Quick Navigation

Report Overview

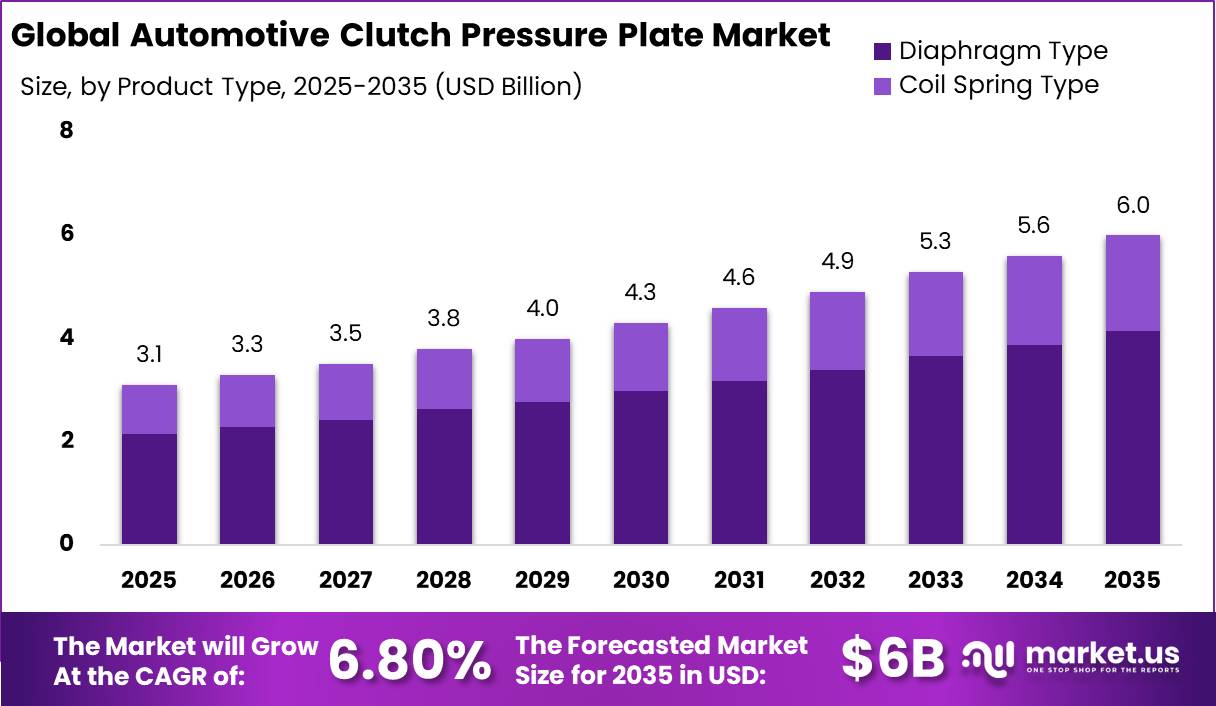

Global Automotive Clutch Pressure Plate Market size is expected to be worth around USD 6.0 Billion by 2035 from USD 3.1 Billion in 2025, growing at a CAGR of 6.80% during the forecast period 2026 to 2035.

The automotive clutch pressure plate market covers mechanical components that clamp the clutch disc against the flywheel to transmit engine torque to the drivetrain. The market spans diaphragm-type and coil spring-type pressure plates. It serves two-wheelers, passenger cars, light commercial vehicles, and medium and heavy commercial vehicles through OEM and aftermarket distribution channels.

Key Takeaways

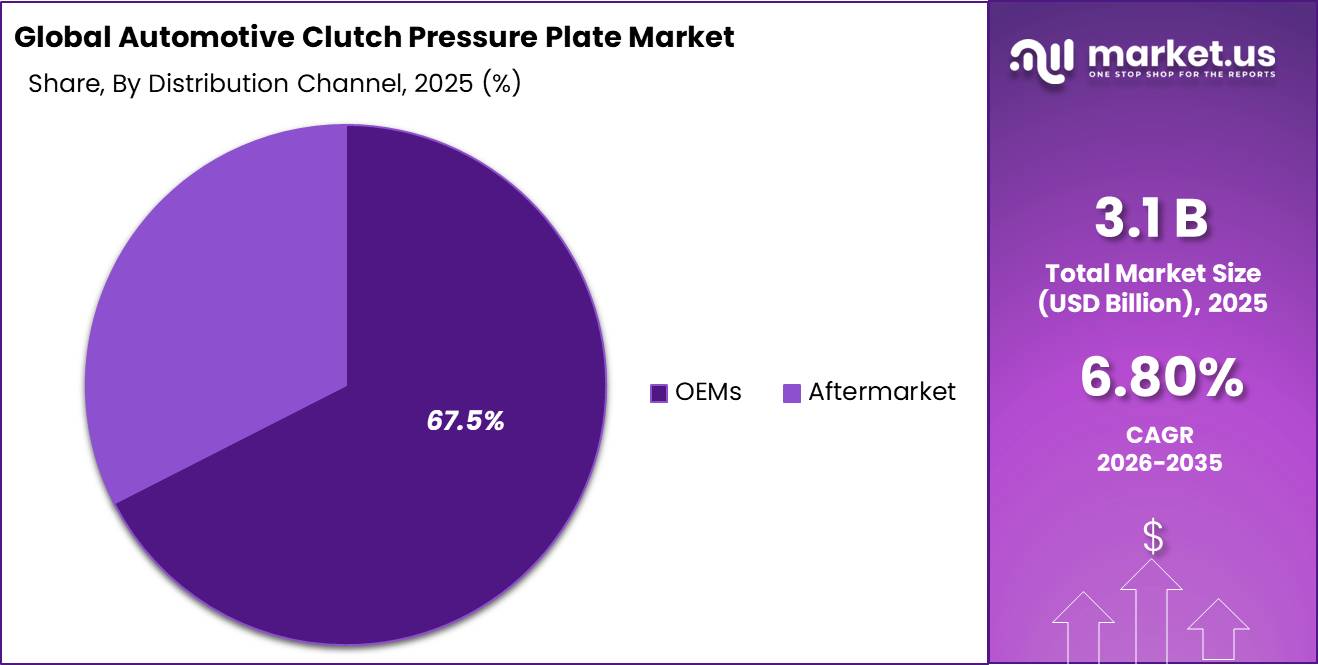

- Automotive Clutch Pressure Plate Market size in 2025 stands at USD 3.1 Billion, forecast to reach USD 6.0 Billion by 2035.

- The market grows at a CAGR of 6.80% from 2026 to 2035.

- Diaphragm Type dominates the Product Type segment with a 69.20% share.

- Passenger Car dominates the Vehicle Type segment with a 49.80% share.

- OEMs dominate the Distribution Channel segment with a 67.50% share.

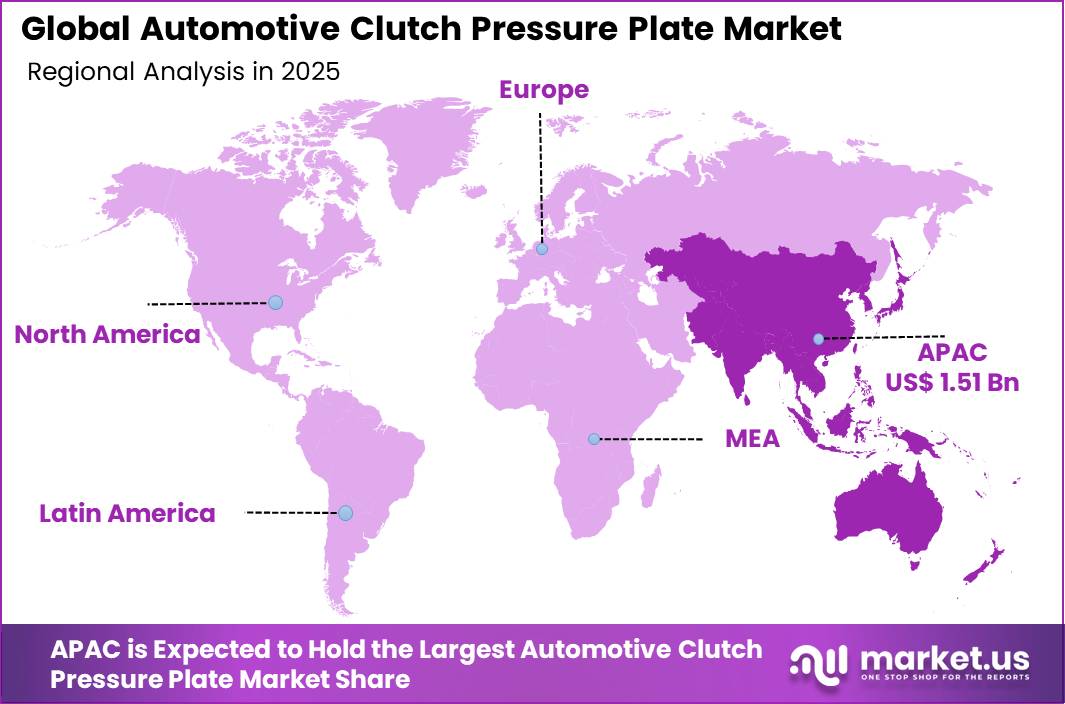

- Asia Pacific leads all regions with a 48.90% market share.

Government policies and emission standards shape pressure plate design requirements across major production markets. Euro 7 compliance tightens driveline specifications for vehicles sold in Europe, pushing OEM suppliers toward lighter, heat-resistant, and more precisely engineered clutch assemblies. Suppliers unable to meet evolving certification thresholds risk losing platform nominations to compliant competitors.

According to OICA, global vehicle production reached 96.4 million units in 2025, sustaining a large OEM demand base for clutch-equipped drivetrains. Battery-electric vehicles reached 19.4% of new EU car registrations in Q1 2026, confirming a structural shift away from clutch-dependent platforms in premium markets. This means suppliers must balance near-term ICE volume against accelerating substitution risk in developed economies.

Type Analysis

Diaphragm Type dominates with 69.20% due to superior clamping force and compact design.

In 2025, Diaphragm Type held a dominant market position in the By Product Type segment of the Automotive Clutch Pressure Plate Market, with a 69.20% share. Diaphragm spring designs deliver consistent clamping loads across the clutch disc surface while reducing pedal effort for drivers. This combination of performance and comfort drives OEM preference across passenger car and light commercial vehicle platforms globally.

Coil Spring Type accounts for the remaining 30.80% of the product type segment. Coil spring pressure plates remain commercially relevant in heavy-duty and commercial vehicle applications where higher torque loads exceed diaphragm spring capacity. Data from ACEA shows diesel trucks represented 92.4% of new EU truck registrations in Q1 2026, confirming a durable base of heavy-duty vehicles requiring coil spring clutch assemblies.

Vehicle Type Analysis

Passenger Car dominates with 49.80% due to largest global production volume base.

In 2025, Passenger Car held a dominant market position in the By Vehicle Type segment of the Automotive Clutch Pressure Plate Market, with a 49.80% share. As reported by ACEA, global passenger car production reached 75.5 million units in 2024, creating a sustained OEM fitment base for clutch pressure plates. This volume guarantees both direct assembly demand and a large future replacement pool for aftermarket suppliers.

Two-Wheeler vehicles represent a structurally distinct sub-segment serving markets where motorcycle and scooter penetration exceeds passenger car ownership. Asia Pacific dominates two-wheeler production and consumption, giving regional suppliers a cost and proximity advantage. Manual clutch systems remain standard across most two-wheeler drivetrains in price-sensitive markets, sustaining volume independent of passenger car transmission trends.

Light Commercial Vehicle and Medium and Heavy Commercial Vehicle segments together serve fleet operators with intensive duty cycles requiring frequent clutch replacement. JD Power data indicates manual transmission vehicles represented approximately 32% of new light-vehicle sales in the United States in 2024. Fleet operators running manual LCVs generate predictable aftermarket pull for replacement pressure plate assemblies at regular service intervals.

Distribution Channel Analysis

OEMs dominate with 67.50% due to direct platform integration and volume contracts.

In 2025, OEMs held a dominant market position in the By Distribution Channel segment of the Automotive Clutch Pressure Plate Market, with a 67.50% share. OEM contracts lock in pressure plate specifications at the platform design stage, creating multi-year supply relationships that aftermarket competitors cannot easily disrupt. This structural advantage rewards suppliers that invest in co-development partnerships with vehicle manufacturers.

Aftermarket distribution captures the remaining 32.50% of the channel segment. Aftermarket demand depends on aging vehicle parc, service frequency, and distribution reach across independent workshops. Suppliers with strong catalog coverage, brand recognition among workshop technicians, and reliable part availability hold a competitive edge in this fragmented channel.

Key Market Segments

By Product Type

- Diaphragm Type

- Coil Spring Type

By Vehicle Type

- Two-Wheeler

- Passenger Car

- Light Commercial Vehicle

- Medium and Heavy Commercial Vehicle

By Distribution Channel

- OEMs

- Aftermarket

Market Dynamics

Technology and Innovation Landscape - Digital simulation and self-adjusting designs redefine pressure plate engineering standards

Finite element analysis and digital simulation have become standard development tools for precision pressure plate engineering. These methods allow suppliers to model clamping force distribution, thermal stress, and fatigue life before physical prototyping, compressing development cycles. Suppliers that integrate simulation early in the design process reduce tooling revision costs and accelerate time-to-nomination against competitors using traditional trial-and-error methods.

Self-adjusting clutch pressure plate technologies extend service life and improve pedal comfort by automatically compensating for friction disc wear over the component’s operating life. This design approach reduces the frequency of adjustment interventions by workshop technicians, lowering total maintenance cost for fleet operators. Commercial vehicle fleet operators running high-mileage duty cycles represent the primary buyer segment for self-adjusting systems, where the total cost of ownership benefit is most quantifiable.

High-heat-resistance friction interface designs address the thermal demands created by downsized turbocharged engines, which generate higher localized heat at the clutch interface relative to naturally aspirated units of equivalent output. This thermal challenge requires suppliers to develop new friction material formulations and surface treatments that maintain consistent torque capacity under elevated temperature cycles. Suppliers with proprietary friction interface materials gain a technical differentiation point that is difficult for lower-cost competitors to replicate without equivalent materials science capability.

Lightweight aluminum-based pressure plate development targets fuel-efficient vehicle platforms where mass reduction contributes to compliance with tightening fuel economy and CO2 regulations. Aluminum components must overcome lower thermal conductivity and fatigue resistance compared with cast iron, requiring new alloy selections and surface coating approaches. Suppliers that solve these engineering constraints first gain access to vehicle programs where weight reduction targets drive material substitution decisions at the platform specification stage.

Market Opportunity Analysis - Localization gaps and underserved fleet segments offer entry points for suppliers

The aftermarket channel, which captures 32.50% of distribution share, remains underserved in Latin America, Southeast Asia, and Africa where workshop density is high but branded part availability is inconsistent. Suppliers that establish regional catalog coverage and distributor partnerships in these geographies can convert high vehicle age into reliable replacement revenue without competing directly against OEM contract holders.

The two-wheeler segment in Asia Pacific represents an underexploited sub-segment where manual clutch systems remain standard but specialized pressure plate product development lags behind passenger car investment. This creates an entry point for suppliers willing to develop cost-optimized, two-wheeler-specific pressure plate families for markets such as India, Vietnam, and Indonesia where two-wheeler parc sizes exceed passenger car volumes.

The Light Commercial Vehicle segment, particularly fleet-grade platforms in India, ASEAN, Africa, and Latin America, carries a potential CAGR upside of 1.1% for suppliers that develop dedicated LCV clutch platforms. Fleet operators in these regions prioritize total cost of ownership over unit price, rewarding suppliers that deliver longer service intervals and lower failure rates rather than lowest acquisition cost.

The circular remanufacturing model in the EU and North America carries a 0.8% potential CAGR upside for suppliers willing to build reverse logistics and remanufacturing capabilities. This segment is currently underdeveloped relative to remanufacturing activity in other drivetrain component categories. Suppliers that enter early can establish quality certification and brand trust before the segment attracts broader competition.

Drivers

Global vehicle production increased from 92.5 million units in 2024 to 96.4 million units in 2025, with China producing approximately 34.5 million vehicles and India approximately 6.5 million vehicles. This concentration of output in Asia Pacific directly expands the OEM addressable base for clutch pressure plates. Suppliers localized near Chinese and Indian assembly hubs gain cost, lead time, and content compliance advantages that determine platform nomination success.

Aging vehicle fleets in mature markets create durable aftermarket pull independent of new vehicle production cycles. S&P Global Mobility data shows the average US vehicle age reached 12.8 years in 2025. Passenger cars on European roads average 12.5 years, vans 12.9 years, and trucks 14.1 years. Older vehicles require more frequent clutch replacement, giving aftermarket suppliers a reliable revenue base even as new vehicle electrification advances.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Asia vehicle output concentration in clutch-bearing platforms | +1.3% | China core, India core, ASEAN spill-over, Latin America selective | Short term (≤ 2 years) |

| Aging vehicle parc supporting replacement cycles | +1.1% | EU core, India, Latin America, Middle East and Africa aftermarket | Short term (≤ 2 years) |

| Euro 7 and fuel-efficiency compliance tightening driveline specs | +0.9% | EU core, supplier programs in Turkey, North Africa, India export-linked | Medium term (2-4 years) |

| Commercial vehicle utilization and higher torque loading | +0.8% | India core, China core, Southeast Asia, Africa logistics corridors | Short term (≤ 2 years) |

| DCT and AMT migration raising value per clutch assembly | +0.6% | China, Europe, India passenger and CV niches | Medium term (2-4 years) |

| Organized aftermarket kit penetration and service standardization | +0.5% | EU core, India organized aftermarket, Latin America selective | Medium term (2-4 years) |

Restraints

Trade friction restrains clutch pressure plate demand realization across major supply corridors. Under USMCA rules, vehicles must meet 75% regional value content, 40% labor value content for passenger vehicles, and 70% North American steel and aluminum sourcing requirements. Non-compliant parts face duties that erode cost competitiveness, while documentation, certification, and audit requirements add transactional cost and working capital burden estimated at a 0.9 percentage point CAGR drag.

The decline in manual gearbox availability directly shrinks the addressable OEM market for clutch pressure plates in developed economies. In the UK, only 82 new vehicle models offered a manual gearbox in 2025 compared with 192 models in 2015. Global EV sales exceeded 17 million units in 2024, representing more than 20% of total car sales. Battery-electric vehicles accounted for 17.4% of new EU car registrations in 2025. Together, these trends confirm that clutch-dependent drivetrains are losing OEM platform share in key markets.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV drivetrain substitution | -2.3% | EU, China, North America core, advanced APAC | Medium term (2-4 years) |

| Automatic and hybrid mix shift | -1.2% | EU, Japan, Korea, China metros, North America | Medium term (2-4 years) |

| Steel cost and energy burden | -1.1% | EU, North America, India, Japan, Korea | Short term (≤ 2 years) |

| Trade-rule and origin compliance drag | -0.9% | USMCA corridor, EU import chain, China-linked sourcing | Short term (≤ 2 years) |

| ICE supplier underutilization | -0.8% | EU core, LatAm, export-oriented Asia plants | Short term (≤ 2 years) |

| Production geography realignment | -0.6% | Europe, North America, Asia supply corridors | Medium term (2-4 years) |

Challenges

Skilled process labor shortages create measurable production friction across clutch pressure plate manufacturing hubs in Germany, Italy, Japan, India, and Mexico. Europe’s automotive transition has already directed reskilling resources toward battery technology, with programs targeting approximately 800,000 workers through the European Battery Academy by end 2025. This labor reallocation tightens competition for stamping, spring metallurgy, and quality control specialists in legacy driveline supply chains.

The operational impact of this deficit includes 3% to 6% higher overtime dependence, 5% to 10% slower setup and die change performance, and onboarding delays of 8 to 16 weeks for replacement workers. Together these factors create an estimated 0.8 percentage point CAGR drag on the market. Suppliers that invest in apprenticeship programs, shop floor digitalization, and cross-skilling can convert this constraint into a competitive barrier against less-organized competitors.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Manual Powertrain Dilution | -1.3% | Europe core, China, North America transition zones, urban APAC | Long term (≥ 4 years) |

| Metals Cost Transmission | -0.8% | EU supplier base, India manufacturing clusters, North America sourcing lanes | Medium term (2-4 years) |

| Shipping Route Instability | -0.7% | Asia-Europe corridors, MENA routes, global aftermarket lanes | Medium term (2-4 years) |

| Skilled Process Labor Deficit | -0.8% | Germany, Italy, Japan, India, Mexico component hubs | Long term (≥ 4 years) |

| Compliance-Driven Reengineering | -0.6% | EU regulatory hubs, Japan, South Korea, North America OEM networks | Medium term (2-4 years) |

| Channel Quality Inconsistency | -0.5% | Latin America, Southeast Asia, Africa, cross-border e-commerce markets | Short term (≤ 2 years) |

Opportunities

Asia Pacific production reached approximately 59.2 million vehicles in 2025, accounting for more than 61% of global output. This geographic concentration of manufacturing creates a localization opportunity for clutch pressure plate suppliers. Moving stamping, diaphragm spring production, and machining closer to India and ASEAN assembly corridors can reduce landed component cost by an estimated 8% to 12% and shorten lead times from roughly 10 to 14 weeks down to 4 to 6 weeks.

Beyond cost reduction, localization near India and ASEAN hubs improves working capital efficiency by more than 1 turn annually and positions suppliers to win new platform nominations in cost-sensitive vehicle programs using manual or clutch-based transmissions. Export-linked supply contracts across India, Southeast Asia, the Middle East, and Africa represent the primary revenue upside, not industry growth alone. Suppliers that establish local footprints now gain first-mover advantage in nomination cycles before competitors localize.

Regional Analysis

Asia Pacific Dominates the Automotive Clutch Pressure Plate Market with a Market Share of 48.90%, Valued at USD 3.1 Billion

Asia Pacific holds the dominant regional position because it concentrates the largest share of global vehicle production, with manual, AMT, and DCT platforms still commercially standard across China, India, and Southeast Asia. The region’s cost-sensitive passenger car and two-wheeler markets sustain high-volume OEM fitment demand. Suppliers localized in this region gain structural advantages in nomination success for new platform contracts.

Europe represents a structurally complex regional market where aging vehicle parc supports aftermarket demand while new vehicle electrification erodes OEM clutch volumes. ACEA data shows the EU recorded 10.6 million new passenger car registrations in 2025. Light commercial vehicle registrations in the EU also rose 8.3% in Q1 2026, providing an offsetting aftermarket and OEM demand source in the commercial vehicle segment.

North America maintains a meaningful clutch pressure plate market anchored by aging fleet vehicles and residual manual transmission adoption in light commercial and performance segments. The US vehicle parc average age of 12.8 years directly lengthens replacement cycles, sustaining aftermarket volumes. USMCA trade rules create compliance complexity for suppliers moving components across the US, Canada, and Mexico corridor.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Competitive Analysis

ZF Friedrichshafen AG holds a structural advantage in the clutch pressure plate market through its integrated drivetrain systems portfolio, which allows the company to bundle pressure plates with broader transmission and clutch module contracts. This bundling approach raises switching costs for OEM customers and creates multi-year revenue visibility. However, ZF’s heavy exposure to European OEM programs increases its vulnerability to regional EV substitution risk.

Aisin Seiki Co., Ltd. benefits from deep integration within Toyota Group supply chains, giving it preferential access to high-volume passenger car platform nominations across Asia Pacific. IEA data confirms more than 70% of vehicles worldwide still use ICE powertrains, sustaining near-term demand across Aisin’s core markets. In April 2025, Valeo launched its remanufactured DQ250 Double Wet Clutch at Rematec 2025, signaling that remanufacturing is becoming a competitive front that Aisin must address to defend aftermarket share.

Key Players

- ZF Friedrichshafen AG

- Aisin Seiki Co., Ltd.

- Valeo SA

- Schaeffler AG

- BorgWarner Inc.

- EXEDY Corporation

- ANAND Group

- Raicam Clutch Ltd.

- Setco Automotive Ltd.

- AP Racing

Recent Developments

- June 2025 – Schaeffler Vehicle Lifetime Solutions launched the LuK RepSet 2CT DMF, the first repair kit combining a double clutch and dual-mass flywheel in a single aftermarket solution, reducing maintenance complexity for workshops handling dual-clutch transmission vehicles.

- April 2025 – Valeo announced the launch of its remanufactured DQ250 Double Wet Clutch solution at Rematec 2025, expanding its aftermarket clutch portfolio to cover millions of vehicles equipped with dual-clutch transmissions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.1 Billion |

| Forecast Revenue (2035) | USD 6.0 Billion |

| CAGR (2026-2035) | 6.80% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Diaphragm Type, Coil Spring Type), By Vehicle Type (Two-Wheeler, Passenger Car, Light Commercial Vehicle, Medium and Heavy Commercial Vehicle), By Distribution Channel (OEMs, Aftermarket) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | ZF Friedrichshafen AG, Aisin Seiki Co., Ltd., Valeo SA, Schaeffler AG, BorgWarner Inc., EXEDY Corporation, ANAND Group, Raicam Clutch Ltd., Setco Automotive Ltd., AP Racing |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |