Global Airfield Drainage Systems Market Size, Share, Growth Analysis By Product Type (Surface Drainage Systems, Subsurface Drainage Systems, Slot Drains, Channel Drains, Others), By Component (Pipes, Grates, Catch Basins, Geotextiles, Others), By Application (Commercial Airports, Military Airbases, Private Airfields, Others), By Installation Type (New Installation, Retrofit), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 183424

- Number of Pages: 247

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

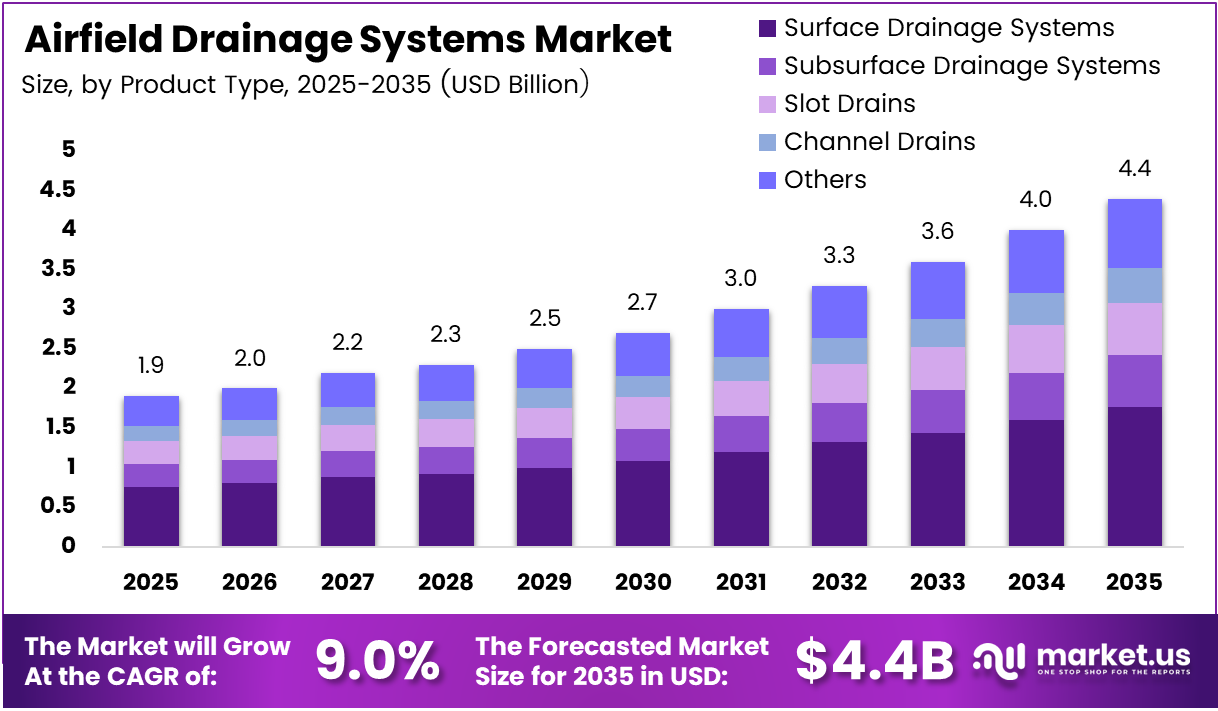

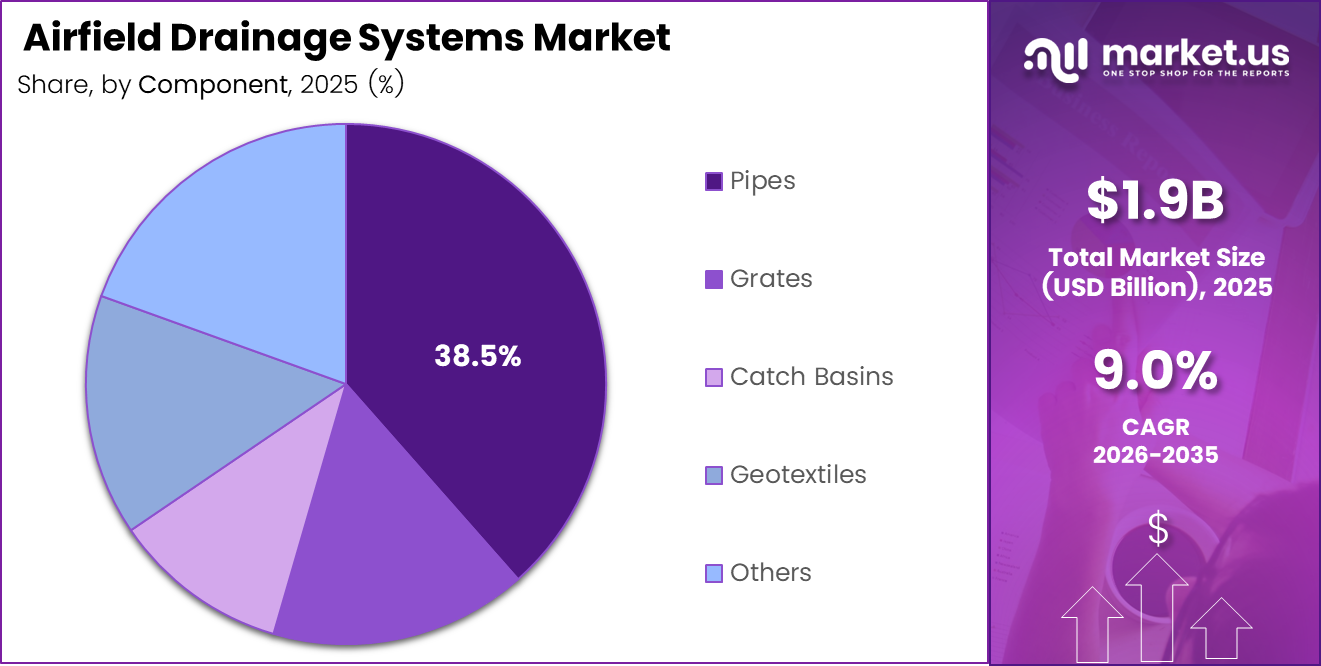

Global Airfield Drainage Systems Market size is expected to be worth around USD 4.4 Billion by 2035 from USD 1.9 Billion in 2025, growing at a CAGR of 9.0% during the forecast period 2026 to 2035.

Airfield drainage systems manage stormwater runoff, surface flooding, and subsurface water accumulation across airport pavements, runways, taxiways, and apron areas. These systems include surface drains, slot drains, channel drains, catch basins, pipes, and geotextile components. Effective drainage directly affects pavement life, aircraft operational safety, and regulatory compliance under international aviation standards.

Commercial airports represent the largest application base, accounting for 69.3% of total market demand. This concentration reflects the scale and complexity of commercial airport infrastructure, where runway surface water must be cleared within strict timeframes to maintain flight schedules and meet safety certification requirements set by bodies such as the FAA and ICAO.

New installation projects hold 65.8% share by installation type, driven by greenfield airport construction across Asia Pacific, the Middle East, and parts of Africa. However, the retrofit segment is expanding as aging airport infrastructure in North America and Europe requires drainage upgrades to meet revised stormwater standards and climate-adjusted design specifications.

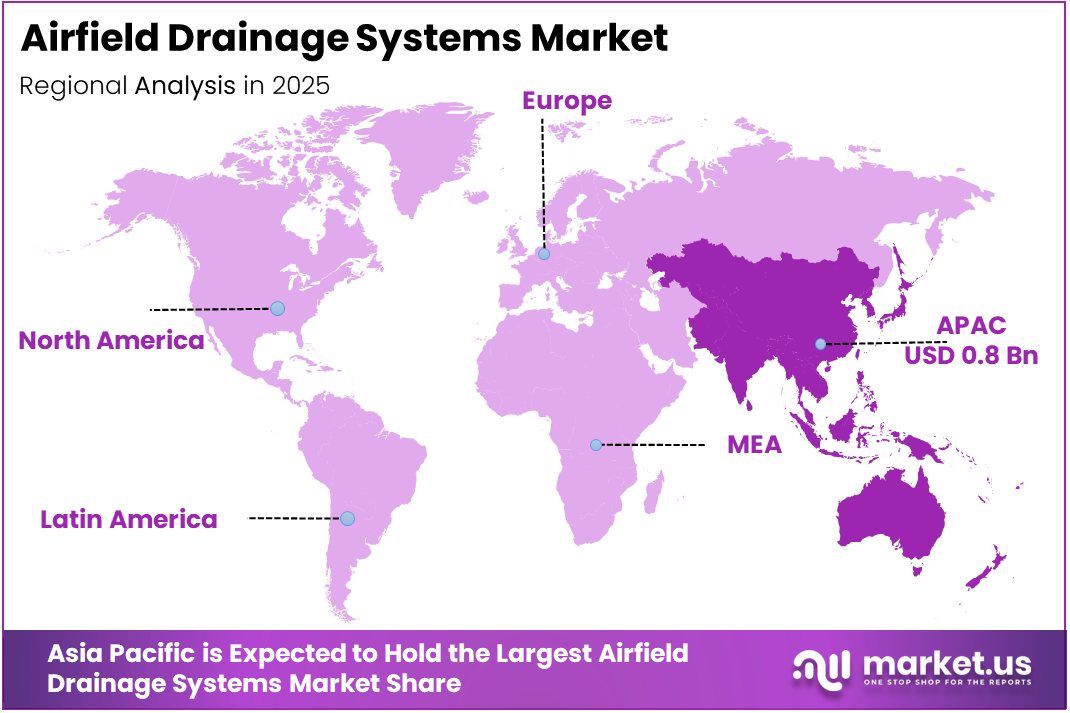

Asia Pacific leads the global market with a 43.7% share, valued at approximately USD 0.8 Billion. Government-backed aviation expansion programs in China, India, and Southeast Asia are adding runway capacity at a scale that requires purpose-built drainage infrastructure from project inception — making Asia Pacific the primary volume driver for the forecast period.

Airport infrastructure sustainability is reshaping procurement criteria for drainage systems. According to the Institute for Sustainable Infrastructure, by the end of 2025, there were 69 registered airport Envision projects, of which 28 were verified. This signals that airport owners are formalizing sustainability credentials — and drainage system performance is now evaluated within those frameworks, not treated as a secondary specification.

The pace of adoption is accelerating. According to the Institute for Sustainable Infrastructure, in 2025 alone, there were 23 new airport project registrations and 8 verifications under the Envision program. This growth means drainage system suppliers who align their products with Envision credit categories — particularly stormwater management and material recyclability — hold a structural advantage in tender evaluations.

Key Takeaways

- The global Airfield Drainage Systems Market was valued at USD 1.9 Billion in 2025 and is forecast to reach USD 4.4 Billion by 2035.

- The market grows at a CAGR of 9.0% during the forecast period 2026 to 2035.

- By Product Type, Surface Drainage Systems lead with a 39.6% share.

- By Component, Pipes hold the dominant share at 38.5%.

- By Application, Commercial Airports account for 69.3% of total market demand.

- By Installation Type, New Installation holds a 65.8% share.

- Asia Pacific dominates regionally with a 43.7% share, valued at USD 0.8 Billion.

Product Analysis

Surface Drainage Systems dominate with 39.6% due to direct runway water clearance requirements.

In 2025, Surface Drainage Systems held a dominant market position in the By Product Type segment of the Airfield Drainage Systems Market, with a 39.6% share. Runway surfaces require immediate water evacuation to prevent hydroplaning and maintain braking coefficient standards. Surface systems — installed along pavement edges, shoulders, and centrelines — provide the first and most critical layer of stormwater control in any airfield design.

Subsurface Drainage Systems serve as the structural foundation beneath airfield pavements, managing groundwater ingress and subgrade saturation that surface systems cannot address. These systems protect pavement structural integrity over the long term. Airports operating in high-rainfall or freeze-thaw climates depend on subsurface drainage to prevent base layer failure and extend pavement service life.

Slot Drains differentiate through a narrow-profile design that minimizes surface disruption while delivering high flow capacity per linear metre. Their low-profile format suits high-traffic aprons and terminal pavements where structural load ratings are critical. Slot drain adoption grows in retrofit applications where full pavement reconstruction is not feasible but drainage capacity must be upgraded.

Channel Drains carry the widest installation footprint across airfield perimeters, taxiway junctions, and cargo apron areas. Their modular construction reduces on-site fabrication time and accommodates varying flow rates. In 2025, ACO launched the ACO DRAIN® Qmax Neo high-capacity slot drainage system, available in 300 and 600 widths and made from recycled MDPE polymer, targeting heavy-load apron drainage with faster installation cycles.

Others in the product type segment include trench drains, edge drains, and inlet structures used in specialized airfield zones such as blast pads, de-icing pads, and fuel farm areas. These applications carry non-standard flow and contamination requirements. Their procurement is typically specification-driven rather than volume-driven, making them lower in share but higher in unit margin.

Component Analysis

Pipes dominate with 38.5% due to high volume use across all drainage system types.

In 2025, Pipes held a dominant market position in the By Component segment of the Airfield Drainage Systems Market, with a 38.5% share. Pipes form the conveyance backbone of every drainage network — surface-collected water routes through catch basins and ultimately discharges through buried pipe networks to retention or treatment systems. No drainage installation proceeds without significant pipe volume, which structurally anchors their share.

Grates control the entry point of surface water into the drainage network and carry a direct safety function — poorly specified grates create FOD (Foreign Object Debris) risk and potential aircraft damage. Grate specification at airports requires compliance with aircraft wheel load ratings and surface friction standards, creating a technically differentiated product segment that commands premium pricing relative to standard commercial drainage grates.

Catch Basins act as collection sumps at low points across aprons, taxiway intersections, and runway shoulders, where water concentrates before entering the pipe network. Their placement and sizing determine whether a system meets the design storm event capacity. At Charlotte-Douglas International Airport, the drainage design was upsized beyond FAA requirements to handle the 10-year storm event, illustrating how catch basin sizing is increasingly specified above minimum standards.

Geotextiles function as filtration and separation layers within subsurface drainage assemblies, preventing fine soil migration that would otherwise block drainage aggregate and reduce system permeability over time. Their use extends subsurface system service life significantly. Geotextile adoption grows alongside subsurface drainage installations in new greenfield airports where long-term pavement performance is a primary design objective.

Others in the component segment include outlet structures, headwalls, detention chambers, and oil-water separators required at de-icing and fuel management areas. At Raleigh-Durham International Airport, the stormwater management system incorporated the largest submerged gravel wetland of its kind in North Carolina, demonstrating that airport drainage components now extend well beyond conventional pipe-and-grate assemblies into integrated natural treatment systems.

Application Analysis

Commercial Airports dominate with 69.3% due to large pavement area and strict safety certification requirements.

In 2025, Commercial Airports held a dominant market position in the By Application segment of the Airfield Drainage Systems Market, with a 69.3% share. Commercial airport runways and aprons cover hundreds of hectares of impervious surface, generating stormwater volumes that require engineered collection, conveyance, and discharge systems. Regulatory certification requirements under FAA and ICAO standards mandate drainage performance levels that drive continuous investment.

Military Airbases operate under sovereign procurement channels and classified design standards, which limit their market accessibility to specialized contractors and approved suppliers. However, military base runway rehabilitation programs — particularly in NATO member countries and U.S. allied nations — represent a consistent procurement stream. Drainage system upgrades typically accompany runway resurfacing contracts, making them indirectly tied to defence infrastructure budget cycles.

Private Airfields carry the smallest share but represent the fastest-growing installation category in markets with expanding general aviation fleets — particularly in the Gulf states, Southeast Asia, and parts of Europe. Private airfield drainage specifications vary widely, creating opportunities for modular and prefabricated drainage products that can be installed without the full engineering resources required for commercial airport projects.

Others in the application segment include heliports, seaplane bases, and drone testing facilities. These non-traditional aviation surfaces are early-stage but technically require stormwater management solutions scaled to their footprint. As drone logistics infrastructure expands, purpose-built landing pads with integrated drainage will represent a new addressable product category for airfield drainage system manufacturers.

Installation Type Analysis

New Installation dominates with 65.8% due to greenfield airport construction across Asia and Middle East.

In 2025, New Installation held a dominant market position in the By Installation Type segment of the Airfield Drainage Systems Market, with a 65.8% share. Greenfield airport projects in Asia Pacific, the Middle East, and Sub-Saharan Africa require complete drainage infrastructure from ground up. These projects specify drainage systems during the master planning phase, giving manufacturers early design influence and long supply contracts tied to multi-year construction schedules.

Retrofit installations address existing airports where original drainage infrastructure no longer meets current design storm event standards, revised regulatory requirements, or expanded pavement footprints. North America and Western Europe represent the core retrofit market, as airports built between the 1960s and 1990s require drainage capacity upgrades. Retrofit projects typically involve slot drain and channel drain products that minimize pavement demolition while maximizing added capacity.

Key Market Segments

By Product Type

- Surface Drainage Systems

- Subsurface Drainage Systems

- Slot Drains

- Channel Drains

- Others

By Component

- Pipes

- Grates

- Catch Basins

- Geotextiles

- Others

By Application

- Commercial Airports

- Military Airbases

- Private Airfields

- Others

By Installation Type

- New Installation

- Retrofit

Drivers

Airport Expansion, Runway Safety Mandates, and Aviation Standards Push Airfield Drainage Investment

Governments across Asia, the Middle East, and Africa are funding new airport construction and runway modernisation at a pace that structural drainage infrastructure must match. Runway safety directly depends on water clearance speed — standing water increases aircraft skidding risk and reduces braking performance below certification thresholds. These safety imperatives convert drainage from a civil works commodity into a regulatory compliance requirement.

International aviation standards set by the FAA and ICAO specify minimum drainage performance levels for runway certification and continued airworthiness. According to the Institute for Sustainable Infrastructure, 84% of registered airport Envision projects use version 3 of the framework, which incorporates stormwater management as a formal credit category. This adoption rate signals that drainage performance now feeds directly into airport sustainability certification scores — not just construction compliance.

Emerging economies represent the sharpest incremental demand source. Government aviation infrastructure budgets in India, Indonesia, Vietnam, and across West Africa are allocating capital to both greenfield airports and secondary runway expansions. Each new runway requires a complete drainage system designed to local rainfall intensity data. This alignment of public investment with safety-driven specification requirements creates durable, budget-backed demand for advanced airfield drainage infrastructure.

Restraints

High Infrastructure Costs and Complex Regulatory Approval Processes Slow Airfield Drainage Deployment

Airfield drainage systems are among the most cost-intensive civil works components in airport construction. Large-scale installations require deep excavation, specialist pipe materials, load-rated grating, and engineered outlet structures — all priced at aviation-grade specifications. For secondary and regional airports with constrained capital budgets, the upfront cost of a compliant drainage system can delay project commencement or force phased construction that leaves drainage capacity short of design targets.

Complex engineering design requirements compound the cost barrier. Airfield drainage must be modelled against design storm events, soil infiltration rates, and runway geometry — a process requiring specialist hydraulic engineers and extended design review periods. Regulatory approval by civil aviation authorities adds further timeline risk. Projects that miss seasonal construction windows due to approval delays face cost escalation, which further discourages smaller airport operators from pursuing comprehensive drainage upgrades.

Maintenance costs add a long-term financial burden that procurement teams underestimate at the design stage. Catch basins require regular inspection and de-silting, grates demand periodic replacement due to FOD risk, and subsurface systems need CCTV inspection to detect blockages invisible from the surface. For airports in developing markets with limited maintenance budgets, this lifecycle cost profile creates reluctance to specify higher-performance systems even when upfront capital is available.

Growth Factors

Smart Drainage Technology, Sustainable Airports, and Rehabilitation Projects Unlock New Revenue Streams

Smart drainage monitoring integrates embedded sensors with airport operations platforms, enabling real-time detection of water accumulation, flow blockages, and system capacity thresholds. This capability shifts drainage management from reactive maintenance to predictive intervention — reducing runway closure risk and extending system service life. Airports that adopt sensor-integrated drainage gain a measurable operational advantage that justifies premium system pricing.

Green airport certification programs are expanding the scope of what drainage systems must deliver. Beyond stormwater conveyance, airports now specify systems that support water reuse, biodiversity protection, and climate resilience. At Charlotte-Douglas International Airport, stormwater drainage was designed to handle the 10-year storm event — exceeding standard FAA sizing — demonstrating that performance thresholds are actively rising above regulatory minimums and creating demand for upgraded system capacity.

Airport rehabilitation and runway resurfacing programs generate a recurring retrofit demand cycle. Every runway resurfacing project creates a defined window to upgrade underlying and adjacent drainage infrastructure. Regional airports across Latin America, Eastern Europe, and South Asia are entering active rehabilitation phases as original infrastructure reaches end-of-life. This retrofit wave runs parallel to greenfield construction demand and gives drainage system suppliers two concurrent market entry points.

Emerging Trends

Permeable Surfaces, Modular Components, and Climate-Resilient Design Redefine Airfield Drainage Standards

Permeable pavement technologies and advanced surface water management systems are entering airfield design specifications as airports seek to reduce peak runoff volumes and meet climate-adjusted drainage standards. These materials reduce the hydraulic load on conventional drain networks by allowing controlled infiltration at the pavement surface. Their adoption signals a shift from purely conveyance-focused drainage to integrated water management at the pavement level.

Modular and prefabricated drainage components are compressing construction timelines on airfield projects where runway closure periods are strictly limited. Prefabricated channel drain units, pre-assembled catch basin sections, and factory-cut geotextile rolls reduce on-site labour requirements and quality variation. ACO introduced its NEXITE® (NX) material in 2025 for the ACO DRAIN® family, offering full recyclability, high load-bearing strength, and REACH-compliant binders — specifically targeting airports that require both performance and sustainability credentials in a single product.

Climate resilience is now a formal design criterion in airport drainage specifications. Extreme rainfall events that previously fell outside standard design storm parameters now appear with greater frequency — forcing drainage engineers to upsize systems beyond historical norms. According to the Institute for Sustainable Infrastructure, the Atlanta South Deicing Facility project, verified in 2025, saw its stormwater system exceed minimum drainage standards specifically to reduce airfield flood risk and improve pavement durability. This project outcome reflects a broader shift: airports are specifying above-minimum drainage performance as operational insurance against climate variability.

Regional Analysis

Asia Pacific Dominates the Airfield Drainage Systems Market with a Market Share of 43.7%, Valued at USD 0.8 Billion

Asia Pacific holds a 43.7% share of the global Airfield Drainage Systems Market, valued at USD 0.8 Billion. State-led aviation expansion in China, India, and Southeast Asian nations is driving new airport construction at a scale that requires complete drainage infrastructure from design inception. High annual rainfall intensity across the region makes advanced stormwater management a non-negotiable design requirement, not an optional upgrade.

North America Airfield Drainage Systems Market Trends

North America holds a mature but active position in the airfield drainage systems space. Aging airport infrastructure built between the 1960s and 1990s requires systematic drainage rehabilitation, particularly as revised FAA stormwater standards raise minimum performance requirements. The U.S. Infrastructure Investment and Jobs Act has directed capital toward airport modernisation, creating a funded pipeline for drainage retrofit projects at mid-size and regional airports.

Europe Airfield Drainage Systems Market Trends

Europe represents a technically demanding market where EU environmental directives on stormwater discharge, de-icing fluid containment, and water quality set drainage performance standards above FAA equivalents. Airports in Germany, France, the UK, and Scandinavia are integrating drainage upgrades into broader sustainability certification programs. European buyers specify high-performance materials with environmental compliance credentials, driving demand for recyclable polymer drainage products.

Middle East and Africa Airfield Drainage Systems Market Trends

The Middle East combines large greenfield airport projects — particularly in Saudi Arabia and the UAE — with drainage specifications calibrated for intense but infrequent rainfall events. Gulf airports require systems engineered for flash flood risk despite low annual precipitation. Africa presents a long-term growth opportunity as aviation infrastructure investment increases under regional connectivity programs, though project financing constraints temper near-term deployment rates.

Latin America Airfield Drainage Systems Market Trends

Latin America holds a smaller but structurally important market position. Brazil and Mexico are the primary demand sources, with airport concession programs requiring drainage upgrades as part of broader infrastructure rehabilitation contracts. The region’s exposure to tropical rainfall — particularly in Central America and the Amazon basin — creates strong technical justification for drainage system investment, though procurement cycles remain longer than in more mature aviation markets.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

ACO Drain occupies the most visible brand position in the airfield drainage systems market, with a product portfolio that spans slot drains, channel drains, grates, and high-capacity apron drainage systems. Its strategic depth lies in product breadth — covering every drainage component category means ACO can supply entire airport projects through a single vendor relationship, reducing procurement complexity for airport contractors and operators.

ABT Inc. positions itself in the heavy-duty trench drain and airport drainage segment with products engineered to aircraft wheel load requirements. Its focus on load-rated drainage solutions for active airfield pavement differentiates it from suppliers serving lighter commercial applications. This specialisation allows ABT to compete on technical specification rather than price, targeting airport drainage projects where structural performance is a non-negotiable procurement criterion.

ACO Systems Ltd. brings integrated drainage system design capability to the market, offering not just individual products but complete engineered drainage solutions for complex airport layouts. This systems-level approach is particularly valuable on large greenfield airport projects where drainage must be coordinated across multiple pavement zones, flow regimes, and discharge points — work that generic drainage suppliers cannot easily service without specialist hydraulic engineering support.

ACO Polymer Products, Inc. focuses on polymer-based drainage channels and grating systems that offer weight advantages, corrosion resistance, and material recyclability over traditional cast iron and concrete alternatives. As airport sustainability certifications increasingly evaluate material lifecycle impact, polymer product manufacturers hold a structural advantage in tender evaluations that include environmental criteria alongside load and flow performance specifications.

Key players

- ACO Drain

- ABT Inc.

- ACO Systems Ltd.

- ACO Polymer Products, Inc.

- ACO Technologies plc

- ACO Infrastructure

- ACO Marine

- ACO Water Management

- ACO Severin Ahlmann GmbH & Co. KG

- ACO DRAIN S.A.

- ACO Passavant

- ACO Wildlife

- ACO Environment

- ACO Guss GmbH

- ACO Building Drainage

- ACO StormBrixx

- ACO Qmax

- ACO KerbDrain

- ACO Sport

- ACO Pipe

Recent Developments

- August 2024 — Advanced Drainage Systems, Inc. (ADS) announced the acquisition of Orenco Systems, Inc., a leading manufacturer of advanced onsite wastewater treatment and drainage-related products. This acquisition expanded ADS’s product range into engineered treatment-integrated drainage systems, positioning the combined entity to address airport drainage applications requiring effluent management alongside stormwater conveyance.

- 2025 — ACO launched the ACO DRAIN® Qmax Neo high-capacity slot drainage system, available in 300 and 600 widths and manufactured from recycled MDPE polymer. The product targets heavy-load airfield aprons and large-area drainage applications, offering optimised flow rates and faster installation cycles compared to conventional slot drain systems.

Report Scope

Report Features Description Market Value (2025) USD 1.9 Billion Forecast Revenue (2035) USD 4.4 Billion CAGR (2026-2035) 9.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Surface Drainage Systems, Subsurface Drainage Systems, Slot Drains, Channel Drains, Others), By Component (Pipes, Grates, Catch Basins, Geotextiles, Others), By Application (Commercial Airports, Military Airbases, Private Airfields, Others), By Installation Type (New Installation, Retrofit) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape ACO Drain, ABT Inc., ACO Systems Ltd., ACO Polymer Products, Inc., ACO Technologies plc, ACO Infrastructure, ACO Marine, ACO Water Management, ACO Severin Ahlmann GmbH & Co. KG, ACO DRAIN S.A., ACO Passavant, ACO Wildlife, ACO Environment, ACO Guss GmbH, ACO Building Drainage, ACO StormBrixx, ACO Qmax, ACO KerbDrain, ACO Sport, ACO Pipe Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Airfield Drainage Systems MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Airfield Drainage Systems MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- ACO Drain

- ABT Inc.

- ACO Systems Ltd.

- ACO Polymer Products, Inc.

- ACO Technologies plc

- ACO Infrastructure

- ACO Marine

- ACO Water Management

- ACO Severin Ahlmann GmbH & Co. KG

- ACO DRAIN S.A.

- ACO Passavant

- ACO Wildlife

- ACO Environment

- ACO Guss GmbH

- ACO Building Drainage

- ACO StormBrixx

- ACO Qmax

- ACO KerbDrain

- ACO Sport

- ACO Pipe

Our Clients

- 183424

- Mar 2026