Quick Navigation

Report Overview

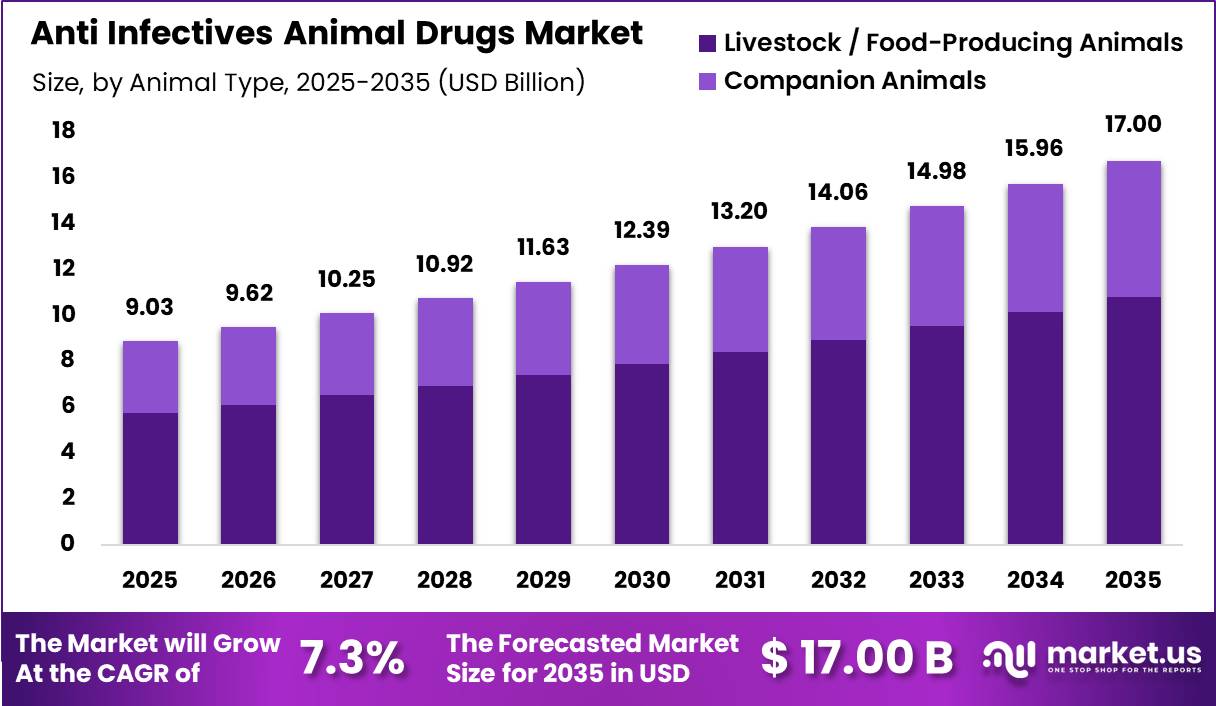

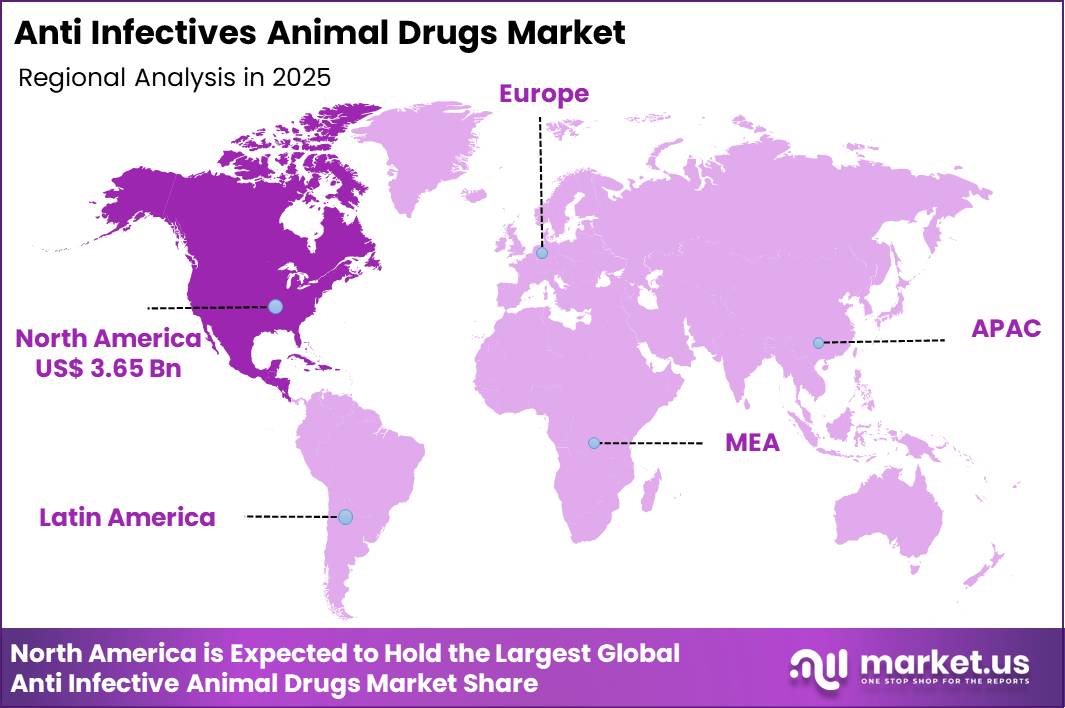

Global Anti Infectives Animal Drugs Market size is expected to be worth around US$ 17.00 Billion by 2035 from US$ 9.03 Billion in 2025, growing at a CAGR of 7.3% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 40.5% share, holding USD$ 3.65 Billion in revenue.

The anti infectives animal drugs market is experiencing sustained growth driven by the increasing need to manage infectious diseases across both commercial livestock operations and companion animal healthcare. Rising pressure on producers to maintain herd health, improve productivity, and reduce economic losses associated with bacterial, viral, fungal, and parasitic infections continues to support demand for anti-infective therapeutics.

At the same time, increasing veterinary expenditure and higher standards of animal care are expanding treatment adoption in companion animals, creating opportunities for advanced and species-specific anti-infective solutions.

Competitive dynamics are increasingly shaped by portfolio diversification, antimicrobial stewardship requirements, and investments in next-generation animal health products. Leading manufacturers are strengthening their positions through product innovation, regulatory approvals, and strategic expansion initiatives aimed at addressing evolving disease challenges.

- In July 2024, Merck Animal Health completed the acquisition of Elanco Animal Health’s aqua business, enhancing its capabilities in aquatic animal disease management and expanding its presence in the rapidly developing aquaculture health segment.

Such strategic investments reflect the industry’s focus on broadening anti-infective offerings across multiple animal categories and production systems. Technology advancement is also influencing market development, with companies focusing on targeted therapies, improved formulations, and integrated disease management approaches that combine prevention and treatment strategies.

Growing regulatory attention toward responsible antimicrobial use is encouraging manufacturers to develop more efficient and specialized products while supporting long-term sustainability objectives across animal production and veterinary healthcare sectors. As a result, innovation, regulatory compliance, and species-specific treatment effectiveness are becoming critical factors shaping competitive positioning within the market.

Key Takeaways

- Market Size: Global Anti Infectives Animal Drugs Market size is expected to be worth around US$ 17.00 Billion by 2035 from US$ 9.03 Billion in 2025.

- Market Share: The market is growing at a CAGR of 7.3% during the forecast period from 2026 to 2035.

- Animal Type Analysis: Livestock / Food-Producing Animals dominated the market, constituting 63.6% of the total market share, driven by the scale of global food production systems and the critical role of anti-infective drugs in herd health management and food safety compliance.

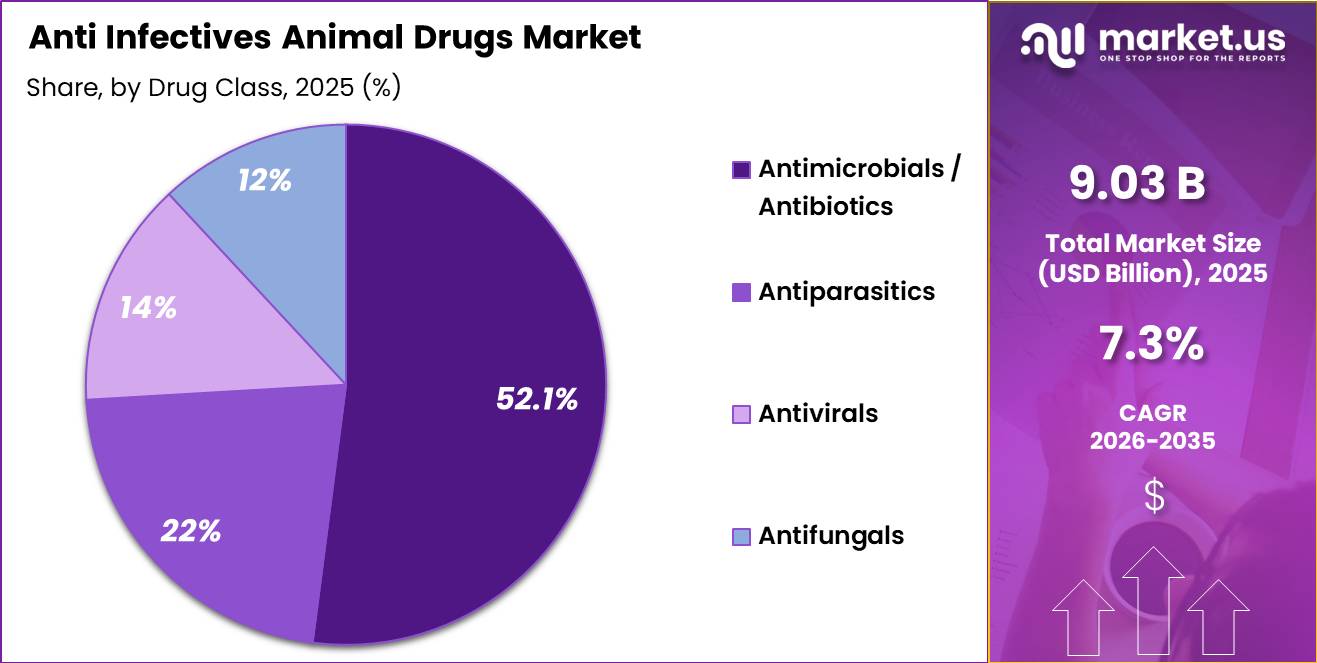

- Drug Class Analysis: Antimicrobials / Antibiotics dominated the Anti-Infectives Animal Drugs Market, with a substantial market share of around 52.0%, anchored by the broadest spectrum of approved indications across animal species and production systems globally.

- Mode of Administration Analysis: Oral administration dominated with a 42.0% market share, driven by ease of large-scale in-feed and in-water delivery in commercial poultry and swine production operations.

- Distribution Channel Analysis: Veterinary Hospitals & Clinics dominated with a 70.0% market share, reflecting the prescription-required regulatory framework for most anti-infective products and the central role of veterinary professionals in treatment authorization and dispensing.

- Regional Analysis: In 2025, North America was the most dominant region in the Anti-Infectives Animal Drugs market, accounting for 40.5% of total global revenue.

Animal Type Analysis

Livestock / Food-Producing Animals Represent the Key Revenue-Generating Segment in the Global Anti-Infectives Animal Drugs Market.

The livestock/food-producing animals segment accounted for 63.6% of the global anti-infectives animal drugs market, making it the largest revenue-generating category. The segment’s dominance is primarily driven by the economic importance of disease prevention and treatment in commercial animal production, where infectious disease outbreaks can significantly impact productivity, mortality rates, feed conversion efficiency, and overall farm profitability.

Large-scale poultry, cattle, swine, and aquaculture operations rely extensively on anti-infective therapies to maintain animal health, ensure consistent production output, and comply with food safety and biosecurity standards.

The commercial nature of livestock production creates a concentrated and recurring demand for anti-infective products, particularly in intensive farming systems where high animal densities increase the risk of disease transmission. The widespread use of antibiotics, antiparasitics, antivirals, and antifungals across multiple food-producing species further strengthens the segment’s market position.

Industry participants continue to expand investments in livestock health solutions to address evolving disease challenges and support production efficiency which reflects the growing importance of anti-infective and health management products across food-producing animal sectors.

While livestock remains the primary demand center, the companion animals segment is steadily expanding due to increasing pet ownership, rising veterinary healthcare expenditure, and greater adoption of advanced infection management therapies for dogs, cats, and horses, supporting broader market growth opportunities.

Drug Class Analysis

Antimicrobials / Antibiotics Represent the Leading Drug Class Segment in the Global Anti-Infectives Animal Drugs Market

The antimicrobials/antibiotics segment accounted for 52.0% of the global anti-infectives animal drugs market, making it the leading drug class category. Its dominance is attributed to the broad applicability of antibiotics in treating a wide range of bacterial infections across livestock and companion animals.

Tetracyclines, penicillins, macrolides, and fluoroquinolones remain widely utilized due to their proven efficacy, established safety profiles, and suitability for multiple species and production systems. The segment benefits from the critical role antibiotics play in reducing disease-related production losses, improving animal welfare, and supporting operational efficiency in commercial farming environments.

Demand is particularly strong in poultry, cattle, and swine production, where bacterial infections can rapidly spread and adversely affect productivity and profitability. The widespread integration of antimicrobial therapies into herd and flock health management programs continues to reinforce segment leadership despite increasing regulatory emphasis on responsible antibiotic use.

Manufacturers are also investing in innovative formulations and stewardship-focused solutions to enhance treatment effectiveness while aligning with evolving regulatory requirements.

- In September 2024, Phibro Animal Health Corporation expanded the availability of its livestock health products across key international markets, supporting producers with disease management solutions designed to improve animal health and production performance.

Meanwhile, antiparasitics, antivirals, and antifungals are steadily gaining traction as producers adopt more comprehensive approaches to disease prevention and treatment, particularly in response to emerging infectious disease challenges and changing animal health requirements.

Mode of Administration Analysis

Oral Administration Represents the Dominant Mode of Administration in the Global Anti-Infectives Animal Drugs Market

The oral administration segment accounted for 42.0% of the global anti-infectives animal drugs market, driven by its convenience, cost-effectiveness, and suitability for large-scale treatment programs. Oral formulations can be administered through feed or water, enabling efficient disease management across poultry, swine, cattle, and aquaculture operations while reducing labor requirements and animal handling. The segment also benefits from strong adoption in companion animal healthcare, where ease of administration and improved treatment compliance are key purchasing considerations.

Manufacturers are increasingly focusing on innovative oral delivery systems to enhance compliance and therapeutic effectiveness.

- In February 2025, Zoetis Inc. expanded its market presence and cattle anti-infective line by acquiring the commercial marketing rights for Loncor® 300 (florfenicol). Injectable and topical formulations continue to serve important roles in severe infections and targeted treatments, but oral products remain the preferred option across a broad range of veterinary applications due to their scalability and ease of use.

This strategic move underscores the industry’s focus on providing versatile anti-infective formulations that offer veterinarians and livestock producers broad-spectrum tools to efficiently manage severe respiratory diseases and control outbreaks.

Distribution Channel Analysis

Veterinary Hospitals & Clinics Represent the Dominant Distribution Channel in the Global Anti-Infectives Animal Drugs Market.

Veterinary hospitals & clinics accounted for 70.0% of the global anti-infectives animal drugs market distribution, driven primarily by strict prescription-only regulatory frameworks governing antimicrobials, antivirals, and key antiparasitic therapies across major markets.

Regulations such as EU Regulation 2019/6 and the U.S. Veterinary Feed Directive (VFD) mandate veterinary diagnosis and authorization for most anti-infective products, structurally positioning clinics as the primary distribution gateway. This regulatory control is reinforced by antimicrobial stewardship policies that prioritize controlled usage, limiting direct farm-level or retail procurement and ensuring clinical oversight in both livestock and companion animal treatment pathways.

The channel’s dominance is further strengthened by the integrated “consultation-to-dispensing” model, particularly in companion animal care, where diagnosis, prescription, and drug supply occur within veterinary facilities, reinforcing compliance and treatment adherence.

Consolidation of veterinary practice networks has also enabled standardized procurement and stronger manufacturer alignment through in-clinic formularies. Industry leaders such as Zoetis, Boehringer Ingelheim, and Merck Animal Health continue to reinforce prescribing influence through targeted veterinary engagement strategies.

- In April 2025, Boehringer Ingelheim International GmbH launched an expanded veterinary professional education program on antimicrobial stewardship best practices for production animal practitioners across European markets, supporting compliance with EU Regulation 2019/6 while strengthening engagement with veterinary prescribers who remain central to anti-infective drug selection and dispensing decisions.

Key Market Segments

By Animal Type

- Livestock / Food-Producing Animals

- Poultry

- Cattle (Beef and Dairy)

- Pigs (Swine)

- Aquaculture (Fish and Seafood)

- Companion Animals

- Dogs

- Cats

- Horses

By Drug Class

- Antimicrobials / Antibiotics

- Tetracyclines

- Penicillins

- Macrolides

- Fluoroquinolones

- Antiparasitics

- Antivirals

- Antifungals

By Mode of Administration

- Oral

- Parenteral (Injectable)

- Topical

By Distribution Channel

- Veterinary Hospitals & Clinics

- Retail & Veterinary Pharmacies

- Online Platforms

Drivers

AMR Stewardship Shifts Demand Toward Premium Targeted Therapies

Antimicrobial resistance AMR stewardship is reshaping veterinary and human anti infective markets by shifting demand away from high volume, broad use antibiotics toward more targeted, regulated, and higher value therapies.

The U.S. Food and Drug Administration 2024 to 2028 stewardship strategy, along with 2026 guidance tightening duration of use requirements, is reinforcing prescription only, veterinarian supervised use in food producing animals, limiting growth promotion and routine prophylactic applications.

At the global level, the World Organisation for Animal Health reports that antimicrobial use intensity has begun to decline, while certain high risk molecules remain under regulatory pressure due to resistance concerns. This combination is accelerating a shift away from commodity antibiotic volume toward structured, indication specific treatment protocols.

Commercially, this transition favors differentiated products such as injectables, combination therapies, and species specific formulations, supported by stronger veterinary oversight and clearer labeling. The market model is moving from kilogram driven sales toward value based therapeutic dosing per treated animal, increasing the importance of compliance, stewardship alignment, and clinical positioning.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Disease pressure in poultry, swine, cattle and aquaculture | +2.1% | North America core, EU, China, India, Brazil, Southeast Asia | Short term |

| AMR stewardship shifts demand to premium targeted therapies | +1.7% | North America core, EU core, advanced APAC, selective LATAM | Medium term |

| Vaccination, biosecurity and herd-health protocols widen prescription intensity | +1.3% | EU, North America, Brazil, India, ASEAN corridors | Medium term |

| Surveillance digitization and tighter duration labeling improve compliant usage | +1.0% | U.S., EU/EEA, Canada, Australia, Japan | Short term |

| Protein demand and livestock productivity economics support therapeutic spend | +1.5% | APAC core, Latin America export belts, Middle East import-dependent markets, Africa spill-over | Long term |

| Aquaculture intensification and species-specific anti-infective need | +0.9% | Norway, Chile, China, Vietnam, India, Indonesia | Medium term |

Challenges

Tightening AMR Stewardship as a Structural Constraint on Anti Infective Growth

Global antimicrobial resistance AMR stewardship is introducing a long term structural constraint on animal and human anti infective markets by limiting broad, preventive use and shifting demand toward targeted, diagnostics led therapies. Since 2017, the World Health Organization has advised against routine use of medically important antibiotics for growth promotion and disease prevention in healthy food animals, a position reinforced by regulatory action in multiple regions.

In parallel, agencies such as the U.S. Food and Drug Administration and the European Union have expanded prescription requirements, restricted certain antimicrobial classes to human use, and tightened rules around medicated feed and prophylactic use. Similar frameworks are emerging in countries such as India, contributing to a global convergence toward stricter stewardship.

These changes reduce volume growth by limiting broad, low cost antibiotic applications, potentially cutting demand in some segments by 20 to 40 %, while increasing complexity per prescription. Companies face higher compliance burdens, including pharmacovigilance, residue testing, and label maintenance, raising operating costs by roughly 10 to 15 %.

Additionally, 3 to 5 % of R&D investment is increasingly redirected toward alternatives such as vaccines, probiotics, and non antibiotic therapies.Overall, tightening stewardship is estimated to create a persistent drag of about 1.5 % points on market growth relative to unconstrained volume expansion, while favoring portfolios that integrate diagnostics, targeted therapies, and stewardship aligned pricing models.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Tightening AMR stewardship | -1.5% | North America, EU, India, China | Long term (≥ 4 years) |

| Volatile API & logistics costs | -1.2% | Global pharma trade lanes | Medium term (2-4 years) |

| Tariff & trade policy uncertainty | -0.9% | U.S., China, India export hubs | Medium term (2-4 years) |

| Veterinary talent & diagnostics gap | -0.8% | Emerging livestock regions | Long term (≥ 4 years) |

| Data, surveillance & compliance load | -0.7% | Regulated markets, large producers | Medium term (2-4 years) |

| Farm-level biosecurity & adoption friction | -0.6% | Smallholder & fragmented farms | Long term (≥ 4 years) |

Restraints

Accelerating Antimicrobial Resistance Pressure as a Structural Market Drag

Antimicrobial resistance (AMR) is increasingly constraining the animal anti-infectives market by reducing drug efficacy and prompting stricter regulatory and stewardship responses that limit volume growth. The World Health Organization estimates that bacterial AMR was directly responsible for about 1.27 million deaths in 2019 and contributed to nearly 5 million, underscoring its scale as a global health and policy priority.This growing burden is driving coordinated “One Health” policies that restrict medically important antimicrobials in livestock and shift treatment toward narrower-spectrum, diagnostic-led use.

At the same time, resistance trends in pathogens such as Salmonella and Campylobacter are increasing treatment failures, pushing adoption of combination therapies and vaccines while reducing reliance on routine antibiotic use.Operationally, this raises per-case treatment costs by 15–25% but suppresses overall volumes as producers invest more heavily in biosecurity and preventive measures.

It also compresses margins for legacy antibiotics, increases regulatory risk around older approvals, and forces R&D investment toward narrower or pathogen-specific agents with longer development timelines and higher costs.Collectively, accelerating AMR pressure is estimated to reduce baseline market CAGR by roughly 2.2 % points over 2026–2030, as structurally constrained volume growth outweighs any pricing or mix upgrades toward higher-value therapies.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating antimicrobial resistance pressure | -2.2% | Global, EU core, North America, APAC livestock hubs | Long term (≥ 4 years) |

| Stricter stewardship and duration-of-use rules | -1.9% | North America core, EU, selected LATAM & APAC exporters | Medium term (2-4 years) |

| Declining antibiotic volumes in food animals | -1.4% | EU, UK, OECD producers, emerging exporters | Medium term (2-4 years) |

| Cost inflation in compliant manufacturing | -1.1% | Global, higher in EU & US | Short–Medium term (≤ 4 years) |

| Supply chain and API sourcing volatility | -0.9% | APAC corridors, global downstream markets | Short term (≤ 2 years) |

| Slow uptake of non-antibiotic alternatives | -0.8% | Global, especially emerging markets | Long term (≥ 4 years) |

Opportunity

Precision, Data Driven Stewardship Platforms

Digital stewardship platforms represent a shift from treating AMR regulation as a constraint to monetizing compliance and efficiency gains in livestock health systems. While global antimicrobial use in animals reached over 60,000 tonnes in earlier estimates and remains under pressure from productivity growth in livestock production, most stewardship efforts today are still non digital and poorly monetized.

By integrating farm level surveillance, prescription decision support, and dosing optimization, these platforms can reduce antimicrobial use per unit of output by 20 to 30 %, lower treatment failures by 10 to 15 %, and reduce disease incidence by 5 to 10 %. The commercial model shifts from commodity drug sales to recurring software and services revenue, typically charged per animal at USD 3 to 5 in intensive production systems such as poultry and swine.

At scale, this creates a multi billion dollar opportunity, USD 2 to 3 billion by 2030, for software plus services layered on top of traditional animal health products, with higher margins of 25 to 35 % than conventional anti infectives. Value is increasingly tied to measurable reductions in antibiotic usage and improved productivity outcomes, aligning with the U.S. Food and Drug Administration and the World Health Organization stewardship expectations.

Overall, as regulation tightens and veterinary oversight expands, early adopters of precision stewardship platforms could add roughly 2 % points to market CAGR by converting compliance requirements into subscription based, outcome linked revenue streams, particularly in North America and Europe where digital adoption and regulatory enforcement are most advanced.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Precision, data-driven stewardship platforms | +2.0% | North America, EU, selected APAC | Short term (≤ 2 years) |

| Non-antibiotic anti-infective adjacencies | +1.8% | EU, APAC emerging, LatAm | Medium term (2-4 years) |

| Integrated livestock health-productivity bundles | +1.5% | APAC emerging, Africa, LatAm | Medium term (2-4 years) |

| AMR-linked outcome-based contracting | +1.2% | North America core, EU | Long term (≥ 4 years) |

| Localized manufacturing and supply-chain regionalization | +1.0% | APAC emerging, Africa, LatAm | Medium term (2-4 years) |

| Genomic and microbiome-guided anti-infective innovation | +1.3% | North America, EU, high-value APAC | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Trade Fragmentation and API Supply Chain Regionalization.

The anti-infectives animal drugs market is increasingly shifting toward near-shoring and regionalized sourcing to mitigate trade fragmentation, protectionist tariffs, and geopolitical vulnerabilities in centralized Asian Active Pharmaceutical Ingredient (API) production hubs.

To insulate critical antibiotic and antiparasitic portfolios from localized customs disputes and transport choke points, major animal health innovators throughout 2025 and 2026 aggressively diversified their supply chains by establishing secondary API procurement networks and manufacturing footprints within the Americas and Western Europe.

This strategic shift from just-in-time logistics to security-focused, just-in-case stock buffering successfully insulates essential veterinary pharmaceutical pipelines from international policy shocks, though it structurally raises baseline manufacturing costs for finished anti-infective formulations.

Food Sovereignty and National Biosecurity Mandates.

Escalating geopolitical focus on national food sovereignty and agricultural supply chain resilience against transboundary diseases is fundamentally restructuring livestock anti-infective procurement. Governments across major food-producing blocs are enforcing stricter domestic disease-surveillance mandates and veterinary oversight to reduce dependence on volatile meat and drug import pipelines, converting anti-infectives from standard farm inputs into highly regulated, state-tracked components of national biosecurity.

Consequently, multinational animal health firms must form deep operational partnerships with regional agricultural cooperatives and state-backed veterinary distribution channels to align with localized food-security protection targets and successfully navigate increasingly protected international agricultural trade landscapes.

Regional Analysis

North America Held the Largest Share of the Global Anti-Infectives Animal Drugs Market.

North America accounted for 40.5% of the global anti-infectives animal drugs market, making it the leading regional market due to its advanced veterinary healthcare infrastructure, large-scale commercial livestock production systems, and high companion animal healthcare expenditure.

The region benefits from strong regulatory enforcement of antimicrobial stewardship, widespread adoption of prescription-based veterinary care, and the presence of major global animal health companies, all of which support structured and sustained demand for anti-infective therapies across livestock and companion animal segments.

Continued capital investment is further reinforcing its leadership position, with a May 2025 Merck Animal Health announcement of an $ 895 million expansion of its manufacturing and R&D facilities in Kansas, strengthening domestic production capacity and enhancing supply chain resilience for animal health products.

Europe remains a highly regulated and sustainability-focused market shaped by strict antimicrobial usage controls under EU Regulation 2019/6, while Asia Pacific is emerging as the fastest-growing region driven by livestock intensification and expanding aquaculture demand.

Latin America shows steady growth supported by export-oriented protein production systems, whereas the Middle East & Africa region is gradually expanding due to increasing food security initiatives and ongoing livestock sector modernization.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global anti-infectives animal drugs market is moderately concentrated, with a small group of multinational leaders capturing the majority of branded revenues across both production animal and companion animal segments. Zoetis Inc., Boehringer Ingelheim International GmbH, Merck Animal Health, and Elanco Animal Health Incorporated form the top-tier competitive core, driven by extensive species coverage, broad anti-infective portfolios, and deep integration with veterinary prescriber networks.

Zoetis maintains the strongest competitive position due to its unmatched global regulatory footprint and diversified product leadership across antimicrobials, antiparasitics, and companion animal therapeutics, while Boehringer Ingelheim and Merck Animal Health strengthen their positions through complementary production animal and companion animal franchises supported by strong veterinary engagement and lifecycle management strategies.

The mid-to-lower tier of the market is characterized by differentiated regional specialists and cost-competitive manufacturers that compete through formulation innovation, niche therapeutic focus, and geographic penetration strategies.

Companies such as Ceva Santé Animale S.A., Virbac S.A., Dechra Pharmaceuticals Plc, and Vetoquinol S.A. focus on specialty companion animal and targeted production animal segments, while Phibro Animal Health Corporation, Huvepharma AD, and Norbrook Laboratories Ltd. maintain strong positions in feed additives, generics, and high-volume livestock antimicrobials.

Emerging market participants including Cipla Limited (Cipla Animal Health), Hester Biosciences Ltd., and Neogen Corporation contribute through regional production animal supply, biologicals, and adjacent diagnostic ecosystems, collectively intensifying competition in price-sensitive and rapidly expanding veterinary markets.

Top Key Players

- Zoetis Inc.

- Boehringer Ingelheim International GmbH

- Merck & Co., Inc. (Merck Animal Health)

- Elanco Animal Health Incorporated

- Ceva Santé Animale S.A.

- Virbac S.A.

- Dechra Pharmaceuticals Plc

- Vetoquinol S.A.

- Bayer AG (Animal Health Division)

- Phibro Animal Health Corporation

- Huvepharma AD

- Cipla Limited (Cipla Animal Health)

- Norbrook Laboratories Ltd.

- Hester Biosciences Ltd.

- Neogen Corporation

Key Development

- In February 2026, Boehringer Ingelheim International GmbH launched an integrated antimicrobial stewardship digital platform for European veterinary production animal practitioners, enabling real-time antibiogram tracking, treatment protocol optimization, and EU Regulation 2019/6 compliance documentation across managed livestock populations.

- In January 2026, Elanco Animal Health Incorporated received European Medicines Agency approval for an expanded label indication for its long-acting injectable antibiotic in swine, broadening the approved treatment indication beyond respiratory disease to include additional bacterial infection types in European pork production systems.

- In December 2025, Merck Animal Health announced a strategic partnership with a precision livestock farming technology company to integrate antimicrobial treatment decision support into automated herd health monitoring systems, enabling evidence-based anti-infective treatment decisions triggered by individual animal health data in commercial beef and dairy cattle operations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 9.03 Billion |

| Forecast Revenue (2035) | US$ 17.00 Billion |

| CAGR (2026-2035) | 7.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Animal Type (Livestock / Food-Producing Animals, Companion Animals), By Drug Class (Antimicrobials / Antibiotics, Antiparasitics, Antivirals, Antifungals), By Mode of Administration (Oral, Parenteral (Injectable), Topical), By Distribution Channel (Veterinary Hospitals & Clinics, Retail & Veterinary Pharmacies, Online Platforms) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Zoetis Inc., Boehringer Ingelheim International GmbH, Merck & Co. Inc. (Merck Animal Health), Elanco Animal Health Incorporated, Ceva Santé Animale S.A., Virbac S.A., Dechra Pharmaceuticals Plc, Vetoquinol S.A., Bayer AG (Animal Health Division), Phibro Animal Health Corporation, Huvepharma AD, Cipla Limited (Cipla Animal Health), Norbrook Laboratories Ltd., Hester Biosciences Ltd., Neogen Corporation, Others. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |