Quick Navigation

Report Overview

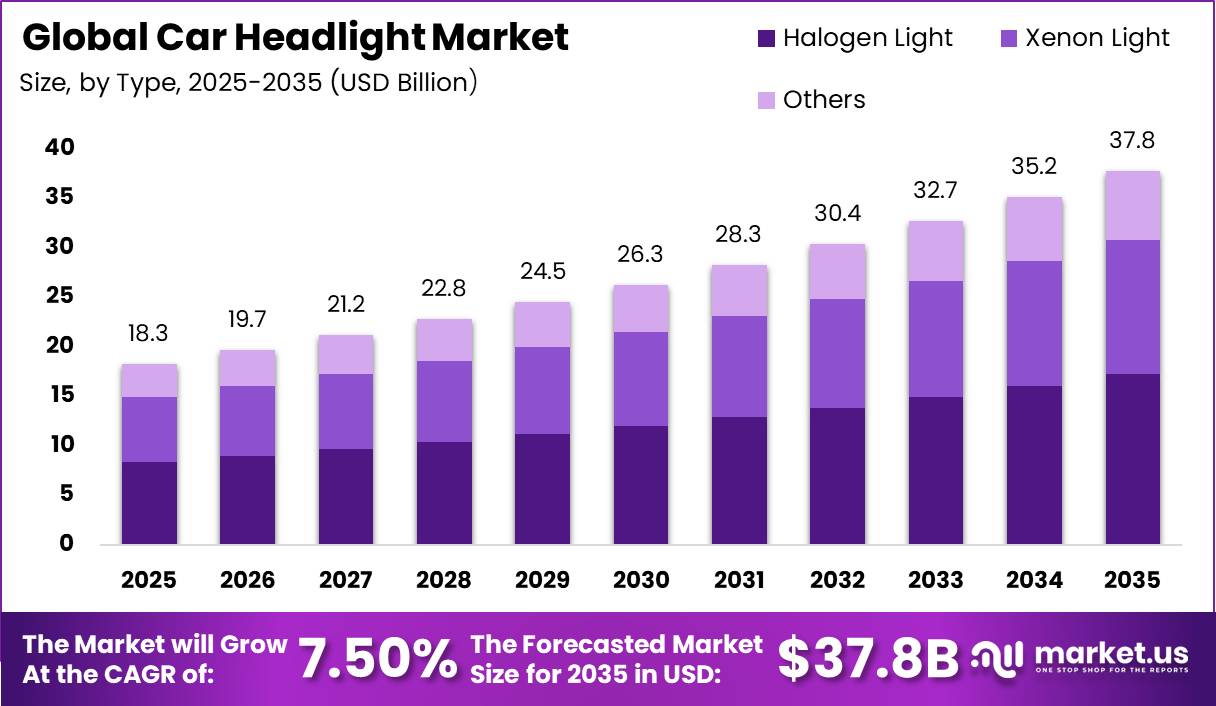

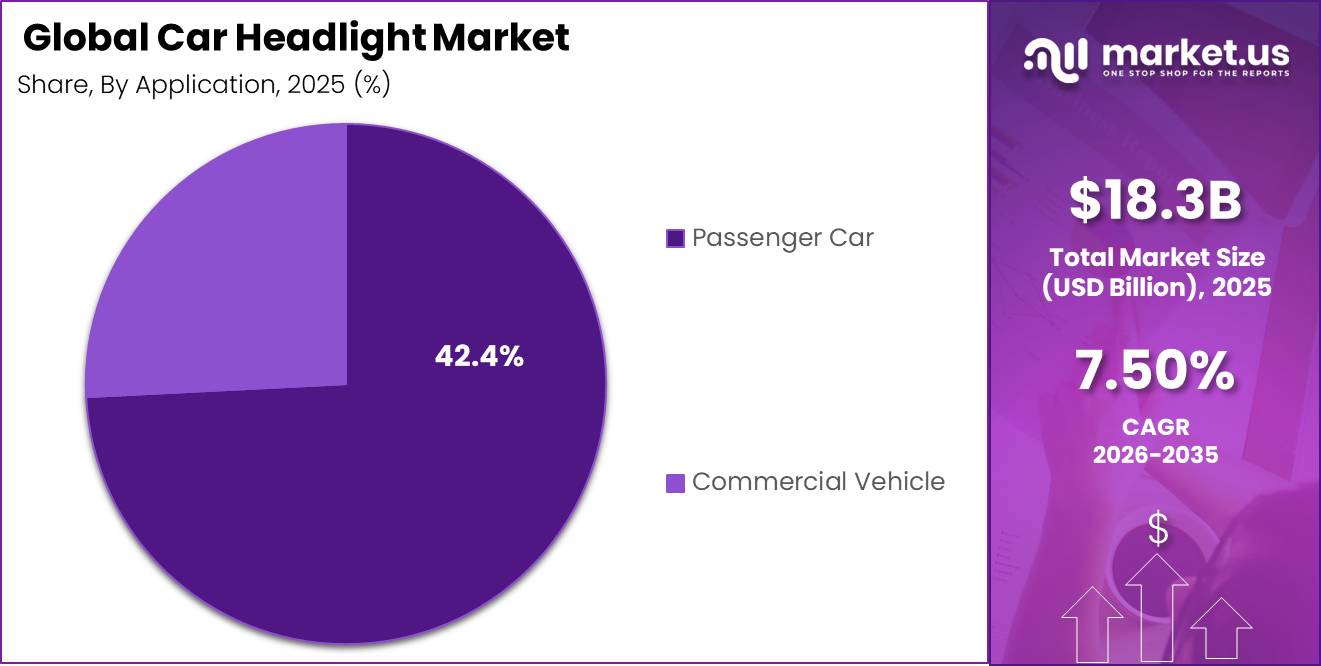

Global Car Headlight Market size is expected to be worth around USD 37.8 Billion by 2035 from USD 18.3 Billion in 2025, growing at a CAGR of 7.50% during the forecast period 2026 to 2035.

The car headlight market covers all forward-facing vehicle lighting assemblies supplied to OEM production lines and aftermarket channels globally. This includes halogen, xenon, and advanced LED-based headlamp systems across passenger cars and commercial vehicles. The market spans full headlamp modules, adaptive beam units, and integrated lighting systems with ADAS and V2X connectivity functions.

Key Takeaways

- Market value in 2025 stands at USD 18.3 Billion, forecast to reach USD 37.8 Billion by 2035.

- The market grows at a CAGR of 7.50% from 2026 to 2035.

- Halogen Light dominates the By Type segment with a 45.60% share in 2025.

- Passenger Car dominates the By Application segment with a 74.20% share in 2025.

- Asia-Pacific leads all regions with a 42.8% market share, valued at USD 7.83 Billion in 2025.

The European Union mandated daytime running lamps on all new passenger cars and small delivery vehicles since 2011, while Canada established mandatory DRL fitment on all new vehicles as early as 1990. According to Carifex, these regulatory timelines confirm that headlight legislation is a persistent market shaper across major automotive jurisdictions. This regulatory pressure sustains long-term OEM procurement volumes for compliant headlamp assemblies across all vehicle classes.

Based on IIHS data, the share of vehicles rated good in headlight performance rose from 4% in 2016 to 51% among 2025 model-year vehicles. This improvement reflects a structural shift in OEM headlamp specification toward higher-quality LED and adaptive systems. Investors targeting headlamp suppliers who serve OEM upgrade programs stand to benefit as this quality-rating trajectory continues to reward premium lighting content in new vehicle programs.

IIHS data shows headlight glare is implicated in only 0.1% to 0.2% of nighttime crashes across multi-state datasets. This finding separates consumer perception from crash risk reality. This creates a regulatory communication gap that advanced lighting suppliers can address by aligning product narratives with safety-rating systems rather than glare complaint volumes.

Type Analysis

Halogen Light dominates with 45.60% due to low cost and broad vehicle compatibility.

In 2025, Halogen Light held a dominant market position in the By Type segment of the Car Headlight Market, with a 45.60% share. AAA data shows halogen headlights remain in over 80% of vehicles currently on the road, reinforcing their entrenched position in the installed base. This scale creates consistent aftermarket replacement demand even as OEM programs transition toward LED technologies.

Xenon Light holds a 36% share in 2025, anchored by its adoption in mid-premium vehicle segments where HID performance justifies cost. HID and LED systems illuminate dark roadways 25% further than halogen counterparts, giving xenon a sustained advantage in performance-focused applications. However, xenon’s position faces erosion as LED systems achieve price parity in the OEM supply chain.

Others, representing 18.4% of the market, includes advanced LED matrix, laser, and adaptive beam headlamp systems. European adaptive driving beam headlights increase roadway lighting by up to 86% compared to US low-beam headlights, according to AAA. This performance gap establishes the commercial case for ADB and laser system adoption in markets where regulation permits. In January 2025, FORVIA HELLA developed highly customized LED Matrix headlamps for the new smart #5 in China, confirming that series-production ADB technology is already entering volume OEM programs in Asia-Pacific.

Application Analysis

Passenger Car dominates with 74.20% due to higher global production volumes and DRL mandates.

In 2025, Passenger Car held a dominant market position in the By Application segment of the Car Headlight Market, with a 74.20% share. AAA data confirms that 64% of Americans do not regularly use their high beams, and most low beams are insufficient at speeds above 39 mph. This creates structural demand for adaptive and ADB systems that automatically optimize beam output, directly lifting the addressable content value per passenger vehicle.

Commercial Vehicle accounts for 25.80% of the market, driven by fleet safety requirements and regulatory pressure on heavy transport lighting compliance. Commercial operators face stricter downtime penalties, making durable and long-life LED lamp systems the preferred procurement choice. Suppliers offering integrated front and rear lighting solutions with unified light signatures hold a structural advantage in this segment.

Key Market Segments

By Type

- Halogen Light

- Xenon Light

- Others

By Application

- Passenger Car

- Commercial Vehicle

Market Dynamics

Market Opportunity Analysis - Underexploited segments and regions offer structured entry points for headlamp suppliers

The aftermarket retrofit segment represents a structurally underexploited channel. Halogen headlights remain in over 80% of vehicles on the road globally, yet aftermarket halogen-to-LED conversion kit penetration remains low in emerging automotive markets. Suppliers who establish retrofit distribution networks in India, ASEAN, Latin America, and Middle East and Africa can capture recurring replacement revenue without competing directly for OEM supply contracts.

The two-wheeler segment in India and ASEAN markets presents a distinct headlamp growth channel not yet fully addressed by major headlamp suppliers. Rapid LED headlight penetration in this segment is a stated opportunity in the data, driven by cost reduction in LED components and tightening road safety norms. This creates an accessible entry point for suppliers capable of adapting automotive-grade LED designs to lower-cost, higher-volume two-wheeler platforms.

Commercial vehicle fleet operators represent an underserved segment relative to their procurement scale. The data confirms commercial fleet safety compliance is a primary purchase driver, yet commercial vehicles account for only 25.80% of the current market versus 74.20% for passenger cars. Suppliers offering bundled front-and-rear lighting systems with unified safety compliance documentation hold a differentiated position in this segment with limited current competition at scale.

The V2X-enabled smart headlight category is a long-horizon channel supported by autonomous vehicle pedestrian signaling and road communication use cases. This segment sits at the intersection of lighting hardware and software-defined vehicle systems, areas where established headlamp suppliers have existing engineering infrastructure. Early movers who integrate V2X communication functions into headlamp modules position themselves as platform providers rather than commodity component suppliers.

Technology and Innovation Landscape - Pixel-level beam control and software-defined lighting reshape headlamp product value

Pixel-level matrix LED architectures enable dynamic, high-resolution beam shaping at the module level, replacing fixed-beam optics with programmable illumination patterns. HID and LED headlight systems already illuminate dark roadways 25% further than halogen counterparts, and matrix LED extends this advantage through real-time beam adaptation. Suppliers with proprietary pixel control platforms hold a defensible IP position as OEMs standardize on high-definition lighting architectures.

Digital micromirror (DLP) projection headlights enable advanced road illumination and symbol projection directly from the headlamp unit. This technology converts the headlamp from a passive safety component into an active road-communication tool. As autonomous and semi-autonomous vehicle programs advance, DLP-capable headlamps become a platform for pedestrian signaling and infrastructure interaction, expanding the addressable revenue per vehicle unit.

Software-defined lighting systems allow headlight behavior customization via vehicle control software, decoupling performance features from fixed hardware specifications. This shift enables OEMs to monetize lighting upgrades through over-the-air software subscriptions rather than hardware replacement cycles. Suppliers who embed software-configurable lighting control into their modules create recurring revenue streams that extend beyond the initial OEM sale.

Only 20% of Americans have performed headlight lens restoration despite the procedure doubling maximum light intensity and reducing glare-producing light scatter by up to 60%, according to AAA. This low adoption rate signals a gap between available restoration technology and consumer awareness. Suppliers and distributors who address this channel through retail and fleet service programs can generate measurable aftermarket revenue from existing vehicle populations without introducing new hardware.

Drivers

The strongest 2026 demand driver is the upgrade from halogen and basic LED systems toward projector LED, matrix LED, and adaptive beam architectures. This transition raises content value per vehicle even when total vehicle output grows only moderately. UNECE Regulation No. 149 covers headlamps, adaptive front-lighting systems, and related road-illumination devices, supporting wider engineering standardization for higher-value lighting packages across passenger and commercial vehicle platforms.

The revenue effect is measurable because adaptive LED systems require more expensive optics, drivers, control units, thermal components, and software calibration than conventional reflector lamps. Suppliers can grow faster than vehicle production through richer product mix rather than pure unit volume. This means headlamp content-per-vehicle value is the more relevant growth metric for investors than unit shipment volumes alone.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adaptive LED Upgrade Cycle | +2.2% | EU core, Japan, South Korea, North America premium segment, China Tier-1 clusters | Short term (≤ 2 years) |

| UNECE-Compliant Smart Lighting Adoption | +1.8% | EU core, UK, Japan, South Korea, export-oriented APAC platforms | Medium term (2-4 years) |

| EV-Led Rise in Electronic Lamp Content | +1.7% | China core, EU, North America | Medium term (2-4 years) |

| Premium SUV and Crossover Mix | +1.3% | North America core, China metro markets, EU premium segment, GCC | Short term (≤ 2 years) |

| Supply Chain Stabilization for Advanced Modules | +1.0% | Global OEM programs, especially Europe, China, US, Mexico | Short term (≤ 2 years) |

| Aging Vehicle Fleet and Replacement Complexity | +0.8% | North America, Europe, Latin America spill-over | Long term (≥ 4 years) |

Restraints

The tariff regime is a measurable restraint. The White House action in March 2025 imposed a 25% tariff on imported automobiles and extended the framework to certain automobile parts, with implementation beginning in April and May 2025. This directly increases landed cost exposure for globally sourced lighting assemblies and subcomponents across OEM supply programs.

In headlight programs, this tariff structure raises module cost through duty stacking, requalification expense, customs complexity, and emergency sourcing shifts. As a result, OEMs delay higher-spec fitment, pressure suppliers for price givebacks, and protect margins by limiting advanced lighting content on cost-sensitive vehicle trims. Suppliers with domestic manufacturing or Mexico-US integrated supply chains carry a structural cost advantage in this environment.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chip allocation pressure | -1.4% | North America, EU, Japan, Korea, China export hubs | Short term (≤ 2 years) |

| Tariff-driven cost inflation | -1.1% | US core, Mexico-US corridor, selected EU import routes | Short term (≤ 2 years) |

| Headlamp homologation burden | -0.9% | EU, UK, UNECE-aligned APAC markets | Medium term (2-4 years) |

| EV cost-down pressure | -0.8% | EU, China, North America, India | Medium term (2-4 years) |

| Tier-supplier instability | -0.7% | Germany, Central Europe, wider EU supply base | Medium term (2-4 years) |

| Carbon-cost metals exposure | -0.6% | EU and Asia-EU supply corridors | Long term (≥ 4 years) |

Challenges

The market faces a growing homologation burden because headlight systems increasingly incorporate adaptive beam shaping, glare control, high-output LEDs, and software-managed illumination functions. These must satisfy different regulatory interpretations and testing pathways across major automotive jurisdictions. Suppliers managing US DOT, UNECE, and regional standards simultaneously face a recurring drag of approximately -0.9 percentage points on achievable CAGR.

Engineering resources are diverted into recertification loops, validation lead times lengthen by one or two development gates, and launch complexity rises as OEMs seek broader product differentiation. Mitigation depends on simulation-led validation, modular beam libraries, and region-configurable compliance engineering embedded earlier in program development. Suppliers who build these capabilities into their core development process convert a cost drag into a barrier that protects them from less sophisticated competitors.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Electronics sourcing concentration | -1.2% | North America core, EU OEM hubs, China vehicle clusters, Japan-Korea supply base | Medium term (2-4 years) |

| Multi-region compliance complexity | -0.9% | US certification market, EU regulatory hubs, Japan advanced lighting programs | Medium term (2-4 years) |

| Skilled engineering gap | -0.7% | Germany-Central Europe, US-Mexico auto belt, China smart-manufacturing zones | Medium term (2-4 years) |

| Thermal durability pressure | -0.8% | Global premium vehicles, hot-climate regions, EV-heavy platforms | Long term (≥ 4 years) |

| Software integration overload | -1.0% | China SDV programs, EU premium OEMs, North America ADAS-linked platforms | Long term (≥ 4 years) |

| Supply-chain timing volatility | -0.6% | APAC export corridors, Europe assembly networks, North America service channels | Short term (≤ 2 years) |

Opportunities

ADB mass-market scaling is a near-term opportunity because the regulatory door has only just opened in key markets. NHTSA’s 2022 final rule amended FMVSS 108 to permit ADB headlamp certification, setting performance requirements but not yet embedding ADB as a standard feature in high-volume nameplates. Adoption remains confined mainly to premium trims, leaving most B and C segment vehicles without adaptive beam functionality.

If OEMs can leverage shared ADB platforms across multiple compact and midsize models and lift ADB take rates by 6 to 8 percentage points in North America, the EU, Japan, and Korea over the next 3 to 5 model years, the incremental upside is measurable. This could represent several million additional ADB-equipped vehicles annually, generating an estimated $80 to $150 per vehicle system uplift. The resulting CAGR upside could reach 2.3 percentage points above the hardware-only baseline as safety ratings increasingly reward glare-managed illumination.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| ADB mass-market scaling | +2.3% | North America, EU, Japan, Korea | Short term (≤ 2 years) |

| Aging-fleet retrofit programs | +1.7% | EU, North America, LATAM, India | Short term (≤ 2 years) |

| Software-defined lighting services | +1.5% | North America, EU, China | Medium term (2-4 years) |

| Micro-LED democratization | +2.0% | China, EU, Japan, Korea | Medium term (2-4 years) |

| Commercial fleet safety bundles | +1.3% | EU, North America, GCC | Medium term (2-4 years) |

| Headlights as communication nodes | +1.8% | China, EU, select APAC smart cities | Long term (≥ 4 years) |

Regional Analysis

Asia-Pacific Dominates the Car Headlight Market with a Market Share of 42.8%, Valued at USD 7.83 Billion

Asia-Pacific commands 42.8% of the global car headlight market at USD 7.83 Billion in 2025. High-volume automotive production in China, India, and Southeast Asia drives large-scale OEM headlight procurement across all vehicle classes. This production concentration makes the region the primary battleground for OEM supply contracts through the forecast period.

North America holds a structurally significant position shaped by a decade-long regulatory transition in adaptive headlamp standards. Toyota first petitioned NHTSA to permit ADB headlamp systems in 2013, but the final rule permitting ADB certification was not published until February 22, 2022, nearly a decade after the initial petition. This delayed approval compressed North American ADB adoption timelines, creating a near-term procurement surge as OEMs now accelerate ADB integration across new model programs.

Europe maintains a strong market position anchored by UNECE Regulation No. 149 and established DRL mandates in force since 2011. The EU regulatory framework supports broader engineering standardization across passenger and commercial vehicle platforms, enabling suppliers to scale adaptive lighting products across multiple OEM programs simultaneously. This standardization advantage reduces per-unit compliance cost relative to fragmented US certification pathways.

Latin America and Middle East and Africa represent smaller but structurally relevant segments driven by aftermarket replacement demand and fleet expansion. Aging vehicle populations in these regions sustain consistent halogen replacement procurement. Retrofit LED conversion kits represent the primary growth channel for suppliers entering these markets at accessible price points.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Competitive Analysis

FORVIA HELLA operates as a high-frequency product launch engine in automotive lighting, with three distinct headlamp innovations released between January and October 2025 alone. In February 2025, the company expanded its SlimLine product family with a new LED combination lamp integrating daytime running light, position light, and indicator functions in a single module for commercial and off-highway vehicles. This modular integration strategy reduces per-vehicle component count and strengthens HELLA’s position in commercial fleet procurement programs across Europe.

Key Players

- Framo

- Mitsui Miike

- Maxon

- Bierens

- GAM

- Tamiya

- Parekh Engineering Company

- Stork

Recent Developments

- September 2025 – Valeo and Ennostar introduced a Mini LED-based high-definition automotive exterior display system at IAA Mobility 2025, enabling V2X communication through smart lighting interfaces.

- October 2025 – FORVIA HELLA launched FlatLight technology for daytime running lights, reducing installation depth to 5 mm while improving energy efficiency by up to 40 percent for next-generation vehicle lighting systems.

- June 2026 – FORVIA HELLA launched series production of LeanLED II, a combined front and rear lighting system designed for commercial and special vehicles with unified light signature architecture.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 18.3 Billion |

| Forecast Revenue (2035) | USD 37.8 Billion |

| CAGR (2026-2035) | 7.50% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Halogen Light, Xenon Light, Others), By Application (Passenger Car, Commercial Vehicle) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Framo, Mitsui Miike, Maxon, Bierens, GAM, Tamiya, Parekh Engineering Company, Stork |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |