Quick Navigation

Report Overview

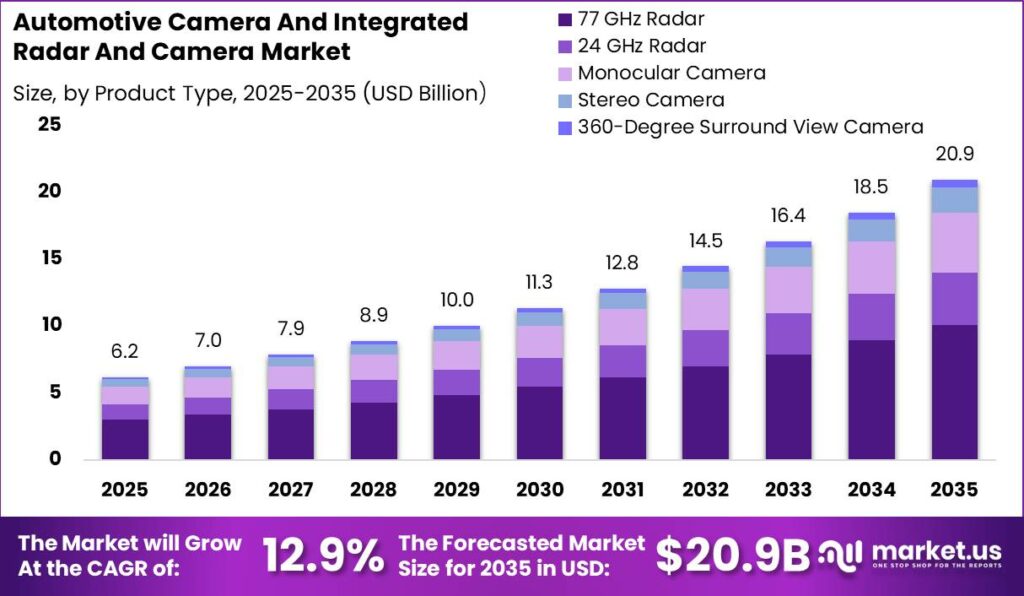

Global Automotive Camera And Integrated Radar And Camera Market size is expected to be worth around USD 20.95 Billion by 2035 from USD 6.20 Billion in 2025, growing at a CAGR of 12.95% during the forecast period 2026 to 2035.

This market encompasses automotive-grade cameras, radar sensors, and integrated radar-camera modules deployed across passenger cars, light commercial vehicles, and heavy commercial vehicles. These systems serve ADAS functions including forward collision warning, automated emergency braking, lane keeping, blind spot detection, parking assistance, and autonomous driving perception. OEM supply channels account for the dominant distribution pathway, with aftermarket integration providing secondary volume across replacement and retrofit applications.

Regulatory mandates from Euro NCAP, NHTSA, and Bharat NCAP are embedding radar and camera sensing into base vehicle type-approval requirements. This policy pressure is shifting OEM procurement from optional ADAS content to mandatory compliance hardware. Tier-1 suppliers with design wins locked into regulatory-driven model cycles are positioned to capture compounding revenue as per-vehicle sensor content requirements escalate.

According to Euro NCAP, in 2025 a record 108 vehicle safety assessments were completed across more than 50 automotive brands, confirming that radar-camera fusion systems are now embedded across the mainstream vehicle production landscape. This volume of testing signals that ADAS sensor compliance has moved from premium differentiation to baseline OEM procurement. Suppliers serving this regulatory cycle face predictable demand growth tied directly to statutory deadlines rather than consumer discretionary spending. As reported by Euro NCAP’s 2025 InReview, 98% of all vehicles tested achieved four stars or higher, demonstrating that advanced camera- and radar-based active safety technologies are now standard across the global vehicle fleet. This result confirms that sensor integration quality has reached a threshold where product differentiation shifts from presence to performance, compelling suppliers to invest in perception accuracy rather than market access.

Automotive radar startups including Arbe Robotics and Uhnder benefited from nearly USD 1 Billion in cumulative industry funding by February 2025, reflecting strong investor conviction in high-resolution imaging radar as the next performance frontier for camera-radar fusion platforms. This funding concentration signals that imaging radar is transitioning from research-stage to commercial-scale deployment, compressing the window for incumbents to defend sensor technology positioning before new entrants reach production volumes.

Key Takeaways

- Market size in 2025: USD 6.20 Billion

- Market size in 2035: USD 20.95 Billion

- CAGR (2026 to 2035): 12.95%

- Dominant component segment: Automotive Camera with 51.20% share

- Dominant technology segment: 77 GHz Radar with 48.20% share

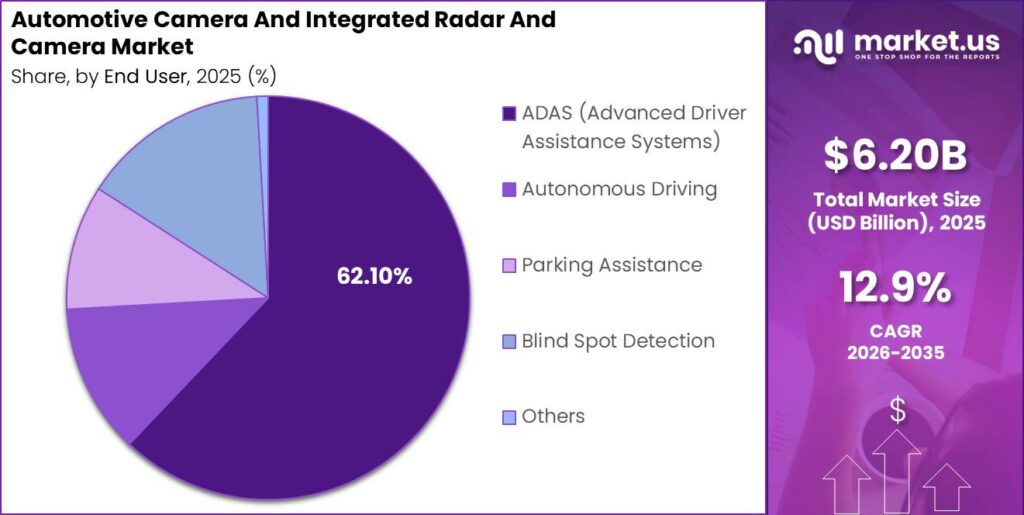

- Dominant application segment: ADAS with 62.10% share

- Dominant vehicle type segment: Passenger Cars with 67.20% share

- Dominant sales channel: OEM with 83.10% share

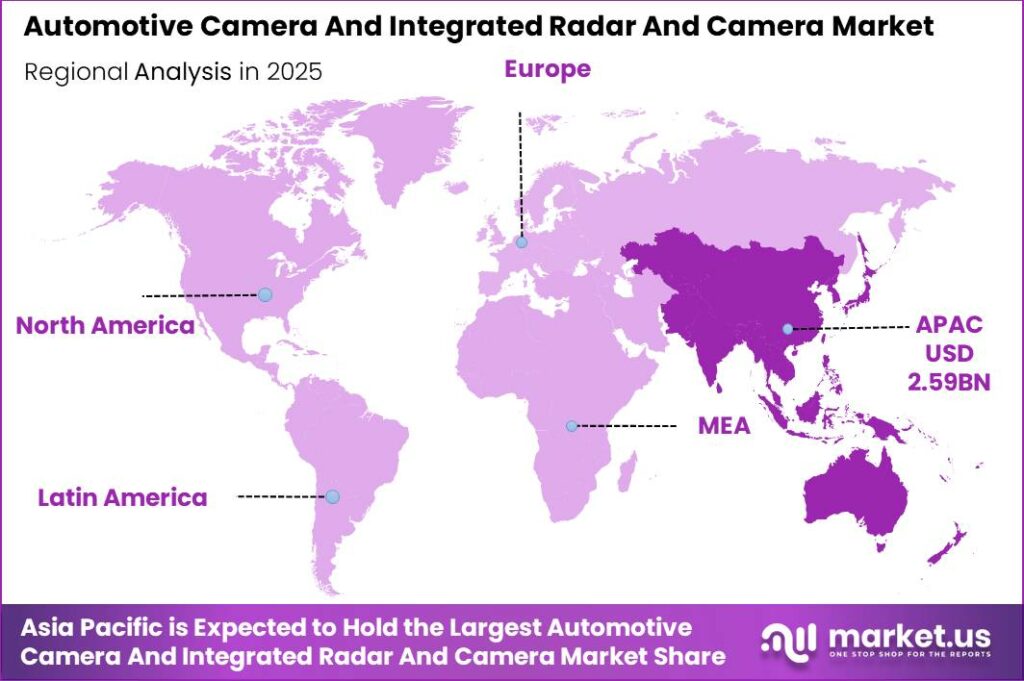

- Dominant region: Asia Pacific with 41.80% share, valued at USD 2.59 Billion

Component Analysis

Automotive Camera dominates with 51.20% due to regulatory mandate-driven base fitment requirements.

In 2025, Automotive Camera held a dominant market position in the By Component segment of the Automotive Camera And Integrated Radar And Camera Market, with a 51.20% share. Camera systems function as the foundational sensing layer across ADAS architectures, serving lane detection, sign recognition, parking guidance, and driver monitoring within a single hardware category. Euro NCAP data shows that 58% of all vehicles tested in 2025 were battery-electric vehicles, and BEV platforms increasingly specify higher camera counts per vehicle to support software-defined ADAS feature stacks. Suppliers securing BEV platform design wins are positioned to capture compounding per-vehicle content value as EV production volumes scale.

Radar Sensor systems provide the independent sensing channel required for AEB, adaptive cruise control, and blind spot detection functions that camera systems alone cannot satisfy under ISO 26262 safety integrity requirements. Radar transceiver adoption is accelerating across mid-segment vehicle programs where functional safety certification demands a redundant non-optical perception pathway. Suppliers combining radar sensing with camera processing on shared SoC architectures are reducing system integration cost, which is the primary barrier to radar adoption in cost-sensitive OEM programs.

Integrated Radar-Camera Modules represent the highest-value hardware category in this market by combining both sensing modalities within a single mechanical and electronic assembly. These units reduce vehicle-level wiring harness cost, simplify OEM integration, and enable tighter sensor fusion algorithm development on co-located processing hardware. As OEMs migrate toward centralized domain controller architectures, integrated modules offering a pre-validated sensor pair are gaining procurement preference over separately sourced radar and camera subsystems.

Technology Analysis

77 GHz Radar dominates with 48.20% due to superior range resolution and all-weather detection capability.

In 2025, 77 GHz Radar held a dominant market position in the By Technology segment of the Automotive Camera And Integrated Radar And Camera Market, with a 48.20% share. This frequency band delivers target range resolution below 5 cm and detection capability at distances exceeding 200 meters, making it the mandatory technology choice for highway-speed AEB, adaptive cruise control, and forward collision warning systems. Euro NCAP’s largest 2025 test programme saw 18 of 23 newly evaluated vehicles receive the maximum five-star safety rating, with advanced driver assistance technologies including 77 GHz radar-based AEB as a core evaluation component. OEMs integrating 77 GHz radar face an expanding design requirement as NCAP protocols demand pedestrian and cyclist detection in addition to vehicle-to-vehicle sensing.

24 GHz Radar occupies short-range sensing positions including rear cross-traffic alert, blind spot monitoring, and near-range parking detection where the reduced frequency band provides adequate resolution at lower hardware cost than 77 GHz transceivers. This technology remains commercially viable in aftermarket-facing applications and cost-constrained mid-tier OEM programs where full-range ACC is not a program requirement. However, regulatory ADAS content requirements at higher safety ratings are gradually compressing the per-vehicle share of 24 GHz versus 77 GHz specifications as OEM ADAS architectures scale upward in functional scope.

Monocular Camera systems remain the highest-volume camera category in production ADAS by unit count, serving forward collision warning, lane departure warning, sign recognition, and pedestrian detection within a compact single-lens optical assembly. Their cost efficiency at scale makes them the default fitment for entry-level regulatory compliance. Stereo Camera and 360-Degree Surround View Camera systems address parking, low-speed maneuvering, and full-perimeter awareness, with surround view architectures typically deploying four wide-angle cameras to eliminate the blind zones that single forward-facing systems cannot cover.

Application Analysis

ADAS dominates with 62.10% due to regulatory mandate-driven fitment across all new vehicle types.

In 2025, ADAS held a dominant market position in the By Application segment of the Automotive Camera And Integrated Radar And Camera Market, with a 62.10% share. ADAS functions including AEB, lane keeping, adaptive cruise control, and driver monitoring collectively define the primary commercial demand pool for camera and radar-camera hardware. A 2026 peer-reviewed study evaluated an Automatic Emergency Braking system across 72 real-world driving sessions and 131,603 camera frames, providing large-scale validation of integrated radar-camera perception performance at production system specifications. This scale of real-world validation data directly supports OEM functional safety certification processes and shortens regulatory type-approval timelines for AEB system variants.

The same 2026 study reported that its radar-guided camera verification algorithm reduced the camera search area by 98.7%, achieved 0.121 ms average processing latency per region of interest, produced an AUC of 0.898, achieved 0.994 recall, and recorded zero missed brake events across 33 staged threat scenarios. These results confirm that radar-guided camera processing can simultaneously improve perception accuracy and reduce compute load, a combination that reduces SoC specification cost and enables OEMs to scale AEB functionality to lower-cost vehicle programs without sacrificing ISO 26262 compliance headroom.

Autonomous Driving applications represent the highest per-vehicle sensor content category, requiring full sensor suite integration including multiple radar units, high-resolution cameras, and centralized fusion processing. Parking Assistance systems represent a stable mid-tier application using rear and surround cameras with short-range ultrasonic or radar complementing optical guidance. Blind Spot Detection relies on rear-corner radar as its primary sensing mechanism. Other applications spanning trailer detection, occupant monitoring, and road condition sensing are building incremental per-vehicle sensor content as OEM feature scope expands.

Vehicle Type Analysis

Passenger Cars dominate with 67.20% due to the largest new vehicle production volume and regulatory coverage.

In 2025, Passenger Cars held a dominant market position in the By Vehicle Type segment of the Automotive Camera And Integrated Radar And Camera Market, with a 67.20% share. Passenger cars represent the largest production volume category globally, and Euro NCAP and NHTSA safety assessment protocols cover passenger cars as their primary vehicle class, directly aligning regulatory mandates with the highest-production vehicle segment. Euro NCAP now evaluates driver monitoring technologies that continuously track driver attention and integrate driver-state information with ADAS functionality, increasing the per-vehicle sensor content specification across the passenger car category. Suppliers covering in-cabin camera and driver monitoring system programs for passenger cars are accessing the broadest addressable design-win pool in this market.

Light Commercial Vehicles represent the next largest vehicle type category for camera and radar-camera system adoption, driven by fleet operator demand for rear-vision compliance, lane keeping for long-distance driving, and blind spot monitoring for urban delivery cycles. Fleet operators procuring at scale provide Tier-1 suppliers with predictable forward order volumes that reduce revenue concentration risk versus OEM passenger car program dependency. Heavy Commercial Vehicles carry a smaller unit production base but higher per-vehicle sensor content value, as truck ADAS systems typically include multiple radar positions, forward cameras, side cameras, and driver monitoring in a single vehicle specification.

Sales Channel Analysis

OEM dominates with 83.10% due to regulatory type-approval requirements forcing factory-fitted sensor integration.

In 2025, OEM held a dominant market position in the By Sales Channel segment of the Automotive Camera And Integrated Radar And Camera Market, with an 83.10% share. Type-approval regulatory frameworks in the EU, United States, Japan, and South Korea require camera and radar systems to be factory-fitted and certified as part of the base vehicle specification, making OEM supply the structurally mandated procurement channel for compliance-driven ADAS content. Tier-1 suppliers with locked OEM design wins benefit from program-length revenue visibility spanning typically 5 to 7 vehicle production years, providing demand predictability unavailable in aftermarket supply relationships. The Aftermarket channel serves replacement, retrofit, and commercial fleet upgrade applications. Aftermarket camera and radar systems address vehicle populations without factory-fitted ADAS, though calibration complexity and liability considerations limit aftermarket penetration in safety-critical AEB and lane-keeping applications versus parking and reversing camera upgrades where consumer installation remains commercially viable.

Key Market Segments

By Component

- Automotive Camera

- Radar Sensor

- Integrated Radar-Camera Module

By Technology

- 77 GHz Radar

- 24 GHz Radar

- Monocular Camera

- Stereo Camera

- 360-Degree Surround View Camera

By Application

- ADAS (Advanced Driver Assistance Systems)

- Autonomous Driving

- Parking Assistance

- Blind Spot Detection

- Others

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

By Sales Channel

- OEM

- Aftermarket

Regional Analysis

Asia Pacific Dominates the Automotive Camera And Integrated Radar And Camera Market with a Market Share of 41.80%, Valued at USD 2.59 Billion

Asia Pacific accounts for 41.80% of global market revenue, valued at USD 2.59 Billion in 2025, driven by the concentration of global vehicle production capacity in China, Japan, and South Korea alongside domestic ADAS regulatory adoption across these three markets. China’s mandatory ADAS content requirements for domestically sold passenger cars and the rapid EV fleet expansion have elevated per-vehicle camera and radar sensor content specifications across Chinese OEM programs. Japanese and South Korean Tier-1 suppliers including Denso and leading radar integrators benefit from domestic OEM program proximity, reducing supply chain risk and enabling tighter co-development cycles versus non-domestic competitors.

Europe is the fastest-growing regulated market for radar-camera fusion system content, driven by the EU General Safety Regulation Phase III implementation deadline for all new vehicles from July 2026, which mandates ADDW interior camera systems and pedestrian-and-cyclist AEB across every new type-approved vehicle. Euro NCAP’s on-road testing programme equips every evaluation vehicle with LiDAR, radar, and cameras to establish precise ground-truth data, directly raising the performance bar for camera and radar-camera systems seeking NCAP validation. In December 2025, HARMAN signed a definitive agreement to acquire ZF Group’s Advanced Driver Assistance Systems business for an enterprise value of €1.5 Billion, consolidating radar technologies, smart cameras, and ADAS software functions under a single entity and reshaping the European Tier-1 competitive structure.

North America holds a structurally significant market position supported by NHTSA’s AEB-pedestrian mandate trajectory and the updated U.S. NCAP scoring framework increasing camera adoption requirements. Latin America and Middle East & Africa represent earlier-stage adoption regions where regulatory ADAS content requirements are emerging, with India’s Bharat NCAP and AIS-157 reverse camera mandate creating a measurable near-term volume uplift for the broader Asia-adjacent supply base serving Southeast Asian and South Asian vehicle programs.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Market Opportunity Analysis - Underserved segments and regulatory white-space markets offer high-value entry points for focused suppliers

The Aftermarket sales channel holds the most structurally underexploited commercial position relative to its addressable vehicle population. With OEM supply commanding 83.10% of channel share, the remaining installed vehicle fleet operating without factory-fitted radar-camera ADAS represents a retrofit addressable market that aftermarket-focused suppliers have not yet converted at scale. Fleet operators managing older commercial vehicle populations face a compliance upgrade cycle as national road safety frameworks extend ADAS requirements to in-service vehicles, creating a pull-through demand pathway for aftermarket radar and camera integration systems that OEM-focused suppliers are not positioned to serve.

Heavy Commercial Vehicles represent an underserved vehicle type category relative to their per-vehicle sensor content potential. The dominant Passenger Car segment commands 67.20% of vehicle type share, concentrating Tier-1 supplier design-win competition in one category. By contrast, HCV programs offer higher per-unit system revenue with longer vehicle replacement cycles that extend aftermarket service revenue streams beyond the shorter passenger car lifecycle. Suppliers entering the HCV radar-camera system space face a less congested competitive field than the passenger car OEM program market while accessing a structurally larger per-vehicle revenue opportunity.

The 360-Degree Surround View Camera sub-segment within the Technology segment holds disproportionate growth potential relative to its current production penetration. As OEMs migrate toward centralized domain controller architectures processing fused radar-camera data, surround-view systems delivering continuous perimeter awareness become a mandatory input layer for full-coverage perception. Suppliers developing surround-view architectures pre-integrated with front radar and corner radar sensing are positioned to capture the domain controller migration as a system-level design win rather than a commodity camera module procurement.

The Latin America and Middle East & Africa regional markets represent the lowest current penetration relative to long-term regulatory trajectory. As Bharat NCAP protocols and AIS-157 mandates in India establish proof-of-concept for emerging-market camera content requirements, neighboring regulatory frameworks in Southeast Asia and the GCC are likely to adopt analogous minimum ADAS content standards within a medium-term window. Suppliers establishing distribution and calibration service infrastructure in these regions before mandatory content requirements activate will capture first-mover advantage in markets where regulatory-driven demand will arrive as a step function rather than a gradual adoption curve.

Technology and Innovation Landscape - AI-native sensor fusion, 4D imaging radar, and OTA-enabled perception architectures define the next competitive tier

The migration from distributed ADAS ECUs to centralized domain controllers processing fused radar-camera data is the most structurally significant platform architecture shift in this market. Centralized processing concentrates perception compute into a single high-performance SoC or chiplet cluster, enabling AI fusion models with parameter counts that distributed ECU architectures cannot support. Suppliers developing perception software validated on centralized domain controller hardware are building a platform dependency that creates multi-year switching costs for OEM programs once the base architecture is locked into a vehicle program cycle.

Dedicated AI accelerators integrated within automotive SoCs are enabling real-time radar-camera perception and trajectory prediction at latencies below 100 ms, which is the functional threshold for AEB intervention timing at highway speeds. Transformer-based and deep-learning radar-camera fusion models are improving 3D object detection accuracy versus earlier convolutional approaches, with the 2026 peer-reviewed AEB study demonstrating a processing latency of 0.121 ms per region of interest using a radar-guided camera algorithm. This latency performance level confirms that AI-native fusion architectures can meet automotive real-time constraints while delivering superior detection accuracy versus rule-based sensor processing pipelines.

Synthetic-data generation and digital validation platforms are compressing the development timeline for radar-camera perception systems by replacing a portion of physical real-world data collection with procedurally generated sensor simulation. This technology reduces the cost of building training datasets across rare adverse weather and low-light edge cases that are statistically underrepresented in naturally collected driving data. Suppliers adopting digital validation platforms alongside physical testing programs are shortening ISO 21448 SOTIF compliance timelines, which translates directly into earlier design-win capture and faster revenue recognition on new OEM platform programs.

Software-defined vehicle architectures enabling over-the-air enhancement of radar-camera perception and ADAS capabilities represent a structural revenue model shift from one-time hardware sales to recurring software upgrade revenue. The Valeo and Amazon Web Services collaboration announced in January 2025 directly targets this model, combining ADAS hardware expertise with cloud-based software development and deployment infrastructure. Suppliers building OTA-capable radar-camera systems today are establishing the technical prerequisite for subscription-based or feature-unlock revenue streams that decouple ADAS revenue growth from physical vehicle production volume.

Drivers

Level 2+ and Level 3 ADAS architectures require radar-camera sensor fusion to meet perception redundancy and functional safety standards mandated under ISO 26262. Euro NCAP and global vehicle safety assessment protocols are compelling OEM integration of fused radar-camera sensing, with NHTSA confirming that driver assistance technologies such as Automatic Emergency Braking and Forward Collision Warning are designed to reduce crashes caused by human error. Suppliers aligned with OEM ADAS platform roadmaps entering these compliance cycles face multi-year revenue predictability from statutory procurement obligations.

Increasing sensor content per vehicle, including front radar, corner radar, and surround-view cameras, is strengthening demand for integrated perception architectures across passenger and commercial vehicles. Advances in AI-enabled sensor fusion algorithms are improving object detection, classification, and tracking performance across challenging weather, lighting, and traffic conditions. Tier-1 suppliers investing in AI perception algorithm development alongside hardware are building a competitive moat that pure hardware vendors cannot replicate, as OEM procurement increasingly bundles perception software into camera and radar-camera system contracts.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU GSR Phase II & III Mandating AEB (Pedestrian/Cyclist), ADDW & DMS Camera Fitment | +3.8% | EU (all 27 member states), cascading to UK, Norway, Switzerland, ASEAN bilateral adopters | Short term (≤ 2 years) |

| NHTSA AEB-Pedestrian Mandate & Updated U.S. NCAP Driving Camera Adoption | +2.6% | United States, Canada | Short term (≤ 2 years) |

| Radar-Camera Sensor Fusion Architecture Becoming Standard in L2+ ADAS Platforms | +2.2% | Global, led by China, Europe, United States, South Korea, Japan | Short term (≤ 2 years) |

| EV Platform Software-Defined Vehicle (SDV) Architecture Increasing Per-Vehicle Camera Count | +1.7% | China, United States, Europe | Short term (≤ 2 years) |

| India Bharat NCAP & AIS-157 Reverse Camera Mandate Driving Emerging Market Volume | +1.2% | India, Southeast Asia, Brazil | Medium term (2–4 years) |

| Euro NCAP 2026 Safe Driving Protocol Incentivizing Driver Monitoring System Upgrades | +0.9% | EU, UK, Australia, Middle East (aligned NCAP markets) | Short term (≤ 2 years) |

Restraints

Functional safety compliance under ISO 26262, sensor calibration requirements, and system-level validation increase engineering costs and lengthen product development timelines for integrated radar-camera perception platforms. These cost and time burdens are most acute for Tier-2 and Tier-3 suppliers without established safety engineering teams, effectively concentrating design-win capture among large Tier-1 incumbents with existing certification infrastructure and compressing the competitive access window for new entrants targeting OEM program positions.

Packaging radar and camera sensing technologies within vehicle space constraints introduces thermal management, electromagnetic compatibility, and mechanical integration challenges that require iterative re-engineering across vehicle platform variants. Each vehicle model variant requiring a unique sensor integration solution multiplies engineering resource consumption per platform, raising program cost for multi-platform suppliers and reducing the margin benefit of scale. These constraints directly slow adoption in segments where OEM budgets cannot absorb incremental system integration engineering cost alongside rising hardware BOM.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive ADAS SoC & Image Sensor Semiconductor Supply Constraints & Extended Lead Times | -2.9% | Global — impacting all OEM and Tier-1 camera system supply chains | Short term (≤ 2 years) |

| U.S.–China Technology Trade Controls Restricting Advanced Imaging & Radar Chip Sourcing | -2.1% | United States, EU, Japan, South Korea — markets limiting China-origin ADAS chip content | Short term (≤ 2 years) |

| High Per-System BOM Cost of Radar-Camera Fusion Constraining Mid- & Entry-Segment Adoption | -1.5% | Global, most acute in India, Southeast Asia, Brazil, and entry-tier EU/U.S. segments | Medium term (2–4 years) |

| Camera Mirror System (CMS) Regulatory Non-Approval in U.S. & Key Emerging Markets | -0.8% | United States, Brazil, India — markets without FMVSS/AIS CMS mirror-replacement approval | Medium term (2–4 years) |

| Cybersecurity & GDPR Compliance Costs on In-Cabin DMS Data Processing | -0.5% | EU, UK — privacy regulation impacting DMS data handling architecture decisions | Short term (≤ 2 years) |

Challenges

Adverse weather and lighting conditions create a persistent functional safety ceiling for camera-based perception systems, requiring radar-camera fusion architectures that add hardware cost to every vehicle program. Cross-platform sensor fusion standardization gaps fragment the development investment required from Tier-1 suppliers across Chinese, European, and U.S. OEM platforms, multiplying engineering resource consumption without proportional revenue return. Suppliers unable to develop platform-agnostic fusion architectures face escalating program costs that compress margins and limit the number of simultaneous design-win pursuits their engineering teams can support.

ADAS perception AI validation under ISO 21448 SOTIF and the shortage of qualified ADAS systems engineering talent are compressing development capacity across the Tier-1 supplier base. Validation datasets for radar-camera perception systems require millions of annotated multi-sensor frames across diverse real-world conditions, a data infrastructure investment that few suppliers can build independently. Camera and radar calibration complexity in the aftermarket and repair cycle adds an operational constraint that limits ADAS system adoption in fleet management and independent repair network markets, reducing the addressable revenue pool beyond the OEM supply channel.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Adverse Weather & Lighting Sensor Reliability | -2.4% | Global — constrains all-condition ADAS functional safety validation | Long term (≥ 4 years) |

| Cross-Platform Sensor Fusion Standardization Gap | -1.8% | Global, particularly fragmented across Chinese, European, U.S. OEM platforms | Long term (≥ 4 years) |

| ADAS Perception AI Validation & ISO 21448 SOTIF Compliance Burden | -1.4% | Global — ISO 21448 formal compliance applies to all L2+ systems in type-approval markets | Medium term (2–4 years) |

| Qualified ADAS Systems Engineering Talent Shortage | -1.1% | Global, most acute in Europe, United States, Japan engineering hubs | Long term (≥ 4 years) |

| Camera & Radar Calibration Complexity in Aftermarket & Repair Cycle | -0.7% | Global, particularly in independent repair network markets with limited ADAS calibration tools | Medium term (2–4 years) |

Opportunities

Integrating 4D imaging radar with high-resolution camera systems is expanding use cases for highway pilot, automated lane change, and predictive collision avoidance at performance levels unavailable from conventional radar-camera pairs. Radar-camera sensor fusion adoption across commercial vehicles and fleet safety platforms supports next-generation ADAS deployment at scale. Fleet operators purchasing camera-radar integrated safety systems in volume provide Tier-1 suppliers with a revenue concentration point that improves forward order visibility beyond the standard OEM model-year cycle.

Software-defined vehicle architectures enabling over-the-air enhancement of radar-camera perception and ADAS capabilities create a recurring revenue layer for suppliers whose systems support field-upgradeable perception algorithms. Synthetic-data generation and digital validation platforms are reducing development time for radar-camera perception systems, directly compressing time-to-market for new system variants and lowering the dataset acquisition cost barrier that previously restricted perception AI development to large-scale incumbents. Early movers standardizing on OTA-capable radar-camera platforms position themselves to capture both the initial hardware sale and subsequent software upgrade revenue streams across the vehicle’s operational lifetime.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Camera Monitor System (CMS) Regulatory Approval & Full Mirror Replacement Commercialization in U.S. & Emerging Markets | +2.8% | United States, Brazil, India — the three largest markets without active CMS mirror-replacement approval | Medium term (2–4 years) |

| AI-Native Edge Perception SoC Integration Enabling Over-the-Air ADAS Feature Unlocking | +2.1% | Global, led by China, United States, Europe in SDV-first OEM programs | Medium term (2–4 years) |

| Radar-Camera Fusion for Two-Wheeler & Three-Wheeler ADAS in India & Southeast Asia | +1.6% | India, Indonesia, Vietnam, Thailand | Long term (≥ 4 years) |

| In-Cabin Occupant Monitoring Expansion Beyond DMS to Child Presence & Biometric Functions | +1.2% | EU, United States, China, GCC | Medium term (2–4 years) |

| V2X-Integrated Perception — Camera & Radar Data Feeding Roadside Infrastructure & Fleet AI Networks | +0.9% | China, United States, EU (C-V2X deployment corridors) | Long term (≥ 4 years) |

Key Company Insights

Robert Bosch GmbH holds a structural advantage in this market through its vertically integrated radar-camera system portfolio spanning radar transceivers, camera modules, and perception processing software. In March 2025, Bosch introduced its SX600 and SX601 77 GHz radar SoC family designed for SAE Level 2+ driver assistance systems, directly addressing the next-generation radar-camera perception architecture requirement. Bosch’s data confirms that combining radar and camera data increases measurement reliability, extends detection range, and improves object confirmation versus standalone sensors, which reflects the integration depth that OEM procurement decision-makers now treat as a baseline system requirement rather than a premium differentiation.

Continental AG competes through a broad ADAS product portfolio covering radar sensors, forward cameras, surround-view systems, and integrated perception ECUs that span multiple vehicle segments and price tiers. This multi-tier product architecture positions Continental to serve both premium OEM ADAS specifications and cost-optimized mid-segment compliance programs within a single supplier relationship, reducing OEM program management complexity. However, breadth across multiple sensor categories creates internal resource competition for engineering investment, which may slow Continental’s speed to market on next-generation imaging radar and AI-native perception platforms where focused specialists are compressing development cycles.

Key Players

- Robert Bosch GmbH

- Continental AG

- Valeo SA

- Denso Corporation

- Aptiv PLC

- Infineon Technologies AG

- Texas Instruments Incorporated

- NXP Semiconductors N.V.

- Mobileye Global Inc.

- ZF Friedrichshafen AG

- Hella GmbH & Co. KGaA

- Autoliv Inc.

Recent Developments

- January 2025: Valeo and Amazon Web Services announced a collaboration to develop software-defined vehicle technologies, combining Valeo’s ADAS expertise with AWS cloud capabilities to accelerate AI-enabled perception and sensor-fusion development.

- July 2025: ZF Friedrichshafen commercially launched its complete Brake-by-Wire portfolio, enabling tighter integration with camera- and radar-based ADAS functions for automated braking applications.

- September 2025: Mobileye introduced next-generation imaging radar capabilities alongside its autonomous driving platform, strengthening multi-sensor fusion for advanced driver assistance and automated driving systems.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 6.20 Billion |

| Forecast Revenue (2035) | USD 20.95 Billion |

| CAGR (2026-2035) | 12.95% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Automotive Camera, Radar Sensor, Integrated Radar-Camera Module), By Technology (77 GHz Radar, 24 GHz Radar, Monocular Camera, Stereo Camera, 360-Degree Surround View Camera), By Application (ADAS, Autonomous Driving, Parking Assistance, Blind Spot Detection, Others), By Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles), By Sales Channel (OEM, Aftermarket) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Robert Bosch GmbH, Continental AG, Valeo SA, Denso Corporation, Aptiv PLC, Infineon Technologies AG, Texas Instruments Incorporated, NXP Semiconductors N.V., Mobileye Global Inc., ZF Friedrichshafen AG, Hella GmbH & Co. KGaA, Autoliv Inc. |

| Customization Scope | Customization for segments, region / country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License | Multi-User License (Up to 5 Users) | Corporate Use License (Unlimited User and Printable PDF) |