Quick Navigation

Report Overview

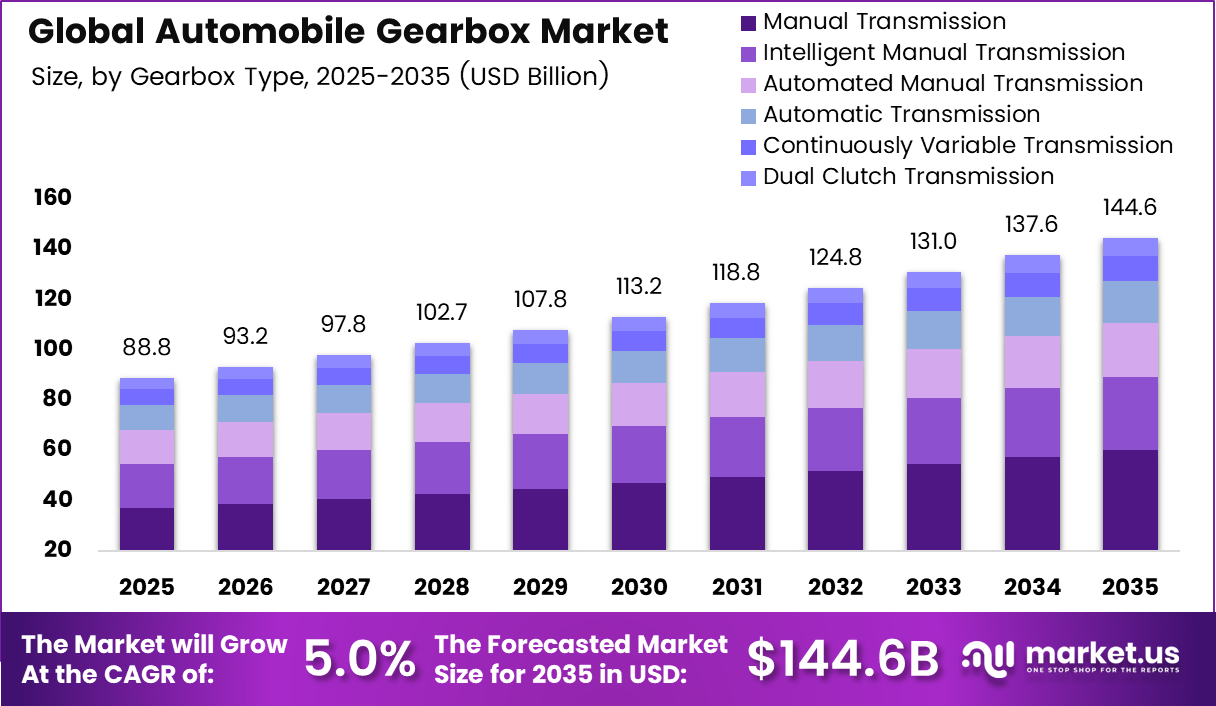

Global Automobile Gearbox Market size is expected to be worth around USD 144.6 Billion by 2035 from USD 88.8 Billion in 2025, growing at a CAGR of 5.00% during the forecast period 2026 to 2035.

The automobile gearbox market covers all transmission systems that transfer engine torque to the drivetrain across passenger cars, light commercial vehicles, and heavy commercial vehicles. This market spans manual, automated manual, automatic, dual-clutch, continuously variable, and intelligent manual transmission types. As a result, it serves a broad range of powertrain architectures from pure ICE to hybrid and battery electric configurations.

Key Takeaways

- Market size in 2025: USD 88.8 Billion

- Forecast market size by 2035: USD 144.6 Billion

- CAGR (2026 to 2035): 5.00%

- Dominant gearbox type segment: Manual Transmission with 41.60% share

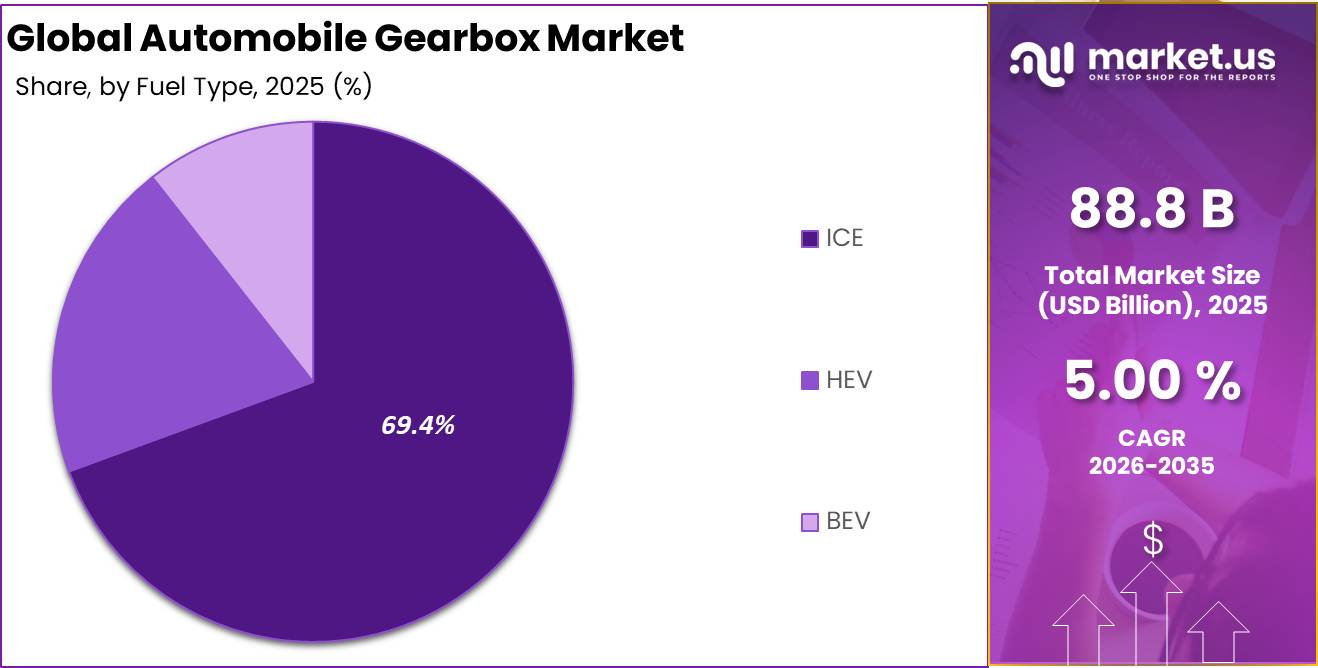

- Dominant fuel type segment: ICE with 69.40% share

- Dominant vehicle type segment: SUV with 41.70% share

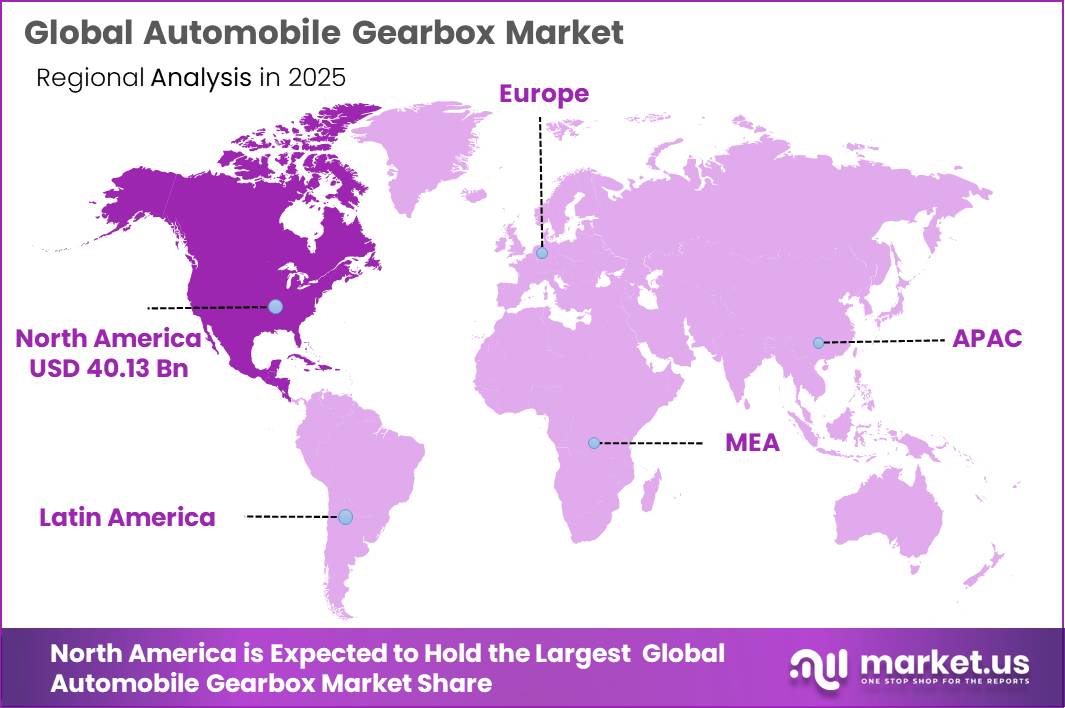

- Dominant region: North America with 45.20% share, valued at USD 40.1 Billion

Global passenger vehicle production recovered past 94 million units in 2024, directly lifting OEM gearbox procurement volumes across all transmission types. This production rebound confirms that OEM sourcing pipelines are active and expanding. Suppliers positioned for multi-speed automatic and hybrid transmission platforms gain the most from this volume recovery.

In Europe, only about 32% of new cars produced in 2023 had manual transmissions. This shift away from manual gearboxes accelerated OEM investment into automatic and automated alternatives. Transmission suppliers that have already diversified away from manual-only product lines are better positioned to capture replacement and new-fitment demand in European markets.

Commercial vehicle fleet expansion across Asia-Pacific is sustaining demand for heavy-duty manual and AMT gearboxes. This structural demand pattern keeps volume-driven suppliers active even as passenger car transmission preferences shift. Investors tracking long-term gearbox revenue should monitor commercial vehicle production cycles in China and India as separate demand levers from passenger car trends.

Gearbox Type Analysis

Manual Transmission dominates with 41.60% due to high fitment in emerging market vehicles.

In 2025, Manual Transmission held a dominant market position in the By Gearbox Type segment of the Automobile Gearbox Market, with a 41.60% share. This dominance reflects persistent fitment in cost-sensitive markets across Asia and Latin America. However, declining European adoption signals that this segment faces long-term volume pressure as automatic alternatives become more affordable at scale.

Intelligent Manual Transmission held 20.00% of the gearbox type segment. This category bridges conventional manual operation with electronic clutch assistance, reducing driver effort without requiring full automation. Fleet operators and commercial vehicle buyers in mid-tier markets favor this option for its lower acquisition cost relative to full automatics, making it a viable transition technology in price-sensitive geographies.

Automated Manual Transmission captured 15.00% of the segment. AMT systems use actuators to automate gear selection on existing manual architectures, lowering production cost versus purpose-built automatics. According to our reserach, AMT adoption is rising in cost-sensitive emerging markets replacing traditional manuals, confirming this sub-segment as a direct beneficiary of the global manual-to-automatic transition.

In February 2026, ZF Friedrichshafen AG and BMW signed a long-term agreement for supply and ongoing development of 8-speed automatic transmissions through the late 2030s, demonstrating that premium OEMs are committing to multi-speed automatic platforms over the long term.

Fuel Type Analysis

ICE dominates with 69.40% due to volume leadership across global vehicle parc.

In 2025, ICE held a dominant market position in the By Fuel Type segment of the Automobile Gearbox Market, with a 69.40% share. Internal combustion engine vehicles still represent the majority of global vehicle production and registration. This share level guarantees that multi-gear transmission demand remains the market baseline through the forecast period, particularly in commercial and emerging market applications.

HEV held 20.00% of the fuel type segment. Hybrid powertrains require sophisticated transmission systems that integrate motors, planetary gearsets, clutches, and electronic controls, which raises average transmission value per vehicle. This positions HEV as a high-margin growth area for gearbox suppliers capable of producing mechatronically integrated units rather than purely mechanical assemblies.

BEV accounted for 10.60% of the fuel type segment. Battery electric vehicles typically use single-speed reduction units, which reduces revenue per vehicle for traditional multi-gear transmission suppliers. This structural compression means that BEV share growth directly competes with conventional gearbox revenue, making powertrain diversification a strategic priority for Tier-1 suppliers over the forecast period.

Vehicle Type Analysis

SUV dominates with 41.70% due to sustained global consumer preference for high-riding vehicles.

In 2025, SUV held a dominant market position in the By Vehicle Type segment of the Automobile Gearbox Market, with a 41.70% share. SUVs typically carry higher-torque powertrain requirements and greater all-wheel-drive fitment rates, which favor automatic and dual-clutch transmission systems over manual alternatives. This mix drives higher average gearbox selling prices within the SUV sub-segment compared to hatchback and sedan platforms.

Hatchback and Sedan platforms remain a significant volume contributor to the global gearbox market. These body styles serve the highest production volumes in markets such as India, China, and Europe, where affordability drives fitment decisions toward manual, AMT, and CVT options. Suppliers targeting this sub-segment compete primarily on cost efficiency and production scalability rather than on premium feature differentiation.

LCV and HCV segments collectively anchor commercial vehicle gearbox demand. Light commercial vehicles in urban logistics and heavy commercial vehicles in long-haul freight each carry distinct transmission requirements, with AMT gaining ground in LCV and traditional manual or step-AT systems dominating HCV. Asia-Pacific fleet expansion makes these sub-segments a multi-year demand source that operates independently of passenger car powertrain trends.

Key Market Segments

By Gearbox Type

- Manual Transmission

- Intelligent Manual Transmission

- Automated Manual Transmission

- Automatic Transmission

- Continuously Variable Transmission

- Dual Clutch Transmission

By Fuel Type

- ICE

- HEV

- BEV

By Vehicle Type

- Hatchback/Sedan

- SUV

- LCV

- HCV

Drivers

Hybrid vehicles reached 34.4% of new vehicle registrations in Europe in 2025, exceeding the 17.4% BEV share and confirming hybrids as a mainstream powertrain rather than a compliance niche. Unlike fully electric vehicles, hybrids require e-CVTs, power-split units, and dedicated hybrid transmissions that integrate motors, planetary gearsets, clutches, and advanced electronic controls. This raises transmission value per vehicle and sustains multi-gear complexity across the European market.

Toyota sold 11.3 million vehicles in 2025, with hybrid models driving a large share of that volume. This scale confirms that hybrid-specific transmission demand is not speculative but tied to real OEM production commitments. Gearbox suppliers with qualified hybrid transmission programs capture embedded demand that does not depend on BEV adoption timelines, giving them revenue stability across multiple powertrain transition scenarios.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid drivetrain expansion lifting e-CVT and power-split transmission demand | +1.9% | EU, Japan, North America core, India urban PV | Short term (≤ 2 years) |

| China NEV scale-up accelerating single-speed reduction gear and e-axle gearbox volumes | +1.6% | China core, APAC export corridors, EU import-linked programs | Short term (≤ 2 years) |

| Euro 7 and post-2027 emissions compliance pushing higher-efficiency transmission calibration and lightweighting | +1.1% | EU core, UK adjacency, Turkey and North Africa supply spill-over | Medium term (2-4 years) |

| Fuel-economy and emissions rules sustaining multi-speed automatic and hybrid gearbox upgrades in ICE-heavy fleets | +0.9% | North America core, ASEAN, Latin America, Middle East | Medium term (2-4 years) |

| Commercial vehicle automation shifting manuals toward AMT and advanced step-AT systems | +0.8% | China core, India, Europe CV corridors, Brazil | Medium term (2-4 years) |

| Asia-led production localization improving gearbox sourcing density and supplier utilization | +0.7% | China, India, ASEAN, Eastern Europe spill-over | Long term (≥ 4 years) |

Restraints

Euro 7 standards apply from November 2026 for new vehicle types and from November 2027 for all new registrations. These regulations add engineering, validation, durability, and compliance requirements across combustion and hybrid vehicle platforms. Automakers are responding by extending existing transmission platforms and reducing new variant introductions, which compresses the new-program pipeline that Tier-1 gearbox suppliers depend on for forward revenue.

Dual-clutch transmissions deliver approximately 6% better fuel economy than 6-speed manual gearboxes. This performance advantage has accelerated OEM preference for DCT fitment on compliance-driven programs. However, the regulatory shift is also shortening transmission investment payback periods from approximately 6 to 7 years to 3 to 5 years in some cases, raising per-unit development costs and reducing financial incentives for launching entirely new ICE and hybrid gearbox families at scale.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Metal tariff inflation | -1.8% | North America core, Mexico, EU exporters | Short term (≤ 2 years) |

| ICE mix erosion | -2.1% | China, EU, North America, Japan-Korea | Medium term (2-4 years) |

| Euro 7 / CO2 compliance | -1.2% | EU, UK-linked Europe, Turkey supply base | Short term (≤ 2 years) |

| Supplier cash stress | -1.0% | EU, North America, Tier-2/3 APAC corridors | Medium term (2-4 years) |

| Critical minerals / chips | -0.9% | China-dependent APAC, EU, North America | Short term (≤ 2 years) |

| OEM production deferrals | -0.8% | Europe, North America, export APAC | Medium term (2-4 years) |

Challenges

Modern automatic, dual-clutch, and hybrid gearboxes now depend on transmission control units, sensors, power electronics, cybersecurity processes, and software update governance. UNECE R155 and R156 requirements have applied to newly produced vehicles since July 2024, forcing gearbox suppliers to maintain cybersecurity management systems, software update traceability, threat analysis, fleet monitoring, and supply-chain risk controls. This shifts part of the software-defined vehicle compliance burden directly onto transmission programs.

These regulatory demands create 10% to 18% longer software-hardware validation cycles and 15% to 25% more calibration variants across vehicle lines. Figures from the data show a recurring -0.9% drag on growth potential until suppliers standardize E/E interfaces, reduce ECU proliferation, and build multidisciplinary controls teams at scale. Suppliers without dedicated software validation infrastructure face both margin compression and program delay risks that compound across multi-platform transmission portfolios.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Tariffed metals volatility | -1.1% | North America core, EU export chains | Medium term (2-4 years) |

| Tier-2 financial fragility | -1.3% | EU supplier belt, North America, Japan | Medium term (2-4 years) |

| Electronics-software integration strain | -0.9% | EU regulatory hubs, North America, China, Korea | Long term (≥ 4 years) |

| Skilled mechatronics labor gap | -0.8% | Germany, Central Europe, US Midwest, Mexico, India | Long term (≥ 4 years) |

| Red Sea logistics rerouting | -0.7% | Europe-bound APAC corridors, MENA-linked routes | Short term (≤ 2 years) |

| Localization compliance complexity | -1.0% | USMCA corridor, China-centered sourcing networks | Medium term (2-4 years) |

Opportunities

Electrified vehicles reached 22% of light-duty sales in the U.S. in 2025, with hybrids proving more resilient than pure BEVs in consumer adoption. EPA data shows model-year 2023 EVs and PHEVs helped cut CO2 emissions by 11%, confirming regulatory and consumer support for architectures that still require sophisticated power-split and multi-mode gearing. This creates a confirmed demand signal for hybrid-dedicated gearbox development rather than speculative volume assumptions.

A gearbox supplier that shifts 12% to 18% of R&D and capital expenditure toward hybrid-dedicated units could open an adjacent addressable revenue pool equal to roughly 8% to 12% of its legacy passenger-car transmission sales by 2030. Average selling prices for hybrid-dedicated units run 10% to 20% above standard manual gearboxes. This margin premium, combined with integrated mechatronics complexity, creates a gross-margin expansion opportunity that pure manual or AMT programs cannot replicate.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Hybrid-dedicated gearsets | +1.9% | North America, EU, Japan, India | Short term (≤ 2 years) |

| Software-linked transmission revenue | +1.2% | North America core, EU, China, premium APAC | Short term (≤ 2 years) |

| E-axle and reducer roll-up | +2.4% | China, Korea, EU, North America | Medium term (2-4 years) |

| Commercial fleet electrified driveline | +1.6% | North America, EU, India, ASEAN | Medium term (2-4 years) |

| Remanufactured circular gearbox platforms | +1.4% | EU, North America | Medium term (2-4 years) |

| India export-localization hub | +1.7% | India, EU supply chain, North America, MEA | Long term (≥ 4 years) |

Regional Analysis

North America Dominates the Automobile Gearbox Market with a Market Share of 45.20%, Valued at USD 40.1 Billion

North America holds 45.20% of the global automobile gearbox market, valued at USD 40.1 Billion. The region’s dominance reflects its deep consumer preference for automatic transmissions across passenger cars, light trucks, and SUVs, which command premium gearbox ASPs. Aftermarket replacement demand for aging automatic transmissions in the large North American vehicle parc adds a second revenue layer beyond new vehicle fitment.

Europe represents the second-largest regional market, driven by regulatory pressure from Euro 7 compliance timelines and sustained hybrid vehicle adoption. Hybrids reached 34.4% of new vehicle registrations in Europe in 2025, outpacing BEV share and confirming that multi-speed and power-split transmissions retain high fitment relevance. Gearbox suppliers with hybrid-integrated product lines hold a structural pricing advantage in this market.

Asia-Pacific drives the highest production volume for gearbox units globally. China’s NEV scale-up is accelerating single-speed reducer and e-axle gearbox volumes, while India and ASEAN markets sustain demand for AMT and manual systems in cost-sensitive commercial and passenger car segments. This dual demand profile makes Asia-Pacific a critical market for suppliers serving both conventional and electrified powertrain platforms.

Latin America maintains steady gearbox demand anchored by Brazil and Mexico, where ICE vehicle production remains the dominant powertrain configuration. Fleet renewal cycles in these markets sustain manual and AMT fitment rates. This region offers lower regulatory complexity compared to Europe, giving suppliers operating here longer runway on existing product platforms before electrification mandates force portfolio changes.

Middle East and Africa represent an early-stage but volume-relevant market for gearbox suppliers. ICE vehicles dominate across both regions, and commercial fleet expansion in Gulf Cooperation Council countries supports sustained demand for heavy-duty manual and automatic transmissions. Electrification timelines here remain extended, meaning conventional multi-gear transmission demand remains commercially viable well into the forecast period.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Competitive Analysis

ZF Friedrichshafen AG holds a structurally strong position in the global gearbox market through its multi-speed automatic transmission platforms and long-term OEM partnerships. The company’s February 2026 agreement with BMW for 8-speed automatic transmission supply through the late 2030s locks in forward revenue visibility. This contract-backed demand base reduces ZF’s exposure to short-cycle program cancellations, giving it a cost-absorption advantage over smaller Tier-1 competitors without platform-level OEM commitments.

Aisin Seiki Co., Ltd. benefits from deep integration within Toyota’s hybrid powertrain ecosystem, which produced 11.3 million vehicle sales in 2025. This embedded position across Toyota’s e-CVT and power-split transmission programs insulates Aisin from open-market bidding pressure on hybrid gearbox platforms. However, Aisin’s concentration within a single OEM group creates platform dependency risk if Toyota accelerates its in-house transmission development for next-generation BEV architectures.

Key Players

- ZF Friedrichshafen AG

- Aisin Seiki Co., Ltd.

- Allison Transmission

- Eaton Corporation plc

- BorgWarner Inc.

- Schaeffler AG

- Magna International Inc.

- GKN Automotive Limited

- Voith Group

Recent Developments

- November 2025 – General Motors announced a USD 300 Million investment to expand 10-speed automatic transmission production capacity at its Romulus Propulsion Systems plant in Michigan.

- April 2026 – General Motors confirmed a combined USD 830 Million U.S. manufacturing investment that includes USD 300 Million to boost production of 10-speed transmissions at Romulus Propulsion Systems.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 88.8 Billion |

| Forecast Revenue (2035) | USD 144.6 Billion |

| CAGR (2026-2035) | 5.00% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Gearbox Type (Manual Transmission, Intelligent Manual Transmission, Automated Manual Transmission, Automatic Transmission, Continuously Variable Transmission, Dual Clutch Transmission); By Fuel Type (ICE, HEV, BEV); By Vehicle Type (Hatchback/Sedan, SUV, LCV, HCV) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | ZF Friedrichshafen AG, Aisin Seiki Co., Ltd., Allison Transmission, Eaton Corporation plc, BorgWarner Inc., Schaeffler AG, Magna International Inc., GKN Automotive Limited, Voith Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |