Quick Navigation

Report Overview

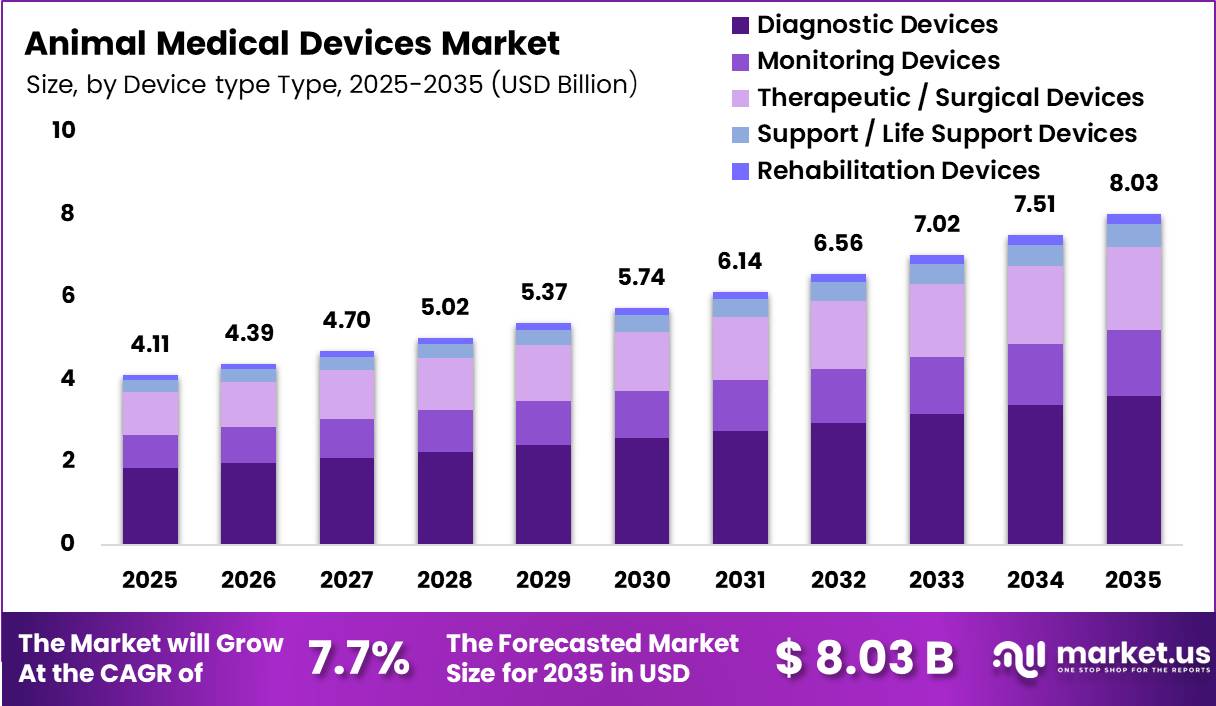

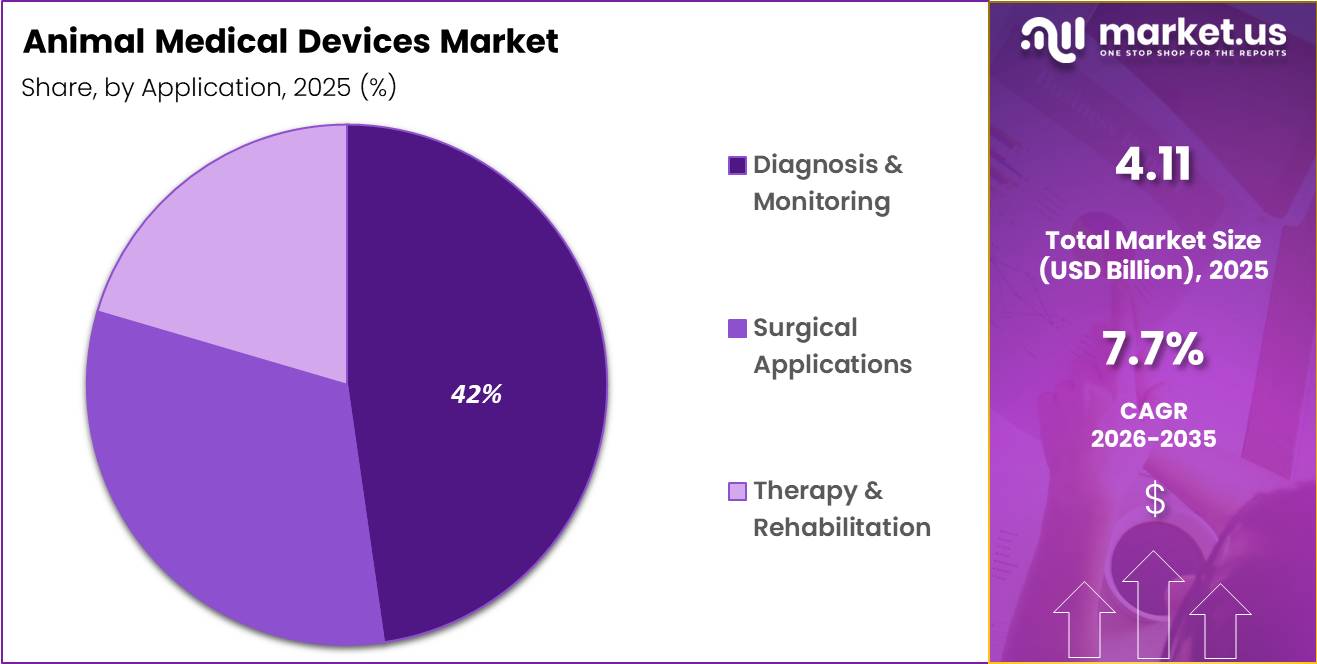

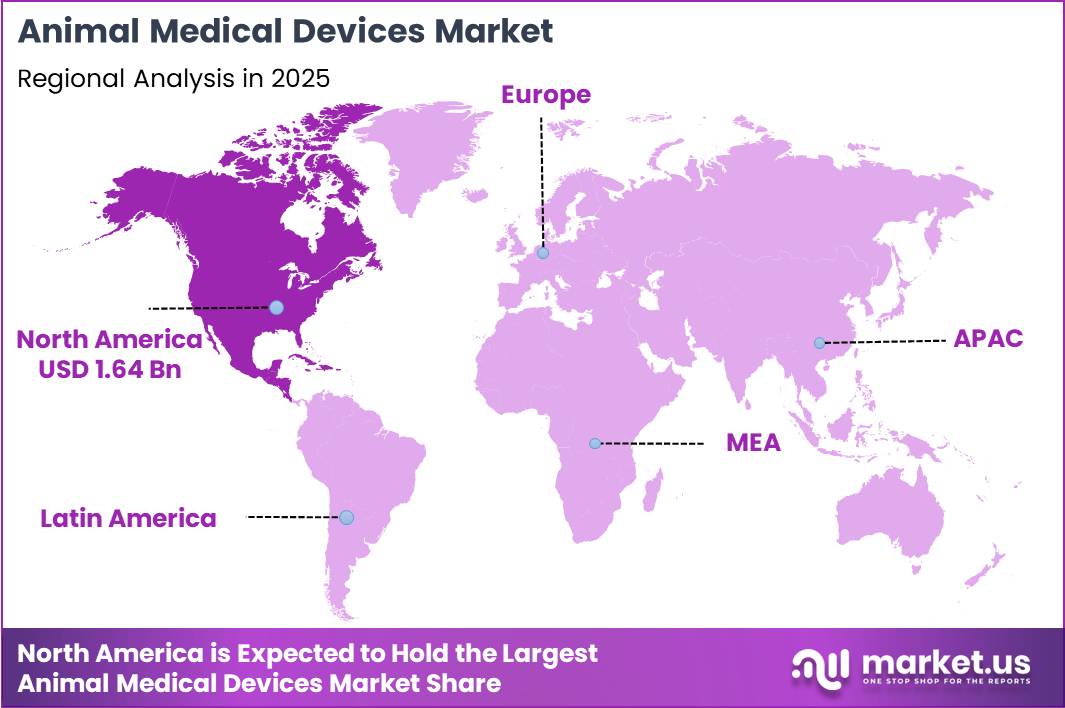

In 2025, the Global Animal Medical Devices Market was valued at US$4.11 billion, and between 2025 and 2035, this market is estimated to register a CAGR of 7.7%, reaching about US$ 8.03 billion by 2035. North America held a dominant market position, capturing more than a 40% share, holding USD 1.64 billion in revenue.

