Global Automotive Filters Market Size, Share, Growth Analysis By Filter (Air Filters, Oil Filters, Fuel Filters, Cabin Air Filters, Others), By Material (Cellulose, Synthetic, Activated Carbon, Electrostatic, Others), By Vehicle Type (Passenger Cars, Commercial Vehicles, Two-Wheelers), By Propulsion (Internal Combustion Engine (ICE) Vehicles, Electric Vehicles (EVs), Hybrid Vehicles (HEVs/PHEVs)), By Sales Channel (Aftermarket, OEM), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 178370

- Number of Pages: 281

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

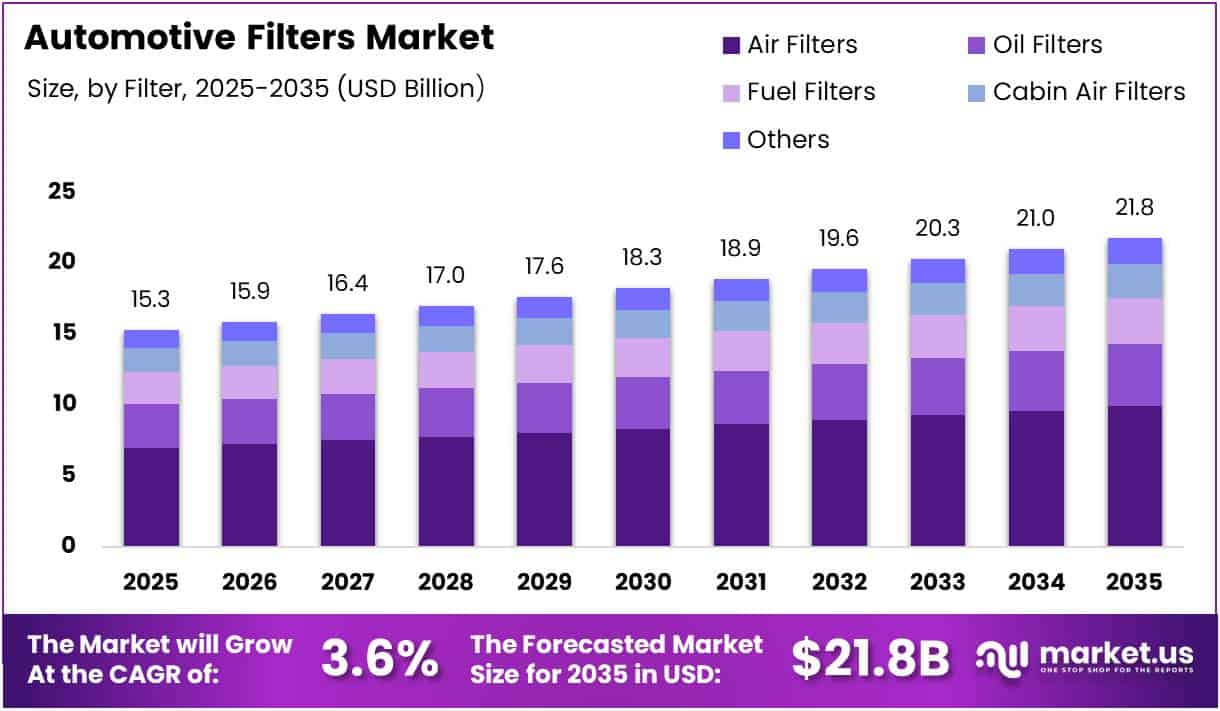

The Global Automotive Filters Market size is expected to be worth around USD 21.8 Billion by 2035 from USD 15.3 Billion in 2025, growing at a CAGR of 3.6% during the forecast period 2026 to 2035.

The automotive filters market covers a broad range of filtration products designed to remove contaminants from engine air, oil, fuel, and cabin airflow in vehicles. These components are essential for maintaining engine health, reducing emissions, and ensuring passenger comfort. Moreover, they are critical across both original equipment manufacturing and aftermarket distribution channels globally.

Automotive filters are classified by function, material, vehicle type, propulsion system, and sales channel. Each category addresses a specific filtration need within a vehicle’s operating system. Consequently, product innovation in filter media, design efficiency, and service life has become a key competitive factor for manufacturers operating in this space.

Rising vehicle ownership levels and longer fleet lifespans are driving steady replacement filter demand worldwide. As vehicles remain in service longer, periodic filter maintenance becomes more frequent. Additionally, expanding commercial logistics fleets across emerging economies are generating higher consumption of heavy-duty filtration products, particularly in the oil and air filter categories.

Governments across North America, Europe, and Asia Pacific continue to tighten emission regulations for both new and in-service vehicles. These standards directly raise performance requirements for filtration systems. Therefore, manufacturers are actively investing in advanced filter media, smart sensor integration, and lightweight designs to meet compliance requirements and satisfy evolving customer expectations.

According to the U.S. Department of Energy, replacing a clogged air filter can improve gas mileage by up to 10% in older carbureted vehicles, delivering measurable fuel savings. According to Champion Auto Parts, oil filters should typically be replaced every 10,000 km for petrol vehicles and every 15,000 km for diesel vehicles, reinforcing stable aftermarket demand.

According to HEPA filtration standards, automotive particulate filters must achieve at least 99.97% efficiency at 0.3 µm to meet minimum retention benchmarks. Additionally, according to Mann-Filter, cabin air filters remove up to 90% of harmful particulates and are recommended for replacement approximately every 15,000 km or once per year, supporting growing aftermarket volumes.

Key Takeaways

- The Global Automotive Filters Market was valued at USD 15.3 Billion in 2025 and is projected to reach USD 21.8 Billion by 2035.

- The market is expected to grow at a CAGR of 3.6% during the forecast period 2026 to 2035.

- By Filter, Air Filters dominate the segment with a market share of 45.7% in 2025.

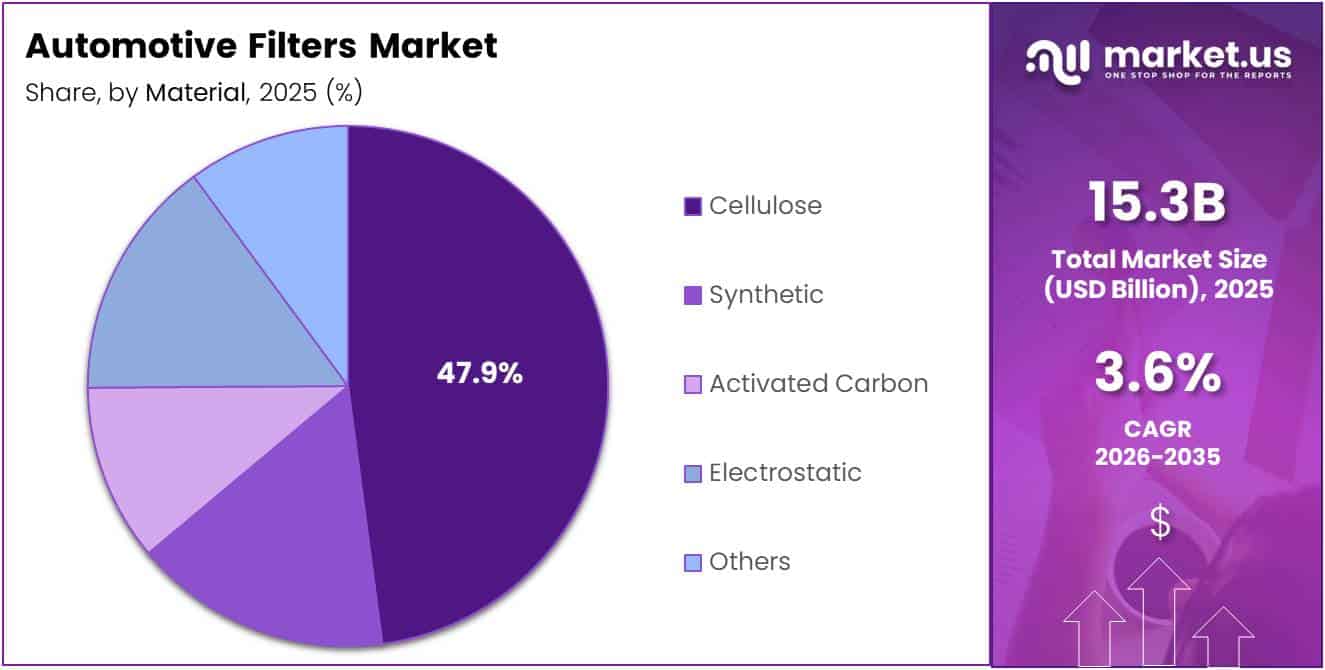

- By Material, Cellulose leads the segment with a 47.9% share in 2025.

- By Vehicle Type, Passenger Cars account for the largest share at 62.8% in 2025.

- By Propulsion, Internal Combustion Engine (ICE) Vehicles dominate with a 71.2% share in 2025.

- By Sales Channel, the Aftermarket segment holds the largest share at 78.5% in 2025.

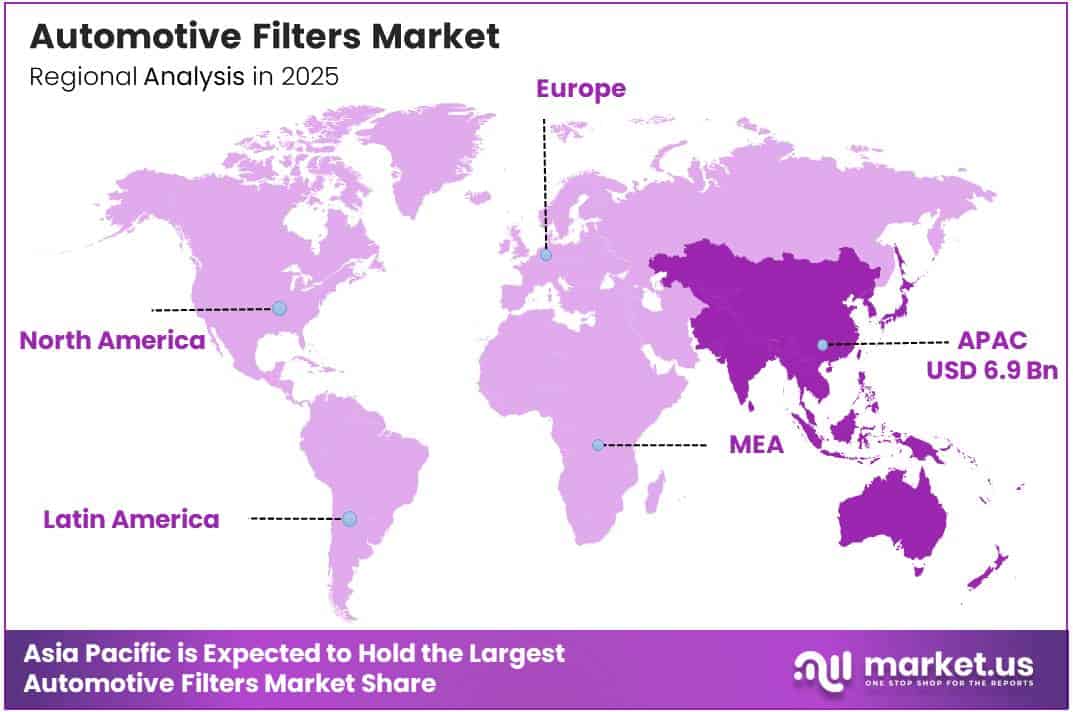

- Asia Pacific is the dominating region, holding a 45.70% market share valued at USD 6.9 Billion in 2025.

By Filter Analysis

Air Filters dominate with 45.7% due to their widespread use across all vehicle types and essential role in engine protection and emission compliance.

In 2025, Air Filters held a dominant market position in the By Filter segment of the Automotive Filters Market, with a 45.7% share. Their universal application across passenger cars, commercial vehicles, and two-wheelers, combined with mandatory periodic replacement cycles, makes them the highest-volume filter category in both OEM and aftermarket channels.

Oil Filters represent a consistently high-demand segment supported by mandatory oil change intervals across petrol and diesel vehicles. Their critical role in removing metallic and organic contaminants from engine oil directly supports engine durability. Moreover, growing commercial vehicle fleet operations continue to sustain strong and predictable oil filter replacement volumes globally.

Fuel Filters maintain steady demand by protecting fuel injection systems and combustion chambers from impurities. Regular replacement cycles, particularly in diesel-powered vehicles, underpin consistent aftermarket sales. Additionally, concerns over fuel quality in developing markets are keeping this segment relevant and supporting its stable contribution to overall filter revenues.

Cabin Air Filters are gaining significant traction, driven by rising passenger awareness of indoor air quality inside vehicles. Premium and mid-range vehicles increasingly feature advanced anti-allergen and anti-viral filtration options. Consequently, this sub-segment is expected to grow at an above-average pace as health-conscious consumers prioritize cleaner cabin environments during the forecast period.

Others sub-segment covers specialty products such as transmission filters and hydraulic filters for specific vehicle applications. Although smaller in volume, this category benefits from demand in heavy-duty and off-highway vehicle sectors. Therefore, it continues to make a meaningful contribution to total market revenues, particularly in industrial and fleet-oriented applications.

By Material Analysis

Cellulose dominates with 47.9% due to its cost-effectiveness, wide availability, and proven performance across standard engine filtration applications.

In 2025, Cellulose held a dominant market position in the By Material segment of the Automotive Filters Market, with a 47.9% share. Its low production cost, compatibility with conventional engine air and oil filters, and established supply chains make it the most widely used filter media across both OEM production lines and aftermarket replacement products.

Synthetic filter media is gaining increasing adoption due to its superior dirt-holding capacity, longer service life, and enhanced filtration efficiency compared to cellulose alternatives. Manufacturers are increasingly offering synthetic-based products for premium and high-performance vehicle applications. Moreover, growing awareness of extended-life filtration benefits is encouraging consumers to shift toward synthetic options over time.

Activated Carbon media is specifically used in cabin air filters to adsorb gaseous pollutants, odors, and volatile organic compounds from incoming air. Demand is rising as vehicle occupant health and air quality standards become more stringent. Additionally, urban air pollution concerns are motivating automakers to include activated carbon layers as standard features in cabin filtration systems.

Electrostatic filter media uses charged fibers to capture fine particulates with high efficiency, making it suitable for premium cabin and engine air applications. While currently a smaller segment, its adoption is increasing in premium and electric vehicle models. Consequently, technological improvements in electrostatic filtration are expected to broaden its application scope during the forecast period.

Others includes glass fiber, foam, and composite media used in specialized filtration environments. These materials serve niche industrial and heavy-duty automotive applications where standard media may not meet performance demands. Therefore, this category contributes incrementally to overall market volume, particularly through heavy-duty and off-road vehicle filtration requirements.

By Vehicle Type Analysis

Passenger Cars dominate with 62.8% due to large global fleet size and frequent filter replacement requirements.

In 2025, Passenger Cars held a dominant market position in the By Vehicle Type segment of the Automotive Filters Market, with a 62.8% share. This segment includes Hatchbacks, Sedans, SUVs, and MPVs, all of which generate consistent demand for air, oil, fuel, and cabin filters through both OEM installation and regular aftermarket replacement cycles worldwide.

Commercial Vehicles represent a high-value segment driven by the expansion of logistics, freight, and public transport fleets globally. This sub-segment covers Light Commercial Vehicles (LCVs), Medium Commercial Vehicles (MCVs), and Heavy Commercial Vehicles (HCVs). Moreover, their intensive usage cycles and stricter maintenance schedules result in significantly higher filter consumption rates compared to standard passenger car applications.

Two-Wheelers, including Motorcycles and Scooters, form a growing filtration market, especially across Asia Pacific and Latin America where two-wheeler ownership continues to expand rapidly. Although individual filter values are lower, the sheer volume of two-wheelers in service drives significant cumulative demand. Consequently, this sub-segment presents meaningful growth opportunities for aftermarket filter suppliers in high-density urban markets.

By Propulsion Analysis

Internal Combustion Engine (ICE) Vehicles dominate with 71.2% due to continued global ICE vehicle production and extensive existing fleet base.

In 2025, Internal Combustion Engine (ICE) Vehicles held a dominant market position in the By Propulsion segment of the Automotive Filters Market, with a 71.2% share. ICE vehicles require the full range of engine air, oil, and fuel filters, ensuring consistent high-volume demand across both OEM assembly and the large global aftermarket replacement network.

Electric Vehicles (EVs) present a shifting demand profile, as they do not require conventional engine oil or fuel filters. However, EV adoption is driving significant growth in cabin air filtration, particularly HEPA-grade and activated carbon filters. Moreover, battery thermal management and HVAC filtration requirements are creating new product development opportunities specific to the EV segment.

Hybrid Vehicles (HEVs/PHEVs) retain the need for most traditional filtration products since they continue to operate combustion engines under certain driving conditions. Additionally, their more complex powertrain systems may introduce additional filtration requirements. Consequently, this sub-segment supports steady filter demand as hybrid adoption grows across major global automotive markets during the forecast period.

By Sales Channel Analysis

Aftermarket dominates with 78.5% due to regular filter replacement cycles and extensive distribution networks serving vehicle maintenance needs.

In 2025, Aftermarket held a dominant market position in the By Sales Channel segment of the Automotive Filters Market, with a 78.5% share. The large installed base of aging vehicles worldwide, combined with mandatory maintenance schedules, ensures a continuous and predictable stream of replacement filter demand through service centers, retail stores, and online distribution platforms.

OEM channels supply original equipment filters during vehicle production and through authorized dealership networks. These channels emphasize quality assurance and warranty compliance. However, premium pricing limits OEM market share compared to cost-effective aftermarket alternatives increasingly accepted by consumers for non-critical maintenance components.

Key Market Segments

By Filter

- Air Filters

- Oil Filters

- Fuel Filters

- Cabin Air Filters

- Others

By Material

- Cellulose

- Synthetic

- Activated Carbon

- Electrostatic

- Others

By Vehicle

- Passenger Cars

- Hatchbacks

- Sedans

- SUVs

- MPVs

- Commercial Vehicles

- Light Commercial Vehicles (LCVs)

- Medium Commercial Vehicles (MCVs)

- Heavy Commercial Vehicles (HCVs)

- Two-Wheelers

- Motorcycle

- Scooter

By Propulsion

- Internal Combustion Engine (ICE) Vehicles

- Electric Vehicles (EVs)

- Hybrid Vehicles (HEVs/PHEVs)

By Sales Channel

- Aftermarket

- OEM

Drivers

Stringent Emission Norms and Growing Vehicle Fleet Age Drive Strong Demand for Automotive Filtration Systems

Increasingly strict emission regulations across major markets such as the European Union, the United States, and China are mandating higher-performance filtration systems in both new and in-service vehicles. These standards require filters that deliver greater contaminant removal efficiency and longer service reliability. Consequently, automakers and fleet operators are prioritizing quality filtration components to maintain regulatory compliance.

The global vehicle fleet continues to grow while the average age of in-service vehicles rises steadily. Older vehicles require more frequent filter replacements to maintain performance and fuel efficiency. Therefore, this aging fleet dynamic directly translates into sustained aftermarket demand for air, oil, fuel, and cabin filters across all major vehicle categories worldwide.

Rapid expansion of commercial vehicle fleets, particularly in logistics, e-commerce, and freight transport sectors, is generating higher consumption of heavy-duty filtration products. Additionally, these vehicles operate under intensive duty cycles that accelerate filter wear and shorten replacement intervals. Moreover, growing infrastructure investment in emerging economies is further supporting fleet growth and boosting demand for commercial-grade automotive filter products.

Restraints

Vehicle Electrification and Long-Life Filter Technologies Pose Challenges to Traditional Filter Replacement Demand

The accelerating transition toward battery electric vehicles is reducing long-term demand for conventional engine-related filters, including oil, fuel, and engine air filters. As EV penetration rates rise in major markets, the addressable market for these traditional filter categories will progressively contract. Consequently, manufacturers face growing pressure to diversify product portfolios toward EV-compatible filtration solutions.

Advances in long-life filtration technologies are extending service intervals for key filter types, including synthetic oil filters and extended-service air filters. While beneficial for vehicle owners, these innovations directly reduce replacement frequency and compress aftermarket sales volumes. Therefore, higher product durability is creating a structural headwind for revenue growth in the traditional replacement filter segment over the medium term.

Additionally, cost sensitivity among vehicle owners in price-driven markets often leads to delayed or skipped filter maintenance, further reducing effective demand volumes. In lower-income regions, the prioritization of essential repairs over preventive maintenance limits aftermarket filter sales. Moreover, the availability of low-cost, non-branded filter alternatives continues to pressure the revenue margins of established filtration product manufacturers globally.

Growth Factors

Smart Filtration Technologies and Advanced Cabin Air Solutions Open New Revenue Streams for Market Participants

Integration of smart filter monitoring sensors capable of detecting filter saturation levels in real time is emerging as a significant growth opportunity. These sensors enable predictive maintenance systems that alert drivers before performance degrades. Consequently, demand for sensor-enabled filtration solutions is expected to grow rapidly, particularly in premium passenger vehicles and connected commercial fleet applications.

Growing consumer awareness of vehicle cabin air quality is driving strong adoption of advanced cabin air filters with anti-allergen and anti-viral filtration capabilities. Health-conscious consumers increasingly demand cleaner in-cabin air environments, especially in urban areas with high pollution levels. Moreover, post-pandemic sensitivity to airborne pathogens has further accelerated interest in high-efficiency cabin filtration across all vehicle segments globally.

Sustainability initiatives are creating demand for eco-friendly and recyclable filter media as both automakers and consumers focus on reducing environmental impact. Development of biodegradable filter materials and recycling programs for used filters is gaining traction. Therefore, manufacturers investing in green filtration solutions are well-positioned to capture growing market share among environmentally conscious OEM partners and retail consumers.

Emerging Trends

HEPA Cabin Filtration, Extended-Life Products, and Lightweight Designs Are Reshaping the Automotive Filters Market

A clear shift toward High-Efficiency Particulate Air (HEPA) cabin filtration is visible in the premium vehicle segment, where manufacturers are integrating hospital-grade air purification standards into passenger compartments. This trend is being accelerated by rising urban air pollution levels and stronger consumer demand for healthier in-vehicle environments. Consequently, HEPA-grade cabin filters are transitioning from luxury features to expected standards.

Automakers and aftermarket suppliers are increasingly focusing on extended-life oil and fuel filters with enhanced dirt-holding capacity and longer service intervals. These products reduce maintenance frequency and total ownership costs, making them attractive to both fleet operators and individual consumers. Moreover, technological improvements in synthetic and composite filter media are enabling these performance gains without compromising filtration efficiency or engine protection.

OEM engineering teams are prioritizing lightweight and compact filtration system designs to improve vehicle efficiency and meet stringent fuel economy targets. Reducing filter assembly weight directly contributes to overall vehicle mass reduction strategies. Additionally, compact designs allow greater flexibility in engine compartment packaging, making next-generation filtration solutions compatible with the increasingly space-constrained architectures of modern vehicles, including hybrids and EVs.

Regional Analysis

Asia Pacific Dominates the Automotive Filters Market with a Market Share of 45.70%, Valued at USD 6.9 Billion

Asia Pacific leads the global automotive filters market, holding a dominant share of 45.70% and valued at USD 6.9 Billion in 2025. The region’s dominance is driven by its massive vehicle production base in China, Japan, South Korea, and India, combined with rapidly growing vehicle ownership rates across Southeast Asia. Additionally, a large aging vehicle parc sustains high-volume aftermarket filter demand across the region.

North America Automotive Filters Market Trends

North America represents a mature and high-value market for automotive filters, supported by a large fleet of aging personal and commercial vehicles. Stringent EPA and CARB emission regulations continue to drive demand for high-performance filtration products. Moreover, strong consumer preference for branded aftermarket replacement filters and a well-established distribution network contribute to sustained revenue generation across the United States and Canada.

Europe Automotive Filters Market Trends

Europe maintains a significant market share driven by rigorous Euro emission standards and strong automotive manufacturing activity in Germany, France, and Italy. Demand for advanced cabin air filtration and eco-friendly filter media is particularly high in this region. Consequently, European manufacturers and suppliers are at the forefront of sustainable filtration innovation, including recyclable media and extended-service filter product development.

Middle East and Africa Automotive Filters Market Trends

The Middle East and Africa region is witnessing steady growth in automotive filter demand, supported by expanding vehicle ownership and growing logistics infrastructure investment. Harsh environmental conditions, including high dust levels and extreme temperatures, create elevated filter replacement frequencies compared to other regions. Therefore, air filtration products in particular see strong demand across Gulf Cooperation Council countries and sub-Saharan African markets.

Latin America Automotive Filters Market Trends

Latin America presents growing opportunities driven by rising vehicle parc numbers in Brazil and Mexico and increasing awareness of preventive vehicle maintenance. Economic growth in key markets is boosting demand for both OEM and aftermarket filter products. Moreover, government initiatives targeting fleet modernization and emission control in urban transport systems are further supporting filter market development across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Atmus Filtration Technologies has established itself as a focused, independent filtration specialist following its separation from Cummins. The company serves heavy-duty on-highway, off-highway, and industrial markets with a broad portfolio of air, fuel, and lube filtration products. Its recent acquisition of Koch Filter Corp for $450 million demonstrates a clear strategy to expand product scope and market coverage.

Denso is a globally recognized automotive components manufacturer with significant filtration operations spanning air, oil, and cabin filter categories. The company leverages its deep OEM relationships with leading Japanese and global automakers to maintain strong original equipment supply positions. Moreover, Denso continues to invest in advanced cabin air filtration technologies aligned with growing vehicle electrification and occupant air quality trends.

Donaldson Company is a diversified industrial and transportation filtration leader with a strong presence across engine and aftermarket filter segments. Its strategic acquisition of Filtration Group’s Facet Filtration business for approximately $820 million reflects its commitment to expanding into adjacent filtration markets. Donaldson’s broad global distribution network and engineering expertise position it as a formidable competitor across multiple filtration end markets.

Freudenberg operates in the automotive filtration space through its filtration division, supplying advanced filter media and finished filter products to OEM and aftermarket customers globally. The company’s acquisition of all remaining shares in Japan Vilene Company strengthens its technical capabilities in nonwoven filter media manufacturing. Additionally, Freudenberg’s focus on sustainability and next-generation filter materials supports its long-term competitive positioning in evolving vehicle markets.

Key Players

- Atmus Filtration Technologies

- Denso

- Donaldson Company

- Freudenberg

- Hengst Filtration

- Mahle

- Mann+Hummel

- Parker Hannifin

- Purflux

- Robert Bosch

Recent Developments

- February 2026 – Donaldson Company Inc has entered into a definitive agreement to acquire Filtration Group’s Facet Filtration business in an all-cash transaction valued at approximately US$820 million, expanding the company’s aerospace and specialty automotive filtration capabilities.

- November 2025 – Atmus Filtration Technologies has agreed to acquire Koch Filter Corp. for $450 million in cash, strengthening its position in the North American filtration market and expanding its aftermarket presence.

- November 2025 – Parker Hannifin Corporation is acquiring Filtration Group Corporation in a US$9.25 billion cash transaction, significantly expanding its motion and control technologies portfolio with comprehensive filtration solutions.

- November 2025 – Freudenberg acquires all remaining shares in Japan Vilene Company, consolidating its presence in Asian markets and strengthening manufacturing capabilities for automotive and industrial filtration applications.

Report Scope

Report Features Description Market Value (2025) USD 15.3 Billion Forecast Revenue (2035) USD 21.8 Billion CAGR (2026-2035) 3.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Filter (Air Filters, Oil Filters, Fuel Filters, Cabin Air Filters, Others), By Material (Cellulose, Synthetic, Activated Carbon, Electrostatic, Others), By Vehicle Type (Passenger Cars, Commercial Vehicles, Two-Wheelers), By Propulsion (Internal Combustion Engine (ICE) Vehicles, Electric Vehicles (EVs), Hybrid Vehicles (HEVs/PHEVs)), By Sales Channel (Aftermarket, OEM) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Atmus Filtration Technologies, Denso, Donaldson Company, Freudenberg, Hengst Filtration, Mahle, Mann+Hummel, Parker Hannifin, Purflux, Robert Bosch Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Atmus Filtration Technologies

- Denso

- Donaldson Company

- Freudenberg

- Hengst Filtration

- Mahle

- Mann+Hummel

- Parker Hannifin

- Purflux

- Robert Bosch

Our Clients

- 178370

- Feb 2026