Top Market Takeaways

- By Organization Size, Large Enterprises accounted for 75.5% of the market share, reflecting higher cybersecurity budgets, complex digital infrastructures, and strong demand for advanced threat mitigation solutions.

- By Security Type, DDoS Protection held 43.7% of the market, driven by the increasing frequency and scale of distributed denial of service attacks targeting high traffic platforms and digital services.

- By End-user Industry, Media and Entertainment captured 30.0% of the total share, supported by rising video streaming consumption, live content delivery, and the need to secure high bandwidth digital assets.

- By Deployment Mode, On-Premise solutions led with 58.7%, indicating continued preference for direct control over security architecture, data privacy, and compliance management.

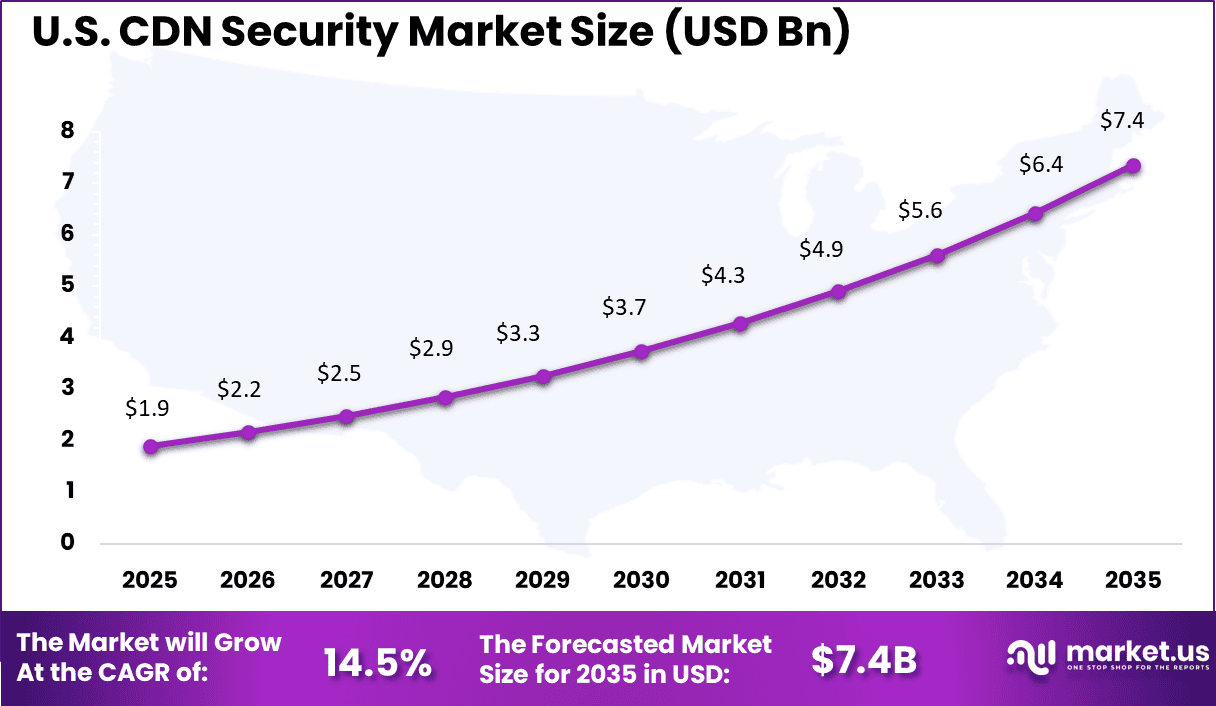

- Regionally, North America held 37.8% of the global market share, with the U.S. market valued at USD 1.93 billion in 2025 and expanding at a CAGR of 14.5%, supported by strong cloud adoption, digital media expansion, and advanced cybersecurity investments.

Report Overview

The CDN market covers products and services that deliver web and application content from a distributed network of servers placed closer to end users. A CDN is typically used to cache and serve static assets such as images, video segments, software downloads, and website files, and it can also accelerate dynamic content through optimized routing and edge capabilities. Content is delivered from nearby points of presence to reduce distance, improve responsiveness, and limit load on the origin infrastructure.