The animal medical devices market is undergoing a structural shift toward advanced diagnostics, real-time monitoring, and technology-enabled veterinary care. Growth is increasingly supported by rising spending on companion animal healthcare, expansion of specialized veterinary services, and broader adoption of imaging, monitoring, and surgical technologies across veterinary clinics and hospitals.

Market demand is also benefiting from the growing emphasis on preventive healthcare, early disease detection, and improved treatment outcomes in both companion and production animals. Demand is no longer confined to large animal hospitals in developed markets; the breadth of device adoption now spans companion animal clinics, livestock management systems, and wildlife conservation programs across multiple geographies.

Technology innovation remains a key competitive differentiator. Diagnostic platforms capable of delivering rapid in-clinic results, digital imaging systems, and integrated monitoring solutions are strengthening clinical workflows and improving decision-making efficiency

Key Takeaways

- The Global Animal Medical Devices Market was valued at US$4.11 billion in 2025.

- The Global Animal Medical Devices Market is projected to grow at a CAGR of 7.7% and is estimated to reach US$8.03 billion by 2035.

- On the basis of device type, the Diagnostic Devices dominated the market, constituting 0% of the total market share.

- Based on the Application, the Diagnosis & Monitoring dominated the Global Animal Medical Devices Market, with a substantial market share of around 42%.

- Based on the Animal type, Companion Animals led the market, comprising 58% of the total market.

- Among the end-users, the Veterinary Clinics held a major share in the Animal Medical Devices market, 50% of the market share.

- In 2025, the North America was the most dominant region in the Global Animal Medical Devices Market, accounting for 40% of the total global consumption.

Device Type Analysis

Diagnostic Devices Represent the Dominant Segment in the Animal Medical Devices Market.

Diagnostic devices represent the largest segment of the animal medical devices market, accounting for 45.0% of global revenue. Their leadership position is driven by increasing clinical demand for early disease detection, preventive healthcare programs, routine wellness testing, and faster clinical decision-making. Veterinary providers are prioritizing diagnostic capital investments because they fundamentally improve treatment outcomes while supporting highly predictable, recurring testing revenue streams and enabling higher daily patient throughput.

- In March 2025, Antech Diagnostics launched trūRapid™ FOUR, a room-temperature point-of-care system screening for four major canine vector-borne diseases in minutes without manual snapping. This rollout directly advanced clinic monetization by maximizing the speed and clinical volume of routine in-house screening workflows.

Monitoring Devices, Therapeutic/Surgical Devices, Support/Life Support Devices, and Rehabilitation Devices continue to gain rapid traction as veterinary medicine becomes increasingly specialized. Monitoring technologies are benefiting from greater clinical adoption of continuous patient telemetry observation systems, while therapeutic and surgical devices are expanding alongside the market-wide growth in advanced soft-tissue and orthopedic veterinary procedures. Rehabilitation solutions remain a smaller but steadily expanding market opportunity, supported by increasing consumer demand for structured post-operative physical therapy and long-term canine mobility management.

Application Analysis

Diagnosis & Monitoring Represents Strategically Growing Demand Categories.

Diagnosis & Monitoring accounts for 42% of market revenue, making it the leading application segment. The segment’s dominance is supported by routine veterinary check-ups, metabolic tracking, preventive screening programs, and increasing emphasis on early disease identification. Healthcare providers continue to prioritize diagnostic investments because earlier intervention improves treatment success rates while reducing overall care costs.

Commercially, diagnosis and monitoring applications create recurring demand for consumables, testing services, and software-enabled clinical workflows. The expansion of in-clinic testing capabilities is enabling veterinarians to accelerate diagnosis and improve patient management efficiency. Recent innovation activity from diagnostic provider’s further highlights industry focus on strengthening monitoring and disease detection capabilities.

- In June 2025, IDEXX Laboratories, Inc. launched the Catalyst Cortisol Test to expand real-time endocrine diagnostics capabilities for canine patients, reinforcing the industry’s movement toward point-of-care testing and earlier intervention strategies.

Surgical Applications continues to benefit from increasing adoption of soft-tissue and orthopedic procedures. Therapy & Rehabilitation is gaining momentum as veterinary providers expand physiotherapy and recovery treatment offerings, particularly for aging companion animals and post-surgical patients.

Animal Type Analysis

Companion Animals Dominate the Animal Medical Devices Market by Animal Type.

Companion Animals account for 58% of total market demand, representing the largest and most profitable animal category. Market expansion is primarily driven by escalating, non-discretionary healthcare spending on dogs, cats, horses, and small mammals. The growing consumer expectation for human-grade veterinary care, combined with the rising clinical utilization of advanced diagnostics, digital imaging, continuous telemetry monitoring, and specialized surgical procedures, continues to elevate device demand within this segment.

- In January 2025, Zoetis Inc. launched its Vetscan OptiCell™ platform at the Veterinary Meeting & Expo (VMX). This screenless, point-of-care hematology analyzer integrates viscoelastic focusing (VEF) microfluidic technology with AI-enabled algorithms. It enables rapid, in-clinic automated complete blood count (CBC) analysis within minutes using a single-use cartridge, reinforcing the shift toward advanced, data-driven veterinary diagnostic workflows.

Companion animal healthcare also generates vastly superior, recession-resilient recurring revenue opportunities compared with other animal categories. This economic engine is fueled by regular lifelong wellness examinations, preventive screening programs, and multi-stage chronic disease management. Diagnostic innovation across corporate and independent veterinary practices remains heavily concentrated within this segment, supporting sustained long-term institutional investment in premium medical technologies.

Conversely, livestock and production animal applications remain strategically tied to herd health management, large-scale disease surveillance, and food-supply productivity optimization. Zoo, wildlife, and exotic animal applications represent a smaller, highly specialized niche supported by global conservation initiatives and advanced academic veterinary services.

End User Analysis

Veterinary Clinics Are the Leading End User in the Global Animal Medical Devices Market.

Veterinary clinics account for 50% of global animal medical device revenue, establishing them as the primary purchasing channel for diagnostics, monitoring, and treatment technologies. Their dominance is driven by their central role in providing routine preventive care, outpatient treatments, and early disease detection.

Clinics benefit commercially from high patient throughput, recurring demand for diagnostic consumables, and integrated device workflows that enable same-day clinical decisions. Investments in diagnostic and imaging systems improve operational efficiency and allow clinics to expand service offerings, increasing overall revenue per patient. The proliferation of compact, point-of-care technologies is reinforcing clinic-level adoption.

While veterinary clinics dominate revenue, other end users are contributing to broader market growth. Animal hospitals are increasingly adopting advanced surgical, imaging, and monitoring technologies to manage complex cases and specialty care. Research laboratories and academic institutions generate demand for specialized analytical and diagnostic devices, while other segments, including mobile veterinary services and rehabilitation centers, are gradually incorporating modern medical technologies. This dynamic underscores veterinary clinics as the foundation of market demand while highlighting emerging opportunities across adjacent end-user categories.

Key Market Segments

By Device Type

- Diagnostic Devices

- Monitoring Devices

- Therapeutic / Surgical Devices

- Support / Life Support Devices

- Rehabilitation Devices

By Application Type

- Diagnosis & Monitoring

- Surgical Applications

- Therapy & Rehabilitation

By Animal Type

- Companion Animals

- Livestock / Production Animals

- Zoo & Wildlife Animals

By End-User

- Veterinary Clinics

- Animal Hospitals

- Research Laboratories & Academic Institutes

- Others

Driver

Oncology led biologics launch intensity

The 2025 approval cycle confirms that biologics innovation remains commercially concentrated in specialty care, especially oncology and immune mediated disease. FDA CDER approved 46 novel drugs in 2025, including multiple biologics such as ADCs, monoclonal antibodies, and protein based products, while an industry review of the same cycle noted that biologics accounted for about one quarter of approvals and that cancer remained the main therapeutic focus.

That matters for 2026 forecasting because oncology biologics typically carry higher annual revenue density per launch than primary care products, benefit from faster uptake through concentrated prescriber networks, and are increasingly paired with biomarker led patient selection that improves pricing defensibility and treatment persistence.

Commercially, this driver supports above baseline growth by lifting launch value per approved asset, increasing infusion center and specialty pharmacy throughput, and extending lifecycle economics through line extension strategies such as subcutaneous reformulations and combo regimens, as seen in the continued cadence of antibody and oncology approvals during 2025.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oncology-led biologics launch intensity | +1.4% | North America core, EU, Japan, China urban specialty centers | Short term (≤ 2 years) |

| Biosimilar scale-up and interchangeability expansion | +1.1% | EU core, U.S. catch-up, Canada, select APAC | Medium term (2-4 years) |

| Cell and gene therapy commercialization broadening | +1.6% | U.S. core, EU5, UK, Japan, Gulf premium hubs | Medium term (2-4 years) |

| Manufacturing platform standardization and faster CMC pathways | +0.9% | U.S., EU, Singapore, South Korea, India biologics corridors | Short term (≤ 2 years) |

| Medicare pricing pressure shifting portfolio mix toward high-value biologics | +0.8% | U.S. core with global portfolio spill-over | Medium term (2-4 years) |

| Prevention, immunology, and rare-disease biologics diversification | +1.0% | North America, EU, affluent APAC, LatAm private-channel spill-over | Long term (≥ 4 years) |

Challenge

Sterile Capacity Bottlenecks

Sterile biologics capacity remains a growth friction because demand has shifted faster than qualified fill finish, aseptic suite, and high containment expansion cycles, while the approval pipeline continues to refresh commercial scale needs, including 55 new FDA approvals in 2025 that sustain downstream manufacturing loading across biologics and specialty injectables.

In practical terms, a new commercial biologics line still typically requires 24 to 36 months to design, validate, and stabilize, with ramp losses of roughly 8% to 15% in initial throughput as media fills, line clearances, campaign sequencing, and tech transfer deviations suppress asset utilization below modeled nameplate. This does not stop sales today, but it can shave about 1.4% points from the market’s achievable CAGR by extending launch to steady state timelines by 2 to 4 quarters, pushing CMO slot premiums higher, and forcing firms to hold 3 to 6 months of extra safety stock for high value SKUs.

The strategic response is not just more steel in the ground; firms increasingly need modular fill finish footprints, dual region release capacity, and earlier late stage network locking so capacity risk is absorbed during phase III rather than after filing, especially in North America, Western Europe, Singapore, and South Korea where biologics node concentration is highest.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Sterile Capacity Bottlenecks | -1.4% | North America core; EU biologics hubs; APAC export bases | Medium term (2-4 years) |

| Quality Deviation Recurrence | -1.2% | US FDA supply chain; EU regulatory hubs; Japan/Korea plants | Medium term (2-4 years) |

| Cold-Chain Integrity Gaps | -0.9% | Global vaccine lanes; EM logistics corridors; rural last-mile networks | Medium term (2-4 years) |

| Bioprocess Talent Deficit | -1.0% | US and EU advanced plants; India; Singapore; Korea | Long term (≥ 4 years) |

| Multi-Node Supply Fragility | -1.1% | EU import-dependent markets; US biologics network; APAC input clusters | Medium term (2-4 years) |

| Regulatory Data Burden | -0.8% | US; EU; ICH markets; cross-border launch programs | Short term (≤ 2 years) |

Restraints

U.S. tariff shock on patented biologics inputs

The April 2026 U.S. proclamation created a new cost overhang for patented pharmaceutical products and associated ingredients, with headline duty rates reaching 100% for covered imports, 20% for firms with approved onshoring plans, and 15% for imports from the EU, Japan, Korea, Switzerland and Liechtenstein, while generics and biosimilars were exempt for now; for biopharma, that sharply raises landed-cost uncertainty around monoclonal antibody intermediates, high-value APIs, and single-use processing inputs embedded in patented therapy supply chains.

The direct bottleneck is not only tariff expense but network redesign: companies now face qualification of alternate supply nodes, inventory buffering, and duplicate release testing, all of which lengthen planning cycles and can push procurement and tech-transfer timelines out by two to four quarters for complex biologics.

Strategically, this acts as a near-term drag on revenue conversion and operating margin because manufacturers cannot fully pass through cost inflation in contracted channels, especially where payer pressure is rising, so management teams are more likely to defer incremental line expansions, prioritize domestic fill finish over new molecule launches, and re-rank portfolios toward exempt orphan, plasma derived, or biosimilar categories.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| U.S. tariff shock on patented biologics inputs | -1.4% | North America core, EU export nodes, Japan, Korea, Switzerland | Short term (≤ 2 years) |

| GMP failures and batch-release disruptions | -1.1% | North America core, EU, India, APAC biologics hubs | Short term (≤ 2 years) |

| IRA price compression on mature biologics | -1.3% | U.S. core; spillover to EU pricing corridors | Medium term (2-4 years) |

| CDMO/outsourcing realignment under BIOSECURE rules | -0.9% | U.S., China-linked supply chains, Singapore, Korea, EU | Medium term (2-4 years) |

| Weak biotech funding and delayed scale-up CapEx | -1.0% | U.S., EU, UK, selective APAC innovation clusters | Short term (≤ 2 years) |

| EU regulatory transition and compliance burden | -0.6% | EU core, UK-linked exporters, global filing hubs | Medium term (2-4 years) |

Opportunity

Building Regional Biologics and mRNA Hubs in LMICs to Unlock New Demand Pools

This qualifies as an opportunity because baseline forecasts generally assume demand growth is served by today’s established production geographies, while the untapped upside comes from building regional manufacturing and commercialization ecosystems in low and middle income countries that can create new demand pools, procurement access, and sovereign supply contracts not yet fully captured in current models.

WHO’s mRNA technology transfer program had 15 partners as of May 2025 and is explicitly expanding from COVID vaccines toward other mRNA vaccines and therapeutics, including monoclonal antibodies, while Gavi has approved up to $1.2 billion for the African Vaccine Manufacturing Accelerator and broader 2026 to 2030 support for regional manufacturing, creating a rare policy financing window to localize fill finish, drug substance, and platform technologies.

Companies that move early can convert this into 20% to 30% lower logistics exposure, 10% to 15% tender price advantages in public procurement, faster emergency access positioning, and a new long duration TAM across Africa, MENA, Southeast Asia, and parts of Latin America where localized production can support $300 million to $800 million regional revenue platforms per asset class by 2030, especially when using modular mRNA or recombinant platforms that can be repurposed across vaccines, antibodies, and outbreak response products

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Biosimilar void capture | +2.4% | U.S., EU, India, select LATAM | Medium term (2-4 years) |

| AI-native bioprocess monetization | +1.6% | North America core, EU, Japan, Korea | Short term (≤ 2 years) |

| LMIC regional biologics hubs | +2.1% | Africa, Southeast Asia, MENA, LATAM | Medium term (2-4 years) |

| ADC/CGT platform roll-ups | +1.9% | U.S., EU, China, Korea | Medium term (2-4 years) |

| Outcomes-based specialty access | +1.3% | U.S., EU5, Gulf states | Short term (≤ 2 years) |

| Lifecycle reformulation plays | +1.1% | U.S., EU, Japan, urban China | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Supply Chain Diversification and Regional Manufacturing Expansion

Global trade fragmentation, rising regulatory scrutiny on medical-grade electronics, and supply chain disruptions continue to reshape the animal medical devices market. Manufacturers of diagnostic and monitoring systems are increasingly adopting regionalized production strategies to reduce exposure to cross-border trade risks and ensure compliance with varying veterinary medical device regulations. This shift is particularly important for imaging systems and in-clinic diagnostics, where component availability and regulatory certification directly impact commercialization timelines and clinic adoption rates.

- In June 2025, Vimian Group AB completed the acquisition of AllAccem Inc., strengthening its veterinary dental portfolio and reinforcing its European market footprint.

The transaction reflects a broader industry pattern of using acquisitions to secure regional capabilities and improve supply chain proximity within high-growth companion animal healthcare markets. At a structural level, veterinary diagnostics and device manufacturers are also increasingly investing in localized manufacturing and assembly networks across Asia Pacific and Europe, although most of these capacity expansions are not consistently disclosed at a precise dated-event level in public filings. This ongoing localization trend is being driven by regulatory alignment requirements, tariff volatility, and the need for faster distribution to high-density veterinary care markets.

Regional Analysis

North America Held the Largest Share of the Global Animal Medical Devices Market.

North America accounts for 40% of global animal medical device revenue, making it the dominant regional market. The region’s leadership is underpinned by a mature veterinary healthcare ecosystem, high companion animal ownership, and robust spending on preventive and specialty veterinary services.

Advanced diagnostic adoption, including in-clinic analyzers and imaging systems, is widespread, supported by strong veterinary infrastructure and an emphasis on early disease detection and chronic care management. This commercial and operational advantage sustains recurring demand for high-value medical devices and positions North America as the innovation hub for companion animal healthcare technologies.

- In March 2025, IDEXX Laboratories, Inc. expanded its North American diagnostic distribution network, reinforcing supply chain reliability and enabling faster deployment of point-of-care diagnostic solutions to clinics across the region.

Europe remains a strategic market, driven by high animal welfare standards, established veterinary networks, and growing adoption of advanced diagnostics and monitoring solutions. Asia Pacific is a rapidly expanding market, fueled by rising pet ownership, improving veterinary infrastructure, and increasing awareness of animal health technologies. Latin America is gaining traction as veterinary healthcare spending rises, while the Middle East & Africa represents an emerging opportunity due to modernization of veterinary services and increasing adoption of advanced devices.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The animal medical devices market is moderately concentrated, with a clear tilt toward companies that operate integrated veterinary healthcare ecosystems rather than standalone device manufacturers. Market share is increasingly dominated by players with strong positions in diagnostics and recurring consumables, as these models generate continuous revenue and deepen long-term customer dependency within veterinary clinics. IDEXX Laboratories, Inc. holds a leading position, supported by its installed base of in-clinic diagnostic platforms and consumables-driven model, which strengthens retention and repeat usage across veterinary practices.

Alongside this, Zoetis Inc. maintains a strong market presence through its diversified animal health portfolio, enabling influence across preventive care, treatment, and adjacent diagnostic-support segments.

Other segments, including imaging, monitoring, and cost-sensitive diagnostic devices, remain more fragmented but continue to play a strategic role in shaping overall market dynamics. Established players such as Mindray Medical International Ltd. hold strong positions in advanced imaging and monitoring solutions for veterinary hospitals and specialty clinics. At the same time, emerging companies are gradually expanding in price-sensitive and growth markets through compact, accessible diagnostic devices. The competitive landscape is also seeing consolidation and platform-focused strategies, reflecting a broader industry trend toward integrated veterinary healthcare solutions.

Market Key Players

- IDEXX Laboratories, Inc.

- Zoetis Inc.

- GE Healthcare

- Mindray Medical International Ltd.

- Carestream Health

- Medtronic plc

- Midmark Corporation

- Nonin Medical, Inc.

- Vimian Group AB

- Digicare Biomedical Technology

- EKF Diagnostics Holdings plc

- DiaSys Diagnostic Systems GmbH

- Chengdu Seamaty Technology Co., Ltd.

- BIOLABO GROUP

- Guangzhou Yueshen Medical Equipment Co., Ltd.

Recent Development

- In October 2025 Mars Science & Diagnostics (Heska) rolls out global software updates across its Element AIM® diagnostic ecosystem, applying enhanced AI-driven identification for in-clinic urine sediment processing.

- In March 2026, Vimian Group AB officially consolidates the acquisition of the companion animal diagnostics company I-Vet Diagnostics, establishing a localized diagnostics network in Southern Europe.

- In March 2026, Midmark Corporation updates its clinical veterinary workspace asset lines, embedding modular mounting arm frames and high-frequency diagnostic connection points into its Synthesis® treatment table systems.

- In May 2026, Medtronic (Veterinary Division) begins distribution of a specialized veterinary variation of its Sonicision™ cordless ultrasonic dissector, engineered specifically for delicate soft-tissue management in avian and exotic surgeries.

- In September 2025 IDEXX Reference Laboratories unveils its IDEXX Cancer Dx™ panel at the Veterinary Cancer Society Annual Conference, launching a liquid-biopsy biomarker blood profile to catch canine lymphoma prior to visible signs.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 4.11 Bn |

| Forecast Revenue (2035) | US$ 8.03 Bn |

| CAGR (2026-2035) | 7.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Device Type (Diagnostic Devices, Monitoring Devices, Therapeutic / Surgical Devices, Support / Life Support Devices, Rehabilitation Devices), By Application (Diagnosis & Monitoring, Routine check-ups, metabolic tracking, early disease detection), By Animal Type (Companion Animals, Livestock / Production Animals, Zoo & Wildlife Animals), By End-use Industry (Veterinary Clinics, Animal Hospitals, Research Laboratories & Academic Institutes, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | IDEXX Laboratories, Zoetis, GE Healthcare, Mindray Medical, Carestream Health, Medtronic (Veterinary), Midmark Corporation, Nonin Medical, Vimian Group, Digicare Biomedical, EKF Diagnostics, DiaSys Diagnostic Systems, Chengdu Seamaty, BIOLABO GROUP, Guangzhou Yueshen, and Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |