Global AI Energy Efficiency Tools Market Size, Share, Industry Analysis Report By Component (Software & Platforms – Predictive Maintenance, Energy Management Systems (EMS), Building Automation & Control Systems, Demand Response Management, Others; Services – Consulting & Integration, Deployment & Maintenance, Managed Services), By Deployment Mode (Cloud-Based, On-Premise), By End-User Industry (Commercial & Residential Real Estate, Manufacturing & Industrial, Utilities & Power Grids, Oil, Gas, & Energy Producers, Transportation & Logistics, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: August 2025

- Report ID: 156554

- Number of Pages: 236

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

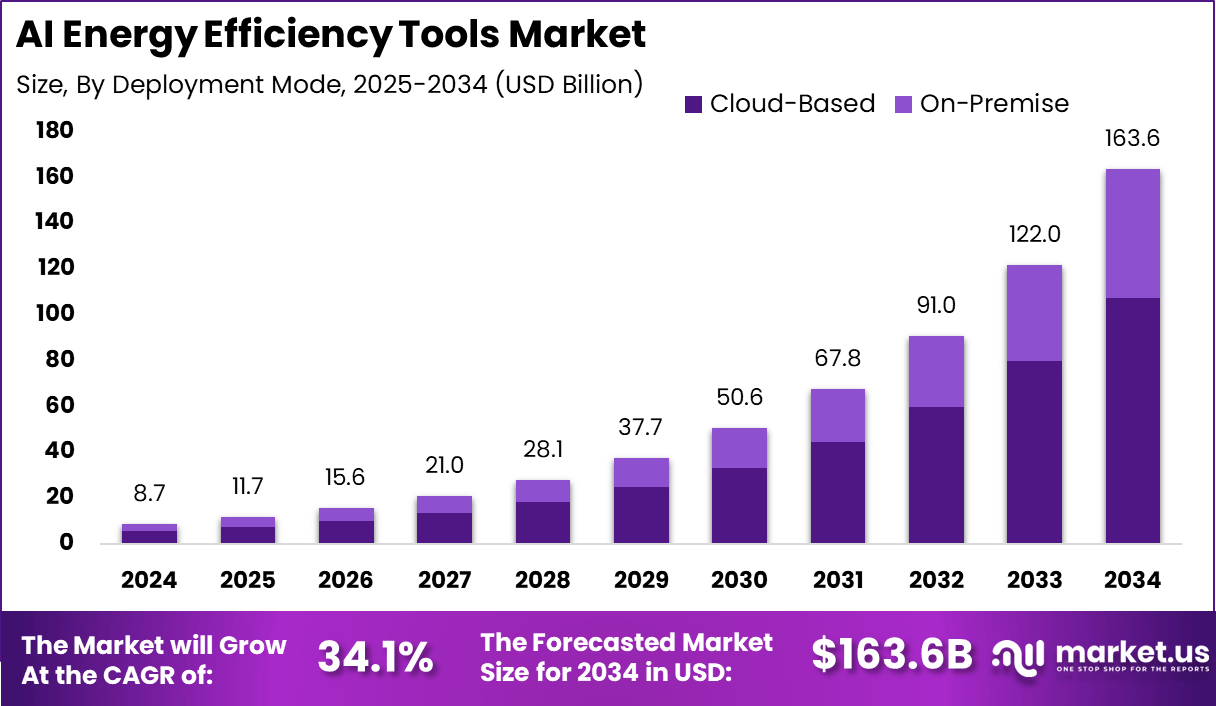

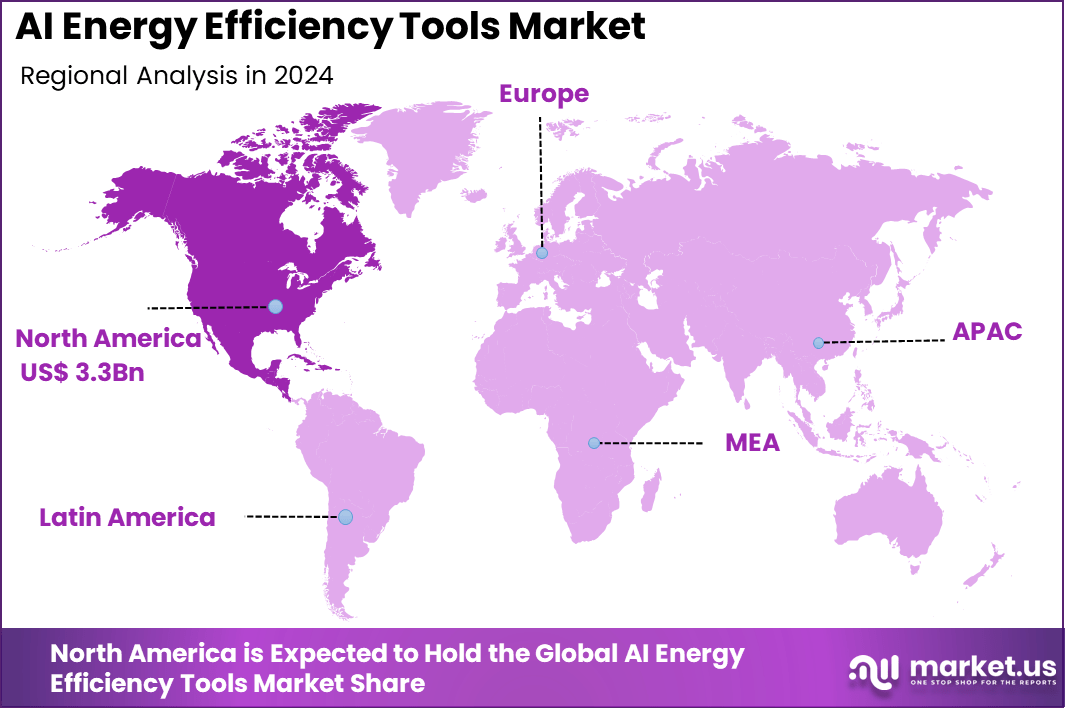

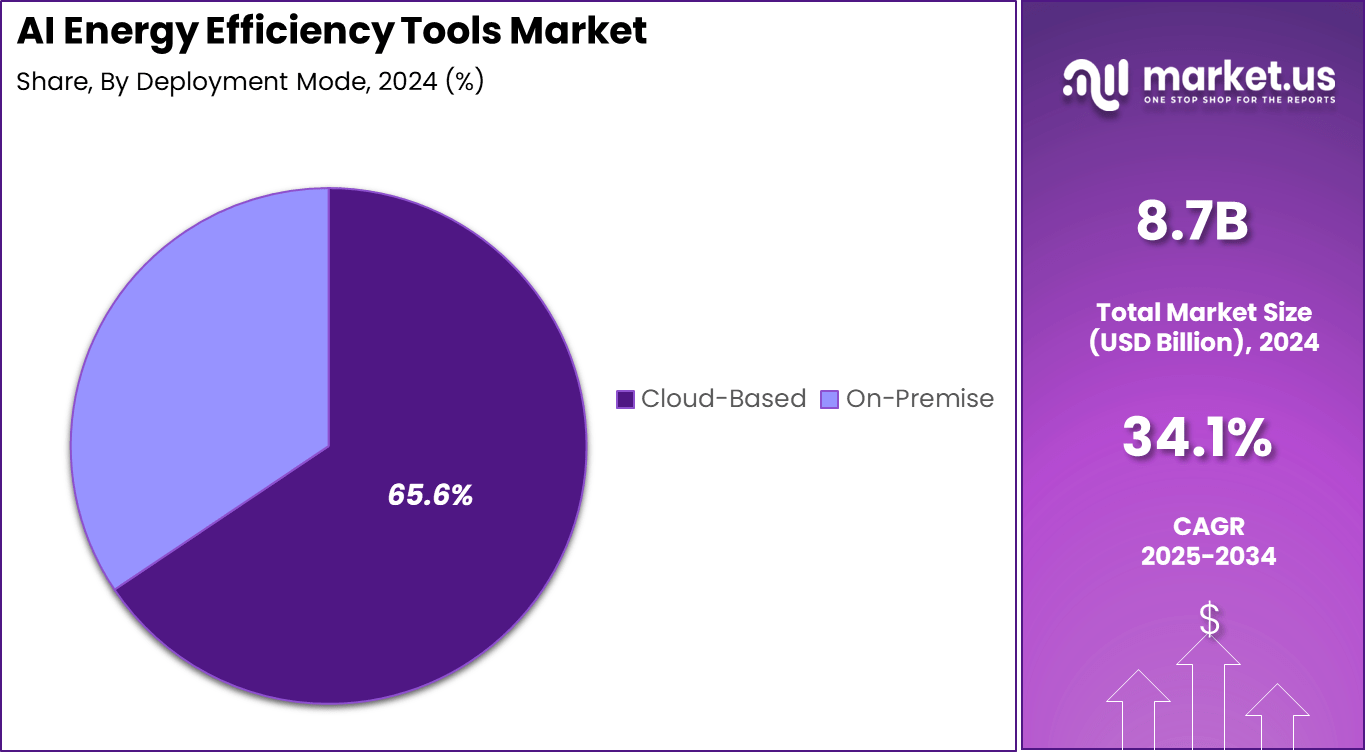

The Global AI Energy Efficiency Tools Market size is expected to be worth around USD 163.6 Billion By 2034, from USD 8.7 billion in 2024, growing at a CAGR of 34.1% during the forecast period from 2025 to 2034. In 2024, North America held a dominan market position, capturing more than a 38.2% share, holding USD 3.3 Billion revenue.

The AI Energy Efficiency Tools Market focuses on technologies that use AI to optimize energy consumption, reduce waste, and improve operational efficiency across various sectors. These tools use data analytics, machine learning, and IoT integration to monitor and manage energy usage in real time, helping organizations to cut costs and enhance sustainability. This market is growing due to the global emphasis on reducing energy consumption and environmental impact while maintaining operational productivity.

Top driving factors for this market include rising energy costs, increasing regulatory pressure to meet sustainability goals, and the advancement of AI, IoT, and cloud computing technologies. These factors push companies to adopt AI tools to enhance energy management, reduce carbon footprints, and comply with government policies. Additionally, the need to modernize aging infrastructure and the growing share of renewable energy sources create a strong demand for AI-driven energy optimization.

Based on data from wifitalents, Around 62% of energy companies are already applying AI to optimize renewable energy generation, highlighting its role in driving efficiency and sustainability. Predictive maintenance powered by AI is reducing equipment downtime by as much as 40%, while AI-based forecasting models are delivering more than 20% improvement in accuracy compared to traditional approaches.

The adoption of AI-enabled demand response programs is also reshaping grid management, with the potential to cut peak load by up to 15%. Confidence in its future impact is strong, as 75% of energy executives believe AI will be critical for enhancing operational efficiency. In addition, AI applications in energy storage are extending battery lifespan by about 30%, while asset management processes are seeing efficiency gains of nearly 35%, underscoring the broad benefits of AI across the energy value chain.

Key Insight Summary

- By Component, Software & Platforms led with a 68.2% share, reflecting high demand for AI-powered energy monitoring and optimization solutions.

- By Deployment Mode, Cloud-Based systems dominated with a 65.6% share, driven by scalability, integration, and real-time energy analytics.

- By End-User Industry, Commercial & Residential Real Estate accounted for 30.4% share, highlighting the use of AI tools in smart buildings, energy savings, and sustainability initiatives.

- By Region, North America held the leading position with 38.2% share, supported by strong regulatory push and adoption of green building technologies.

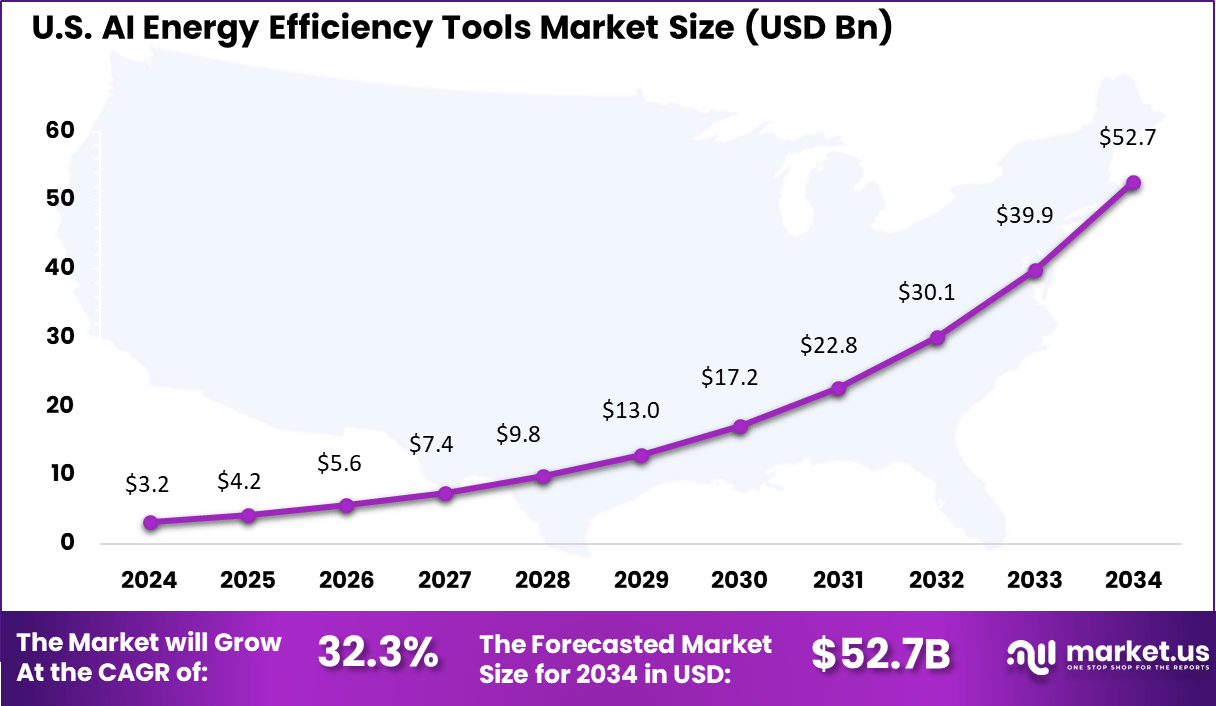

- The U.S. market was valued at USD 3.21 Billion in 2024, with a projected CAGR of 32.3%, reflecting rapid adoption of AI-based energy management systems.

US Market Size

The U.S. AI Energy Efficiency Tools Market was valued at USD 3.2 Billion in 2024 and is anticipated to reach approximately USD 52.7 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 32.3% during the forecast period from 2025 to 2034.

In 2024, North America held a dominant market position, capturing more than 38.2% share and generating USD 3.3 billion revenue in the AI energy efficiency tools market. The region’s leadership is largely driven by strict regulatory frameworks promoting sustainable energy practices and the early adoption of advanced digital solutions.

Companies across industries are under growing pressure to meet carbon reduction goals, and AI-powered tools are being widely deployed to monitor, analyze, and optimize energy consumption in real time. Strong government incentives for green technologies, combined with a well-developed digital infrastructure, have positioned North America as the leading hub for innovation in this sector.

The leadership of North America is further supported by the high concentration of enterprises and utilities adopting AI to reduce operational costs and improve efficiency. Growing awareness among consumers and industries about energy conservation has accelerated demand for predictive analytics and automation solutions. The presence of major technology providers and active startups has driven innovation, enabling quicker use of AI-driven energy efficiency tools in commercial, residential, and industrial sectors.

Analysts’ Viewpoint

Investment opportunities in this market arise from the growing need to upgrade energy infrastructure, the expansion of renewable energy, and increasing government incentives for sustainability projects. Investors are drawn by the potential to develop smarter energy systems and scalable AI solutions that support corporate environmental commitments.

Business benefits from AI energy efficiency tools include reduced operational costs, greater energy reliability, and improved compliance with environmental regulations. Companies gain better visibility into energy data, enabling targeted actions to improve efficiency and maintenance scheduling. This leads to prolonged equipment life, fewer breakdowns, and enhanced brand reputation as sustainable operators.

The regulatory environment is increasingly influencing this market, with laws such as the EU AI Act introducing requirements around energy consumption transparency and sustainability in AI applications. These regulations drive the responsible use of AI while encouraging innovation to reduce carbon footprints. Compliance with such frameworks is becoming a business imperative, stimulating demand for AI tools designed to deliver measurable energy efficiency results in regulated markets.

Key Use Cases

Use Case Description Predictive Maintenance Early detection of equipment failure via sensor data analysis to reduce downtime and costs Smart Grid Management AI-based optimization of power distribution and load balancing Real-Time Energy Monitoring AI-enhanced smart meters for demand-supply balancing and customer energy management Energy Optimization in Buildings AI controls HVAC, lighting, and appliances for reduced consumption Waste Management Tracking and analyzing waste to improve recycling and reduce food waste Carbon Emission Reduction Using AI to model and reduce industrial energy use and emissions Economic Impact

Impact Area Details Cost Savings Reduction in energy waste, operational costs, and unplanned maintenance Efficiency Gains Up to 30% improvement in energy usage due to optimized operations Environmental Benefits Significant reductions in CO₂ emissions and carbon footprint Market Growth Drivers Rising energy costs, sustainability goals, regulatory pressures By Component

|In 2024, Software and platforms dominate the AI energy efficiency tools market with a 68.2% share, reflecting their central role in enabling organizations to optimize energy usage. These solutions integrate AI technologies such as machine learning, predictive analytics, and real-time monitoring to analyze vast energy data and provide actionable insights.

The software platforms facilitate automated control of energy systems, enabling reductions in waste and operational costs while improving sustainability metrics. The importance of these platforms is growing as businesses and property managers increasingly seek end-to-end solutions that can integrate with existing infrastructure like smart meters and IoT devices.

By Deployment Mode

In 2024, Cloud-based deployment accounts for 65.6% of the market, highlighting the preference for scalable, flexible, and cost-efficient AI energy efficiency solutions. Cloud platforms simplify implementation by eliminating the need for significant on-premises infrastructure, providing access to advanced AI capabilities through subscription-based models.

The cloud-based model also supports continuous updates and integration with other enterprise systems, enhancing overall operational efficiency. Its accessibility and reduced upfront investment make it especially attractive for mid-sized and large organizations aiming to implement energy-saving initiatives without complex IT overhead.

By End-User Industry

The commercial and residential real estate sector constitutes 30.4% of the AI energy efficiency tools market, driven by growing regulatory pressures and sustainability goals. Building owners and property managers use AI-powered tools to reduce energy consumption in heating, ventilation, air conditioning (HVAC), lighting, and other building systems.

These technologies enable predictive maintenance, occupant behavior analysis, and automated energy management, leading to significant cost savings and reduced carbon footprints. The adoption in real estate is fueled by the increasing integration of smart building technologies and IoT sensors, allowing AI tools to optimize energy use continuously based on real-time conditions.

Key Market Segments

By Component

- Software & Platforms

- Predictive Maintenance

- Energy Management Systems (EMS)

- Building Automation & Control Systems

- Demand Response Management

- Others

- Services

- Consulting & Integration

- Deployment & Maintenance

- Managed Services

By Deployment Mode

- Cloud-Based

- On-Premise

By End-User Industry

- Commercial & Residential Real Estate

- Manufacturing & Industrial

- Utilities & Power Grids

- Oil, Gas, & Energy Producers

- Transportation & Logistics

- Others

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Increasing Demand for Energy Efficiency and Sustainability

A significant driver for AI energy efficiency tools is the growing demand for energy efficiency coupled with sustainability goals. Businesses and utility companies are facing mounting pressure to reduce operational costs and carbon footprints. AI technologies enable these organizations to optimize energy consumption by analyzing vast amounts of data from smart meters and IoT devices.

This helps in precise load forecasting, predictive maintenance, and integration of renewable energy sources, leading to more efficient energy use and lower emissions. Such capabilities make AI tools indispensable for modern energy management systems aiming to meet stringent regulatory requirements and sustainability targets.

Additionally, the push for integrating AI with smart grids and renewable energies such as solar and wind is accelerating market growth. AI improves the reliability of energy distribution networks and supports the transition to cleaner energy by managing the variability and intermittency of renewable sources. The use of AI-powered predictive analytics enhances operational efficiency, reduces downtime through early fault detection, and assists in demand-response management.

Restraint

High Energy Consumption of AI Systems

A major restraint facing AI energy efficiency tools is the significant energy consumption required to run AI models and data centers that support them. AI operations, especially training complex models, demand substantial computational power, leading to increased electricity usage.

Research indicates that data centers hosting AI could consume energy levels comparable to entire countries, and their consumption is expected to grow sharply by 2030. This surge in AI-driven power demand adds strain to existing energy grids and contradicts the sustainability goals that AI is supposed to support.

Moreover, data centers supporting AI require massive water resources for cooling, raising environmental concerns beyond electricity consumption. The infrastructure needed for AI deployment is costly and resource-intensive, which can be prohibitive for many organizations. This energy and resource demand create operational challenges, limiting the scalability and widespread adoption of AI-driven energy efficiency solutions until more energy-friendly AI hardware and efficient data center practices are adopted

Opportunity

Advanced AI for Grid Modernization and Renewable Integration

The rapidly evolving energy sector presents a significant opportunity for AI tools to drive modernization and support renewable energy integration. AI’s ability to analyze real-time data for precise energy demand forecasting, anomaly detection, and automated optimization can transform aging grid infrastructures into smarter, more flexible systems.

By improving grid management and balancing supply and demand, AI supports the increasing share of intermittent renewable energy sources like solar and wind, ensuring reliable energy delivery. Furthermore, regulatory frameworks worldwide are promoting sustainability, making AI-driven solutions critical for compliance and competitive advantage.

With advancements in big data analytics, IoT, and machine learning, AI offers the chance to reduce operational costs, enhance predictive maintenance, and improve overall energy efficiency. This positions AI as a vital enabler of the global energy transition towards cleaner and more resilient energy systems, creating new market opportunities for technology providers and energy companies alike.

Challenge

Integration Complexity and Data Quality Issues

One of the key challenges for AI energy efficiency tools is the complexity involved in integrating AI technologies into existing energy infrastructures. Many energy systems rely on outdated hardware and software, making it difficult to retrofit AI solutions without significant investment in modernization.

The integration process can be costly, time-consuming, and demanding in terms of technical expertise, slowing down the adoption curve for many organizations. Another substantial challenge is ensuring the availability of high-quality, real-time energy data needed to train and operate AI models effectively.

Inaccurate, incomplete, or delayed data can reduce AI performance, requiring frequent retraining and updates, which adds to operational costs. The lack of seamless data sharing across distributed energy networks hinders the ability of AI solutions to optimize energy consumption accurately.

Competitive Analysis

ABB, Eaton, General Electric, Hitachi, Honeywell, and Johnson Controls are recognized as long-established industrial leaders. Their expertise in automation, electrical infrastructure, and building management has enabled them to develop AI-based platforms that reduce energy waste and optimize system performance. These companies continue to integrate AI with traditional hardware systems, which strengthens their ability to serve manufacturing, construction, and utilities sectors.

Technology-driven corporations such as Microsoft, Amazon, IBM, and Infosys are playing a critical role by embedding advanced AI capabilities into cloud-based energy efficiency tools. Their solutions focus on real-time data analytics, predictive maintenance, and large-scale optimization of energy use across industries. Microsoft and Amazon, for example, integrate AI into smart building solutions and large data centers.

Specialized automation and engineering firms including Siemens, Schneider Electric, Mitsubishi Electric, Rockwell Automation, and C3.ai are strongly positioned. Their competitive advantage lies in tailored AI solutions for industrial operations, smart grids, and renewable energy integration. Siemens and Schneider Electric, in particular, are advancing intelligent energy distribution platforms, while Mitsubishi Electric and Rockwell Automation focus on industrial automation and AI-enabled control systems.

Top Key Players in the Market

- ABB Ltd.

- Amazon.com Inc.

- C3.ai Inc.

- Eaton Corp. plc

- General Electric Co.

- Hitachi Ltd.

- Honeywell International Inc.

- Infosys Ltd.

- IBM Corp.

- Johnson Controls International Plc

- Microsoft Corp.

- Mitsubishi Electric Corp.

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Others

Recent Developments

- In early 2025, ABB acquired Dutch energy management specialist Sensorfact to expand its digital energy portfolio, especially for industrial customers, leveraging AI to reduce energy costs and optimize demand peaks. Additionally, ABB made a minority investment in Canadian AI energy startup Edgecom Energy, which uses generative AI to transform complex energy datasets into actionable savings.

- Hitachi has accelerated investments in energy-efficient technology with a $400 million commitment focused on AI-driven solutions and renewable integration. In June 2025, Hitachi partnered with Southwest Power Pool to develop AI-powered tools to speed planning and improve grid reliability and flexibility.

Report Scope

Report Features Description Market Value (2024) USD 8.7 Bn Forecast Revenue (2034) USD 163.6Bn CAGR(2025-2034) 34.1% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Software & Platforms – Predictive Maintenance, Energy Management Systems (EMS), Building Automation & Control Systems, Demand Response Management, Others; Services – Consulting & Integration, Deployment & Maintenance, Managed Services), By Deployment Mode (Cloud-Based, On-Premise), By End-User Industry (Commercial & Residential Real Estate, Manufacturing & Industrial, Utilities & Power Grids, Oil, Gas, & Energy Producers, Transportation & Logistics, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape ABB Ltd., Amazon.com Inc., C3.ai Inc., Eaton Corp. plc, General Electric Co., Hitachi Ltd., Honeywell International Inc., Infosys Ltd., IBM Corp., Johnson Controls International Plc, Microsoft Corp., Mitsubishi Electric Corp., Rockwell Automation Inc., Schneider Electric SE, Siemens AG, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  AI Energy Efficiency Tools MarketPublished date: August 2025add_shopping_cartBuy Now get_appDownload Sample

AI Energy Efficiency Tools MarketPublished date: August 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- ABB Ltd.

- Amazon.com Inc.

- C3.ai Inc.

- Eaton Corp. plc

- General Electric Co.

- Hitachi Ltd.

- Honeywell International Inc.

- Infosys Ltd.

- IBM Corp.

- Johnson Controls International Plc

- Microsoft Corp.

- Mitsubishi Electric Corp.

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Others

Our Clients

- 156554

- August 2025