Quick Navigation

Report Overview

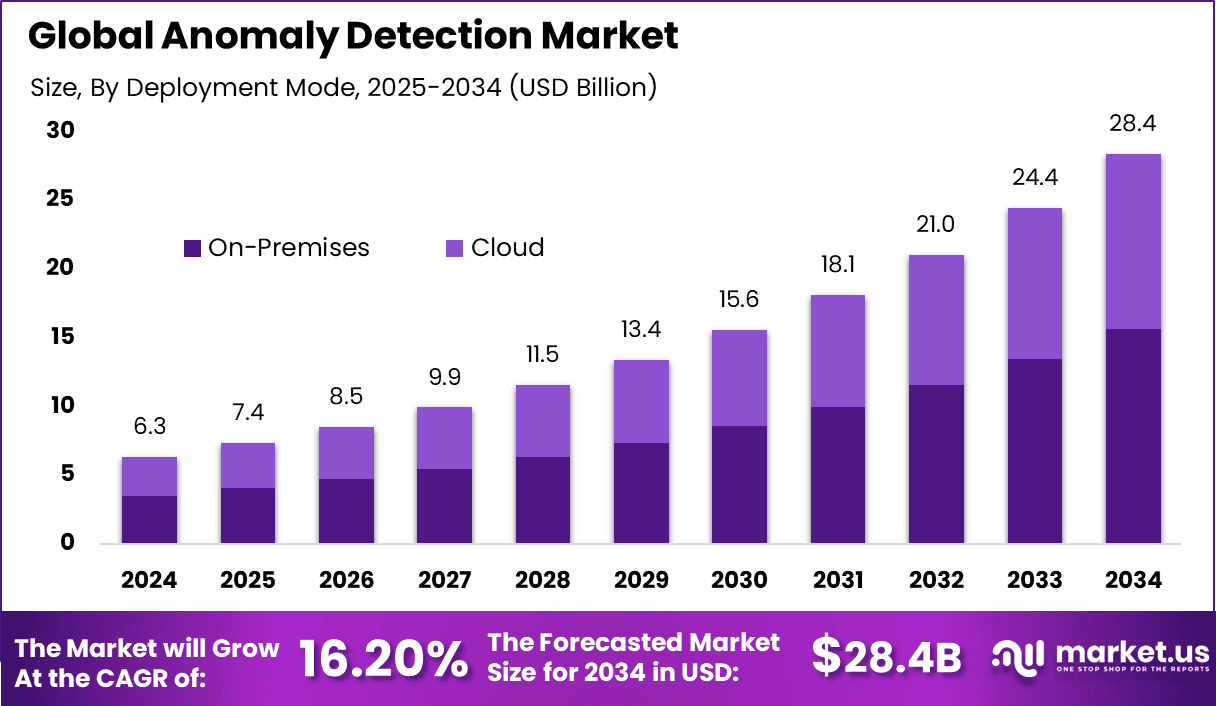

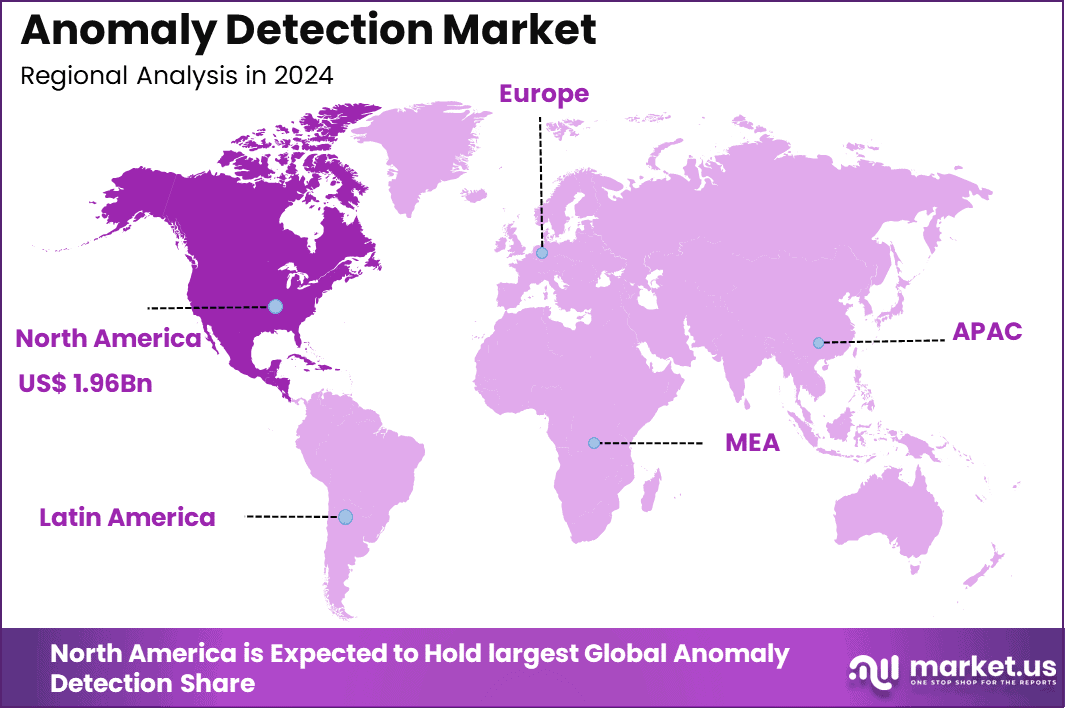

The Global Anomaly Detection Market generated USD 6.3 billion in 2024 and is predicted to register growth from USD 7.4 billion in 2025 to about USD 28.4 billion by 2034, recording a CAGR of 16.20% throughout the forecast span. In 2024, North America held a dominan market position, capturing more than a 31.1% share, holding USD 16.2 Billion revenue.

The anomaly detection market refers to a group of advanced analytical systems designed to identify unusual patterns, unexpected behavior, or deviations in data across digital and physical environments. These systems are widely used in cybersecurity, financial monitoring, healthcare analytics, and industrial operations. As organizations increasingly rely on data driven processes, the ability to automatically detect irregularities has become essential for maintaining system integrity and operational continuity.

The strongest driver behind this market is the rising cost and frequency of digital risk. IBM reported that the global average cost of a data breach was USD 4.4 million in 2025, and it linked the decline from the prior year to faster identification and containment supported by AI-enhanced security tools. Verizon’s 2025 breach findings also showed that ransomware appeared in 44% of breaches reviewed and that its presence increased by 37% from the previous year, while system intrusion breaches remained heavily tied to ransomware activity.

Demand for anomaly detection is broadening because abnormal pattern detection is no longer limited to cybersecurity. In fraud management, the ACFE’s anti-fraud technology benchmarking report found that anomaly detection and exception reporting were already used by 57% of organizations, showing that the technology has moved into mainstream control environments.

In banking, FATF guidance states that transaction monitoring is an essential part of identifying suspicious activity and notes that automated systems may be the only realistic method where large transaction volumes exist. In manufacturing, NIST has formally demonstrated behavioral anomaly detection for industrial control systems because cyberattacks and abnormal machine behavior can threaten both property and human safety.

Top Market Takeaways

- By component, the solutions segment dominates with 70.1% market share, reflecting strong demand for integrated anomaly detection software and tools.

- By deployment mode, the on-premise segment holds 55%, indicating preference for in-house data control, especially in sensitive sectors.

- By technology, big data analytics leads with 41% share, driven by the need to analyze massive datasets for anomalies effectively.

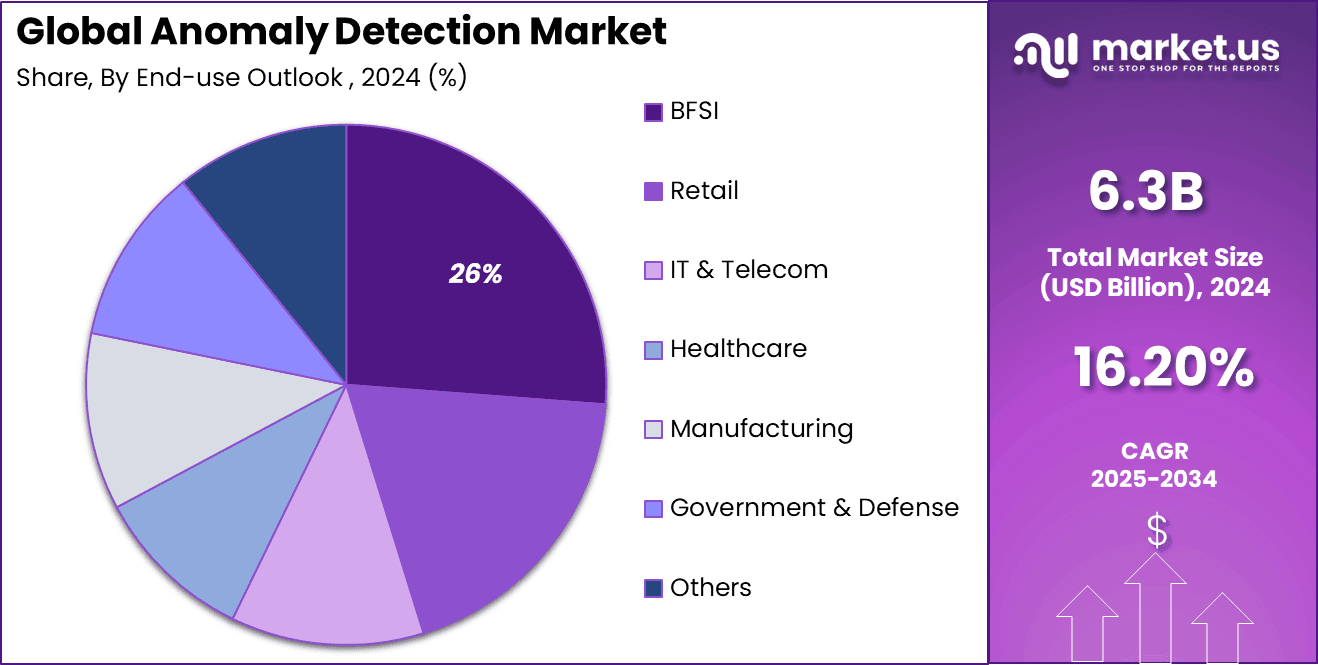

- By end-use, the BFSI (Banking, Financial Services, and Insurance) segment accounts for 26.2% of the market, highlighting the critical role of anomaly detection in fraud prevention and security.

- Regionally, North America captures approximately 31.1% of the global market share, supported by advanced IT infrastructure and high cybersecurity investments.

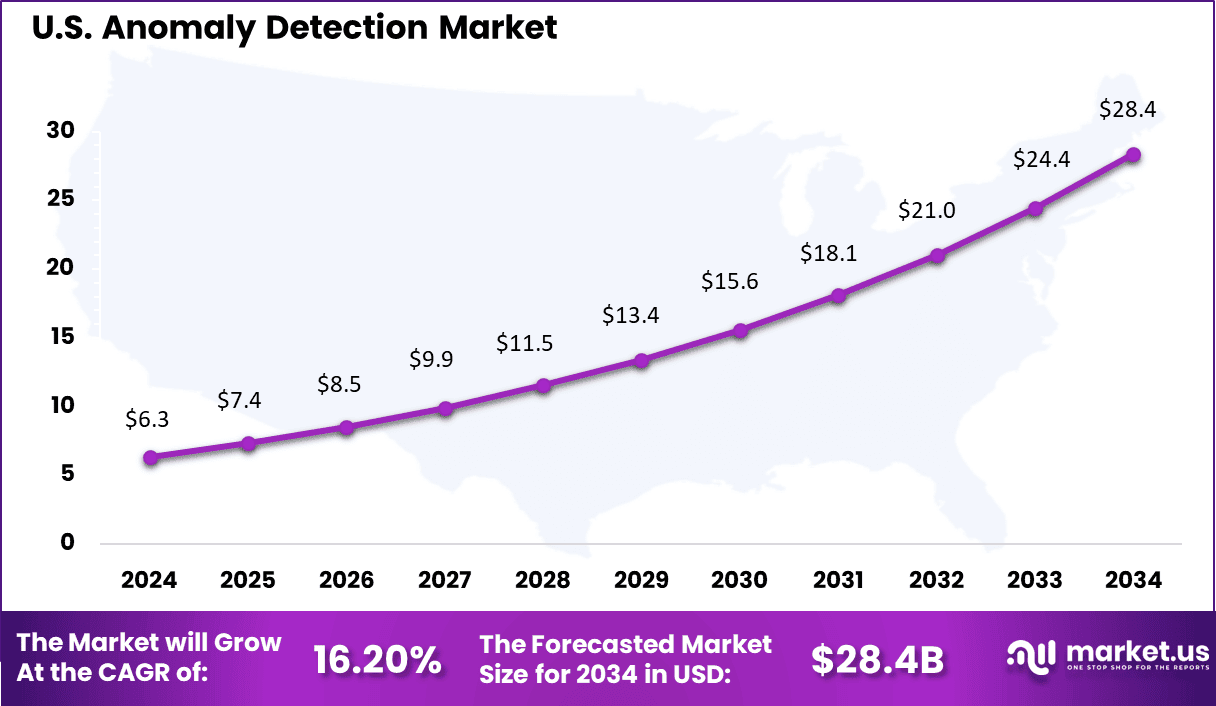

- The U.S. anomaly detection market size is approximately USD 2.3 billion in 2025, showcasing strong growth driven by increasing cyber threats and regulatory demand.

- The market is growing rapidly with a CAGR of 16.2%, reflecting rising adoption of AI, machine learning, and big data technologies in anomaly detection.

By Component

In 2024, the solutions segment dominated the anomaly detection market with a share of 70.1%, driven by the increasing need for automated systems that can identify unusual patterns in large datasets. Organizations are adopting solution-based platforms that combine machine learning, statistical modeling, and real-time monitoring to detect anomalies across operations. These tools help improve fraud detection, system monitoring, and cybersecurity response.

The segment’s strength is further supported by the rising demand for proactive risk management and predictive analytics. Businesses are focusing on deploying advanced solutions that can detect irregularities before they escalate into critical issues. These platforms offer scalability, automation, and integration with enterprise systems, making them highly effective. This has positioned solutions as the core component in anomaly detection deployments.

By Deployment

In 2024, the on-premise segment held a 55% share, reflecting strong preference for in-house deployment in data-sensitive environments. Organizations dealing with confidential data, such as financial institutions and government agencies, prioritize on-premise systems for better control and security. This deployment model allows enterprises to manage infrastructure, data access, and compliance requirements internally. As a result, it remains a preferred choice in highly regulated sectors.

The segment’s continued relevance is also linked to concerns around data privacy and external security risks. Many organizations believe that on-premise deployment offers stronger protection against unauthorized access. Existing legacy systems and infrastructure investments further support its adoption. Despite the growth of cloud technologies, on-premise solutions continue to play a significant role in the market.

By Technology

In 2024, the big data analytics segment captured 41% share, driven by the growing need to analyze large and complex datasets for anomaly detection. Big data technologies enable organizations to process high volumes of structured and unstructured data in real time. This capability is essential for identifying patterns and detecting anomalies across multiple systems. As businesses generate more data, the importance of big data analytics continues to increase.

The segment’s growth is further supported by advancements in data processing frameworks and analytics tools. Organizations are leveraging big data platforms to enhance detection accuracy and reduce response times. These technologies allow for deeper insights into operational performance and potential risks. This has strengthened the role of big data analytics in modern anomaly detection systems.

By End-Use Outlook

In 2024, the BFSI segment held 26.2% share, reflecting strong demand for anomaly detection solutions in financial services. The sector relies heavily on these systems to detect fraudulent transactions, monitor account activities, and prevent financial crimes. With increasing digital transactions and online banking, the need for real-time anomaly detection has become critical. This has driven significant investment in advanced detection technologies within the BFSI sector.

The segment’s leadership is also supported by strict regulatory requirements and the need to maintain customer trust. Financial institutions are adopting advanced analytics and machine learning tools to improve detection accuracy. Continuous monitoring systems help identify suspicious activities quickly and reduce potential losses. This has positioned BFSI as a key end-user in the anomaly detection market.

By Region

In 2024, North America accounted for 31.1% of the anomaly detection market, supported by strong adoption of advanced analytics and cybersecurity solutions. The region has a mature digital ecosystem, which drives demand for technologies that can monitor and protect data in real time. Organizations across industries are investing heavily in anomaly detection to improve operational efficiency and reduce risks. This has contributed to consistent market growth.

The regional dominance is further supported by high awareness of cybersecurity threats and strong regulatory frameworks. Companies in North America are early adopters of data-driven technologies, including machine learning and big data analytics. Continuous innovation and investment in technology have strengthened the region’s position. These factors collectively support sustained market expansion.

In 2024, the United States anomaly detection market reached USD 6.3 billion and is growing at a CAGR of 16.2%, reflecting strong demand for advanced data monitoring solutions. The country’s large digital economy and high data generation levels create a need for efficient anomaly detection systems. Organizations are deploying these solutions to enhance security, detect fraud, and improve operational performance. This has driven consistent adoption across sectors.

The growth in the U.S. is also supported by increasing investments in artificial intelligence and analytics technologies. Businesses are focusing on improving data visibility and real-time decision-making capabilities. Rising cybersecurity risks and regulatory requirements further encourage adoption. As a result, the United States remains a key contributor to the global anomaly detection market.

Key Market Segments

By Component

- Solution

- Network Behavior Anomaly Detection

- User Behavior Anomaly Detection

- Services

- Professional Services

- Managed Services

By Deployment

- Cloud

- On-Premise

By Technology

- Machine Learning & Artificial Intelligence

- Big Data Analytics

- Business Intelligence & Data Mining

By End-use Outlook

- BFSI

- Retail

- IT & Telecom

- Healthcare

- Manufacturing

- Government & Defense

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Emerging Trends Analysis

The anomaly detection market is moving toward real-time and autonomous analytics systems that can identify irregular patterns instantly across large and complex datasets. The use of advanced machine learning and deep learning models has improved the ability to detect subtle anomalies that were previously difficult to identify using rule-based systems. These models are increasingly being deployed across cloud environments, enabling continuous monitoring of data streams from multiple sources such as applications, networks, and connected devices.

Another important trend is the growing integration of anomaly detection with edge computing and IoT ecosystems. As connected devices generate large volumes of real-time data, there is an increasing need for localized anomaly detection to reduce latency and improve response time. This has led to the development of lightweight and efficient models that can operate directly on edge devices, supporting applications such as industrial monitoring, smart cities, and autonomous systems.

Driver Analysis

The primary driver of the anomaly detection market is the increasing need for advanced cybersecurity solutions. Organizations are facing a rising number of sophisticated cyber threats that cannot be detected using traditional security methods. Anomaly detection systems help identify unusual behavior patterns in networks and user activities, enabling early detection of potential security breaches and reducing the risk of data loss.

In addition, the rapid growth in data generation across industries is significantly contributing to market demand. Businesses are generating large volumes of structured and unstructured data from digital platforms, transactions, and connected devices. Anomaly detection tools are essential for analyzing this data in real time, helping organizations improve operational efficiency, identify risks, and make informed decisions based on data insights.

Restraint Analysis

One of the key restraints in the anomaly detection market is the dependency on high-quality and well-structured data. Machine learning models require accurate datasets for effective training and performance. Poor data quality or incomplete datasets can lead to incorrect anomaly detection results, which reduces system reliability and limits adoption in critical use cases.

Another restraint is the complexity involved in deploying and managing these systems. Implementing anomaly detection solutions often requires integration with multiple data sources and existing IT infrastructure. This process can be resource-intensive and may require skilled professionals, which can be a barrier for small and medium-sized organizations.

Opportunity Analysis

Significant opportunities are emerging from the increasing adoption of predictive maintenance in industrial sectors. Anomaly detection systems are widely used to monitor equipment performance and identify early signs of failure. This helps organizations reduce downtime, lower maintenance costs, and improve overall productivity, especially in manufacturing, energy, and transportation industries.

Furthermore, the expansion of cloud computing and digital transformation initiatives is creating new growth opportunities. Cloud-based anomaly detection solutions offer scalability, flexibility, and cost efficiency, making them accessible to a wider range of organizations. These solutions enable real-time data analysis and support advanced use cases such as fraud detection, system monitoring, and business intelligence.

Challenge Analysis

A major challenge in the anomaly detection market is the occurrence of false positives. Systems may generate alerts for activities that are not actually harmful, which can lead to unnecessary investigations and reduced operational efficiency. Managing and minimizing false alerts is essential to ensure the effectiveness of anomaly detection systems.

Another challenge is the need for continuous model updates due to changing data patterns. As user behavior and system environments evolve, anomaly detection models must be regularly retrained to maintain accuracy. This ongoing requirement increases operational complexity and demands continuous investment in data management and model optimization.

Competitive Analysis

The Anomaly Detection Market is led by global cloud and enterprise technology providers offering scalable AI-driven monitoring platforms. Amazon Web Services, Inc., Microsoft Corporation, and International Business Machines Corporation provide advanced analytics and real-time anomaly detection solutions. Cisco Systems, Inc. and Broadcom, Inc. enhance network and infrastructure security. These companies focus on AI integration.

Cybersecurity and observability-focused vendors play a critical role in detecting irregular patterns and system risks. Splunk, Inc., Dynatrace, LLC, and LogRhythm, Inc. deliver real-time analytics and automated alerting systems. Trend Micro, Inc. and SAS Institute, Inc. strengthen predictive detection capabilities. These firms focus on behavioral analytics. Their solutions reduce operational risks. This improves system performance and security outcomes.

Emerging and service-oriented players contribute to innovation in AI-based anomaly detection. Anodot Ltd., Happiest Minds, and GURUCUL offer specialized analytics and monitoring tools. Dell Technologies, Inc. and Hewlett Packard Enterprise Company support infrastructure-level detection solutions. These companies enhance automation and scalability. Their innovations support growing enterprise demand. This competitive landscape drives continuous advancement in anomaly detection technologies.

Top Key Players in the Market

- Amazon Web Services, Inc.

- Anodot Ltd.

- Broadcom, Inc.

- Cisco Systems, Inc.

- Dell Technologies, Inc.

- Dynatrace, LLC

- GURUCUL

- Happiest Minds

- Hewlett Packard Enterprise Company

- International Business Machines Corp.

- LogRhythm, Inc.

- Microsoft Corp.

- SAS Institute, Inc.

- Splunk, Inc.

- Trend Micro, Inc.

Recent Developments

- January, 2026 – Splunk Enterprise Security added ML-powered anomaly baselines across 100 metrics. SOC teams detect insider threats 85% faster via behavioral analytics. Fortune 100 firms reduced alert fatigue 60%.

- February, 2026 – Dynatrace Davis AI engine expanded to Kubernetes anomaly detection. Davis Copilot resolves root causes autonomously 70% of incidents. Cloud-native apps gained 99.99% availability.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 6.3 Bn |

| Forecast Revenue (2034) | USD 28.4 Bn |

| CAGR(2025-2034) | 16.20% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Solution (Network Behavior Anomaly Detection, User Behavior Anomaly Detection), Services (Professional Services, Managed Services)], By Deployment (Cloud, On-Premise), By Technology (Machine Learning & Artificial Intelligence, Big Data Analytics, Business Intelligence & Data Mining), By End-use Outlook (BFSI, Retail, IT & Telecom, Healthcare, Manufacturing, Government & Defense, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Amazon Web Services, Inc., Anodot Ltd., Broadcom, Inc., Cisco Systems, Inc., Dell Technologies, Inc., Dynatrace, LLC, GURUCUL, Happiest Minds, Hewlett Packard Enterprise Company, International Business Machines Corp., LogRhythm, Inc., Microsoft Corp., SAS Institute, Inc., Splunk, Inc., Trend Micro, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |