Global Amorphous Polyalphaolefin Market Size, Share, And Business Benefits By Product Type (Co-polymer, Homo-polymer, Terpolymer), By Chemical Composition (Polyalphaolefin Copolymers, Polyalphaolefin Homopolymers, Additive Modified Polyalphaolefin), By Application (Paper and Packaging, Personal Hygiene, Wood Working, Adhesives), By Region, and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: October 2025

- Report ID: 163690

- Number of Pages: 244

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

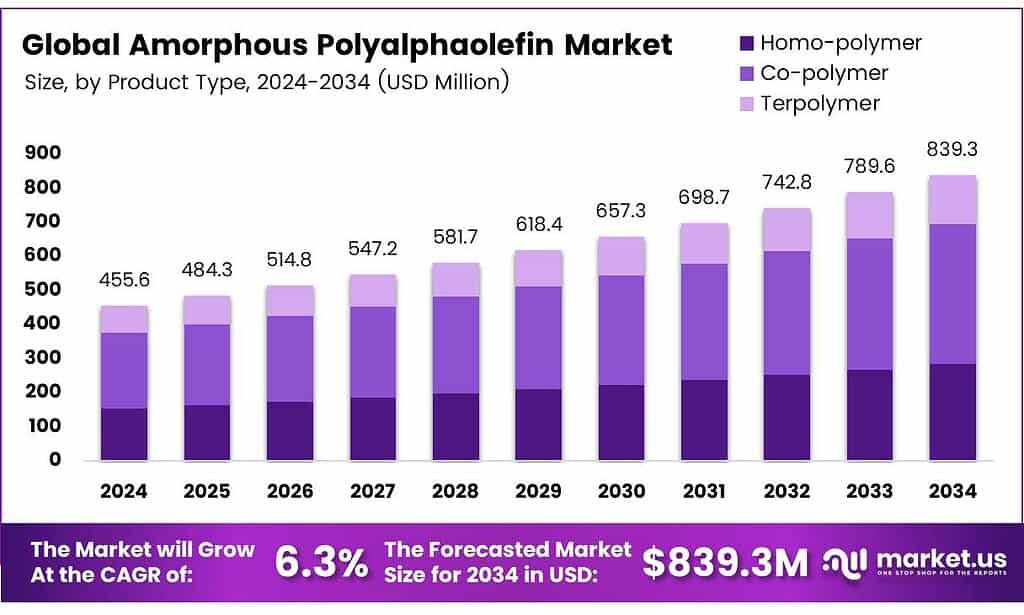

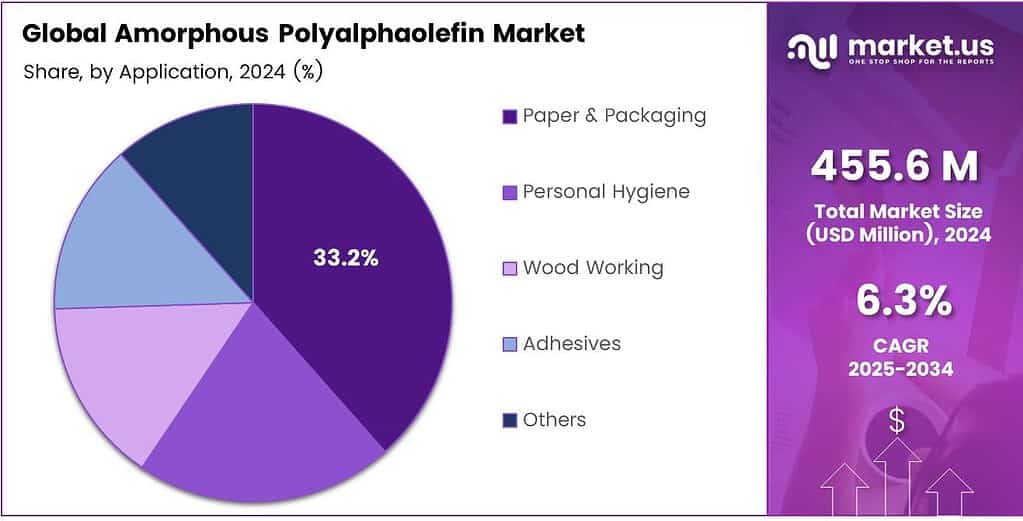

The Global Amorphous Polyalphaolefin Market size is expected to be worth around USD 839.3 Million by 2034, from USD 455.6 Million in 2024, growing at a CAGR of 6.3% during the forecast period from 2025 to 2034.

Amorphous poly alpha olefin (APAO) is a low molecular weight amorphous plastic material that exhibits high compatibility with asphalt binder. It is defined as an amorphous polyolefin used as a raw material in hot-melt adhesives and various film and foil applications, noted for its flexibility, compatibility with other polyolefins, reduced glass transition temperature, and recyclability. Formed by the copolymerization of α-olefin, APAO possesses characteristics of high fluidity, low crystallinity, and high randomness. APAO can be completely dissolved in asphalt binder when its content is no more than 6 wt.%.

APAO-modified binder with high stability can be processed without shearing or stabilizers. Research has shown that the processing temperature for APAO-modified binder can be controlled at 165 °C, which is lower than the 180 °C required for SBS-modified binder. These findings demonstrate that APAO enables the production of modified asphalt binder at reduced processing temperatures without the need for shearing or stabilizers. Numerous studies have investigated the impact of APAO on asphalt binder performance.

APAO enhances the elastic properties and reduces temperature susceptibility of the binder, though it adversely affects creep stiffness and creep rate. It improves high-temperature performance, storage stability, and aging resistance in waste tire rubber (WTR)-modified binders. When combined with SBS, APAO yields superior high- and intermediate-temperature properties and storage stability compared to SBS alone, with low-temperature performance equivalent to that of SBS-modified binder.

APAO also enhances high- and low-temperature properties as well as storage stability in terminal blend rubberized binders. Furthermore, it strengthens elastic recovery, aging resistance, and low-temperature cracking resistance in EVA-modified binders while serving as an effective stabilizer to improve overall binder stability. APAO satisfies modification requirements due to its superior compatibility with asphalt binder, simple processing, and excellent performance effects. With a price comparable to SBS, APAO is cost-competitive.

Key Takeaways

- The Global Amorphous Polyalphaolefin Market is expected to grow from USD 455.6 million in 2024 to USD 839.3 million by 2034 at a 6.3% CAGR.

- Co-polymer segment dominated in 2024 with 48.8% share, driven by flexibility, adhesion, and impact strength in hot-melt packaging applications.

- Polyalphaolefin Copolymers held 44.9% market share in 2024, excelling in wettability, heat resistance, and durability for packaging and adhesives.

- Paper and Packaging application led in 2024 with a 33.2% share, fueled by APAO’s moisture-resistant seals and e-commerce-driven demand.

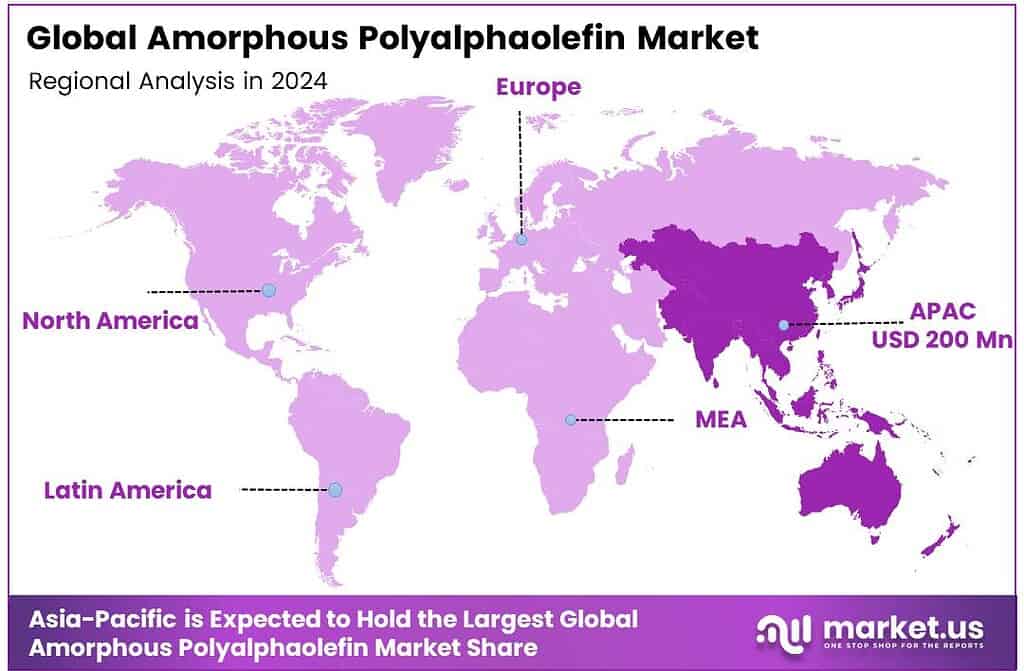

- Asia-Pacific (APAC) commanded 43.9% global share in 2024 (USD 200.0M), led by strong demand in packaging, automotive, and hygiene sectors for hot-melt adhesives.

By Product Type

Co-polymer dominates with 48.8% due to its enhanced durability, toughness, and processability in adhesives.

In 2024, Co-polymer held a dominant market position in the Amorphous Polyalphaolefin Market, with a 48.8% share. This segment thrives because co-polymers blend seamlessly, boosting flexibility and adhesion in hot melt applications. Manufacturers favor it for superior impact strength, driving widespread use in packaging. Consequently, demand surges as industries seek reliable bonding solutions.

Homo-polymer follows closely, offering consistent performance across substrates. It excels in uniform structure, ensuring reliable adhesion without complexity. Industries adopt it for cost-effective bonding in woodworking and hygiene products. Thus, homo-polymer sustains steady demand through dependable qualities. Transitioning from co-polymers provides simpler alternatives for basic needs.

Terpolymer rounds out the segment, incorporating multiple monomers for tailored properties. It enhances thermal stability and chemical resistance, ideal for specialized adhesives. Emerging applications in advanced packaging leverage its randomness. Therefore, terpolymer gains traction as innovation pushes boundaries. Building on others, it addresses niche requirements innovatively.

By Chemical Composition

Polyalphaolefin Copolymers lead with 44.9% thanks to their versatility and improved clarity in high-performance uses.

In 2024, Polyalphaolefin Copolymers held a dominant market position segment of the Amorphous Polyalphaolefin Market, with a 44.9% share. These copolymers shine in diverse applications, providing excellent wettability and heat resistance. They integrate smoothly into formulations, enhancing overall durability. The packaging and adhesives sectors embrace them widely. This dominance fuels efficient, high-quality production.

Polyalphaolefin Homopolymers provide cost-effective adhesion with uniform consistency. They bond effectively to various surfaces, supporting woodworking and basic hygiene needs. Their simplicity reduces processing costs, appealing to budget-conscious manufacturers. Hence, homopolymers maintain relevance in everyday uses. Shifting from copolymers, they offer straightforward reliability.

Additive Modified Polyalphaolefin tailors performance through enhancements like better flexibility. Additives boost specific traits, such as UV resistance for outdoor applications. This customization attracts innovative industries seeking optimized solutions. Thus, it carves a growing niche. Extending from homopolymers, it elevates functionality precisely.

By Application

Paper and Packaging commands 33.2% with its moisture resistance suiting food and e-commerce demands.

In 2024, Paper and Packaging held a dominant market position in the By Application Analysis segment of the Amorphous Polyalphaolefin Market, with a 33.2% share. APAO excels here, offering robust seals against moisture in cartons and labels. E-commerce boom amplifies need for secure packaging. Consequently, it secures bonds swiftly, reducing waste. This leadership stems from essential daily utility.

Personal Hygiene benefits from APAO’s gentle adhesion in diapers and sanitary products. It ensures comfort without irritation, aligning with hygiene awareness. Manufacturers integrate it for leak-proof designs, boosting consumer trust. Therefore, the segment expands with population growth. Transitioning from packaging, it prioritizes health-focused bonding.

Woodworking utilizes APAO for strong, quick-setting joints in furniture assembly. Its low viscosity aids precise application on porous woods. This enhances durability against wear, supporting construction surges. Hence, woodworking thrives on reliable performance. Building upon hygiene, it tackles structural challenges adeptly.

Key Market Segments

By Product Type

- Co-polymer

- Homo-polymer

- Terpolymer

By Chemical Composition

- Polyalphaolefin Copolymers

- Polyalphaolefin Homopolymers

- Additive Modified Polyalphaolefin

By Application

- Paper and Packaging

- Personal Hygiene

- Wood Working

- Adhesives

- Others

Emerging Trends

Mono-material, recyclable polyolefin packaging pushes APAO hot-melts

Brand owners in Europe are redesigning packs to be mono-material and fully recyclable, a requirement under the EU’s proposed Packaging and Packaging Waste Regulation (PPWR). That shift favors amorphous polyalphaolefin (APAO) hot-melt adhesives because APAO is polyolefin-based and bonds well to PE/PP films without contaminating recycling streams.

The European Commission’s PPWR page states that all packaging must be recyclable, with increasing recycled-content obligations, clear policy pressure that rewards APAO formulations compatible with PE/PP mono-material designs. Polyolefins dominate plastics. PlasticsEurope’s latest Fast Facts 2023 shows a global polymer mix where PP is 18.9%, LD/LLDPE 14.1%, and HD/MDPE 12.2% of production, together roughly 45% of output.

- Recycling infrastructure is also aligning with polyolefins. The European Parliament reports 40.7% recycling of plastic packaging waste, while Plastics Recyclers Europe notes 3.5 Mt of installed recycling capacity for polyolefin (PO) films, about 26% of total EU27+3 capacity. As PO recycling capacity expands, adhesive systems that don’t hinder reprocessing become more valuable, again pointing to APAO’s fit in PE/PP flows.

Drivers

Strong regulatory push for recyclable, mono-polymer packaging fuels APAO usage

One major driving factor for increasing demand for amorphous polyalphaolefin (APAO) adhesives is the strong regulatory momentum toward packaging that is fully recyclable and designed for circular use. In the Packaging and Packaging Waste Regulation (PPWR) adopted by the European Commission, all new packaging placed on the market must be 100% recyclable, with a requirement that packaging with a recyclability rate below 70% will no longer be considered recyclable starting.

- In parallel, the waste statistics show that in 2023 in the European Union, 79.7 million tonnes of packaging waste were generated, equivalent to 177.8 kg per inhabitant. For plastic packaging specifically, the EU average recycling rate was 42.1% in 2023, and each person generated about 35.3 kg of plastic packaging waste, of which 14.8 kg got recycled.

This regulatory push matters for APAO because many converters and brands are redesigning packaging toward mono-polymer structures, which simplify sorting and recycling. APAO adhesives are polyolefin-based, making them compatible with PE/PP packaging systems and favouring adhesive choices that support recyclability rather than hinder it. In other words, the adhesive becomes part of a sustainable packaging “system” rather than an obstacle.

Restraints

Volatile polyolefin feedstocks and energy costs squeeze APAO economics

A major restraint for amorphous polyalphaolefin (APAO) is the volatility of its petrochemical feedstocks—principally propylene/alpha-olefins amplified by high and unstable energy costs. U.S. Energy Information Administration data show how refinery-grade propylene output swings month to month: it dipped to 6,332 thousand barrels and rose to 8,548 thousand barrels; in 2024, it ranged from 6,419 to 8,640 thousand barrels.

Such swings ripple through propylene pricing and availability, tightening margins for APAO producers and adhesive formulators when supply is tight. Europe’s plastics and chemicals backdrop adds further pressure. PlasticsEurope reports 42.9 Mt of European plastics produced, reflecting a sector still recovering and rebalancing after the energy crisis conditions that can depress cracker and polymer operating rates and intermittently constrain polyolefin chains used to make APAO.

- The European Chemical Industry Council notes capacity utilization fell to 74.1%, and stresses Europe’s competitive disadvantage versus the U.S., China, and the Middle East due to higher energy and feedstock costs, a structural headwind that ultimately filters into specialty polyolefin adhesive costs. APAO fits sustainability-driven monomer designs; the real-economy friction of feedstock and energy volatility is a tangible restraint on broader, smoother adoption.

Opportunity

Expansion of polyolefin-based substrates accelerates APAO usage

One of the key growth factors for amorphous polyalphaolefin (APAO) adhesives is the rapid expansion of polyolefin-based substrates such as polyethylene (PE) and polypropylene (PP) in packaging and flexible film applications. Global consumption of linear alpha-olefins (LAO), which are feedstocks for polyolefins, including PE.

- In Europe, recent statistics show that plastic packaging waste per person was 35.3 kg, reflecting how widespread plastic-film usage remains. As brands and converters increasingly adopt PE/PP films for cost-effectiveness and recyclability, adhesives that bond well with these polyolefin materials become more important, and APAO, being polyolefin-based, fits that need.

Government and regulatory initiatives also bolster this trend. The Packaging and Packaging Waste Regulation (PPWR) in the EU mandates that all packaging must be recyclable, which encourages mono-polymer solutions and simpler film-laminate systems. In such systems, adhesives that do not interfere with sorting or recycling, such as APAO adhesives that remain within the polyolefin family, gain preference.

Regional Analysis

Asia-Pacific leads with a 43.9% share and a USD 200.0 Million market value.

In 2024, Asia-Pacific (APAC) led the global amorphous polyalphaolefin (APAO) market with a 43.9% share, valued at USD 200.0 million. This dominance stems from strong demand in packaging, automotive, and hygiene sectors for durable, low-temperature hot-melt adhesives.

Key drivers include heavy investments in sustainable packaging and infrastructure in China, India, Japan, and South Korea. China’s booming consumer goods and packaging production plays a central role, with Asia accounting for over of global packaging consumption, per the World Packaging Organisation.

APAO excels in eco-friendly applications due to its compatibility with polyolefin films and recyclable mono-material packaging. Government policies further boost adoption, such as Japan’s Plastic Resource Circulation Act and India’s Extended Producer Responsibility rules, which promote recyclable adhesives.

The region’s automotive and construction sectors also drive growth, using APAO for interior assemblies, nonwovens, and waterproofing due to its low odor and heat resistance. Supported by low costs, urbanization, and industrial expansion, APAC is expected to maintain market leadership.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Qida Chemicals leverages its strategic position in the Asia-Pacific region to serve growing local demand. The company focuses on the production and supply of amorphous polyalphaolefin (APAO) for adhesives, sealants, and coatings. Its competitive edge likely stems from cost-effective manufacturing and a strong regional distribution network, allowing it to cater to price-sensitive markets and various industrial applications.

Ter Hell & Co. GmbH is a well-established German specialty chemicals distributor with a long history. While not a manufacturer, it plays a crucial role as a key supplier and distributor of APAO and other polymer products across Europe. The company’s strength lies in its deep technical expertise, robust logistics, and strong relationships with both producers and end-users.

ExxonMobil Corporation is a leading force in the APAO market, operating under its brand Vistamaxx. The company’s strength is rooted in its backward integration into raw materials, massive scale of production, and extensive R&D capabilities. This allows it to offer a wide range of high-performance APAO products, driving innovation and setting industry standards for applications in packaging, hygiene.

Top Key Players in the Market

- Qida Chemicals Co. Ltd.

- Ter Hell and Co. GMBH

- Exxonmobil Corporation

- Soltex

- Chevron Phillips Chemical

- Evonik Industries AG

- Ineos Oligomers

- REXtac LLC

- A S Harrison and Co. Pty Limited

Recent Developments

- In 2024, Qida Chemicals Co. Ltd., a key player in APAO production, focused on innovation and capacity expansion. The company unveiled a nanofiller-enhanced APAO formulation incorporating silica nanoparticles, which boosts tensile strength and improves adhesion on coated substrates.

- In 2024, Ter Hell & Co. GMBH, a German distributor specializing in polymer additives, showed limited public updates on APAO-specific activities. The company continued to emphasize its role in supplying APAO for hot melt adhesives in Europe, leveraging its distribution network for applications in packaging and woodworking.

Report Scope

Report Features Description Market Value (2024) USD 455.6 Million Forecast Revenue (2034) USD 839.3 Million CAGR (2025-2034) 6.3% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Co-polymer, Homo-polymer, Terpolymer), By Chemical Composition (Polyalphaolefin Copolymers, Polyalphaolefin Homopolymers, Additive Modified Polyalphaolefin), By Application (Paper and Packaging, Personal Hygiene, Wood Working, Adhesives, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Qida Chemicals Co. Ltd., Ter Hell and Co. GMBH, Exxonmobil Corporation, Soltex, Chevron Phillips Chemical, Evonik Industries AG, Ineos Oligomers, REXtac LLC, A S Harrison and Co. Pty Limited Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Amorphous Polyalphaolefin MarketPublished date: October 2025add_shopping_cartBuy Now get_appDownload Sample

Amorphous Polyalphaolefin MarketPublished date: October 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- Qida Chemicals Co. Ltd.

- Ter Hell and Co. GMBH

- Exxonmobil Corporation

- Soltex

- Chevron Phillips Chemical

- Evonik Industries AG

- Ineos Oligomers

- REXtac LLC

- A S Harrison and Co. Pty Limited

Our Clients

- 163690

- October 2025