Top driving factors are largely tied to the scale and complexity of internet usage and the need for consistent performance. Global connectivity has expanded the addressable base for digital services, with the number of people using the internet estimated at about 5.3 billion in 2023, or roughly 65% of the world’s population.

At the same time, traffic patterns are dominated by high bandwidth applications, with video representing the largest downstream category across regions, commonly in the range of 41% to 48% of downstream volume. These conditions can increase the value of distributed delivery, caching, and edge placement because peak demand is spread globally and users expect fast access regardless of location.

Drivers Impact Analysis

Driver Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Rising Frequency of DDoS and Application Layer Attacks +3.2% North America, Europe Immediate Growth in Cloud Native and Multi Cloud Deployments +2.7% North America, Asia Pacific Short to Medium Term Increasing Adoption of Edge Computing Architectures +2.1% North America, Europe Medium Term Expansion of E Commerce and Digital Media Platforms +1.6% Global Immediate to Medium Term Regulatory Emphasis on Data Protection Compliance +1.1% Europe, North America Medium Term Restraint Impact Analysis

Restraint Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline High Deployment and Subscription Costs -2.4% Emerging Markets Short Term Complexity in Integrating Legacy Infrastructure -1.8% Global Medium Term Shortage of Skilled Cybersecurity Professionals -1.3% North America, Asia Pacific Medium Term False Positives and Traffic Filtering Errors -0.9% Global Ongoing Vendor Lock In Concerns -0.6% North America, Europe Medium Term By Organization Size: Large Enterprises

Large enterprises account for 75.5% of the CDN security market. These organizations operate high-traffic digital platforms that require continuous availability and performance protection. With increasing online transactions and streaming activities, enterprises face elevated cyber risks.

CDN security solutions help mitigate threats that could disrupt service delivery or compromise sensitive data. This drives strong adoption among large-scale digital operators. Enterprise networks often span multiple regions and cloud environments.

Centralized CDN security platforms provide visibility and control across distributed infrastructures. Advanced analytics and automated threat mitigation reduce downtime and financial exposure. Integration with enterprise security frameworks further enhances resilience. The scale of operations explains the dominant share of large enterprises in this market.

By Security Type: DDoS Protection

DDoS protection holds 43.7% of the CDN security segment. Distributed denial-of-service attacks remain one of the most common threats targeting online platforms. These attacks attempt to overwhelm network resources and disrupt service availability. CDN-based DDoS mitigation absorbs and filters malicious traffic before it reaches origin servers. This ensures stable user access even during high-volume attack attempts.

Modern DDoS protection systems use real-time traffic monitoring and behavior analysis. Automated filtering mechanisms distinguish legitimate users from malicious requests. Rapid detection and mitigation minimize service interruptions and reputational damage. As digital dependency grows across industries, demand for DDoS protection continues to strengthen. This security layer remains a critical component of CDN defense strategies.

By End-User Industry: Media and Entertainment

The Media and Entertainment sector accounts for 30.0% of the CDN security market. Streaming platforms and digital media providers rely heavily on content delivery networks to distribute high-volume video and audio content. Ensuring uninterrupted streaming and secure content access is essential for user satisfaction. CDN security helps prevent piracy, service disruption, and unauthorized access. This strengthens operational reliability across digital media platforms.

High traffic volumes during live events increase exposure to cyber threats. CDN security solutions help manage traffic spikes while filtering malicious activity. Secure content delivery also protects intellectual property rights. As digital media consumption continues to expand, security investment within this sector remains strong. The industry’s dependence on continuous online availability explains its significant share.

By Deployment Mode: On-Premise

On-premise deployment represents 58.7% of the CDN security market. Organizations with strict data control requirements often prefer localized security management. On-premise deployment allows direct oversight of configurations, policies, and monitoring systems. This is particularly important for enterprises handling sensitive customer or financial information. Internal control strengthens compliance and operational assurance.

Certain industries operate under regulatory frameworks that limit cloud-based security deployments. On-premise systems provide customized integration with existing IT infrastructure. They also reduce reliance on third-party cloud providers for critical security functions. Direct hardware-level control enhances response speed in some environments. These factors support the continued relevance of on-premise deployment models.

Regional Overview: North America

North America holds 37.8% of the global CDN security market. The region demonstrates strong digital infrastructure and high online content consumption. Enterprises invest heavily in cybersecurity to protect digital services and customer data. Growth in e-commerce, streaming, and cloud services continues to drive demand. This supports consistent market expansion across the region.

The United States leads regional activity with a market value of USD 1.93 Bn and a CAGR of 14.5%. Organizations prioritize advanced threat mitigation and network resilience strategies. The presence of large digital enterprises further accelerates adoption. Continuous innovation in content delivery and cybersecurity technologies strengthens regional leadership. North America remains a key hub for CDN security deployment and advancement.

Emerging Trends Analysis

The CDN security market is witnessing increased integration of advanced threat intelligence and real time traffic analysis within content delivery infrastructure. Security capabilities such as bot management, API protection, and web application firewalls are being embedded directly into CDN platforms. This integration enables enterprises to secure digital assets at the edge of the network. As online traffic volumes continue to grow, edge based security models are becoming more critical.

Another emerging trend is the expansion of zero trust and secure access service edge architectures within CDN environments. Enterprises are shifting toward distributed security frameworks that combine network delivery with identity based access control. This approach enhances protection against distributed denial of service attacks and application layer threats. Edge security innovation is therefore shaping the evolution of CDN security solutions.

Opportunity Analysis

A major opportunity lies in the expansion of edge computing and 5G driven applications. As real time services such as online gaming, video streaming, and IoT platforms grow, demand for low latency and secure content delivery increases. CDN providers that combine performance optimization with advanced security controls can address this demand effectively. Edge based protection is expected to create new service differentiation.

Growth in emerging digital economies also presents significant opportunity. Expanding internet penetration and mobile commerce adoption are increasing online traffic volumes in developing regions. Businesses entering these markets require scalable and secure content distribution networks. Vendors that offer flexible pricing and localized support can capitalize on this expansion.

Challenge Analysis

A major challenge in the CDN security market is managing increasingly sophisticated attack techniques. Cybercriminals are leveraging automated tools and AI driven tactics to bypass traditional filtering mechanisms. Constant updates and threat intelligence integration are required to maintain effective defense. Failure to adapt quickly can expose enterprises to service disruption.

Another challenge involves maintaining performance while implementing strong security controls. Excessive filtering or misconfigured policies can lead to latency issues or false positives that affect user experience. Balancing security with speed and reliability is critical for customer retention. Achieving this balance requires continuous optimization and monitoring.

Key Market Segments

By Organization Size

- Small and Medium-Sized Businesses (SMBs)

- Large Enterprises

By Security Type

- DDoS Protection

- Web Application Firewall (WAF)

- Bot Mitigation and Screen-Scraping Protection

- Data Security and Content Integrity

- Others

By End-user Industry

- Media and Entertainment

- Retail and E-commerce

- BFSI

- IT and Telecom

- Healthcare and Life Sciences

- Government and Public Sector

- Education

- Others

By Deployment Mode

- On-Premise

- Cloud

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Investor Type Impact Matrix

Investor Type Impact on CAGR Forecast (~%) Geographic Relevance Investment Horizon Cybersecurity Technology Providers +3.0% North America Long Term Cloud Infrastructure Companies +2.4% Global Medium to Long Term Private Equity in Security Platforms +1.7% North America, Europe Medium Term Venture Capital in Edge Security Startups +1.2% North America, Asia Pacific Medium Term Telecom and Network Operators +0.8% Asia Pacific, Europe Long Term Technology Enablement Analysis

Technology Enabler Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline AI Driven Threat Detection and Mitigation +3.5% Global Immediate Web Application and API Protection Solutions +2.8% North America, Europe Short to Medium Term Zero Trust Network Access Integration +2.0% North America Medium Term Secure Edge Computing Platforms +1.4% Asia Pacific, Europe Medium Term Automated Bot Management Systems +0.9% Global Immediate Competitive Analysis

Global content delivery and edge security leaders such as Akamai Technologies Inc., Cloudflare Inc., and Fastly Inc. dominate the CDN security market. These vendors provide integrated DDoS protection, web application firewalls, and bot mitigation at the edge. Edgio Inc. and CDNetworks Inc. strengthen global delivery footprints. Demand is driven by rising application-layer attacks and growing online traffic volumes.

Cloud platform providers such as Amazon Web Services Inc., Google LLC, Microsoft Corp., and Alibaba Cloud embed CDN security within broader cloud ecosystems. These vendors benefit from scalable infrastructure and integrated security controls. Adoption is strong among enterprises migrating workloads to public cloud environments.

Specialized security providers such as Imperva Inc., Radware Ltd., F5 Inc., StackPath LLC, G-Core Labs S.A., Corero Network Security plc, Nexusguard Ltd., Neustar Security Services, NETSCOUT Systems, and Verizon Media Platform enhance advanced threat mitigation capabilities. Other vendors expand innovation and regional reach, supporting continued growth in CDN security solutions globally.

Competitive Capability Matrix

Competitive Capability Market Influence Level Geographic Strength Strategic Impact Timeline Global Edge Network Footprint Very High North America, Europe Long Term Integrated CDN and Security Stack High Global Medium Term Real Time Threat Intelligence Feeds High North America Immediate Scalable Multi Cloud Compatibility Moderate to High Asia Pacific Medium Term Customer Support and SLA Reliability High Global Ongoing Top Key Players in the Market

- Akamai Technologies Inc.

- Amazon Web Services Inc. (CloudFront)

- Cloudflare Inc.

- Google LLC (Cloud CDN)

- Microsoft Corp. (Azure Front Door)

- Imperva Inc.

- Fastly Inc.

- Edgio Inc. (Limelight Networks)

- Verizon Media Platform

- Radware Ltd.

- F5 Inc.

- StackPath LLC

- G-Core Labs S.A.

- Alibaba Cloud (Alibaba Group)

- Corero Network Security plc

- Nexusguard Ltd.

- CDNetworks Inc.

- Neustar Security Services

- Akamai (Prolexic)

- NETSCOUT Systems (Arbor)

- Others

Recent Developments

- Cloudflare partnered with Mastercard in February 2026 to fuse Recorded Future intel into its platform, spotting rogue assets before attacks land.

- In May 2025, Cinema8 introduced an intelligent video hosting and CDN solution that moves beyond basic content delivery. The offering is positioned to make video more interactive and measurable, supporting a smarter, data-driven viewing experience rather than passive streaming.

- Microsoft rolled out smarter WAF and Bot Manager SKUs in June 2025, powered by its threat intel for proactive blocks.

Report Scope

Report Features Description Market Value (2025) USD 6.0 Bn Forecast Revenue (2035) USD 29.8 Bn CAGR(2026-2035) 17.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Organization Size (Small and Medium-Sized Businesses (SMBs), Large Enterprises), By Security Type (DDoS Protection, Web Application Firewall (WAF), Bot Mitigation and Screen-Scraping Protection, Data Security and Content Integrity, Others), By End-user Industry (Media and Entertainment, Retail and E-commerce, BFSI, IT and Telecom, Healthcare and Life Sciences, Government and Public Sector, Education, Others), By Deployment Mode (Cloud, On-Premise) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Akamai Technologies Inc., Amazon Web Services Inc. (CloudFront), Cloudflare Inc., Google LLC (Cloud CDN), Microsoft Corp. (Azure Front Door), Imperva Inc., Fastly Inc., Edgio Inc. (Limelight Networks), Verizon Media Platform, Radware Ltd., F5 Inc., StackPath LLC, G-Core Labs S.A., Alibaba Cloud (Alibaba Group), Corero Network Security plc, Nexusguard Ltd., CDNetworks Inc., Neustar Security Services, Akamai (Prolexic), NETSCOUT Systems (Arbor), Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Akamai Technologies Inc.

- Amazon Web Services Inc. (CloudFront)

- Cloudflare Inc.

- Google LLC (Cloud CDN)

- Microsoft Corp. (Azure Front Door)

- Imperva Inc.

- Fastly Inc.

- Edgio Inc. (Limelight Networks)

- Verizon Media Platform

- Radware Ltd.

- F5 Inc.

- StackPath LLC

- G-Core Labs S.A.

- Alibaba Cloud (Alibaba Group)

- Corero Network Security plc

- Nexusguard Ltd.

- CDNetworks Inc.

- Neustar Security Services

- Akamai (Prolexic)

- NETSCOUT Systems (Arbor)

- Others

Our Clients

- 178697

- Feb. 2026