Quick Navigation

Report Overview

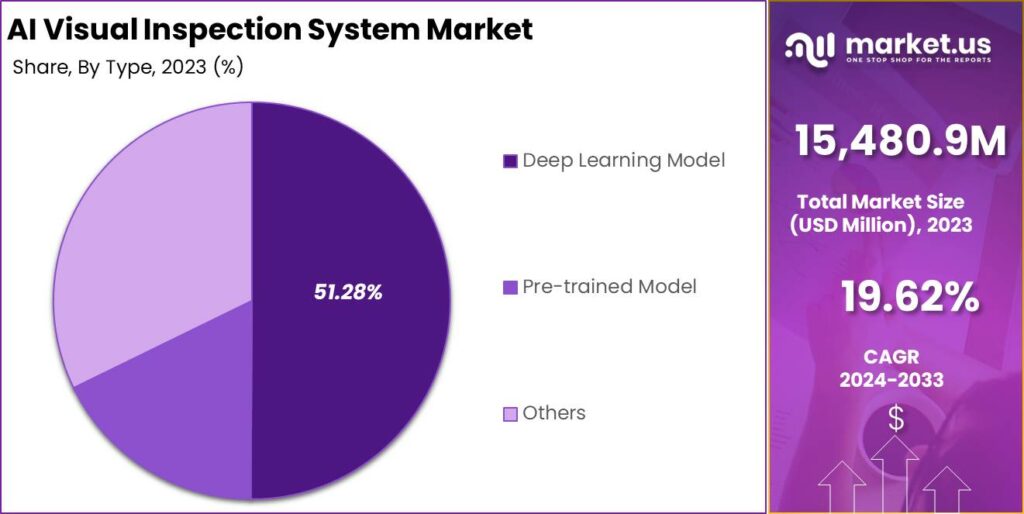

The Global AI Visual Inspection System Market size is expected to be worth around USD 89,726.3 Million By 2033, from USD 15,480.9 Million in 2023, growing at a CAGR of 19.62% during the forecast period from 2024 to 2033. North America dominated a 36.81% market share in 2023 and held USD 5,698.5 Million in revenue from the AI Visual Inspection System Market.

An AI Visual Inspection System is a technology that leverages artificial intelligence (AI) and computer vision to automatically inspect products or processes for defects or anomalies. It uses cameras, sensors, and machine learning algorithms to detect visual irregularities in products during manufacturing or quality control processes.

The market for AI visual inspection systems is expanding significantly across various industries due to its ability to enhance quality control and production efficiency. Industries such as manufacturing, automotive, and aerospace utilize these systems for critical inspections that demand high accuracy and reliability. The capability of AI systems to operate continuously and detect minute defects, which are often invisible to the human eye, has driven their adoption.

Moreover, the integration of these systems with existing production lines is supported by their scalability and the continuous advancements in AI and machine learning technologies. The primary driving factors for the AI Visual Inspection System market include the need for higher productivity and quality assurance across manufacturing processes.

Traditional manual inspection methods are often prone to errors, inconsistency, and fatigue. AI systems address these issues with their ability to perform continuous, precise inspections without the subjectivity and limitations of human inspectors. This not only enhances the detection of defects but also significantly reduces inspection times and labor costs.

Demand for AI visual inspection systems is driven by their critical role in maintaining high quality and compliance with industry standards, especially in sectors such as electronics, automotive, and pharmaceuticals. As industries strive for zero defects in their production processes, the need for sophisticated inspection systems that can detect even the slightest discrepancies is becoming essential.

The ongoing advancements in AI and computer vision technologies present substantial opportunities for the AI Visual Inspection market. These advancements are making it possible to deploy highly accurate inspection systems even with limited initial data, reducing setup times and costs. Additionally, the expansion of these technologies into emerging markets and the adaptation to various industrial applications offer new growth avenues.

Moreover, the ability to customize and scale these systems according to specific industrial needs adds a competitive edge to businesses adopting this technology. Recent technological advancements in AI visual inspection involve the enhancement of computer vision algorithms, which allow for finer tuning of AI models with fewer images, making the implementation process quicker and more cost-effective.

Improvements in camera technologies and machine learning frameworks have also contributed to the increased accuracy and efficiency of these systems. The integration of AI with robotics and automation for defect detection and correction is pushing the boundaries of what these systems can achieve, leading to broader applications across different production environments.

Key Takeaways

- The Global AI Visual Inspection System Market size is expected to be worth around USD 89,726.3 Million By 2033, from USD 15,480.9 Million in 2023, growing at a CAGR of 19.62% during the forecast period from 2024 to 2033.

- In 2023, Hardware held a dominant market position in the By Component segment of the AI Visual Inspection System Market, capturing more than a 47.43% share.

- In 2023, Deep Learning Model held a dominant market position in the By Type segment of the AI Visual Inspection System Market, capturing more than a 51.28% share.

- In 2023, Manufacturing held a dominant market position in the Industry Vertical segment of the AI Visual Inspection System Market, capturing more than a 42% share.

- North America dominated a 38.5% market share in 2023 and held USD 7.12 Billion in revenue from the AI Visual Inspection System Market.

- Europe has secured a market share of 24.55%. This notable percentage reflects Europe’s advanced manufacturing capabilities and stringent quality control requirements across various industries such as automotive and pharmaceuticals.

- The Asia-Pacific region shows a strong adoption rate with a market share of 30.47%. This is the highest among the regions, driven by rapid industrialization and expansion of manufacturing sectors in countries like China, Japan, and South Korea.

- Latin America holds a smaller portion of the market at 4.34%. While it is a modest share, it reflects growing interest and incremental adoption in regions striving to modernize their manufacturing sectors and improve product quality through technology.

- The Middle East & Africa region accounts for 3.83% of the market. This share indicates an emerging interest in AI technologies, with countries in these regions beginning to explore the benefits of digital transformation in industries such as oil and gas, which require stringent quality checks.

Component Analysis

In 2023, the Hardware segment held a dominant market position within the AI Visual Inspection System market, capturing more than a 47.43% share. This substantial market share can be attributed to the critical role hardware components play in the operational framework of AI visual inspection systems. These components, including cameras, processors, and sensors, are essential for capturing and processing high-quality images, which form the backbone of any AI-driven inspection solution.

The increasing demand for quality assurance and the automation of inspection processes across manufacturing industries has significantly driven the growth of the hardware segment. Manufacturers are continually seeking advanced hardware solutions that can integrate seamlessly with AI software to enhance precision and efficiency in detecting defects.

As industries such as automotive, electronics, and pharmaceuticals strive for higher accuracy and faster production times, the adoption of sophisticated inspection hardware becomes imperative. Furthermore, technological advancements in imaging technologies and the miniaturization of electronic devices have expanded the capabilities of visual inspection systems.

Modern hardware components are not only more efficient but also increasingly compact and easier to integrate into existing production lines, thereby reducing setup times and maintenance requirements. This has made AI-powered visual inspection systems more accessible to a broader range of industries, further bolstering the market growth of the hardware segment.

Investments in research and development by leading hardware manufacturers have also played a crucial role in the evolution of this segment. Enhanced features, such as improved image resolution, faster processing speeds, and greater environmental adaptability, make these hardware components more appealing to end-users seeking robust and reliable inspection solutions.

Type Analysis

In 2023, the Deep Learning Model segment held a dominant market position in the AI Visual Inspection System market, capturing more than a 51.28% share. This prominence is largely due to the superior capabilities of deep learning models in processing and interpreting complex visual data with a high degree of accuracy.

Deep learning models, which mimic human brain functionality, have proven particularly effective in identifying subtle patterns and anomalies that would typically elude traditional inspection methods. The adoption of deep learning models has been significantly accelerated by their ability to learn from vast amounts of data and improve over time without human intervention.

This aspect is crucial in environments like manufacturing, where the precision and speed of defect detection can directly influence production quality and throughput. Industries such as automotive, semiconductor, and packaging have shown rapid uptake of these systems as they strive to meet stringent quality standards while minimizing waste and operational costs.

Moreover, the integration of deep learning technologies has facilitated the automation of visual inspection across various challenging conditions, such as varying lighting and complex surface textures. These models are continuously evolving, driven by advancements in machine learning algorithms and computational power, which enhances their attractiveness to industries looking for cutting-edge technologies to refine their quality control processes.

The market’s confidence in deep learning models is also reinforced by the ongoing development and availability of specialized hardware and software that support these complex computations. As technology providers continue to unveil more robust and adaptable AI solutions, the deep learning model segment is expected to maintain its market dominance, fueled by its proven effectiveness and broadening scope of applications.

Industry Vertical Analysis

In 2023, the Manufacturing segment held a dominant market position in the AI Visual Inspection System market, capturing more than a 42% share. This substantial market share is primarily driven by the increasing need for precision and efficiency in manufacturing operations, where quality control is paramount.

AI visual inspection systems offer manufacturers the ability to detect defects and inconsistencies at a speed and accuracy that manual inspections cannot match, significantly reducing waste and increasing production efficiency. The adoption of AI visual inspection technologies in manufacturing is further propelled by the integration of Industry 4.0 principles, where automation and data exchange in manufacturing technologies are prevalent.

These systems are equipped to handle the complex and varied demands of modern manufacturing lines, adapting to different environments and learning from new data to improve over time. This adaptability is crucial in sectors such as automotive and consumer electronics, where production volumes are high and product standards are stringent.

Additionally, the economic benefits associated with implementing AI visual inspection systems, such as reduced downtime, lower rework costs, and decreased scrap rates, make these systems highly attractive to manufacturers aiming to optimize their operations. The ability of these systems to work continuously and under conditions that are challenging for human inspectors adds to their value proposition.

As manufacturers continue to focus on enhancing product quality and compliance with global standards, the reliance on AI visual inspection systems is expected to grow. Continuous technological advancements and the increasing affordability of these systems are likely to further drive their adoption across diverse manufacturing sectors, maintaining the segment’s leading position in the market.

Key Market Segments

By Component

- Hardware

- Software

- Services

By Type

- Deep Learning Model

- Pre-trained Model

- Others

By Industry Vertical

- Manufacturing

- Semiconductors & Electronics

- Healthcare

- Retail

- Others

Drivers

Key Drivers of AI Visual Inspection

In the AI Visual Inspection System market, several factors are driving growth. As an analyst, I observe that industries increasingly require precise and efficient manufacturing processes to ensure product quality and reduce waste.

AI-powered visual inspection systems provide real-time monitoring and defect detection, surpassing traditional methods in speed and accuracy. This technology is particularly crucial in the electronics, automotive, and pharmaceutical sectors where precision is paramount. Additionally, the integration of AI with IoT devices has enhanced the capabilities of inspection systems, making them smarter and more interconnected.

These advancements help companies maintain stringent quality standards, leading to the widespread adoption of AI visual inspection systems across various industries. This adoption trend is propelled further as companies aim to automate their processes and enhance productivity while minimizing human error.

Restraint

Challenges in AI Inspection Adoption

One major challenge is the high initial cost of integrating AI inspection technologies, which can deter small and medium enterprises (SMEs) from adopting these systems.

These costs include not only the expense of the systems themselves but also the investment in training personnel and upgrading existing infrastructure to support advanced AI capabilities. Furthermore, there are concerns about the complexity of AI systems, which require specialized knowledge to operate and maintain.

This complexity can lead to reluctance among businesses that lack the technical expertise, slowing down the adoption rate of AI visual inspection solutions. These factors combine to create a barrier that might slow market growth, particularly in sectors where cost sensitivity is more pronounced.

Opportunities

Expanding Markets for AI Inspection

The ongoing advancements in machine learning and computer vision are making these systems more accurate and faster, which broadens their applicability across various sectors, including manufacturing, automotive, electronics, and pharmaceuticals.

There is a growing trend towards automation within industries that are traditionally labor-intensive. This shift is not only improving the speed of production but also enhancing the precision of the inspection processes. Moreover, the expansion of smart factories and the adoption of Industry 4.0 principles are opening new avenues for the deployment of AI visual inspection systems.

These trends present a lucrative opportunity for market expansion as more companies look to integrate advanced technologies to maintain competitiveness and meet stringent quality standards.

Challenges

Hurdles in AI Inspection Systems

A primary concern is data privacy and security, particularly as these systems often handle sensitive information that, if compromised, could lead to significant financial and reputational damage.

Additionally, the integration of AI systems with existing infrastructure poses technical challenges, requiring substantial customization and testing to ensure compatibility and effectiveness. The complexity of configuring and maintaining these systems also demands a high level of expertise, which can be a scarce resource in many organizations.

Furthermore, regulatory hurdles, especially in industries such as pharmaceuticals and food processing, can delay the implementation of new technologies, affecting market growth. These challenges require thoughtful strategies and solutions to ensure the successful deployment and operation of AI visual inspection systems in various industries.

Growth Factors

Growth Drivers for AI Inspection

Industries such as automotive, electronics, and pharmaceuticals are rapidly adopting AI visual inspection systems to enhance accuracy and reduce defects, thereby improving overall product quality.

Secondly, technological advancements in AI and machine learning are continually enhancing the capabilities of these systems, making them more reliable and efficient. Moreover, as global manufacturing sectors push towards automation and smart factories, AI visual inspection systems are becoming integral to these initiatives.

Lastly, the rising trend towards minimizing human involvement in hazardous or repetitive tasks in industrial settings is further boosting the market. These factors collectively contribute to the robust growth of the AI visual inspection system market, promising substantial advancements in various sectors.

Emerging Trends

Trends Shaping AI Visual Inspection

One prominent trend is the integration of AI with Internet of Things (IoT) devices, which enhances the capabilities of inspection systems by enabling more extensive data collection and real-time analysis. This integration facilitates more sophisticated monitoring and predictive maintenance strategies.

Additionally, there’s a shift towards cloud-based platforms, which allow for the scalability of operations and accessibility of data across multiple locations, improving the operational efficiency of businesses. Moreover, the adoption of 3D vision technologies combined with AI is increasing, providing deeper insights and more accurate defect detection in complex manufacturing environments.

These trends are not only expanding the applications of AI visual inspection systems but are also driving innovations that meet the evolving demands of modern industries.

Regional Analysis

In 2023, North America held a dominant market position in the AI Visual Inspection System market, capturing more than a 36.81% share with revenue amounting to USD 5,698.5 million. This leading stance is predominantly attributed to the region’s robust manufacturing base, advanced technological infrastructure, and significant investments in research and development.

The presence of major technology players and startups focused on AI and machine learning innovations has fostered a conducive environment for the adoption of advanced inspection systems. The region’s leadership in the market is further bolstered by stringent quality standards across various industries, including automotive, pharmaceuticals, and electronics.

These sectors demand high accuracy and reliability in quality assurance processes, driving the adoption of AI visual inspection systems. North American manufacturers are increasingly integrating AI technologies to maintain competitive edges, such as enhancing production efficiency, reducing waste, and complying with regulatory standards.

Additionally, the widespread acceptance of Industry 4.0 and smart manufacturing practices in North America contributes significantly to the growth of the AI visual inspection market. These practices emphasize the importance of data and automation in manufacturing processes, where AI visual inspection systems play a crucial role in real-time monitoring and decision-making.

Government initiatives and funding in AI and manufacturing sectors also play a critical role in this regional market dominance. Policies that encourage the adoption of advanced technologies in industrial operations propel the market forward, making North America a significant contributor to the development and growth of global AI visual inspection technologies.

In Europe, the AI Visual Inspection System market accounted for 24.55% of the global share in 2023. This notable market presence is driven by the region’s strong focus on quality manufacturing, particularly in the automotive and pharmaceutical sectors.

European companies are increasingly leveraging AI visual inspection technologies to enhance operational efficiencies and adhere to the EU’s stringent regulatory standards. The rise of smart factories and the integration of Industry 4.0 technologies across European manufacturing plants further stimulate the demand for these advanced inspection solutions.

The Asia-Pacific region captured 30.47% of the market share, making it a significant player in the AI Visual Inspection System industry. This growth is fueled by the rapid industrialization in countries like China, Japan, and South Korea, combined with their substantial investments in electronics and automotive manufacturing. Asia-Pacific’s commitment to adopting cutting-edge technologies to maintain high standards in production quality significantly contributes to the adoption of AI-driven visual inspection systems.

Latin America holds a smaller segment of the market at 4.34%. The region is gradually recognizing the potential of AI visual inspection systems, especially in sectors like manufacturing and food processing. Although adoption rates are slower compared to North America and Asia-Pacific, there is a growing awareness of the benefits these systems offer in terms of quality control and operational efficiency.

Lastly, the Middle East and Africa have shown an interest in AI visual inspection technologies, accounting for 3.83% of the market. The adoption in this region is primarily driven by the oil and gas industry, where there is a high demand for maintaining stringent safety and quality standards. Investments in infrastructure development and industrial modernization, particularly in Gulf Cooperation Council (GCC) countries, are expected to boost the market growth in this region over the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The AI Visual Inspection Systems market sees significant activity from its key players, with strategic moves like acquisitions, mergers, and product launches driving their market positions.

IBM Corporation has been at the forefront, leveraging acquisitions to strengthen its AI capabilities. A recent acquisition aimed at enhancing its AI-driven visual inspection solutions allowed IBM to integrate advanced analytics into its manufacturing processes. Additionally, IBM consistently introduces new products that incorporate AI to streamline operations and improve accuracy in industrial environments, ensuring they remain competitive and innovative in the sector.

Alphabet Inc., through its subsidiary Google, has also made significant strides by launching innovative products that enhance AI visual inspection technologies. These products are designed to be adaptable across various industries, improving defect detection rates and operational efficiency. Alphabet’s approach to expansion often involves strategic partnerships and collaborations, which not only enhance product offerings but also broaden their applicability in different market segments.

Amazon.com Inc. focuses heavily on integrating AI into its vast array of services and has made notable advancements in visual inspection technologies through its Amazon Web Services (AWS) platform. By continually upgrading and launching new AI tools, Amazon supports industries ranging from electronics to automotive, helping them to improve quality control processes.

Top Key Players in the Market

- IBM Corporation

- Alphabet Inc.

- Amazon.com Inc.

- Siemens AG

- Cognex Corporation

- Fujitsu Limited

- NEC Corporation

- Ombrulla

- OMRON Corporation

- Basler AG

- Other Key Players

Recent Developments

- In June 2024, AMD launched a new series of GPUs designed to enhance AI visual inspection capabilities in industrial applications. These GPUs process visual data 50% faster than previous models.

- In May 2024, Alphabet, through its subsidiary Google, acquired VisionTech, a startup specializing in AI-driven visual inspection technologies, aiming to integrate these capabilities into its cloud services.

- In April 2024, Amazon introduced a new feature in its AWS platform that supports AI visual inspection, streamlining quality control processes for manufacturing clients, and improving detection accuracy by 30%.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 15,480.9 Million |

| Forecast Revenue (2033) | USD 89,726.6 Million |

| CAGR (2024-2033) | 19.62% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Hardware, Software), By Type (Deep Learning Model, Pre-trained Model, Others), By Industry Vertical (Manufacturing, Semiconductors & Electronics, Healthcare, Retail, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | IBM Corporation, Alphabet Inc., Amazon.com Inc., Siemens AG, Cognex Corporation, Fujitsu Limited, NEC Corporation, Ombrulla, OMRON Corporation, Basler AG, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |