Quick Navigation

Report Overview

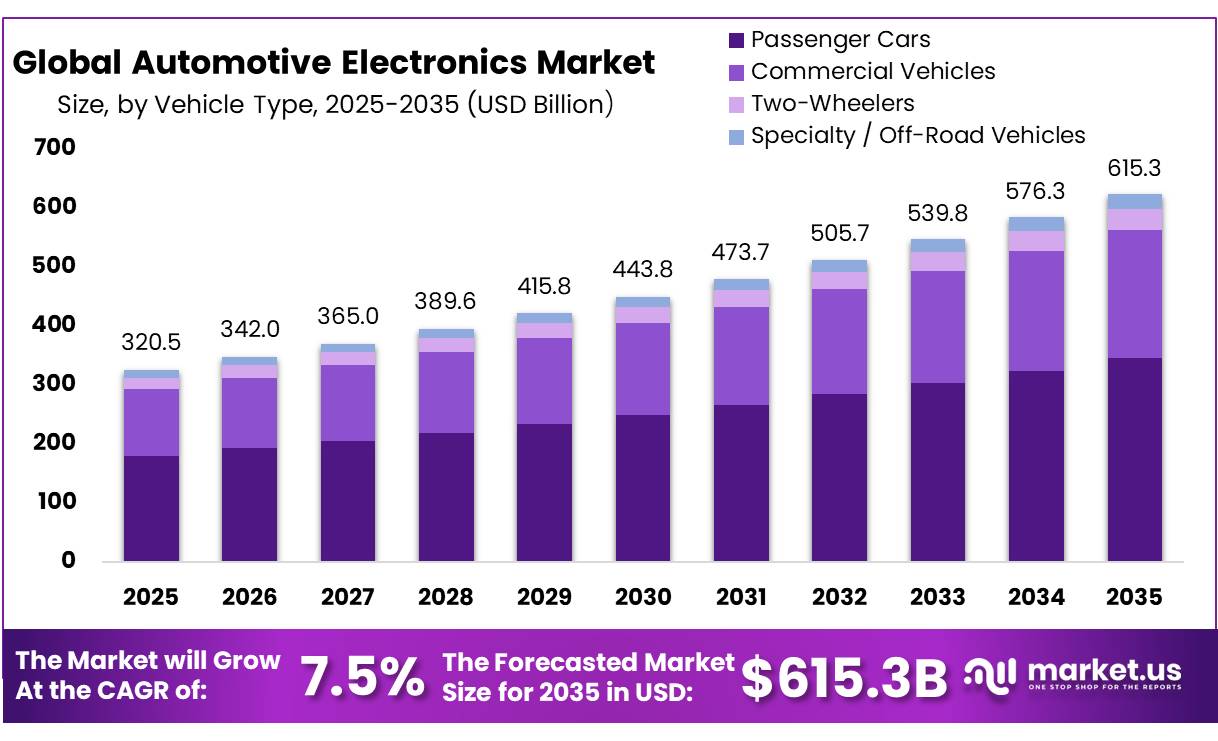

The Global Automotive Electronics Market is projected to reach around USD 615.3 billion by 2035, rising from USD 320.5 billion in 2025, and expanding at a CAGR of 7.5% over the 2025–2035 forecast period.

North America held a dominant market position, capturing more than a 35.6% share, holding USD 30.19 billion in revenue.

The industrial scenario strengthened during 2025 as electrification and digital features expanded.

- The International Energy Agency reported that global electric-car sales exceeded 20 million units in 2025, rising 20% and representing 25% of total car sales. Nearly 22 million electric cars were produced during the year, more than 25% above 2024.

These vehicles require battery-management systems, inverters, onboard chargers, power semiconductors and advanced thermal-control electronics, creating a broad manufacturing base for component suppliers.

Semiconductor availability remains central to industry performance. The Semiconductor Industry Association stated in February 2026 that worldwide semiconductor sales reached USD 791.7 billion in 2025, increasing 25.6%. Although this total covers multiple end-use industries, it reflects expanding capacity and investment in logic, memory, analog and power devices that support automotive applications. In Europe, battery-electric cars represented 17.4% of new registrations in 2025, while hybrid-electric models held 34.5%, supporting continued demand for electronic powertrain and control systems.

Safety regulation is another major driver. European Union rules applying to all new vehicles from July 2024 require technologies such as intelligent speed assistance, reversing detection, driver-attention warnings and emergency-stop signals. The measures are expected to save more than 25,000 lives and prevent at least 140,000 serious injuries by 2038. In the United States, automatic emergency braking will become mandatory for new passenger cars and light trucks from September 2029. Future opportunities will therefore develop around ADAS, vehicle connectivity, centralized computing, battery intelligence, over-the-air software, cybersecurity and wide-bandgap power semiconductors at scale.

Global Automotive Electronics Market Segmentation

Application Analysis

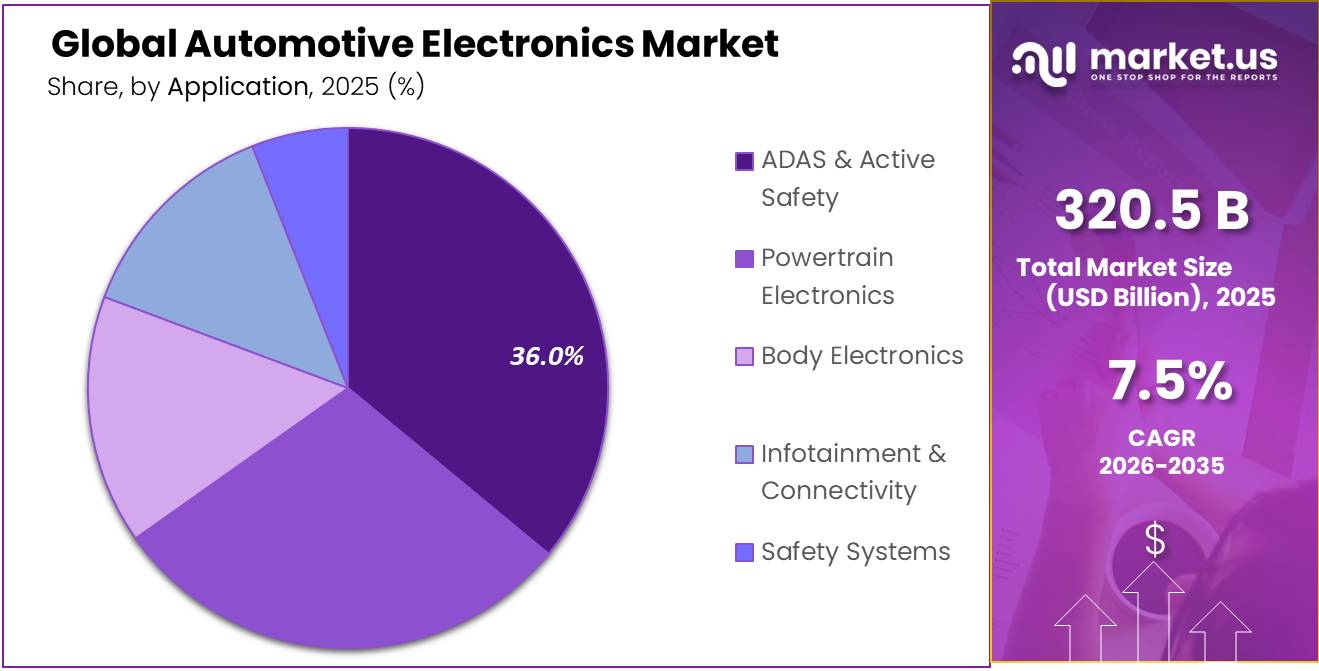

ADAS & Active Safety leads with 36.0% as automakers focus on accident prevention and driver protection.

In 2025, ADAS & Active Safety held a dominant market position, capturing more than a 36.0% share. In December 2025, demand remained strong as manufacturers expanded the use of cameras, radar, ultrasonic sensors, electronic control units, and warning systems. These technologies support functions such as lane assistance, blind-spot detection, adaptive cruise control, parking support, and emergency braking. Their wider adoption was encouraged by tighter vehicle-safety rules, rising consumer awareness, and the growing use of connected systems. Automakers also used these solutions to improve driving comfort and reduce human error.

Powertrain Electronics emerged as the growing segment in 2026. Demand increased for battery-management systems, inverters, motor controllers, transmission controls, and engine-management units. Growth in electric and hybrid vehicles, together with the need for energy efficiency and lower emissions, supported installation across passenger and commercial vehicles.

Component Analysis

Electronic Control Units and Domain Control Units lead with 44% as vehicles become more connected, automated, and software-driven.

In 2025, Electronic Control Units (ECU) / Domain Control Units (DCU) held a dominant market position, capturing more than a 44% share. In December 2025, demand remained strong as automakers combined powertrain, safety, infotainment, comfort, and connectivity functions within electronic architectures. These units process data, coordinate vehicle systems, and support faster communication between components. Their ability to reduce wiring complexity, improve system response, and enable software updates strengthened their use across passenger and commercial vehicles. Rising adoption of electric vehicles and advanced driver-assistance features further supported the segment.

Sensors & Cameras emerged as the growing segment in 2026. Their use expanded in parking assistance, lane monitoring, collision warning, driver observation, and cabin control. Increasing demand for safer vehicles, better visibility, and real-time environmental data continued to support their integration across vehicle platforms.

Vehicle Type Analysis

Passenger Cars lead with 56.20% as buyers prefer safer, connected, and feature-rich vehicles.

In 2025, Passenger Cars held a dominant market position, capturing more than a 56.20% share. In December 2025, the segment remained strong as automakers expanded the use of electronic control units, infotainment systems, digital displays, sensors, cameras, and driver-assistance technologies. Passenger cars are produced in high volumes and receive frequent upgrades in comfort, safety, connectivity, and energy management. Growing demand for electric and hybrid models also increased the need for battery controls, power electronics, and smart cabin systems. These factors kept passenger cars at the center of automotive electronics demand.

Commercial Vehicles emerged as the growing segment in 2026. Fleet operators adopted telematics, electronic braking, navigation, engine controls, driver-monitoring systems, and predictive-maintenance tools. These technologies supported better route planning, lower downtime, safer operations, improved fuel use, and more efficient management of trucks, vans, and buses across markets.

Propulsion Analysis

ICE vehicles dominate with 66.60% as established production and service networks continue to support broad electronic demand.

In 2025, ICE (Internal Combustion Engine) held a dominant market position, capturing more than a 66.60% share. In December 2025, the segment remained central to automotive electronics demand because petrol and diesel vehicles continued to use engine control units, transmission modules, fuel-injection controls, emission sensors, ignition systems, infotainment, and safety technologies. Mature manufacturing systems, widespread servicing facilities, and a large installed vehicle base supported component demand. Automakers also continued improving fuel efficiency, diagnostics, and emission management through electronics, helping the segment retain its leading position.

EV & Hybrid Electric Vehicles (HEV / PHEV) Platforms emerged as the fastest-growing segment in 2026. Their expansion increased demand for battery-management systems, inverters, motor controllers, charging modules, thermal controls, and safety electronics. Rising electrification and software integration continued strengthening this segment across passenger and commercial vehicle platforms.

Sales Analysis

OEM sales lead with 61.30% as automakers rely on factory-fitted electronics and approved supply networks.

In 2025,OEM (Original Equipment Manufacturers) held a dominant market position, capturing more than a 61.30% share. In December 2025, the channel remained strong because vehicle manufacturers sourced electronic control units, sensors, displays, power modules, safety systems, and connectivity hardware directly from approved suppliers. Factory installation supports better system integration, product testing, software compatibility, and warranty coverage. Long-term supply agreements and strict quality standards also helped OEMs maintain reliable component availability across passenger and commercial vehicle production. Growing use of advanced driver assistance, electrified powertrains, and connected cabins further supported this channel.

Aftermarket / Replacement emerged as the growing segment in 2026. Demand increased as vehicle owners replaced worn sensors, cameras, control modules, infotainment units, and electronic accessories. An aging vehicle fleet, repair needs, technology upgrades, and wider access to independent service centers supported aftermarket activity.

Key Market Segments

By Application

- ADAS/Active Safety

- Powertrain Electronics

- Body Electronics

- Infotainment & Connectivity

- Safety Systems

- Airbag Control Units

- Seatbelt Pretensioner Electronics

- Others

By Component

- Electronic Control Units (ECU) / Domain Control Units (DCU)

- Sensors & Cameras

- LiDAR Sensors

- RADAR Sensors

- Ultrasonic Sensors

- Others

- Power Electronics

- Inverters & Converters

- On-Board Chargers (OBC)

- Others

- Displays & Interfaces

- Microcontrollers (MCUs) & Semiconductors

- Others

By Vehicle Type

- Passenger Cars

- Sedans

- SUVs / Crossovers

- Hatchbacks

- Commercial Vehicles

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV) / Trucks

- Buses & Coaches

- Two-Wheelers

- Specialty / Off-Road Vehicles

By Propulsion

- ICE (Internal Combustion Engine)

- EV & Hybrid Electric Vehicles (HEV / PHEV)

By Sales

- OEM

- Aftermarket / Replacement

- Authorized Dealer Networks

Drivers

Restraints

Opportunity

Challenge

Geopolitical Impact Analysis

Disruptions in the supply chain and reliance on semiconductors affecting the automotive electronics sector.

Geopolitical conflicts, trade policies, and disruptions within the value chain related to the manufacture of semiconductors, raw materials, and automobiles contribute to the dynamics of the international automobile electronics market. The existence of geopolitical conflicts such as the war between Russia and Ukraine and escalating trade relations between key economies has made the market volatile due to fluctuations in energy prices and logistics.

The car manufacturing industry continues to be very reliant on semiconductors in areas such as ADAS, infotainment, power electronic products, and even electric vehicles. This is because there have been disruptions within the manufacturing process and shipping routes that have made it difficult for automotive OEMs and their respective suppliers to source and manufacture electronic components. Moreover, material limitations due to exportation laws are creating further pressures on car manufacturers.

In addition, the industry is also seeing a rising interest from the government in supporting domestic production of semiconductors, development of the EV eco-system, and building of regional supply chains in North America, Europe, and Asia Pacific. With increasing investment in chip production facilities, battery manufacturing plants, and automotive electronics manufacturing, there will be reduced geopolitical risks in the long run.

Regional Analysis

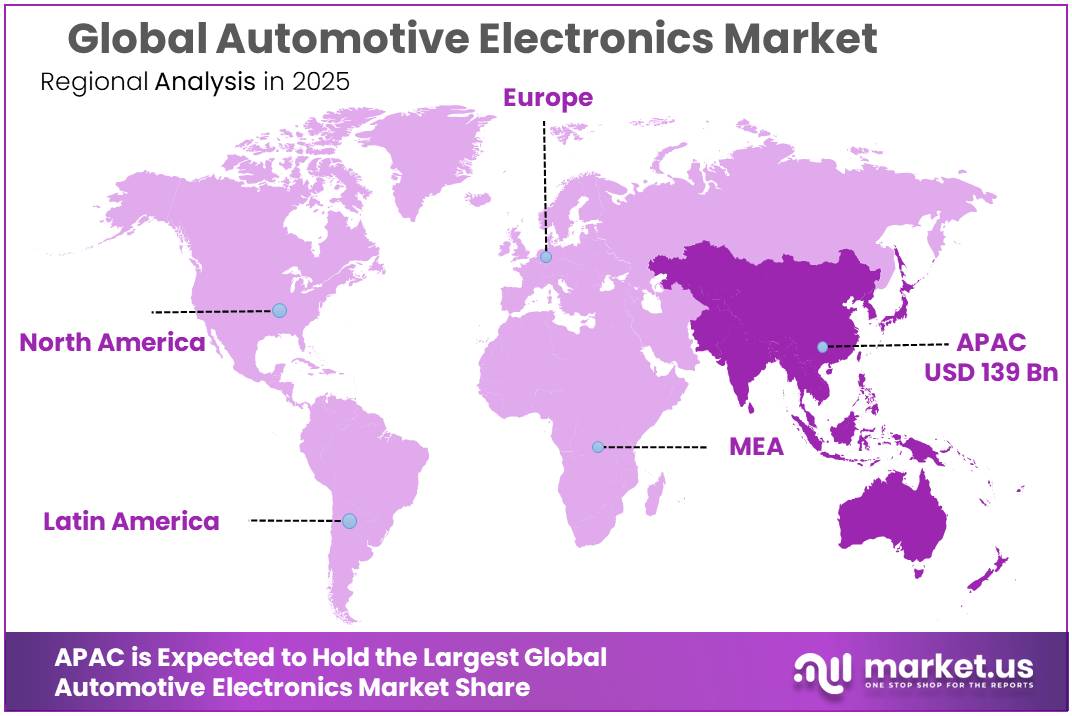

Asia-Pacific: The Dominator (43.4% Market Share)

Asia-Pacific has a market share of 43.4% in the Automotive Electronics Market, which amounts to USD 139.0 billion. This dominance can be attributed to the mass manufacturing of automobiles in countries such as China, Japan, and South Korea, and also to the rapid penetration of advanced automotive systems such as ADAS and electronic components for EVs. Also, growth in the middle class is anticipated to fuel the sales of cars in the region with better facilities.

The region’s success is supported by the presence of a highly developed ecosystem comprising a strong supplier base, competent engineers, and governmental policies that promote the adoption of electrification and automation. In addition to this, the presence of large automobile and electronics firms in the region enables innovation and quick implementation of new technologies. Exports-oriented manufacturing and good trading conditions further ensure the domination of the region in the global automotive electronics market. The importance of Asia-Pacific in the coming decade is going to grow due to urbanization and electrification/automation.

Key Regions and Countries Covered

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The global automotive electronics market is highly competitive and moderately consolidated, driven by continuous advancements in vehicle electrification, ADAS technologies, automotive semiconductors, and connected mobility systems. Competition within the industry is primarily centered around technological innovation, software-defined vehicle platforms, power electronics integration, and strategic partnerships with automotive OEMs. Companies are increasingly investing in centralized computing architectures, AI-enabled vehicle systems, and next-generation automotive semiconductor technologies to strengthen their market position.

The market is witnessing increasing collaborations between automotive OEMs, semiconductor manufacturers, and software providers to accelerate the development of autonomous driving systems, EV architectures, and connected vehicle ecosystems. Rising investments in electric mobility, AI-driven automotive systems, and over-the-air (OTA) software technologies are further intensifying competition within the global automotive electronics industry.

Market Key Players

-

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Aptiv PLC

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Texas Instruments Inc.

- ZF Friedrichshafen AG

- Valeo S.A.

- Magna International Inc.

- Hyundai Mobis Co., Ltd.

- Panasonic Corporation

- Autoliv Inc.

- STMicroelectronics N.V.

- Lear Corporation

Key Development

January 2026: FORVIA HELLA and Analogue Devices revealed a strategic development combining an all‑electronic fuse (eFuse) IC with intelligent control software (iConF), aimed at raising efficiency and protection for future vehicle electrical architectures and zone-control concepts

March 2026: NXP Semiconductors announced the CoreRide Z248 zonal reference system, a pre‑integrated hardware/software foundation that combines 48‑V power distribution with intelligent data routing to accelerate deployment of scalable zonal E/E architectures in next‑generation vehicles.

May 2026: Microchip Technology introduced next‑generation 100/1000BASE‑T1 Single Pair Ethernet (SPE) PHYs that integrate MACsec security, Time‑Sensitive Networking (TSN) support, and functional safety features, targeting the move toward all‑Ethernet, software‑defined vehicle (SDV) architectures

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$320.5 Bn |

| Forecast Revenue (2035) | US$615.3 Bn |

| CAGR (2026-2035) | 7.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Electronic Control Units (ECUs) / Domain Controllers, Sensors & Cameras, Power Electronics, Inverters & Converters, Displays & Interfaces, Microcontrollers (MCUs) & Semiconductors, and Others), By Application (ADAS & Active Safety, Powertrain Electronics, Body Electronics, Infotainment & Connectivity, Safety Systems, and Others), By Vehicle Type (Passenger Cars, Commercial Vehicles, Two-Wheelers, and Specialty / Off-Road Vehicles), By Propulsion Type (ICE (Internal Combustion Engine) and EV & Hybrid Electric Vehicles (HEV/PHEV)), By Sales Channel (OEM (Original Equipment Manufacturer), Aftermarket / Replacement, and Authorized Dealer Networks), |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Robert Bosch GmbH,Continental AG,Denso Corporation,Aptiv PLC,Infineon Technologies AG,NXP Semiconductors N.V.,Texas Instruments Inc.,ZF Friedrichshafen AG,Valeo S.A.,Magna International Inc.,Hyundai Mobis Co., Ltd.,Panasonic Corporation,Autoliv Inc.,STMicroelectronics N.V.,Lear Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |