Quick Navigation

Report Overview

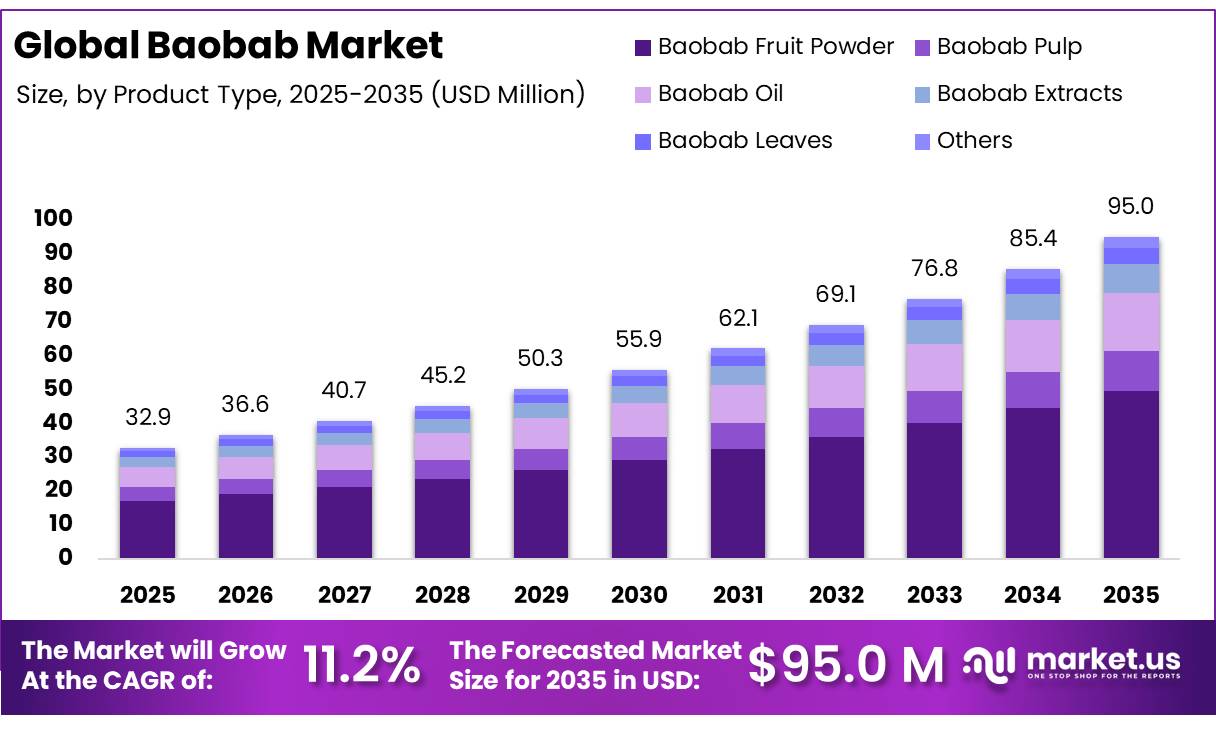

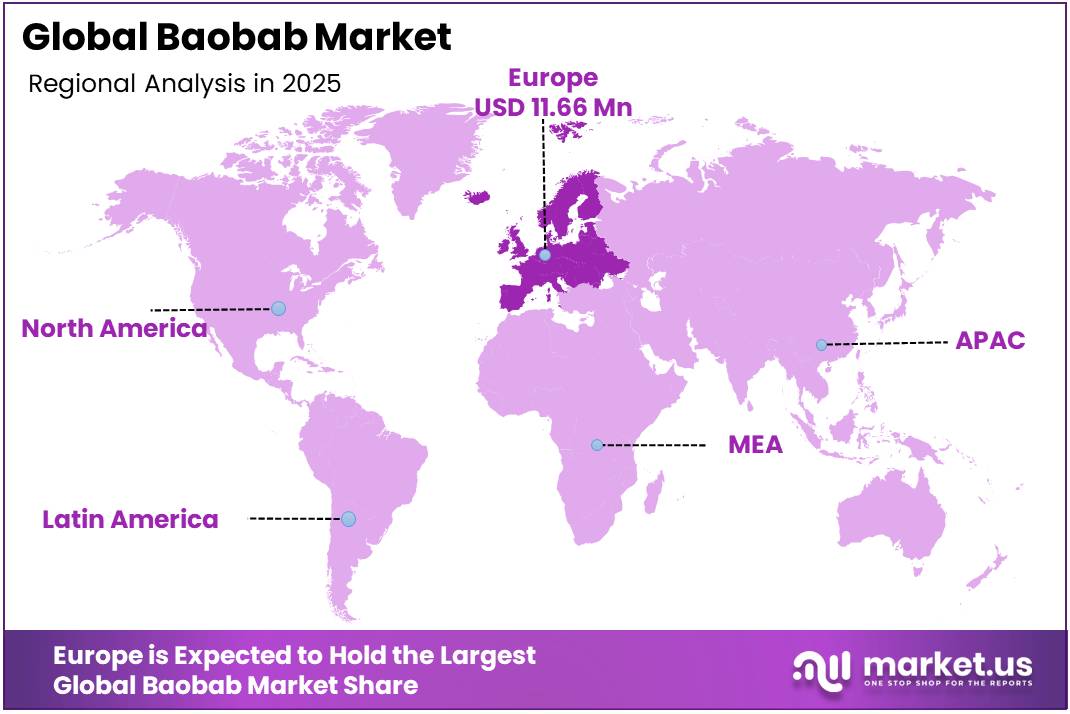

In 2025, the Global Baobab Market was valued at USD 32.9 million. Between 2026 and 2035, this market is estimated to register a CAGR of 11.2%, reaching approximately USD 95.0 million by 2035. In 2025, Europe led the market, achieving over 35.4% share with a revenue of USD 11.66 million.

The Baobab market is a global natural ingredients sector encompassing fruit powder, pulp, oil, extracts, and leaves derived from the Adansonia digitata tree supplied to food and beverage manufacturers, nutritional supplement producers, cosmetic formulators, and pharmaceutical companies across global markets.

- According to the U.S. Department of Agriculture (USDA) FoodData Central in 2025, 100 g of baobab fruit pulp contains approximately 5 g of dietary fibre, 24.6 g of total sugars, 300 mg of calcium, and 2.3 mg of iron, highlighting its strong nutritional profile for use in functional foods and beverages.

Key Takeaways

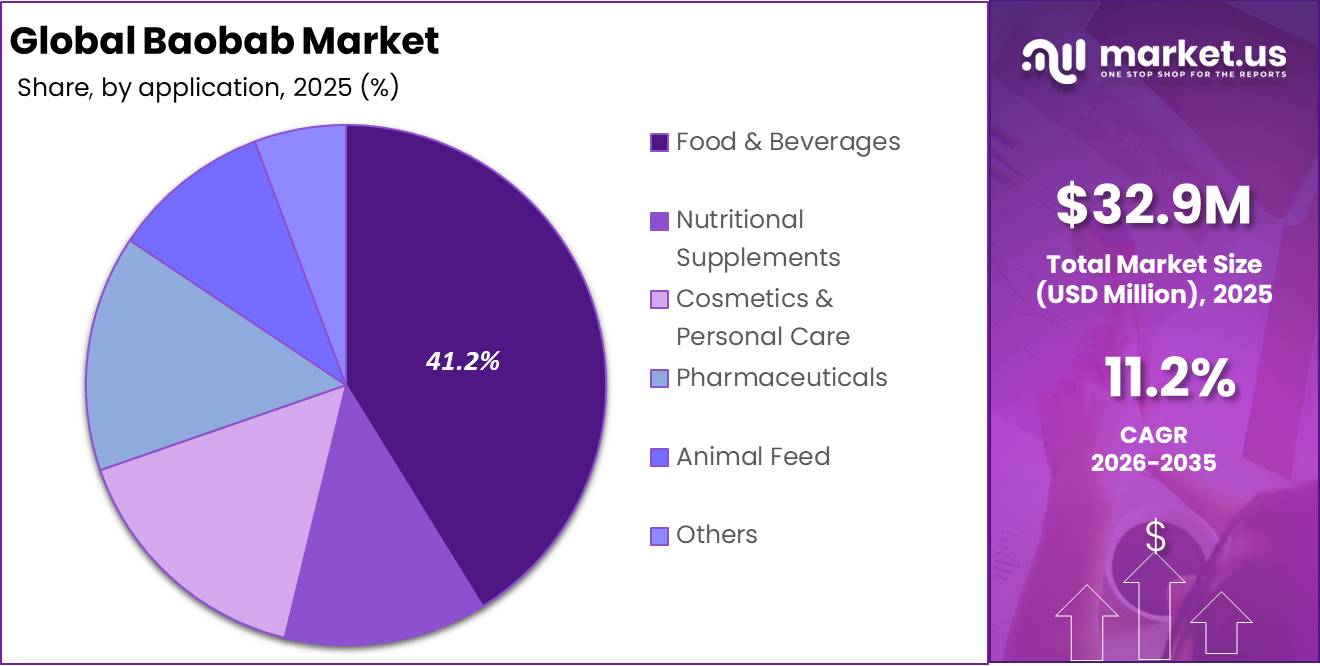

- The global baobab market was valued at USD 32.9 million in 2025.

- The market is projected to grow at a CAGR of 11.2% and is estimated to reach USD 95.0 million by 2035.

- Baobab fruit powder is the dominant product type, accounting for 52.3% of the market in 2025, driven by its broad application across food, beverage, supplement, and cosmetic manufacturing formats.

- Organic is the dominant nature segment at 63.4%, reflecting strong consumer preference for certified organic superfoods across European and North American retail markets.

- Powder form is the dominant form at 58.6%, supported by its versatility in food formulation, nutritional supplement manufacturing, and cosmetic ingredient applications.

- Food & Beverages leads application demand at 41.2%, anchored by baobab powder’s use as a functional ingredient in smoothies, energy bars, and fortified beverages.

- Business-to-Business (B2B) is the dominant distribution channel, accounting for 46.5% of the market in 2025.

- Europe holds the largest regional share at 35.4%, driven by EU novel food regulatory approval, high consumer health awareness, and established natural ingredient supply chains.

The baobab fruit is naturally dry inside its shell and is rich in vitamin C, antioxidants, fibre, calcium, and magnesium. It carries a tangy, citrus-like flavor. Baobab is native to sub-Saharan Africa, Madagascar, and parts of Australia and Arabia, with virtually all commercial supply sourced through wild harvest by rural communities across African producing regions.

According to the World Health Organization (WHO, 2025), more than 2 billion people worldwide continue to suffer from deficiencies in essential vitamins and minerals. This has increased interest among food manufacturers in nutrient-rich plant ingredients such as baobab, which naturally contains high levels of vitamin C, dietary fiber, calcium, and potassium for functional food applications.

The future outlook relies on integrating AI into agricultural supply networks. Machine learning algorithms optimize wild-harvest tracking, predict seasonal yields, and manage supply chain traceability via automated digital platforms. AI-powered traceability systems and digital supply chain platforms are being deployed to address baobab’s sourcing challenges improving origin verification, quality consistency, and ethical procurement transparency across the wild harvest supply chain.

Baobab Market Segmentation

By Product Type

Baobab Fruit Powder Represents the Dominant Segment in the Market

In 2025, Baobab Fruit Powder accounted for a leading 52.3% share of the Baobab market by product type, due to its broad formulation versatility across food and beverage manufacturing, nutritional supplement production, and cosmetic ingredient applications. For instance, Nexira a leading baobab ingredient supplier specifically supplies organic baobab pulp powder to food, health, and nutrition industry customers, confirming the commercial centrality of the powder format to global baobab supply chains by Nexira. EU novel food regulatory approval, FDA market access confirmation, shelf stability relative to fresh fruit formats, and broad manufacturing formulation compatibility are the primary structural determinants of Baobab Fruit Powder segment dominance.

Baobab Extracts are the fastest-growing product type across the forecast period. Standardised baobab extracts concentrated for specific bioactive fractions including polyphenols, iridoid glycosides, and vitamin C are gaining commercial traction in pharmaceutical and cosmetic applications where precise active compound concentration is required.

Type Analysis

Organic Represents the Dominant Segment in the Market

In 2025, Organic accounted for a leading 63.4% share of the Baobab market by nature, due to strong consumer preference for certified organic superfoods across European and North American retail markets where organic certification is increasingly used as a quality and safety signal by health-conscious consumers purchasing functional food ingredients. Consumer demand for certified organic superfoods, EU regulatory frameworks supporting organic ingredient labelling, and retailer requirements for organic certification in premium natural food and supplement product lines are the primary structural determinants of organic segment dominance.

Conventional baobab is the fastest-growing nature segment across the forecast period. Rising demand for cost-competitive baobab ingredients across food manufacturing, animal feed, and pharmaceutical applications where organic certification is not a purchasing requirement is driving conventional segment growth.

By Form

Powder Represents the Dominant Segment in the Market

In 2025, Powder accounted for a leading 58.6% share of the Baobab market by form, due to its broad formulation compatibility across food and beverage manufacturing, nutritional supplement production, and cosmetic ingredient applications. Powdered baobab is shelf-stable, easy to blend, and compatible with dry mixing, encapsulation, and beverage fortification processes making it the default format for industrial ingredient buyers across all major application categories. Shelf stability, formulation versatility across food and supplement applications, compatibility with industrial mixing and blending processes, and lower logistics cost relative to liquid formats are the primary structural determinants of powder segment dominance.

Oil is the fastest-growing form segment. Cold-pressed baobab seed oil is gaining commercial traction in premium cosmetic and personal care formulations valued for its moisturising, conditioning, and antioxidant properties. The rising consumer demand for natural and organic cosmetic ingredients is expected to drive baobab oil adoption across luxury skincare product lines globally.

By Application

Food & Beverages Represents the Dominant Application in the Market

In 2025, Food & Beverages accounted for a leading 41.2% share of the Baobab market by application, due to baobab powder’s broad use as a functional ingredient in smoothies, energy bars, fortified beverages, yoghurts, and bakery products across European and North American health food markets. For instance, FAO confirmed baobab as a key indigenous food species with documented applications in gruels, jams, yoghurts, wines, and juice across its traditional consumption geographies, confirming broad food application compatibility.

Cosmetics & Personal Care is the fastest-growing application segment across the forecast period. Baobab oil and baobab extract are gaining commercial traction in premium skincare formulations valued for their moisturising, antioxidant, and anti-inflammatory properties. The rising consumer demand for natural and clean beauty ingredients is expected to accelerate baobab oil and extract adoption across luxury and mass-market cosmetic product lines globally.

By Distribution Channel

Business-to-Business (B2B) Represents the Dominant Segment in the Market

In 2025, Business-to-Business (B2B) accounted for a leading 46.5% share of the Baobab market by distribution channel, due to baobab’s primary commercial flow as an industrial ingredient supplied directly from African producers and European processors to food manufacturers, nutritional supplement producers, cosmetic formulators, and pharmaceutical companies. The B2B channel reflects the ingredient-market nature of baobab where the majority of commercial volume is transacted between ingredient suppliers and industrial buyers rather than through consumer retail formats.

Online retail is the fastest-growing distribution channel for baobab consumer products. Direct-to-consumer e-commerce platforms including Amazon, iHerb, and brand-owned health supplement websites are expanding consumer access to baobab powder, capsule, and oil products across European and North American markets. The online retail is projected to capture an increasing share of consumer-facing baobab product distribution as health-conscious consumer awareness of baobab grows alongside digital commerce infrastructure.

Key Market Segments

Product Type

- Baobab Fruit Powder

- Baobab Pulp

- Baobab Oil

- Baobab Extracts

- Baobab Leaves

- Others

By Nature

- Organic

- Conventional

By Form

- Powder

- Liquid

- Capsules & Tablets

- Oil

- Others

Application

- Food & Beverages

- Nutritional Supplements

- Cosmetics & Personal Care

- Pharmaceuticals

- Animal Feed

- Others

Distribution Channel

- Business-to-Business (B2B)

- Business-to-Consumer (B2C)

Driver Analysis

EU novel-food clarity and compliant market access

A second structural driver is regulatory clarity rather than deregulation: baobab fruit pulp already sits within the EU’s novel-food architecture, and the current framework gives exporters a defined route through either full authorization or the traditional-food-from-third-countries pathway with evidence of at least 25 years of safe use. This matters commercially because regulatory certainty reduces buyer hesitation, shortens onboarding cycles for importers and private-label brands, and lowers the perceived risk premium attached to new African botanicals in food applications.

Under the EU regime, EFSA’s scientific opinion can run on a 9-month timetable, followed by about 7 months for the Commission draft act, while traditional-food notifications can proceed if no substantiated safety objections arise within 4 months; those clock speeds are critical for launch planning, distributor commitments, and inventory financing. In practice, the effect is a +1.2 percentage-point CAGR contribution because the rulebook does not create consumer demand by itself, but it unlocks scalable B2B commercialization by making compliance more predictable for importers, contract manufacturers, and branded food companies targeting the EU first and then extending to adjacent markets that often view EU acceptance as a de-risking signal.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Functional nutrition demand for vitamin-C-rich baobab pulp | +1.9% | EU core, North America core, urban APAC premium channels | Short term (≤ 2 years) |

| EU novel-food clarity and compliant market access | +1.2% | EU, UK spill-over, Africa-to-EU export corridors | Medium term (2-4 years) |

| Beauty and personal-care uptake of baobab seed oil | +1.0% | EU cosmetics, North America naturals, Gulf premium beauty | Short term (≤ 2 years) |

| African sourcing commercialization and women-led export chains | +1.4% | Southern Africa, West Africa, EU import hubs | Medium term (2-4 years) |

| Wild-harvest dependence and climate-linked supply volatility | +0.6% | Sub-Saharan Africa source markets, EU and North America importers | Long term (≥ 4 years) |

| Premiumization in powders, blends, and clean-label formulations | +0.9% | North America, EU, APAC specialty nutrition | Short term (≤ 2 years) |

Restraint Analysis

EU authorization drag

The EU remains one of the most commercially attractive end markets for baobab ingredients, but novel-food entry mechanics still slow portfolio expansion because products new to the European market must pass either full authorization or the traditional-food notification route under Regulation (EU) 2015/2283, with EFSA typically given 9 months for a safety opinion and the Commission then 7 months to prepare the draft act, while traditional-food notifications can still be delayed if safety objections are raised within 4 months.

For baobab operators this creates a practical commercialization lag of roughly 16 to 24 months once dossier preparation, clock-stops, and buyer qualification are layered in, which suppresses new-SKU velocity, delays distributor onboarding, and pushes revenue recognition out by one to two budget cycles; in CAGR terms, that timing friction is reasonably modeled as a -1.4 percentage-point drag because innovation-led category expansion in powders, inclusions, beverage blends, and functional nutrition cannot scale at the same pace as consumer demand signals when regulatory clocks govern launch sequencing.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU authorization drag | -1.4% | EU core, UK-adjacent EU supply chains | Medium term (2-4 years) |

| High compliance cost | -1.1% | Southern Africa export hubs, EU corridor | Medium term (2-4 years) |

| U.S. import detention risk | -0.9% | North America core, West/East Africa export lanes | Short term (≤ 2 years) |

| Fragmented raw material base | -1.6% | Sub-Saharan Africa source markets, EU/APAC buyers | Long term (≥ 4 years) |

| Quality standardization gaps | -1.2% | EU, North America, premium nutraceutical channels | Short term (≤ 2 years) |

| Trade scaling bottlenecks | -0.8% | Africa-to-EU corridors, secondary APAC markets | Medium term (2-4 years) |

Opportunity Analysis

AfCFTA value-chain formalization

The market’s largest white space is the conversion of fragmented, informal, low-value collection into cross-border African ingredient trade under more organized standards, aggregation, and processing systems, especially because UNCTAD’s Africa trade work emphasizes the role of regional integration in scaling value chains while older baobab market briefs already identified food, beverage, botanical remedy, and nutraceutical segmentation as distinct demand pools rather than a single export stream.

If exporters and cooperatives use AfCFTA-era trade coordination to formalize collection nodes, add first-stage processing near source, and standardize quality grades, the market could reasonably capture +2.4 percentage points of CAGR upside by lifting producer-to-export recovery rates by 15–25%, reducing post-harvest and quality rejection losses by 8–12%, and increasing within-Africa value retention by 10–18 percentage points before final export; this is an opportunity, not a driver, because it depends on supply-chain redesign, investment in aggregation infrastructure, and institutional execution that most producing corridors have not yet completed.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| EU formulation expansion | +1.9% | EU core, UK | Short term (≤ 2 years) |

| AfCFTA value-chain formalization | +2.4% | West Africa, Southern Africa, East Africa | Medium term (2-4 years) |

| Seed oil premiumization | +1.6% | EU, North America, Gulf | Short term (≤ 2 years) |

| Leaf nutraceutical scaling | +1.3% | Southern Africa, EU, APAC health markets | Medium term (2-4 years) |

| Climate-resilient ingredient platforms | +2.1% | Sahel, East Africa, India dryland importers | Long term (≥ 4 years) |

| Traceable women-led sourcing models | +1.5% | EU, UK, North America | Short term (≤ 2 years) |

Challenges Analysis

Wild-harvest supply volatility

The baobab market in 2026 remains heavily dependent on non-domesticated trees in semi-arid and sub-humid zones, with most pulp and leaf supply still originating from naturally occurring stands rather than organized orchards, which introduces year-to-year volume swings of 15–25 percent at a local scale due to irregular flowering, fruiting, and localized droughts. Value-chain overviews for southern Africa report roughly 4,000 tonnes of baobab fruit harvested to yield about 500 tonnes of powder and 13.5 tonnes of seed oil in the formal sector, supported by approximately 60 SMEs and nearly 10,000 rural harvesters, implying that even modest shocks to household labor availability, access roads, or local rainfall patterns can remove hundreds of tonnes from exportable supply in a single season.

FAO’s statistical work on agrifood systems shows that global primary crop production rose by 56 percent between 2000 and 2022, yet Africa’s production environment remains exposed to water stress and rainfall variability, with many dryland systems facing elevated inter-annual yield volatility that transmits directly into baobab fruit availability. Strategically, this volatility translates into an estimated 1.2 percentage point drag on the market’s long-run CAGR because exporters and brand owners must price in safety stocks, multi-origin sourcing, and risk premiums for contracts; in response, companies are gradually piloting domestication trials, mixed baobab–crop agroforestry, and farmer-organization contracts, yet tree-maturation timelines of 10–15 years and uncertain yield curves mean that supply normalization will realistically take beyond a four-year horizon to materially dampen current variance.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Wild-harvest supply volatility | -1.2% | Sahel & Southern Africa | Long term (≥ 4 years) |

| Fragmented rural value chains | -0.9% | SSA sourcing basins | Medium term (2-4 years) |

| Climate & land-use stress | -0.8% | Sub-Saharan drylands | Long term (≥ 4 years) |

| Quality & food-safety variance | -1.0% | EU & OECD import hubs | Medium term (2-4 years) |

| Trade, traceability & ABS compliance | -0.7% | EU, UK, North America | Medium term (2-4 years) |

| Skills, standards & processing gaps | -0.6% | Africa processing hubs | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Climate Stress, Habitat Loss, and Conflict-Driven Food Insecurity Are Creating Supply and Demand Pressures Across the Global Baobab Market

The baobab market faces a distinctive geopolitical and environmental risk profile rooted in its African supply base. Climate change is creating measurable stress on wild baobab tree populations across sub-Saharan Africa with FAO confirming that more than 70% of wild food plant diversity in Africa, including baobab, is threatened at double the global average rate of decline due to habitat loss, land-use change, and climate stress. This ecological pressure threatens the long-term viability of wild harvest supply chains that currently supply the entire global baobab market.

Simultaneously, conflict and economic deterioration across baobab-producing regions particularly in the Sahel and Central Africa is disrupting harvesting, processing, and export logistics. In 2024, hunger in Africa reached its highest levels in over two decades across several conflict-affected subregions. These geopolitical pressures do not threaten market demand European and North American consumer demand for baobab ingredients continues to grow. But they introduce meaningful supply chain risk that manufacturers and ingredient distributors must actively manage through diversified sourcing, supplier development programmes, and forward contract frameworks through 2035.

Regional Analysis

Europe Held the Largest Share of the Global Baobab Market

Europe dominated the global baobab market in 2025, capturing 35.4% of consumption. Europe represents the leading regional market for baobab ingredients, driven by strong demand for functional and clean-label foods, early regulatory acceptance under EU Novel Food authorization for baobab fruit pulp, and well-established natural ingredient processing infrastructure. Key markets include the United Kingdom, Germany, France, and the Netherlands, where ingredient suppliers such as Nexira, Henry Lamotte Oils, and All Organic Treasures have developed integrated sourcing and distribution networks linking African producers with European manufacturers.

North America is the second-largest market, supported by GRAS regulatory acceptance pathways, rising consumer awareness of African superfoods, and a mature health food retail ecosystem including specialty and natural product retailers. Asia Pacific represents a rapidly emerging growth region, driven by increasing health consciousness, urbanization, and gradual adoption of global superfood trends across China, India, and Southeast Asia, although overall consumption remains at an early development stage compared to Western markets.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The fragmented global baobab market lacks a single dominant manufacturer across its unintegrated tiers of African producers, European processors, and specialty suppliers. Within this competitive framework, Nexira stands out as a primary market leader, leveraging a vertically integrated supply chain that bridges sustainable wild harvesting operations in Africa with centralized manufacturing facilities in France. The company’s premium inavea BAOBAB ACACIA portfolio commands a strong competitive advantage, backed by third-party organic, carbon-neutral, and Fair for Life ethical sourcing credentials

The primary African producer tier consists of companies like Afriplex Pty Ltd., Organic Africa, Aduna Ltd., B’Ayoba (Pvt) Ltd, Baobab Products Mozambique, and BFCS, which supply raw and semi-processed ingredients to global markets. Meanwhile, specialty chemical giants Symrise AG and Evonik Industries AG operate at the advanced formulation tier, blending premium baobab oils and extracts into luxury cosmetic systems. Mainstream success in this sector strictly rewards deep supply chain integration, ethical sourcing compliance, and reliable quality metrics.

The Major Players In The Industry

- Afriplex Pty Ltd.

- Baobab Foods LLC

- BFCS – Baobab Fruit Company Senegal

- Mighty Baobab Ltd

- Woodland Foods

- Henry Lamotte Oils GmbH

- Nexira

- Organic Africa

- Aduna Ltd.

- All Organic Treasures GmbH

- B’Ayoba (Pvt) Ltd

- Eco Products (PTY) Ltd

- Vytrus Biotech

- Huiles Bertin

- Evonik Industries AG

- Symrise AG

- Shree Sai Biotech

- Baobab Products Mozambique

- Greentech Group

- Racines sas

- Other Key Players

Key Development

- In March 2026, Evonik updated its Beauty & Personal Care strategic portfolio, placing an explicit commercial emphasis on bio-based actives. This realignment expands the distribution architecture for its upcycled, circular-economy ingredient lines, catering directly to the clean beauty and sustainable cosmetics market.

- In May 2026, Nexira presented its latest sustainability data validated by the USDA Global Branded Food Products Database, confirming its integrated tree-to-table transparency and organic certifications for baobab pulp powders.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 32.9 Mn |

| Forecast Revenue (2035) | USD 95.0 Mn |

| CAGR (2026-2035) | 11.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Baobab Fruit Powder, Baobab Pulp, Baobab Oil, Baobab Extracts, Baobab Leaves, Others), By Nature (Organic, Conventional), By Form (Powder, Liquid, Capsules & Tablets, Oil, Others), By Application (Food & Beverages, Nutritional Supplements, Cosmetics & Personal Care, Pharmaceuticals, Animal Feed, Others), By Distribution Channel (Business-to-Business (B2B), Business-to-Consumer (B2C)) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Afriplex Pty Ltd., Baobab Foods LLC, BFCS – Baobab Fruit Company Senegal, Mighty Baobab Ltd, Woodland Foods, Henry Lamotte Oils GmbH, Nexira, Organic Africa, Aduna Ltd., All Organic Treasures GmbH, B’Ayoba (Pvt) Ltd, Eco Products (PTY) Ltd, Vytrus Biotech, Huiles Bertin, Evonik Industries AG, Symrise AG, Shree Sai Biotech, Baobab Products Mozambique, Greentech Group, Racines sas, Other Key Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |