Global Application Performance Monitoring Suites Market Size, Share, Industry Analysis Report By Solution (Software, Services), By Deployment (Cloud, On-Premise), By Enterprise Size (Small and Medium-Sized Enterprises (SME's), Large Enterprises), By Access Type (Web APM, Mobile APM), By End-use (BFSI, E-Commerce, Manufacturing, Healthcare, Retail, IT and Telecommunications, Media and Entertainment, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Sept. 2025

- Report ID: 156960

- Number of Pages: 198

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaway

- Analysts’ Viewpoint

- Role of Generative AI in APM

- Emerging Trends

- U.S. APM Suites Market Size

- Solution Analysis

- Deployment Analysis

- Enterprise Size Analysis

- Access Type Analysis

- End-use Analysis

- Key Market Segments

- Key Regions and Countries

- Drivers

- Restraint

- Opportunities

- Challenges

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

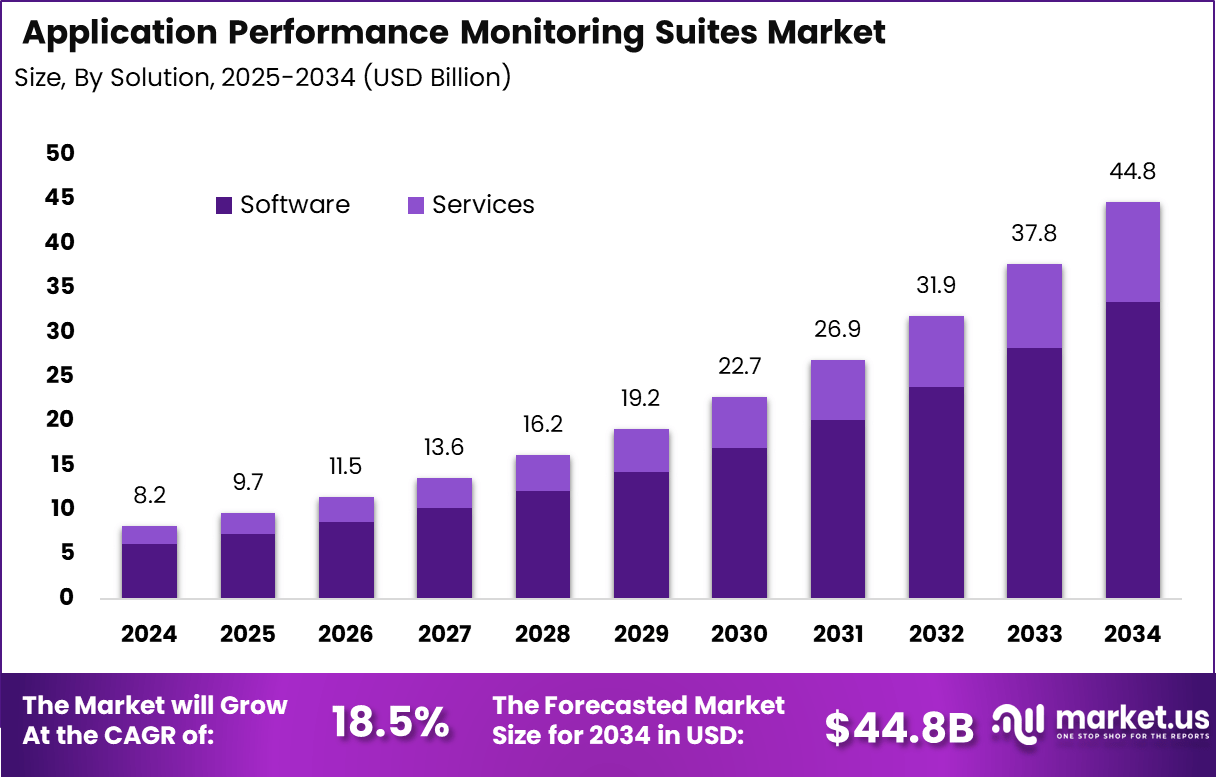

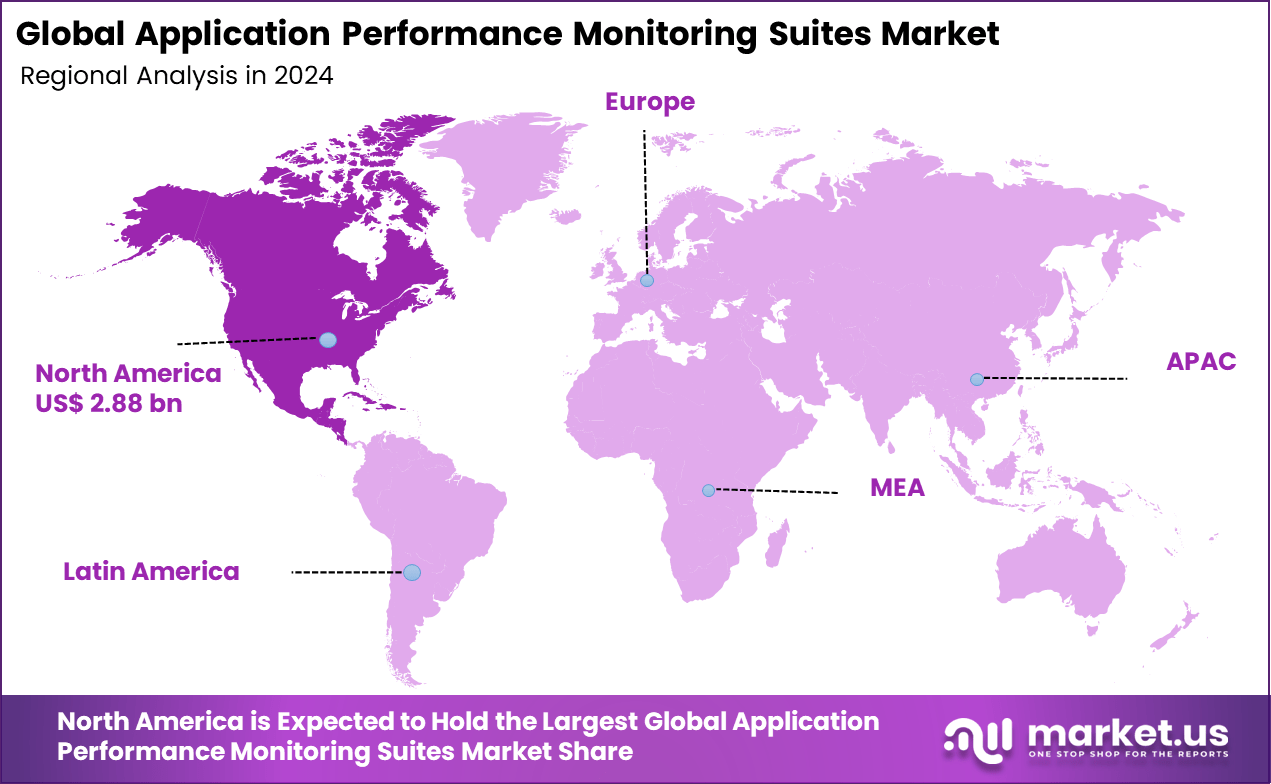

The Global Application Performance Monitoring Suites Market size is expected to be worth around USD 44.8 billion by 2034, from USD 8.2 billion in 2024, growing at a CAGR of 18.5% during the forecast period from 2025 to 2034. In 2024. North America held a dominant market position, capturing more than a 35.2% share, holding USD 2.88 billion in revenue.

Application Performance Monitoring (APM) Suites are essential tools that help organizations monitor, manage, and optimize the performance of their software applications. These suites track application behavior in real time across various platforms such as mobile, cloud, web, and enterprise software.

The core purpose of APM suites is to ensure applications run smoothly by minimizing downtime, identifying performance bottlenecks, and enhancing user experiences. As digital transformation accelerates across industries, these suites have become critical for maintaining business continuity and operational efficiency while supporting increasingly complex IT environments.

Growth in digital transformation efforts across sectors such as finance, healthcare, retail, and manufacturing has been a principal driver of APM Suite adoption. As organizations shift legacy systems to cloud-based and microservices architectures, the need to track health and performance in real time becomes essential.

For instance, in April 2025, New Relic announced a major revamp of its Global Partner Program, aimed at accelerating the adoption of its Application Performance Monitoring (APM) and observability platform. The updated program includes enhanced financial incentives, expanded training and certification pathways, and deeper technical support.

Key Takeaway

- In 2024, the Software segment held a dominant market position, capturing a 74.8% share of the Global Application Performance Monitoring Suites Market.

- In 2024, the On-Premise segment held a dominant market position, capturing a 65.2% share of the Global Application Performance Monitoring Suites Market.

- In 2024, the Large Enterprises segment held a dominant market position, capturing a 70.2% share of the Global Application Performance Monitoring Suites Market.

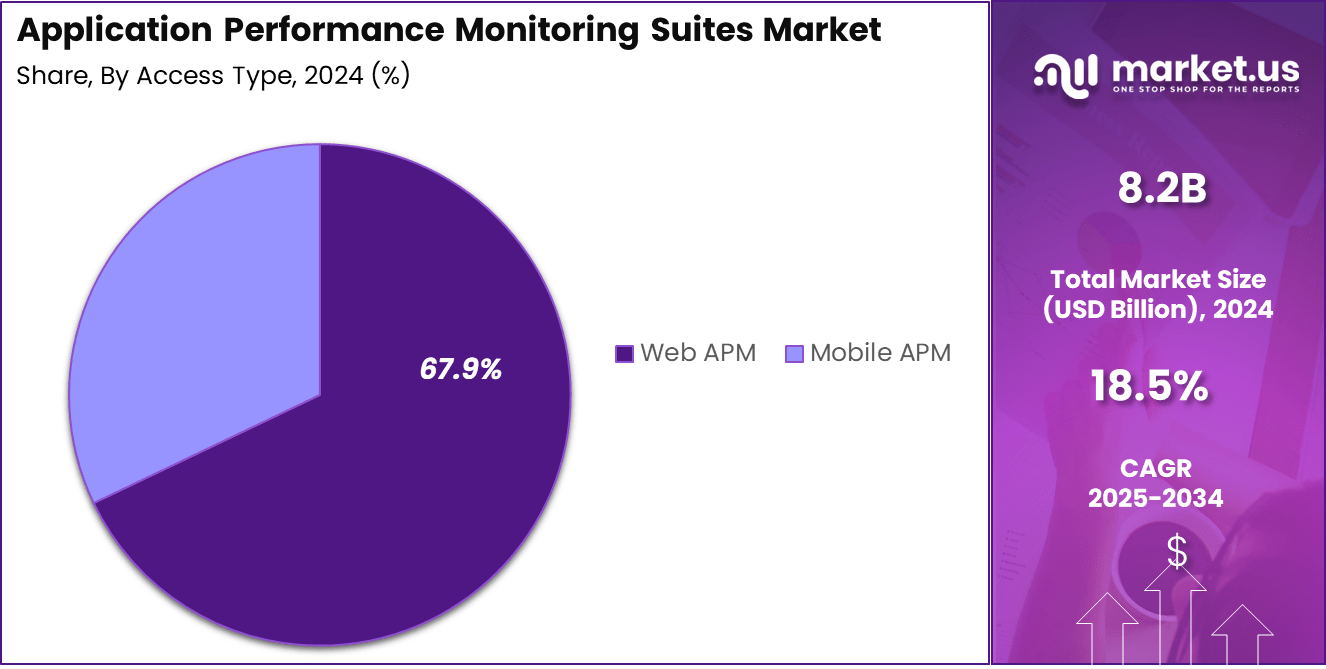

- In 2024, the Web APM segment held a dominant market position, capturing a 67.9% share of the Global Application Performance Monitoring Suites Market.

- In 2024, the IT and Telecommunications segment held a dominant market position, capturing a 28.7% share of the Global Application Performance Monitoring Suites Market.

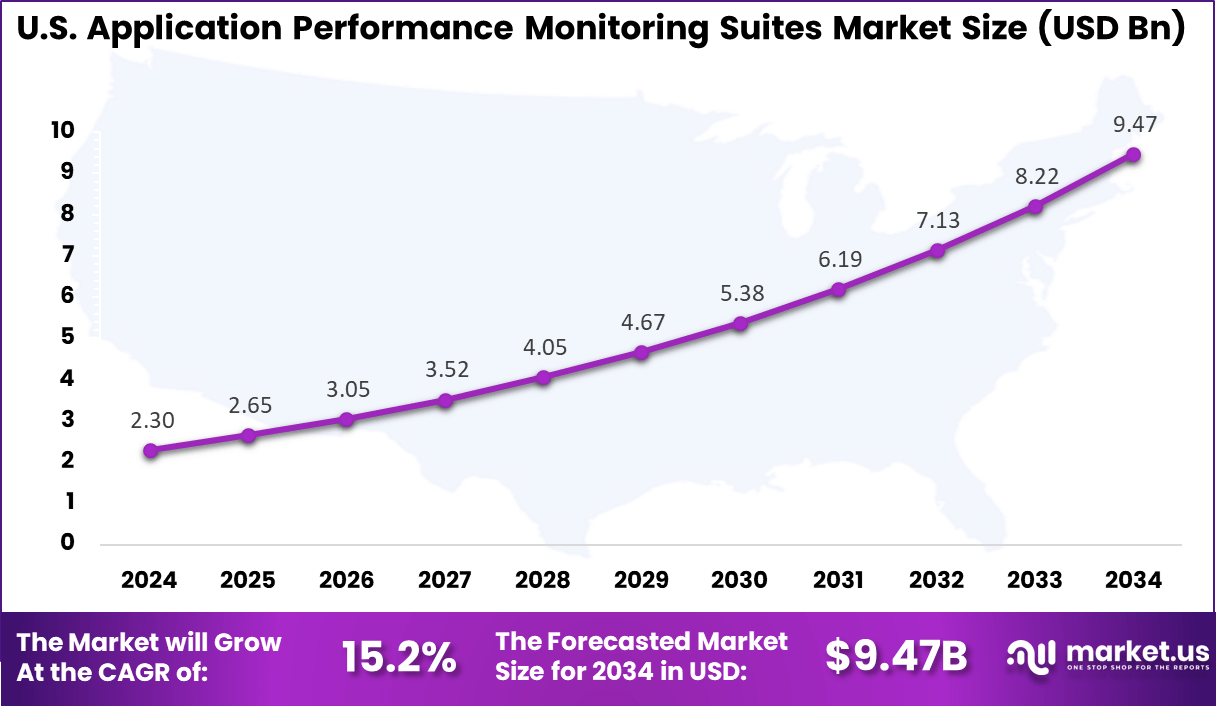

- The U.S. Application Performance Monitoring Suites Market was valued at USD 2.30 Billion in 2024, with a robust CAGR of 15.2%.

- In 2024, North America held a dominant market position in the Global Application Performance Monitoring Suites Market, capturing more than a 35.2% share.

Analysts’ Viewpoint

The integration of next‑generation technologies such as artificial intelligence, automation, edge analytics, and cloud computing has reshaped APM Suite capabilities. These advances enable smarter issue detection, predictive insights, and adaptable workflows, driving adoption across varied sectors including logistics, healthcare, and manufacturing.

Investment opportunities in the APM market are plentiful due to ongoing digital transformation trends. Investors are focusing on companies developing AI and ML-enhanced monitoring solutions, predictive analytics, and cloud-native capabilities. Emerging regions with accelerating digital adoption present strong growth potential. Strategic mergers and acquisitions are common as larger players seek to expand their technology portfolios and geographical footprint.

APM Suites deliver tangible benefits such as reduced application downtime, improved user satisfaction, and support for service‑level commitments. They empower capacity planning and root‑cause investigations, leading to more effective resource utilization. The value derived from prevention of performance issues and expedited response to incidents can be significant.

Role of Generative AI in APM

Key Points Description Natural Language Interaction Generative AI enables engineers to interact with monitoring data using natural language queries, simplifying complex data navigation. Predictive Issue Detection AI models predict potential application issues before they impact users, enabling proactive maintenance. Reduced Cognitive Load AI automates anomaly detection and correlates vast data points, reducing manual analysis effort. Streamlined Troubleshooting Generative AI assists in quickly identifying root causes by summarizing and highlighting key performance anomalies. Enhanced Observability AI integrates diverse telemetry data for clearer, actionable insights across complex distributed systems. Emerging Trends

Key Trends in APM Suites Description AI and Machine Learning Integration Increasing adoption of AI/ML for intelligent anomaly detection, predictive analytics, and automation. Cloud-Native & Hybrid Monitoring Suites optimized for microservices, containers, serverless, and hybrid cloud environments. User Experience Monitoring (UXM) Focus on tracking real user journeys across web, mobile, and multi-channel applications. Real-Time Analytics and Alerting Advanced dashboards and alerts for immediate issue detection and faster remediation. Security and Runtime Application Protection Combining performance monitoring with continuous security monitoring to ensure application safety. U.S. APM Suites Market Size

The market for Application Performance Monitoring Suites within the U.S. is growing tremendously and is currently valued at USD 2.30 Billion, the market has a projected CAGR of 15.2%. The market is growing rapidly due to the country’s accelerated adoption of cloud computing, DevOps practices, and AI-driven digital infrastructure.

U.S. enterprises, especially in finance, healthcare, and e-commerce, demand real-time insights to ensure application reliability and customer satisfaction. The surge in remote work and digital services has further intensified the need for continuous performance visibility. Additionally, strong investment in AI observability and cybersecurity integration is reinforcing the strategic value of APM solutions.

For instance, in May 2025, AppSignal secured a $22 million growth investment to accelerate its expansion within the U.S. Application Performance Monitoring (APM) Suites market. This move highlights U.S. dominance in the sector, fueled by strong investor confidence, a tech-forward business ecosystem, and high demand for developer-friendly, scalable APM solutions.

In 2024, North America held a dominant market position in the Global Application Performance Monitoring Suites Market, capturing more than a 35.2% share, holding USD 2.88 billion in revenue. This dominance is due to advanced digital infrastructure, early embrace of cloud computing and AI, and its dense concentration of technology-focused enterprises.

The region’s mature IT ecosystem, strong emphasis on user experience, and strict regulatory standards have heightened the need for real-time monitoring and application optimization. Moreover, substantial investments in DevOps practices, cybersecurity, and performance management solutions continue to position them as essential tools for ensuring operational agility and driving enterprise-wide digital transformation.

For instance, in August 2025, EXUS Renewables North America launched the EXUSiQ Performance Optimization Suite, debuting its AI-powered Pitch Power Tool aimed at enhancing operational efficiency across wind energy assets. This reflects a broader trend of North America’s dominance in Application Performance Monitoring (APM) Suites, driven by early digital adoption, strong AI integration, and cross-sector demand for real-time performance analytics.

Solution Analysis

In 2024, the Software segment held a dominant market position, capturing a 74.8% share of the Global Application Performance Monitoring Suites Market. This dominance is due to the growing demand for scalable, cloud-native, and AI-integrated monitoring solutions that provide real-time visibility across complex IT environments.

Software-based APM tools offer greater flexibility, faster deployment, and advanced analytics capabilities, making them essential for DevOps, cloud migration, and agile development initiatives. Their ability to optimize performance and enhance user experience drives continued market leadership.

For Instance, in April 2025, AWS announced the launch of Amazon CloudWatch Application Signals for AWS Lambda, enhancing its Application Performance Monitoring (APM) software capabilities. This new feature provides automatic, standardized observability for serverless applications by capturing critical metrics such as latency, error rates, and throughput without manual configuration.

Deployment Analysis

In 2024, the On-Premise segment held a dominant market position, capturing a 65.2% share of the Global Application Performance Monitoring Suites Market. This dominance is due to the strong demand from industries with stringent data security, compliance, and control requirements.

Organizations in sectors such as finance, healthcare, and government continue to prioritize on-premise deployments to maintain full ownership of infrastructure and sensitive data. Additionally, legacy system dependencies and limited cloud readiness in some enterprises have sustained the need for robust, internally managed APM solutions that offer high configurability and control.

For instance, in November 2024, AWS introduced Application Signals for AWS Lambda, marking a strategic expansion of cloud-native, built-in Application Performance Monitoring (APM) capabilities. While this innovation targets serverless and cloud environments, it highlights the contrasting demand in the on-premise APM segment, where organizations with strict data control, compliance, and legacy system requirements continue to favor internally hosted monitoring solutions.

Enterprise Size Analysis

In 2024, the Large Enterprises segment held a dominant market position, capturing a 70.2% share of the Global Application Performance Monitoring Suites Market. This dominance is due to their complex, large-scale IT infrastructures and greater financial capacity to invest in advanced monitoring tools.

Large enterprises prioritize real-time visibility, performance optimization, and security across distributed systems, especially amid ongoing digital transformation initiatives. Their adoption of multi-cloud environments, DevOps practices, and AI-driven operations further drives demand for comprehensive, scalable APM solutions to ensure uptime and operational efficiency.

For Instance, in June 2020, SolarWinds enhanced its Application Performance Monitoring (APM) Suite to better serve the complex needs of large enterprises. The update introduced streamlined monitoring capabilities across hybrid environments, enabling IT teams to gain end-to-end visibility into application health and performance.

Access Type Analysis

In 2024, the Web APM segment held a dominant market position, capturing a 67.9% share of the Global Application Performance Monitoring Suites Market. This dominance is due to the widespread adoption of web-based applications across industries.

This dominance is due to the increasing need for real-time monitoring of user experiences, page load times, and transaction flows in customer-facing digital platforms. Web APM solutions offer seamless deployment, broad compatibility, and actionable insights, making them essential for organizations focused on optimizing performance, uptime, and user satisfaction in web environments.

For Instance, in February 2025, at its annual Perform 2025 conference, Dynatrace unveiled major advancements in Web Application Performance Monitoring (APM), introducing new AI-powered features to enhance digital experience monitoring. These updates focused on real-time user journey insights, proactive anomaly detection, and deeper observability across front-end web layers.

End-use Analysis

In 2024, The IT and Telecommunications segment held a dominant market position, capturing a 28.7% share of the Global Application Performance Monitoring Suites Market. This dominance is due to the sector’s reliance on high-performance, always-on digital infrastructure. This dominance is due to the critical need for real-time visibility, low-latency service delivery, and uninterrupted connectivity in managing vast networks and complex applications.

With the rapid adoption of 5G, cloud-native technologies, and AI-driven operations, IT and telecom providers increasingly depend on APM suites to ensure system reliability, optimize performance, and enhance user experience.

For Instance, in June 2023, Cisco announced its acquisition of Accedian, a Canada-based firm specializing in network performance monitoring and analytics, to strengthen its capabilities in the telecommunications and Application Performance Monitoring (APM) space. This move aims to enhance Cisco’s ability to deliver end-to-end observability across increasingly complex telecom networks.

Key Market Segments

By Solution

- Software

- Services

- Integration & Deployment

- Training & Education

- Support & Maintenance

By Deployment

- Cloud

- On-Premise

By Enterprise Size

- Small and Medium-Sized Enterprises (SME’s)

- Large Enterprises

By Access Type

- Web APM

- Mobile APM

By End-use

- BFSI

- E-Commerce

- Manufacturing

- Healthcare

- Retail

- IT and Telecommunications

- Media and Entertainment

- Others

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Drivers

Accelerated Digital Transformation and Cloud Adoption

Enterprises across finance, healthcare, retail, and manufacturing are rapidly digitizing operations, shifting from monolithic architectures to cloud-native platforms and microservices. This transition amplifies application complexity and necessitates robust, real-time performance monitoring to ensure system reliability, user experience, and business continuity.

As organizations embrace hybrid and multi-cloud environments, APM suites are increasingly vital in providing end-to-end visibility, accelerating incident response, and optimizing performance across dynamic, distributed infrastructures.

For instance, in August 2025, NTT DATA and Microsoft announced a strategic collaboration to accelerate AI-driven cloud transformation across Asia-Pacific. This initiative supports enterprises in modernizing IT environments and adopting cloud-native architectures. As digital complexity increases, the demand for Application Performance Monitoring (APM) Suites grows in parallel.

Restraint

Perceived High Costs and Integration Complexity

One significant restraint slowing APM adoption is the perception of high costs associated with these solutions. Deploying APM suites involves expenses beyond software licenses, including implementation, ongoing maintenance, and integration with existing IT infrastructures. For small and medium-sized enterprises, these costs can be a major barrier, especially when budgets are tight or resources are limited.

Moreover, integrating APM tools within complex and diverse IT environments can be challenging and time-intensive. Organizations may face difficulties in aligning APM solutions with their existing workflows and legacy systems, leading to slower adoption rates. Data privacy concerns also arise, as performance monitoring involves collecting sensitive application data, adding another layer of caution for some organizations.

Opportunities

Expansion in the Asia-Pacific and Emerging Markets

Asia-Pacific represents a high-growth frontier for APM adoption, driven by rapid cloud migration, digital public infrastructure, and a burgeoning base of tech-driven SMEs. Markets such as India, Southeast Asia, and China are witnessing accelerated digital transformation across sectors, creating demand for scalable, localized performance monitoring solutions.

Vendors that tailor offerings to regional regulatory frameworks, pricing sensitivity, and multilingual environments stand to capture substantial market share and establish early leadership in these fast-evolving digital ecosystems.

For instance, in August 2025, New Relic announced a strategic partnership with M.Tech, a leading cybersecurity and network performance distributor, to drive regional expansion across Asia-Pacific. This collaboration aims to extend New Relic’s intelligent Application Performance Monitoring (APM) and observability platform to enterprises in Southeast Asia, leveraging M.Tech’s robust reseller network.

Challenges

Maintaining Monitoring Effectiveness in Agile Environments

Agile methodologies, CI/CD pipelines, and microservice deployments introduce constant changes to application environments, making performance monitoring increasingly complex. Maintaining consistent visibility and diagnostic precision amid frequent code releases and infrastructure updates is a persistent challenge.

APM tools must evolve to deliver adaptive instrumentation, automated anomaly detection, and context-aware alerting. Ensuring monitoring resilience in high-velocity development cycles is essential to sustaining application performance, customer experience, and development velocity in modern digital enterprises.

For instance, in December 2020, AWS and NetApp jointly addressed a core challenge in Application Performance Monitoring (APM), maintaining monitoring effectiveness in agile and cloud-native environments. As development cycles accelerate under DevOps and CI/CD models, traditional monitoring tools often fail to keep pace with frequent code changes and infrastructure updates.

Key Players Analysis

One of the leading players in the market, in May 2025, Datadog expanded its Application Performance Monitoring (APM) and AI capabilities through the acquisition of Eppo, a leading feature experimentation and analytics platform. This strategic move strengthens Datadog’s observability suite by integrating advanced A/B testing, feature flagging, and experimentation tools directly into its monitoring workflows.

Top Key Players in the Market

- Datadog, Inc.

- Dynatrace, Inc.

- New Relic

- SolarWinds Worldwide, LLC.

- Zoho Corporation Pvt. Ltd.

- AppDynamics

- Splunk, Inc.

- LogicMonitor, Inc.

- Hound Technology, Inc.

- Platform.sh SAS

- ServiceNow

- Thundra

- Others

Recent Developments

- In March 2025, Dynatrace advanced its AI-powered observability portfolio with the acquisition of Metis, a specialist in database performance analytics. This integration enhances Dynatrace’s ability to deliver context-rich, AI-driven insights into database health, enabling developers and SREs to proactively detect, diagnose, and resolve performance issues.

Report Scope

Report Features Description Market Value (2024) USD 8.2 Bn Forecast Revenue (2034) USD 44.8 Bn CAGR(2025-2034) 18.5% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics, nd Emerging Trends Segments Covered By Solution (Software, Services), By Deployment (Cloud, On-Premise), By Enterprise Size (Small and Medium-Sized Enterprises (SME’s), Large Enterprises), By Access Type (Web APM, Mobile APM), By End-use (BFSI, E-Commerce, Manufacturing, Healthcare, Retail, IT and Telecommunications, Media and Entertainment, Others) Regional Analysis North America: US, Canada; Europe: Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific: China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America: Brazil, Mexico, Rest of Latin America; Middle East & Africa: South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Datadog, Inc., Dynatrace, Inc., New Relic, SolarWinds Worldwide, LLC., Zoho Corporation Pvt. Ltd., AppDynamics, Splunk, Inc., LogicMonitor, Inc., Hound Technology, Inc., Platform.sh SAS, ServiceNow, Thundra, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to choose from: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users, Printable PDF)  Application Performance Monitoring Suites MarketPublished date: Sept. 2025add_shopping_cartBuy Now get_appDownload Sample

Application Performance Monitoring Suites MarketPublished date: Sept. 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- Datadog, Inc.

- Dynatrace, Inc.

- New Relic

- SolarWinds Worldwide, LLC.

- Zoho Corporation Pvt. Ltd.

- AppDynamics

- Splunk, Inc.

- LogicMonitor, Inc.

- Hound Technology, Inc.

- Platform.sh SAS

- ServiceNow

- Thundra

- Others

Our Clients

- 156960

- Sept. 2025