Global Blood Pressure Transducers Market By Procedure (Non Invasive and Invasive), By Technology (Digital, Aneroid, Wearable and Others), By Type (Disposable and Reusable), By End-User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Jan 2026

- Report ID: 175383

- Number of Pages: 233

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

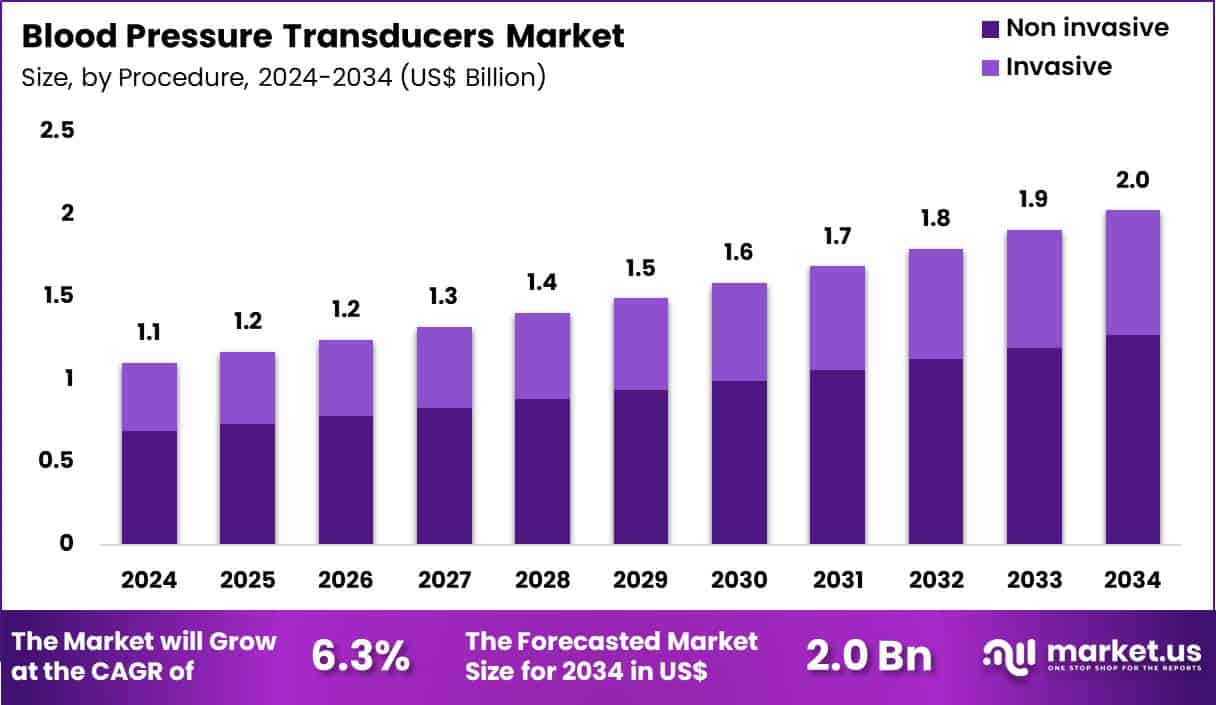

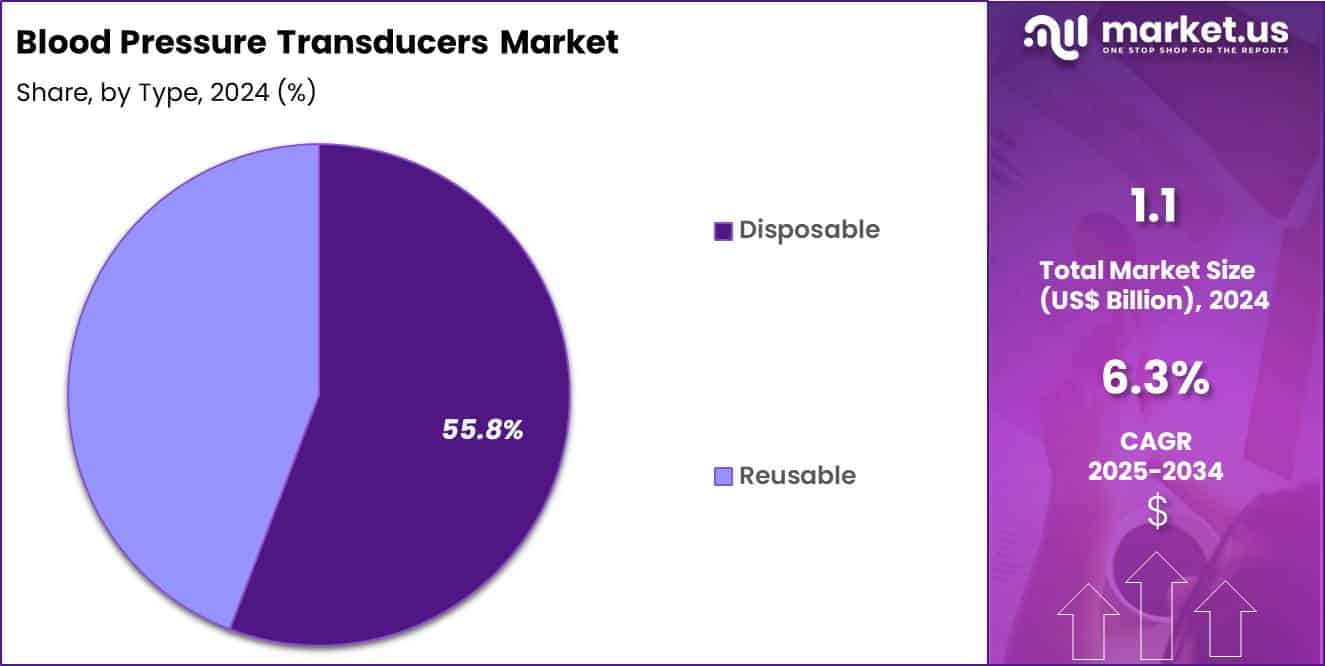

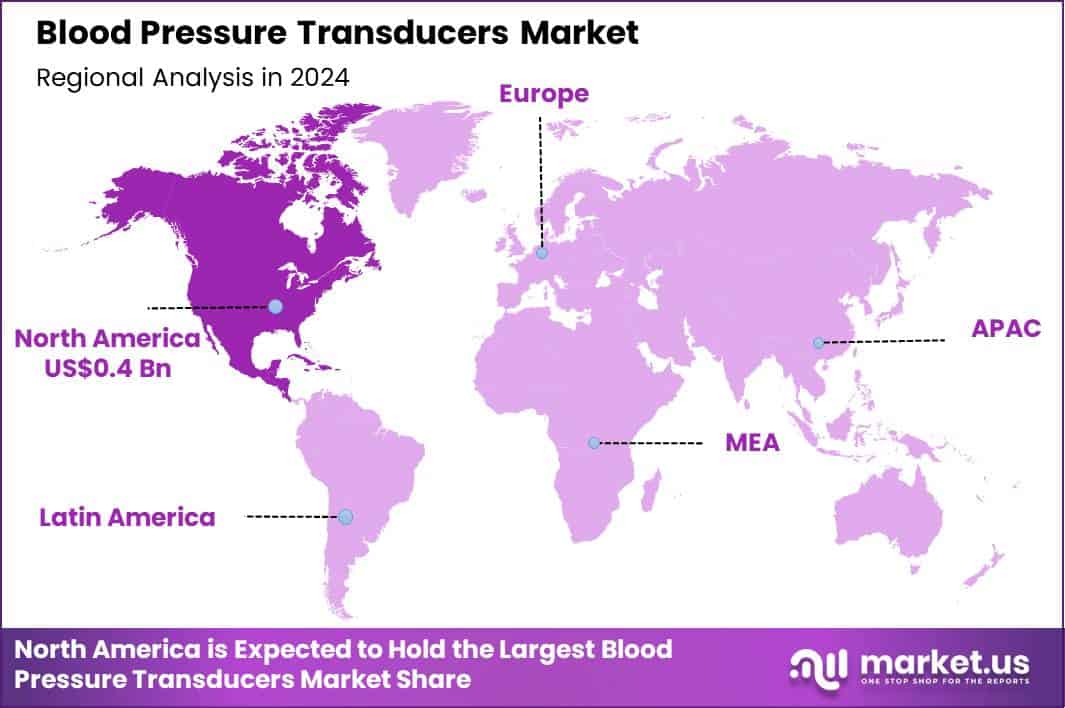

Global Blood Pressure Transducers Market size is expected to be worth around US$ 2.0 Billion by 2034 from US$ 1.1 Billion in 2024, growing at a CAGR of 6.3% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 39.9% share with a revenue of US$ 0.4 Billion.

Increasing prevalence of cardiovascular diseases and critical care needs propels the blood pressure transducers market as healthcare providers require accurate, real-time hemodynamic monitoring to guide therapeutic decisions. Intensivists increasingly utilize invasive arterial pressure transducers in surgical intensive care units to measure systemic arterial pressure continuously, enabling precise titration of vasopressors and inotropes during septic shock or cardiogenic shock.

These devices support intraoperative monitoring in cardiac and major vascular surgeries, where surgeons rely on waveform analysis to assess volume status and guide fluid resuscitation. Anesthesiologists apply blood pressure transducers during general anesthesia to detect hypotension promptly, maintaining organ perfusion in high-risk patients undergoing orthopedic or neurosurgical procedures.

In emergency departments, clinicians deploy transducers for trauma patients with hemorrhagic shock, facilitating rapid identification of blood loss and response to resuscitation efforts. Neonatal intensive care teams use miniaturized transducers to monitor preterm infants, ensuring stable blood pressure during mechanical ventilation and surfactant administration.

Manufacturers pursue opportunities to develop wireless and minimally invasive transducers that reduce infection risks and improve patient mobility in intermediate care settings. Developers advance integrated systems with advanced algorithms that analyze pulse pressure variation and stroke volume variation, enhancing fluid responsiveness assessment in mechanically ventilated patients.

These innovations facilitate applications in ambulatory monitoring for heart failure patients, where non-invasive or semi-invasive transducers track trends and alert to decompensation. Opportunities emerge in disposable, single-patient-use transducers with enhanced signal fidelity, supporting high-acuity environments with stringent infection control protocols.

Companies invest in smart transducers that incorporate predictive analytics, enabling early warning of hemodynamic instability in postoperative recovery. Recent trends emphasize seamless integration with electronic health records and multiparameter monitors, streamlining data flow and supporting value-based care models focused on improved outcomes in critical and perioperative settings.

Key Takeaways

- In 2024, the market generated a revenue of US$ 1.1 Billion, with a CAGR of 6.3%, and is expected to reach US$ 2.0 Billion by the year 2034.

- The procedure segment is divided into non invasive and invasive, with non invasive taking the lead with a market share of 62.7%.

- Considering technology, the market is divided into digital, aneroid, wearable and others. Among these, digital held a significant share of 48.9%.

- Furthermore, concerning the type segment, the market is segregated into disposable and reusable. The disposable sector stands out as the dominant player, holding the largest revenue share of 55.8% in the market.

- The end-user segment is segregated into hospitals, ambulatory surgical centers, specialty clinics and others, with the hospitals segment leading the market, holding a revenue share of 57.4%.

- North America led the market by securing a market share of 39.9%.

Procedure Analysis

Non invasive procedures contributed 62.7% of growth within procedure and lead the blood pressure transducers market due to broad clinical use across routine monitoring and early risk screening. Nurses and clinicians rely on non invasive measurement because it fits triage, ward rounds, outpatient visits, and post-operative observation without vascular access.

The method supports quick repeat readings, which matters for unstable patients, medication titration, and perioperative assessment. Hospitals also prefer non invasive setups because they reduce complication risk and simplify workflow across large patient volumes. Expanding hypertension prevalence increases routine monitoring needs in both acute and ambulatory care, strengthening demand for reliable transducer-enabled devices.

Technology improvements also support this segment through better motion tolerance and faster inflation deflation cycles that improve patient comfort. Remote monitoring programs and bedside telemetry increase measurement frequency, raising transducer usage across different care points. Non invasive monitoring aligns with infection control goals since it reduces exposure to invasive lines and dressing changes.

Clinical guidelines emphasize regular blood pressure checks for cardiovascular risk control, which reinforces high utilization. The segment is projected to remain dominant due to ease of deployment, safety advantages, and the sheer scale of routine blood pressure monitoring across healthcare settings.

Technology Analysis

Digital technology represented 48.9% of growth within technology and drives adoption because it improves readability, data capture, and clinical workflow integration. Clinicians prefer digital systems since they provide fast results with clear displays that reduce manual interpretation errors. Digital devices also support automated cycling, trend tracking, and alarm thresholds, which strengthens monitoring quality in high-acuity environments.

Integration with electronic records and central monitoring platforms increases value for hospitals that manage large patient loads. Digital accuracy validation and calibration support stronger confidence compared to many manual alternatives in high-throughput care settings.

Patient comfort and speed improvements also encourage wider use in wards and outpatient clinics. Demand rises further as hospitals adopt connected care models that depend on consistent, structured vital sign data.

Digital formats support staff efficiency because they reduce documentation burden and standardize readings across shifts. Portable digital systems also expand use during transport, diagnostics, and recovery areas. The segment is anticipated to retain leadership due to operational efficiency, connectivity benefits, and growing preference for automated vital sign capture.

Type Analysis

Disposable products accounted for 55.8% of growth within type and gain traction because healthcare facilities prioritize infection prevention and standardized performance per patient encounter. Hospitals increasingly adopt disposable transducers to limit cross-contamination risk and reduce reprocessing workload.

Single-use designs support faster patient turnover in operating rooms, ICUs, and emergency departments where time matters. Staff also benefit from simplified setup because disposables eliminate repeated cleaning, calibration drift concerns, and maintenance delays. Growing procedural volumes and intensive monitoring needs increase disposable consumption, which strengthens repeat purchasing patterns.

Cost justification improves when hospitals compare labor and sterilization costs against single-use efficiency. Disposable components also support consistent pressure waveform performance in critical monitoring contexts. Many facilities prefer disposables for high-risk patients, including immunocompromised and long-stay ICU populations.

Procurement teams value predictable quality and controlled supply through standardized SKUs. The segment is projected to remain dominant due to infection control priorities, workflow convenience, and rising use of single-patient consumables across acute care.

End-User Analysis

Hospitals generated 57.4% of growth within end-users and remain the largest purchasing base because they conduct the highest volume of vital monitoring across departments. Emergency rooms, operating suites, ICUs, and inpatient wards require constant blood pressure assessment, which sustains steady transducer demand.

Hospitals manage complex cardiovascular, surgical, and critical care cases that need frequent measurement cycles and reliable equipment uptime. Procurement scale supports bulk purchasing agreements, enabling broader deployment across multiple units and facilities. Hospitals also upgrade monitoring infrastructure regularly to improve patient safety, strengthen documentation, and support clinical decision speed.

Digital adoption and centralized monitoring expand hospital demand further because these systems depend on consistent sensor and transducer performance. Staff training programs standardize equipment use, which increases device utilization and replacement cycles. Hospitals also drive demand for disposable products due to strict infection prevention policies and high patient turnover.

Expansion of hospital bed capacity and surgical volumes increases overall monitoring points across floors. The segment is expected to remain dominant due to patient concentration, continuous monitoring requirements, and ongoing modernization of hospital vital sign systems.

Key Market Segments

By Procedure

- Non Invasive

- Invasive

By Technology

- Digital

- Aneroid

- Wearable

- Others

By Type

- Disposable

- Reusable

By End-user

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Others

Drivers

Increasing prevalence of hypertension is driving the market.

The growing global incidence of hypertension has substantially increased the need for accurate monitoring devices, including blood pressure transducers, in clinical and critical care environments. Advanced diagnostic practices and heightened public health awareness have led to more frequent identifications of high blood pressure cases.

According to the World Health Organization, an estimated 1.4 billion adults aged 30–79 years worldwide had hypertension in 2024, representing 33% of this population group. This substantial figure highlights the escalating health challenge and the corresponding demand for invasive monitoring tools in surgical and intensive care settings. Blood pressure transducers enable real-time arterial pressure assessment, essential for managing hypertensive complications during procedures.

The association between hypertension and comorbidities such as heart disease further intensifies the requirement for reliable transduction technology. National health agencies are advocating for enhanced monitoring protocols to mitigate risks in affected populations.

Leading manufacturers are advancing transducer designs to support this expanding diagnostic landscape. This driver is instrumental in promoting investments in healthcare technology for better patient outcomes. Ultimately, the prevalence trend sustains robust market momentum across various medical disciplines.

Restraints

High development costs are restraining the market.

The considerable financial outlay needed for innovating and producing blood pressure transducers restricts market accessibility and innovation pace. Intricate engineering processes for sensor accuracy and biocompatibility elevate overall expenditure in the supply chain. Emerging companies face challenges in securing capital for compliance with stringent medical standards.

Oversight from health authorities demands comprehensive validation, adding to fiscal pressures on developers. In cost-limited healthcare frameworks, these expenses translate to higher product pricing, limiting procurement. ICU Medical reported research and development expenses of $88.6 million in 2024, illustrating the significant investment required for product advancement.

Clinicians may favor established alternatives when facing budget constraints in equipment upgrades. This restraint curtails expansion in underfunded medical sectors globally. Initiatives to streamline development through partnerships seek to ease these burdens gradually. Nevertheless, high costs persist as a key impediment to comprehensive market growth.

Opportunities

Expansion of healthcare infrastructure in Asia-Pacific is creating growth opportunities.

The swift enhancement of medical facilities throughout Asia-Pacific nations fosters prospects for deploying blood pressure transducers in upgraded hospitals and clinics. Governmental commitments to health sector funding enable the integration of advanced monitoring equipment in expanding networks. The region’s demographic pressures, including large populations, necessitate scalable solutions for critical care management.

Alliances with international suppliers aid in meeting regulatory and technical requirements for local adoption. Capacity-building programs for medical personnel promote proficient utilization of transduction systems. Urban development correlates with increased establishment of specialized care units requiring precise pressure monitoring.

Reforms targeting universal coverage amplify infrastructure projects across the area. Prominent corporations are setting up regional operations to leverage efficient distribution and lower transportation expenses. This opportunity facilitates diversification from mature economies into vibrant growth zones. Targeted strategies can secure notable positions in these burgeoning healthcare landscapes.

Impact of Macroeconomic / Geopolitical Factors

Global economic momentum supports expanded hospital budgets for monitoring equipment, advancing the blood pressure transducers market as providers integrate precise invasive and non-invasive sensors to manage cardiovascular care effectively in growing patient populations. Companies pursue opportunities from increasing procedural volumes in outpatient settings, which sustains demand for reliable pressure measurement solutions worldwide.

Nevertheless, sustained inflationary forces worldwide drive up costs for electronic components and sterile materials, obliging manufacturers to address profitability pressures in competitive pricing dynamics. Geopolitical uncertainties in semiconductor and sensor-producing regions create supply interruptions, requiring distributors to handle variability in component availability across global networks.

Industry participants respond by broadening sourcing relationships to more dependable locations, which improves procurement consistency and enables proactive risk management. Current US tariffs on imported medical devices and components from primary suppliers impose added duties, frequently at baseline levels of 10% with higher rates for specific origins under trade policies, which elevates expenses for overseas-sourced transducers entering the U.S. market.

Domestic producers benefit from this structure by intensifying local assembly and component integration, which promotes engineering advancements and reinforces supply independence. Ongoing innovations in wireless connectivity and miniaturized designs steadily invigorate the sector, ensuring enhanced accuracy, operational efficiency, and promising long-term growth for healthcare applications globally.

Latest Trends

Adoption of cellular-enabled monitoring devices is a recent trend in the market.

In 2024, the incorporation of cellular connectivity in blood pressure monitoring has advanced remote patient oversight in chronic care scenarios. These enhancements allow seamless data relay from transducers to healthcare platforms without wired constraints. Multi-cuff configurations in new devices support diverse patient profiles while maintaining measurement precision. Innovations target efficiency in remote patient management and chronic condition tracking.

Smart Meter launched a cellular-enabled multi-cuff blood pressure monitoring device in July 2024, designed specifically for remote patient monitoring and chronic care management. This progress minimizes dependency on traditional setups, improving accessibility in outpatient contexts. Emphasis on integration with electronic records streamlines clinical workflows.

Regulatory endorsements in 2024 for connected features have hastened device rollout. Partnerships enhance sensor capabilities with telecommunication standards. Such evolutions aim to elevate care standards for hypertension and related ailments moving forward.

Regional Analysis

North America is leading the Blood Pressure Transducers Market

North America holds a 39.9% share of the global blood pressure transducers market, illustrating notable progression in 2024 fueled by escalating demands for precise hemodynamic monitoring in critical care settings amid surging cardiovascular incidences. Innovations in disposable transducer designs have minimized cross-contamination risks, aligning with stringent infection control protocols in U.S. hospitals.

Key manufacturers have refined sensor accuracy and integration with electronic health records, facilitating real-time data analytics for improved patient outcomes in surgical and ICU environments. Rising procedural volumes in interventional cardiology have necessitated reliable arterial pressure measurement tools, supporting timely clinical decisions. Federal emphasis on enhancing emergency response capabilities has spurred adoption in trauma centers across the region.

Collaborative R&D between device firms and healthcare providers has optimized calibration-free systems, reducing operational downtime. Expanding telemedicine frameworks incorporate these transducers for remote vital sign oversight, broadening accessibility. In 2024, the National Heart, Lung, and Blood Institute awarded Dynocardia a $500,000 grant to advance its wrist-worn continuous blood pressure monitoring technology under the Commercial Readiness Pilot Program.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Healthcare firms and institutions drive expansion of invasive arterial monitoring technologies throughout the Asia Pacific region over the forecast period, responding to burgeoning chronic hypertension cases and infrastructure upgrades. China spearheads initiatives by subsidizing local production of advanced sensors to ensure affordability in rural hospitals.

India bolsters capabilities through targeted schemes that fund component localization and clinical validation for precision devices. Japan refines miniaturization techniques to integrate these tools into wearable formats for elderly care applications. Pharmaceutical entities collaborate on hybrid systems combining transducers with drug delivery for optimized cardiac management.

Academic networks conduct multicenter studies to adapt international standards to regional patient profiles. Regulatory agencies expedite approvals for innovative designs addressing high-volume emergency needs. In 2024, the Government of India launched a Rs 500 crore scheme to enhance domestic manufacturing of medical devices, including support for R&D labs and capital subsidies.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the Blood Pressure Transducers market drive growth by improving sensor accuracy, signal stability, and disposable safety features that support reliable invasive monitoring in critical care and operating rooms. Companies expand adoption by aligning products with multi-parameter patient monitors and standardized ICU workflows that demand consistent hemodynamic data.

Commercial strategies emphasize hospital contracting, strong distributor coverage, and clinician training to reduce setup errors and support repeat procurement. Innovation priorities focus on reducing drift, enhancing connector compatibility, and simplifying priming and flushing steps to improve ease of use for nursing teams.

Market expansion targets regions increasing surgical volumes and intensive care capacity, where invasive blood pressure monitoring remains routine. Edwards Lifesciences operates as a leading participant through its hemodynamic monitoring expertise, strong hospital relationships, and proven portfolio of high-performance pressure monitoring components.

Top Key Players

- Edwards Lifesciences

- ICU Medical, Inc.

- Becton, Dickinson and Company (BD)

- Smiths Medical

- Baxter International Inc.

- Medtronic

- Merit Medical Systems

- Argon Medical Devices

- Utah Medical Products, Inc.

- Nipro Corporation

Recent Developments

- In May 2024, Masimo Corporation secured USD 250 million in a financing round led by New Enterprise Associates to broaden its noninvasive monitoring portfolio and speed up R&D in advanced blood pressure monitoring technologies. This funding supports faster product development cycles, stronger clinical validation, and wider commercialization efforts, reinforcing innovation momentum in continuous and cuffless blood pressure monitoring solutions across hospital and outpatient care settings.

- In April 2025, the European Commission approved the use of Edwards Lifesciences’ Nexfin noninvasive blood pressure monitoring system for adult intensive care environments across Europe. This authorization strengthens market adoption by expanding regulated access to continuous hemodynamic monitoring tools in critical care, supporting improved patient management and increasing procurement opportunities for noninvasive blood pressure technologies in European hospitals.

Report Scope

Report Features Description Market Value (2024) US$ 1.1 Billion Forecast Revenue (2034) US$ 2.0 Billion CAGR (2025-2034) 6.3% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Procedure (Non Invasive and Invasive), By Technology (Digital, Aneroid, Wearable and Others), By Type (Disposable and Reusable), By End-User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics and Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Edwards Lifesciences, ICU Medical, Inc., Becton, Dickinson and Company (BD), Smiths Medical, Baxter International Inc., Medtronic, Merit Medical Systems, Argon Medical Devices, Utah Medical Products, Inc., Nipro Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Blood Pressure Transducers MarketPublished date: Jan 2026add_shopping_cartBuy Now get_appDownload Sample

Blood Pressure Transducers MarketPublished date: Jan 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Edwards Lifesciences

- ICU Medical, Inc.

- Becton, Dickinson and Company (BD)

- Smiths Medical

- Baxter International Inc.

- Medtronic

- Merit Medical Systems

- Argon Medical Devices

- Utah Medical Products, Inc.

- Nipro Corporation

Our Clients

- 175383

- Jan 2026