Global AI in Self-Driving Cars Market By Component (Hardware (Sensors (LIDAR, RADAR, Ultrasonic), Processors (GPUs, ASICs, FPGAs), On-board computing units, Others), Software (AI Algorithms (Perception, Planning, Control), Sensor Fusion Modules, Decision-Making Systems, Others), Services (Data Labeling & Annotation, Cloud Support & Integration, Maintenance & Testing)), By Level of Autonomy (Level 1: Driver Assistance, Level 2: Partial Automation, Level 3: Conditional Automation, Level 4: High Automation, Level 5: Full Automation), By Technology (Computer Vision, Natural Language Processing (NLP), Machine Learning & Deep Learning, Sensor Fusion AI, Others), By Application (Perception (Object & Environment Recognition), Localization & Mapping (SLAM, GPS-AI Fusion), Decision-Making & Path Planning, Driver Monitoring Systems, Predictive Maintenance, Traffic & Navigation Assistance, Others), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs)), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2034

- Published date: Nov. 2025

- Report ID: 165124

- Number of Pages: 270

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

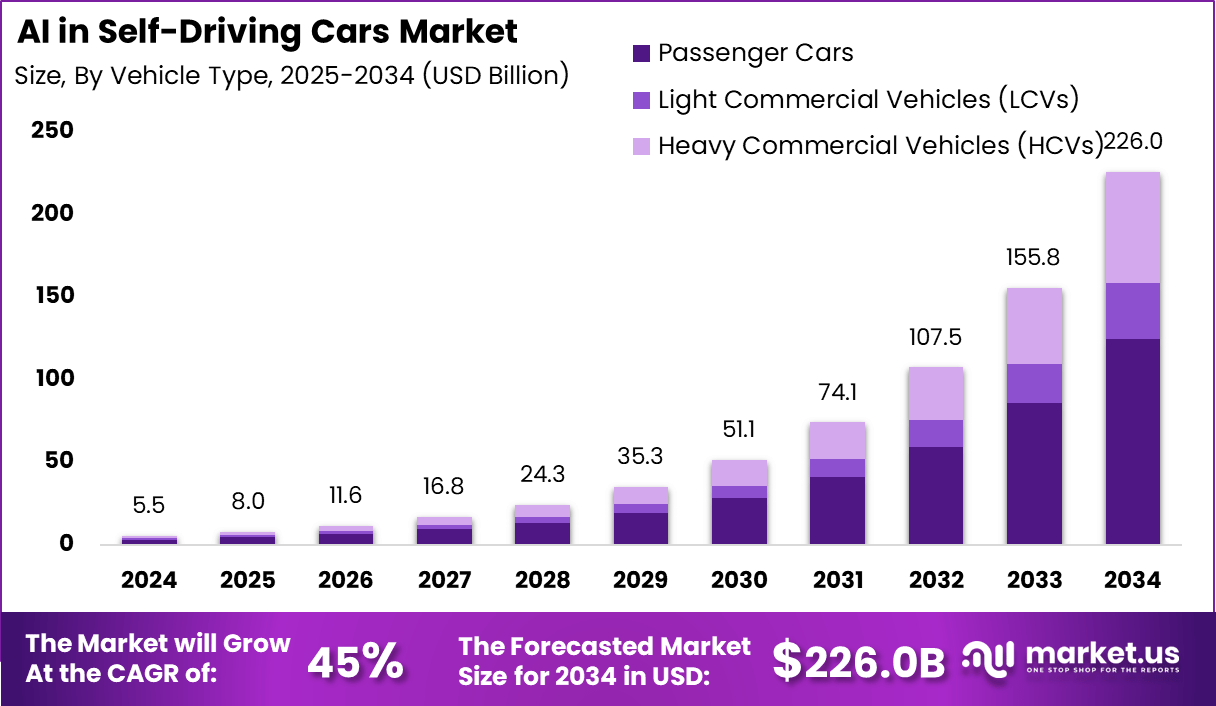

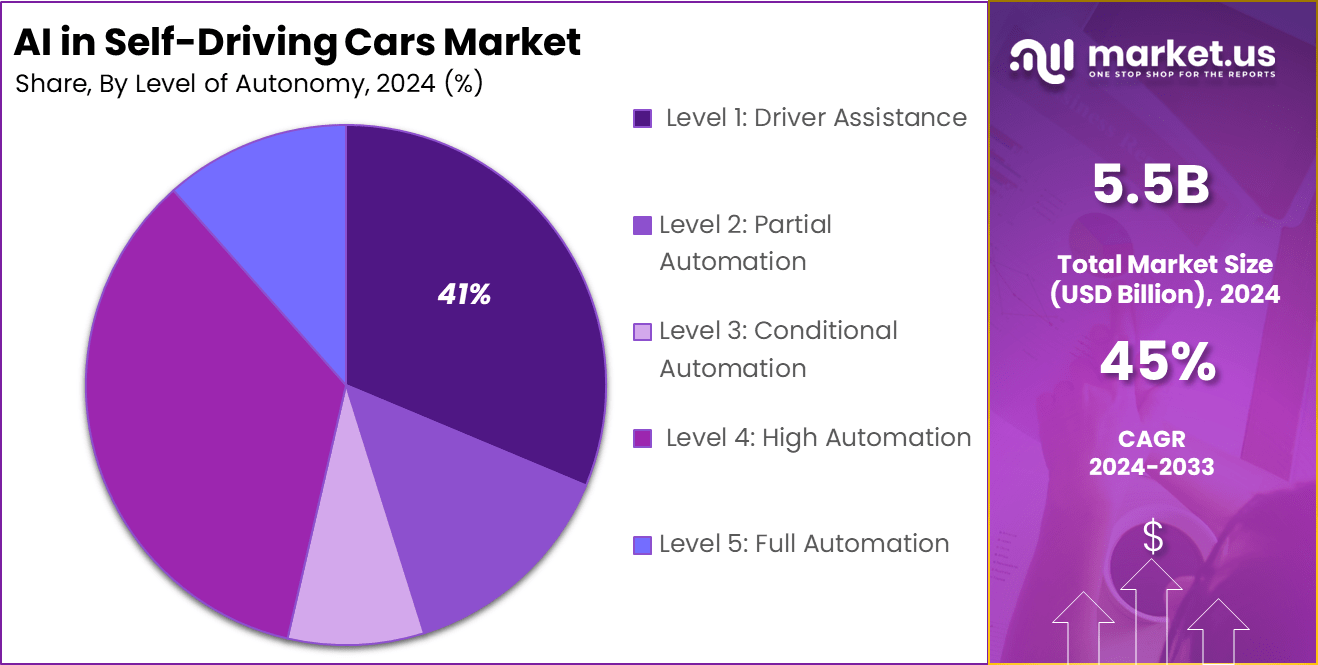

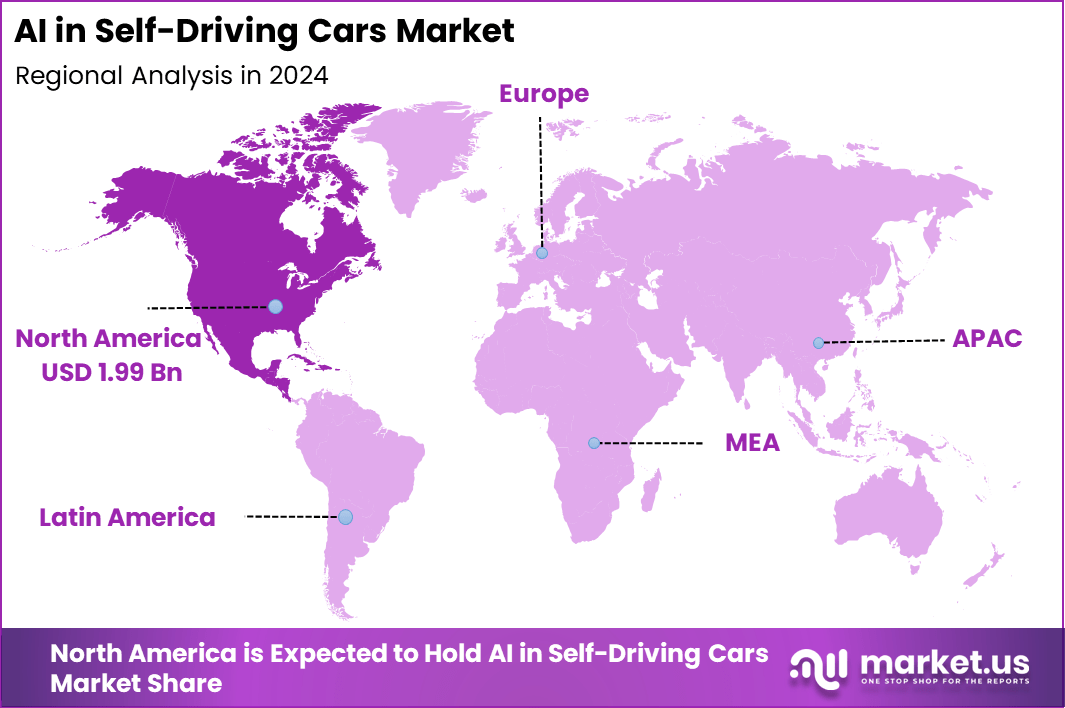

The Global AI in Self-Driving Cars Market generated USD 5.5 billion in 2024 and is predicted to register growth from USD 8.0 billion in 2025 to about USD 226.0 billion by 2034, recording a CAGR of 45% throughout the forecast span. In 2024, North America held a dominan market position, capturing more than a 36.2% share, holding USD 1.99 Billion revenue.

The AI in self-driving cars market has grown substantially as vehicle manufacturers and technology providers invest heavily in automation, sensing, and machine-learning systems for autonomous vehicles. The segment within the broader autonomous mobility landscape has matured to a point where AI technologies are now integral to ADAS and full self-driving platforms. The market’s expansion reflects the shift towards software-defined vehicles and mobility services in addition to traditional vehicle sales.

Several factors are pushing the growth of AI in self-driving cars. The biggest driver is the need for safer roads, as AI can react faster than humans and reduce the number of accidents. Governments are also introducing stricter safety regulations, encouraging automakers to adopt advanced driver assistance systems (ADAS) powered by AI. Urbanization and traffic congestion are other key reasons, especially in fast-growing regions like Asia-Pacific, where smart mobility solutions are in high demand.

Demand analysis reveals that ride-hailing services, logistics, and public transportation sectors are major adopters, deploying AI-driven autonomous fleets for safer, more efficient operations. AI-powered systems improve fuel efficiency and reduce emissions by optimizing driving patterns and route selection. Approximately 70% of consumer interest in self-driving cars is related to convenience and comfort, highlighting how AI enables passengers to utilize travel time productively, promoting a shift in mobility culture.

Top Market Takeaways

- By component, hardware accounts for 52.6% of the market share. This includes sensors (cameras, radar, lidar), processors (GPUs, AI chips), and other embedded systems crucial for real-time data processing and vehicle control.

- By level of autonomy, Level 1 (Driver Assistance) holds 40.7% share. This reflects widespread deployment of ADAS features such as adaptive cruise control, lane-keeping assist, and automated braking, which improve safety while still requiring driver oversight.

- By technology, computer vision dominates with 38.8% share. Computer vision enables perception capabilities like object detection, lane recognition, and environment understanding, which are fundamental for autonomous operation.

- By application, perception (object & environment recognition) captures 35.6% market share. This involves real-time detection and classification of obstacles, pedestrians, vehicles, and road infrastructure.

- By vehicle type, passenger cars dominate the market with 55.2% share, driven by increased integration of AI technologies in consumer vehicles aiming for enhanced safety, comfort, and driving automation.

- Regionally, North America accounts for 36.2% of the market.

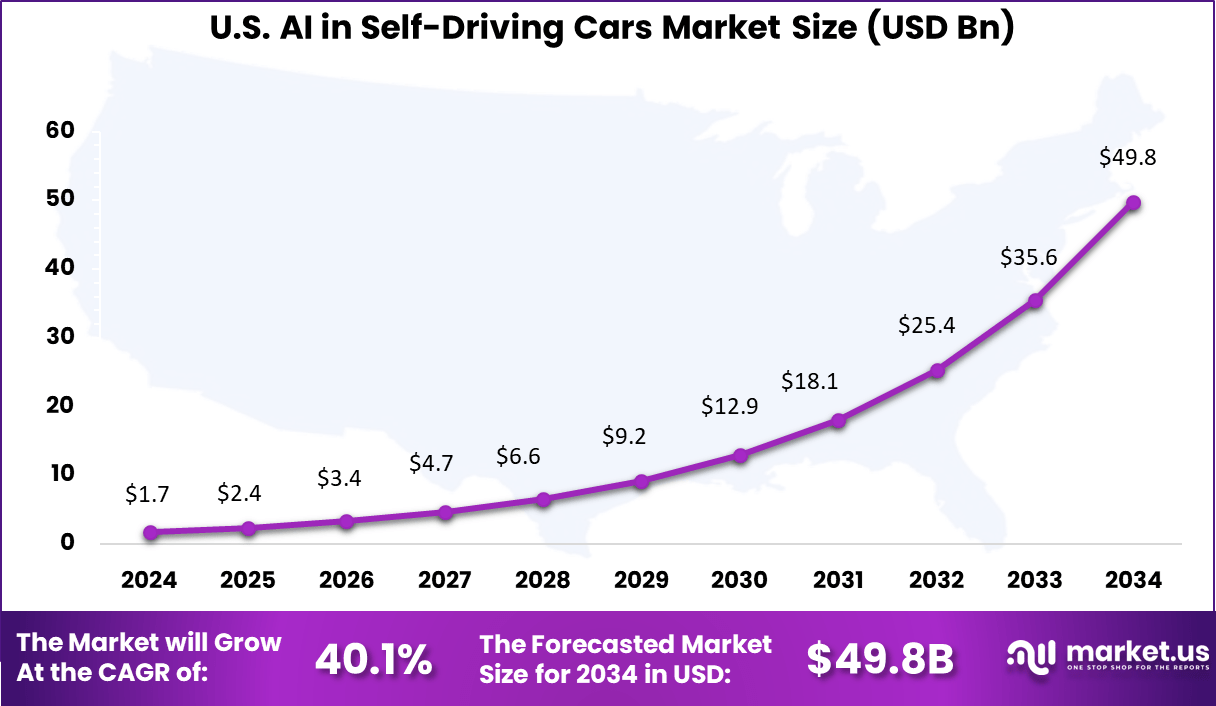

- The U.S. market size is estimated at USD 1.71 billion in 2025.

- The market is growing at a rapid CAGR of 40.1%, fueled by advances in AI technologies, increasing adoption of autonomous features by OEMs, supportive regulatory frameworks, and growing consumer demand for safer, intelligent vehicles.

- Major drivers include partnerships between automakers and AI tech firms, government investments in smart transportation infrastructure, and technological progress in edge computing and sensors.

By Component

In 2024, Hardware makes up 52.6% of the AI in self-driving cars market. This includes sensors, processors, and control units that enable vehicles to perceive and respond to their environment. The demand for advanced hardware is driven by the need for reliable, real-time data processing, which is essential for safe autonomous operation.

Automakers and suppliers are investing heavily in hardware to support features like lane detection, automatic braking, and adaptive cruise control. As vehicles become more autonomous, the complexity and capability of onboard hardware continue to grow, making it a central part of the self-driving ecosystem.

By Level of Autonomy

Level 1 driver assistance systems are the most common, accounting for 41% of the market. These systems provide basic support such as lane-keeping and adaptive cruise control, helping drivers stay safe and comfortable on the road. Most vehicles with AI features today fall into this category, offering incremental improvements over manual driving.

Driver assistance is popular because it enhances safety without requiring full autonomy. Users appreciate the extra layer of protection and convenience, especially in heavy traffic or on long journeys. As technology advances, these systems are becoming standard in new vehicles.

By Technology

In 2024, Computer vision is used in 38.8% of AI self-driving car applications. This technology allows vehicles to interpret visual data from cameras and sensors, detecting objects, pedestrians, and road signs in real time. Computer vision is crucial for safe navigation and decision-making in complex environments.

The reliability of computer vision is improving with advances in deep learning and neural networks. These systems help cars understand their surroundings and respond quickly to changing conditions, making them a key enabler of autonomous driving.

By Application

Perception, which includes object and environment recognition, accounts for 35.6% of AI applications in self-driving cars. This function allows vehicles to identify and classify objects around them, such as other cars, pedestrians, and traffic signals. Accurate perception is essential for safe and efficient autonomous operation.

AI-powered perception systems use data from cameras, LiDAR, and radar to build a detailed picture of the vehicle’s surroundings. This helps cars make informed decisions about steering, braking, and route planning, reducing the risk of accidents.

By Vehicle Type

In 2024, Passenger cars represent 55.2% of the AI in self-driving cars market. Most autonomous technology is being developed and deployed in private vehicles, where safety, comfort, and convenience are top priorities. The rise in demand for luxury and smart vehicles is driving adoption in this segment.

Automakers are integrating AI-based driver assistance into passenger cars to improve safety and efficiency. As regulations and consumer expectations evolve, the integration of AI in passenger vehicles is expected to continue growing.

Emerging Trends

The AI in self-driving cars market is advancing with several emerging trends that are reshaping the future of transportation. A key trend is the move toward higher levels of automation, with vehicles increasingly achieving Level 3 and Level 4 autonomy, allowing cars to handle complex driving tasks with limited human input.

AI-powered systems are becoming smarter through improved machine learning algorithms and sensor fusion technologies, which enable them to perceive their environment more accurately and make faster, safer decisions in real time. Additionally, AI’s role is expanding beyond just driving to include in-cabin monitoring for driver alertness and personalized passenger experiences.

Growth Factors

One of the biggest growth drivers is the urgent need to enhance road safety, as AI in autonomous vehicles can significantly reduce accidents caused by human error, which accounts for a large majority of crashes. The adoption of AI is also supported by growing investments from automakers and tech companies aiming to commercialize fully autonomous vehicles.

Another essential factor boosting growth is the rise of 5G networks and vehicle-to-everything (V2X) communication, which let cars exchange data with other vehicles, infrastructure, and the cloud for better traffic management and navigation. Regulatory support and pilot programs in key regions further accelerate market development by ensuring safety standards and easing adoption.

Key Market Segments

By Component

- Hardware

- Sensors (LIDAR, RADAR, Ultrasonic)

- Processors (GPUs, ASICs, FPGAs)

- On-board Computing Units

- Others

- Software

- AI Algorithms (Perception, Planning, Control)

- Sensor Fusion Modules

- Decision-Making Systems

- Others

- Services

- Data Labeling & Annotation

- Cloud Support & Integration

- Maintenance & Testing

By Level of Autonomy

- Level 1: Driver Assistance

- Level 2: Partial Automation

- Level 3: Conditional Automation

- Level 4: High Automation

- Level 5: Full Automation

By Technology

- Computer Vision

- Natural Language Processing (NLP)

- Machine Learning & Deep Learning

- Sensor Fusion AI

- Others

By Application

- Perception (Object & Environment Recognition)

- Localization & Mapping (SLAM, GPS-AI Fusion)

- Decision-Making & Path Planning

- Driver Monitoring Systems

- Predictive Maintenance

- Traffic & Navigation Assistance

- Others

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

Regional Analysis

In 2024, North America emerged as a leading market for AI in self-driving cars, with a dominant share of 36.2% reflecting the region’s strong technological and automotive capabilities. This growth is underpinned by a rich ecosystem of tech innovators, automakers, and research institutions working collaboratively to advance autonomous driving technologies.

The market benefits from a robust pipeline of AI applications including real-time decision-making, advanced driver assistance systems, and predictive analytics designed to enhance vehicle safety and efficiency. The presence of major players like Tesla, Waymo, and Cruise further accelerates innovation and adoption, supported by progressive regulatory frameworks and extensive testing zones in states like California and Arizona.

Focusing on the U.S., the AI in self-driving cars market was valued at around USD 1.71 billion in 2024 and is projected to grow rapidly with a staggering CAGR of 40.1%. This explosive growth is fueled by a favorable regulatory environment, substantial government and private sector investments, and consumer demand for enhanced safety and convenience.

The U.S. leads with pioneering pilot programs, extensive AV testing zones, and collaborations between technology companies and automakers, spearheading large-scale deployment of AI-enabled vehicles. Additionally, advancements in machine learning, sensor fusion, and edge computing continue to elevate the capabilities of self-driving cars.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Rapid Advances in AI and Sensor Technologies

The AI in self-driving cars market is driven by continuous advancements in artificial intelligence, machine learning, and sensor technologies like LiDAR and radar. These technologies enable vehicles to perceive their environment, make real-time decisions, and navigate complex traffic scenarios with little to no human intervention.

The ability of AI to reduce accidents caused by human error, improve traffic flow, and enhance passenger safety is boosting demand globally. With increasing investments by major automakers and tech firms, AI systems are becoming more sophisticated and reliable.

Restraint

High Costs and Regulatory Challenges

Despite promising growth, high costs associated with AI development and sensor integration restrain widespread adoption. Implementing reliable autonomous systems involves expensive hardware like high-definition sensors and powerful computing platforms. These costs can limit full-scale production and affordability, especially for mid-range vehicles.

Moreover, regulatory frameworks governing autonomous driving are still evolving, leading to uncertainty and delays in market rollout. Governments impose stringent safety standards and testing requirements, requiring significant time and resources. Legal and liability questions around AI decisions in driving further complicate the regulatory landscape.

Opportunity

Expansion of Mobility Services and Smart City Integrations

AI in self-driving cars offers substantial opportunities through integration with mobility-as-a-service (MaaS) models such as ride-hailing and shared autonomous fleets. These services forecast massive growth by providing affordable, convenient, and efficient urban mobility solutions, reducing congestion and emissions.

Additionally, the rise of smart city infrastructure, including connected traffic systems and 5G networks, presents opportunities for enhanced vehicle-to-everything (V2X) communication. This real-time interaction between vehicles, infrastructure, and pedestrians improves safety and traffic management, paving the way for broader AI-driven autonomous vehicle adoption.

Challenge

Managing Data Complexity and Ensuring Public Trust

A critical challenge lies in handling the enormous volumes of real-time data generated by AI-powered self-driving cars. Processing sensor inputs swiftly and accurately is essential to safe navigation but demands advanced edge computing systems and AI models. This complexity requires continuous software updates and robust cybersecurity to prevent vulnerabilities.

Building public trust in autonomous technology also remains a hurdle. Safety concerns, ethical dilemmas over decision-making, and unfamiliarity with AI driving create hesitancy among consumers and regulators. Transparency in AI operations, extensive testing, and effective communication will be crucial to overcoming skepticism and encouraging widespread acceptance.

Competitive Analysis

The AI in Self-Driving Cars Market is anchored by leading innovators such as Waymo LLC, Nvidia Corporation, and Tesla, Inc.. These companies develop core autonomous driving stacks that include perception, mapping, path planning, and decision systems. Their platforms rely on advanced neural networks, sensor fusion, and real-time processing to improve road safety and reduce the need for driver intervention.

Global automotive manufacturers including Mercedes-Benz Group AG, General Motors (Super Cruise), Toyota Motor Corporation, BMW Group, and Volkswagen Group are integrating AI to enhance highway assist, automated parking, and hands-free driving features. Their focus is on high-precision sensors, redundancy architectures, and predictive analytics that manage complex traffic conditions.

Specialised contributors such as Mobileye, Amazon (Zoox), and other major players advance components for vision processing, lidar interpretation, and autonomous ride-hailing development. Their work supports fleet-level intelligence, accident-avoidance models, and continuous learning systems.

Top Key Players in the Market

- Waymo LLC

- Nvidia Corporation

- Tesla, Inc.

- Mercedes-Benz Group AG

- Amazon (Zoox)

- General Motors (Super Cruise)

- Toyota Motor Corporation

- Mobileye

- BMW Group

- Volkswagen Group

- Other Major Players

Recent Developments

- November, 2025, Waymo announced plans to launch its robotaxi service in Detroit, Las Vegas, and San Diego, expanding its commercial autonomous vehicle operations. Waymo aims to provide 1 million trips per week by the end of 2026, marking significant scaling beyond current markets such as Phoenix and San Francisco.

- October, 2025, General Motors unveiled an “eyes-off” autonomous driving capability for its Super Cruise hands-free driving system, initially rolling out on the 2028 Cadillac Escalade IQ electric SUV. GM highlighted over 700 million miles driven with Super Cruise without accidents attributed to the system, emphasizing enhanced safety and convenience.

Report Scope

Report Features Description Market Value (2024) USD 5.5 Bn Forecast Revenue (2034) USD 226 Bn CAGR(2025-2034) 45% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Hardware (Sensors (LIDAR, RADAR, Ultrasonic), Processors (GPUs, ASICs, FPGAs), On-board computing units, Others), Software (AI Algorithms (Perception, Planning, Control), Sensor Fusion Modules, Decision-Making Systems, Others), Services (Data Labeling & Annotation, Cloud Support & Integration, Maintenance & Testing)), By Level of Autonomy (Level 1: Driver Assistance, Level 2: Partial Automation, Level 3: Conditional Automation, Level 4: High Automation, Level 5: Full Automation), By Technology (Computer Vision, Natural Language Processing (NLP), Machine Learning & Deep Learning, Sensor Fusion AI, Others), By Application (Perception (Object & Environment Recognition), Localization & Mapping (SLAM, GPS-AI Fusion), Decision-Making & Path Planning, Driver Monitoring Systems, Predictive Maintenance, Traffic & Navigation Assistance, Others), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs)) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Waymo LLC, Nvidia Corporation, Tesla, Inc., Mercedes-Benz Group AG, Amazon (Zoox), General Motors (Super Cruise), Toyota Motor Corporation, Mobileye, BMW Group, Volkswagen Group, Other Major Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  AI in Self-Driving Cars MarketPublished date: Nov. 2025add_shopping_cartBuy Now get_appDownload Sample

AI in Self-Driving Cars MarketPublished date: Nov. 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- Waymo LLC

- Nvidia Corporation

- Tesla, Inc.

- Mercedes-Benz Group AG

- Amazon (Zoox)

- General Motors (Super Cruise)

- Toyota Motor Corporation

- Mobileye

- BMW Group

- Volkswagen Group

- Other Major Players

Our Clients

- 165124

- Nov. 2025