Quick Navigation

Report Overview

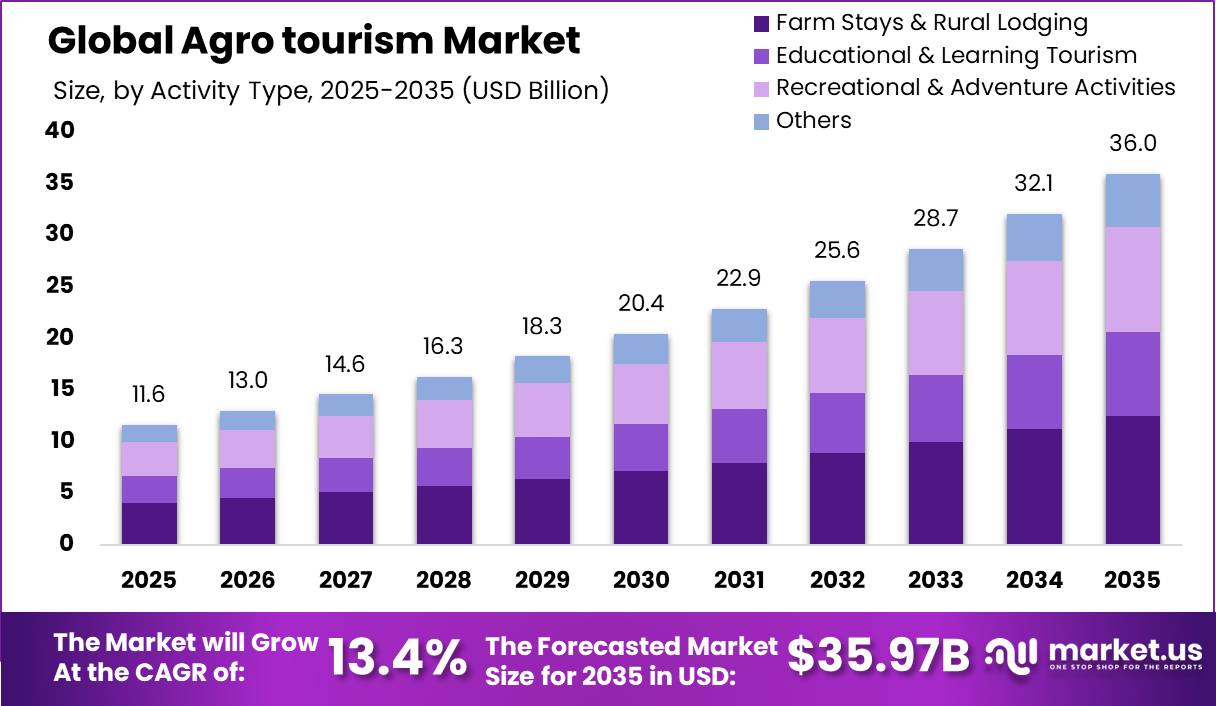

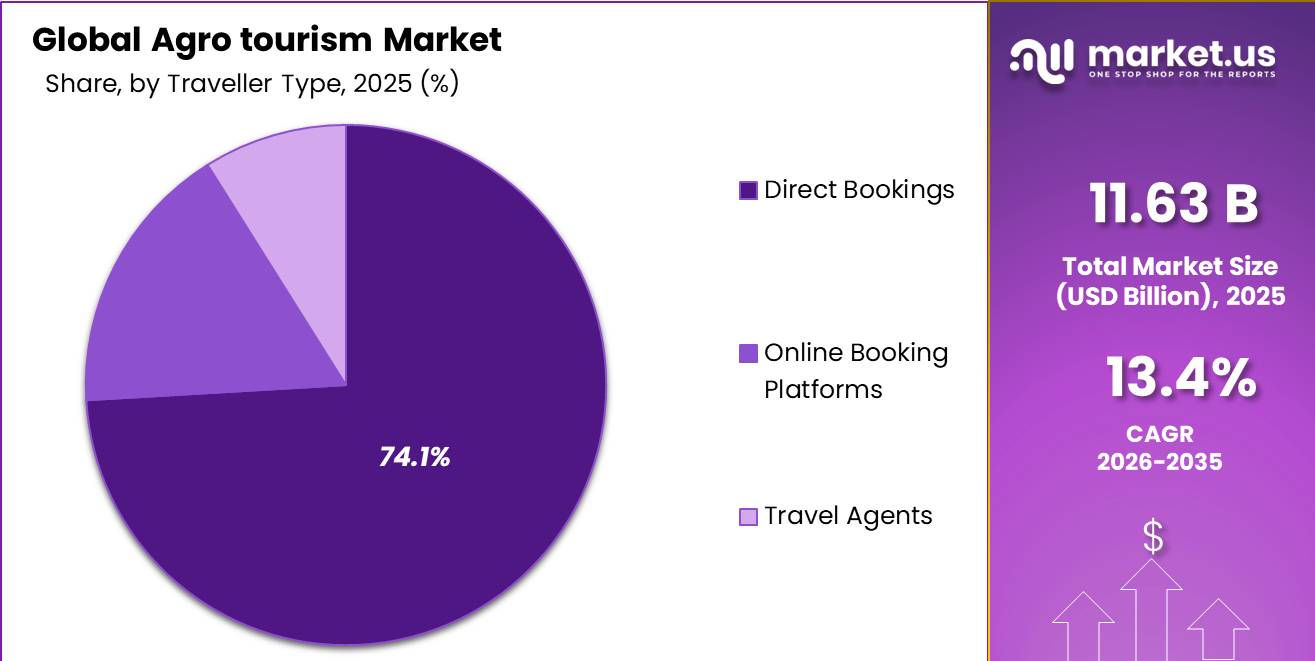

Global Agritourism Market size is expected to be worth around USD 35.97 Billion by 2035 from USD 11.63 Billion in 2025, growing at a CAGR of 13.4% during the forecast period 2026 to 2035.

The Agritourism Market encompasses farm-based visitor experiences that combine agriculture with hospitality, recreation, and education. This market spans farm stays, rural lodging, educational farm programs, vineyard tours, and hands-on harvesting activities. Operators range from small family farms offering seasonal visits to organized rural tourism networks delivering structured multi-day experiences. This reflects a structural shift in how agricultural land generates income.

Key Takeaways

- Market size in 2025: USD 11.63 Billion

- Market size in 2035: USD 35.97 Billion

- CAGR (2026 to 2035): 13.4%

- Dominant Activity Type segment: Farm Stays and Rural Lodging at 34.80%

- Dominant Distribution Channel segment: Direct Bookings at 74.1%

- Dominant Traveler Type segment: Family Groups at 34.60%

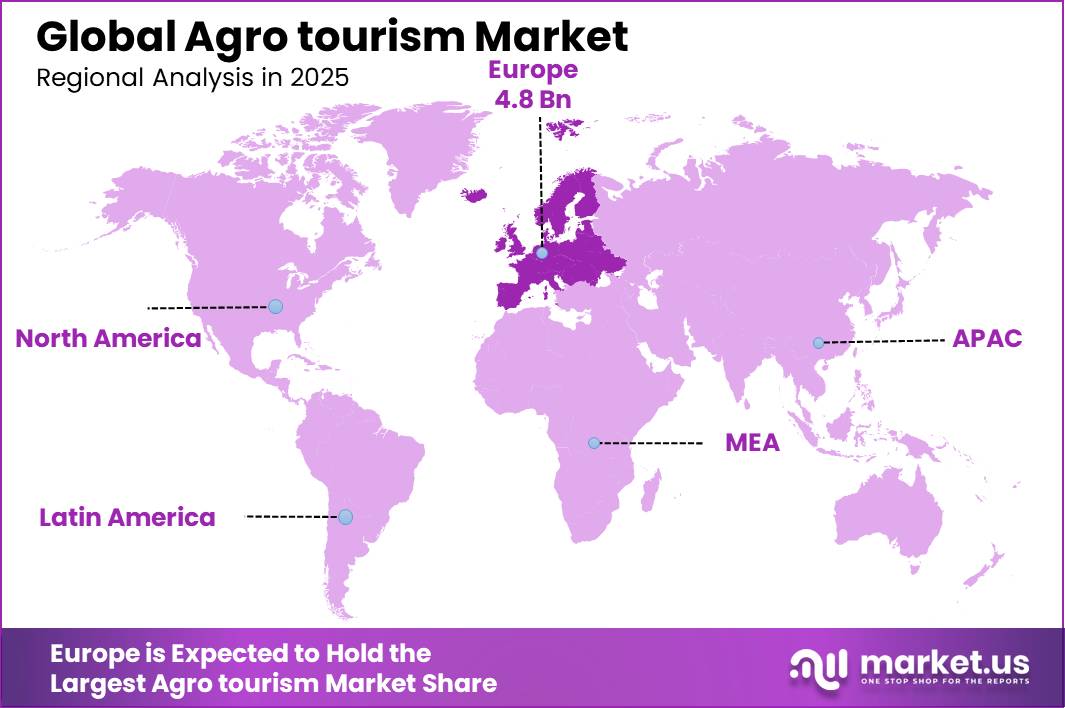

- Dominant region: Europe with 41.47% market share, valued at USD 4.821 Billion

Government-backed rural tourism programs are actively converting informal farm visits into structured revenue-generating destinations. By early 2025, the global rural tourism village network included 254 member villages, with more than 180 formally recognized and around 70 on an upgrade pathway. Member states may submit up to 8 candidate villages annually. This pipeline signals sustained public investment in agritourism infrastructure across multiple continents.

According to Tourism Research Australia, agritourism travelers in Australia generated A$20.3 billion in visitor spending during 2024. This figure confirms that agritourism has moved beyond supplemental farm income and into primary economic territory in mature markets. Investors and operators targeting Australia’s rural corridors face a market already generating institutional-scale returns.

Based on VisitScotland data, 67% of Scottish agritourism businesses offered self-catering accommodation in 2025, making it the most common agritourism activity in the country. This concentration signals that accommodation-led models drive the highest participation rates among farm operators. Suppliers who anchor their offering around lodging rather than day visits are capturing more sustained visitor spending per booking.

Activity Type Analysis

Farm Stays and Rural Lodging dominates with 34.80% due to strong repeat-visitor demand and accommodation revenue stacking.

In 2025, Farm Stays and Rural Lodging held a dominant market position in the By Activity Type segment of the Agritourism Market, with a 34.80% share. This segment anchors agritourism revenue because overnight visitors spend more per trip than day visitors. Operators who invest in lodging infrastructure convert single-visit guests into returning seasonal customers, creating more predictable income streams than crop sales alone.

Recreational and Adventure Activities claimed a 28.40% share, making it the second-largest activity segment. This segment draws younger demographics and groups seeking physical engagement with farm environments. Data from ISTAT shows that in 2024, Italy had 26,360 agritourism establishments, a 0.9% increase versus 2023, many of which have expanded recreational programming to diversify offerings beyond lodging.

Educational and Learning Tourism held a 22.60% share, capturing school-linked travel and structured farm curriculum programs. This sub-segment is increasingly tied to formal institutional relationships, with educational institutions booking seasonal visits as part of curriculum delivery. Operators in this segment benefit from group bookings that fill capacity during shoulder seasons when leisure travelers are absent.

Others accounted for the remaining 14.20% of the activity type segment. This category includes niche offerings such as harvest festivals, cooking workshops, and seasonal photography experiences. As per our research, Italy’s agritourism sector grew by 3.3% in economic value in 2024 compared to 2023, with specialty-category offerings contributing to that expansion. This signals room for product diversification within the Others sub-segment across European markets.

Traveler Type Analysis

Family Groups dominates with 34.60% due to multi-generational appeal and longer average booking windows.

In 2025, Family Groups held a dominant market position in the By Traveler Type segment of the Agritourism Market, with a 34.60% share. Families prioritize safe, supervised, and experience-rich environments for travel. Farm destinations offering animal interaction, harvest participation, and overnight lodging are well-positioned to capture repeat family bookings across multiple seasons.

Educational Institutions, Millennials and Young Adults, Corporate Groups, and Others collectively represent the remaining share of the traveler type segment. Educational Institutions drive structured group bookings tied to academic calendars, creating predictable off-peak demand. Millennials and Young Adults, by contrast, are driven by social media-amplified farm aesthetics and vineyard experiences, favoring shorter stays with high visual appeal.

Distribution Channel Analysis

Direct Bookings dominates with 74.07% due to operator control over pricing and visitor relationships.

In 2025, Direct Bookings held a dominant market position in the By Distribution Channel segment of the Agritourism Market, with a 74.1% share. Farm operators strongly prefer direct booking because it eliminates platform commission costs and allows them to manage visitor volume and experience quality. This concentration also means that operators with weak digital presence risk losing share to farm destinations running their own reservation systems.

Online Booking Platforms and Travel Agents collectively account for the remaining distribution share. Online platforms are gaining traction as real-time availability tools reduce booking friction for first-time agritourism visitors. Travel Agents serve corporate and educational group segments where itinerary complexity justifies intermediary involvement. These channels represent incremental growth vectors as agritourism scales beyond local word-of-mouth networks.

Key Market Segments

By Activity Type

- Farm Stays and Rural Lodging

- Educational and Learning Tourism

- Recreational and Adventure Activities

- Others

By Traveler Type

- Family Groups

- Educational Institutions

- Millennials and Young Adults

- Corporate Groups

- Others

By Distribution Channel

- Direct Bookings

- Online Booking Platforms

- Travel Agents

Market Dynamics

Market Opportunity Analysis - Underexploited segments and emerging regions offer entry points for operators and investors seeking first-mover advantage

The Others activity sub-segment, holding a 14.20% share, remains the least developed category within agritourism. Harvest festivals, cooking workshops, and seasonal photography experiences within this sub-segment generate visitor interest but lack standardized product development. Operators who formalize these offerings into bookable packages with defined pricing can capture incremental revenue with minimal capital investment.

Educational Institutions as a traveler type represent a structurally underexploited booking channel. School-linked farm visits fill shoulder-season capacity gaps that leisure travelers cannot fill. Farm operators who build long-term agreements with educational authorities secure predictable group bookings outside peak summer windows, reducing revenue volatility from seasonal dependence.

Latin America holds significant untapped agritourism potential relative to its agricultural asset base. Women-led digital village models and rural event monetization platforms carry medium-term CAGR upside of +1.7% and +1.8% respectively in this region. Operators who enter Latin American markets now, while formalization infrastructure is still developing, can establish distribution advantages before larger platform players arrive.

Middle East and Africa remain the least penetrated agritourism region despite possessing diverse agricultural heritage and conservation assets. Carbon and conservation tourism carry a long-term CAGR upside of +2.0% globally, with EU, Oceania, and North America identified as primary execution markets. This signals that MEA-based operators who develop credible conservation verification frameworks early can eventually attract high-value international sustainability travelers.

Technology and Innovation Landscape - Digital booking platforms and smart-farm demonstration tourism are reshaping how agritourism destinations attract and retain visitors

Online farm experience booking platforms integrating real-time availability and activity customization represent the most immediate technology shift in agritourism distribution. These platforms reduce booking friction for first-time visitors who lack personal referrals to farm destinations. Operators who integrate real-time inventory management tools into their direct booking systems protect market share against large platform intermediaries.

Smart-farm demonstration tourism is an emerging product category that showcases precision agriculture, drones, and automated farming systems to visitors. This positions technology itself as the agritourism experience rather than a background operational tool. Farm operators in advanced agricultural markets can differentiate their visitor offering by converting working precision-agriculture infrastructure into educational tourism assets without additional capital outlay.

Social media-driven destination marketing is functioning as a low-cost customer acquisition channel for agritourism operators. Harvest festivals and seasonal photo experiences generate organic content that reaches urban audiences who have no prior connection to farm destinations. Operators who design visually compelling seasonal experiences are effectively outsourcing marketing to their own guests, compressing customer acquisition costs relative to traditional travel advertising.

Glamping and luxury farm-stay concepts are replacing traditional day-visit models as the dominant agritourism product format. This shift upgrades the revenue-per-visitor metric by extending average booking duration and adding premium accommodation charges. Operators who invest in designed outdoor lodging rather than conventional farmhouse accommodation capture a higher-spending traveler segment that treats rural farm stays as luxury escapes rather than educational outings.

Drivers

Rural destination formalization is a major market driver because internationally recognized tourism frameworks are helping convert rural locations into structured, investable destinations. By early 2025, the global rural tourism village network included 254 member villages, with more than 180 formally recognized and around 70 on an upgrade pathway. Member states may submit up to 8 candidate villages annually, ensuring a continuous pipeline of new destinations.

These frameworks improve governance, infrastructure planning, health and safety standards, and local value-chain integration. Formal recognition strengthens destination branding and tourism storytelling, making rural attractions more marketable to international visitors. As a result, booking confidence rises, public-sector coordination improves, and route-to-market visibility strengthens, all of which support current agritourism revenue growth.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Farm income diversification push | +2.3% | North America, EU, LATAM, South Asia | Short term |

| Rural destination formalization | +1.8% | Europe, Asia, Africa, Latin America | Medium term |

| Direct-to-consumer traffic conversion | +1.9% | North America, EU peri-urban belts | Short term |

| Women-led rural enterprise uplift | +1.5% | Eastern Europe, South Asia, LATAM | Medium term |

| County-level tourism spread | +1.4% | North America core, spillover to EU rural regions | Short term |

| Policy-backed rural visibility | +1.6% | Global, strongest in UN Tourism member states | Medium term |

Restraints

Safety and liability risk exposure remains a significant restraint because agritourism activities take place in working farm environments containing machinery, livestock, agricultural chemicals, and uneven terrain. Operators must implement premises-liability measures including safety signage, visitor waivers, supervised access to hazardous zones, and structural assessments before opening to guests. Failure to manage these risks leads to accidents, legal claims, and higher insurance costs.

The liability burden discourages some farms from entering agritourism entirely. Insurers and lenders apply conservative risk assessments, limiting expansion plans and new investment. This restricts both the number of farms participating and the breadth of visitor experiences offered, compressing addressable supply even as traveler demand continues to expand.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict village eligibility limits | -1.4% | UN Tourism member states | Long term |

| Population cap on scalable sites | -1.2% | Europe, Asia, Latin America rural belts | Long term |

| Limited nomination throughput | -1.0% | UN Tourism initiative participants | Medium term |

| Safety and liability risk exposure | -1.3% | North America, EU, APAC corridors | Medium term |

| Infrastructure investment gap | -1.6% | South Asia, Africa, Latin America | Long term |

| Climate and hazard vulnerability | -1.1% | Global rural destinations | Long term |

Challenges

Governance bottlenecks remain a major long-term challenge because successful agritourism development depends on destination-level coordination rather than individual farm efforts. Rural tourism recognition programs require applications submitted through national tourism administrations, with a limit of 8 village nominations per country per edition. Eligibility criteria include a maximum population threshold of 15,000 inhabitants and completion of detailed application dossiers.

These requirements make destination development heavily dependent on public-sector facilitation, documentation quality, and multi-stakeholder collaboration. Rural areas may hold strong agricultural and tourism assets yet still struggle to scale due to weak coordination among village committees, tourism authorities, and local operators. Delays in aligning standards, branding strategies, and investment priorities slow development and reduce destination competitiveness.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Fragmented farm readiness | -1.4% | North America, EU, South Asia, LATAM | Medium term |

| Weak digital capability | -1.3% | South Asia, Africa, Eastern Europe, LATAM | Medium term |

| Informal experience design | -1.1% | Global | Medium term |

| Governance bottleneck at village level | -1.0% | UN Tourism member states, emerging rural regions | Long term |

| Thin year-round demand utilization | -1.2% | Temperate rural markets in Europe and North America | Medium term |

| Data classification gaps | -0.9% | Global | Long term |

Opportunities

Conservation-linked agritourism represents a future opportunity because most agritourism businesses still focus on scenery, food, and farm experiences rather than measurable environmental outcomes. Farm-diversification frameworks increasingly encourage revenue streams combining agriculture, tourism, and nature conservation. This creates openings for biodiversity walks, regenerative farming experiences, soil-health education stays, habitat-restoration activities, and carbon-linked visitor programs.

Such offerings allow guests to contribute directly to environmental improvement while participating in tourism experiences. The model can generate higher-value visitor engagement and differentiate destinations beyond traditional farm tourism. Growth will depend on credible verification systems, conservation partnerships, and transparent measurement of environmental outcomes, making this an emerging opportunity rather than an established market driver.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Farm stay yield stacking | +2.2% | Europe, North America, Oceania | Short term |

| Direct-to-consumer agrifood bundling | +1.9% | North America, EU, APAC peri-urban | Short term |

| Women-led digital village models | +1.7% | South Asia, Eastern Europe, LATAM | Medium term |

| Rural event monetization platforms | +1.8% | North America, EU, India, LATAM | Medium term |

| Best-village export replication | +1.5% | Asia, Africa, Mediterranean Europe | Medium term |

| Carbon and conservation tourism | +2.0% | EU, Oceania, North America | Long term |

Regional Analysis

Europe Dominates the Agritourism Market with a Market Share of 41.47%, Valued at USD 4.821 Billion

Europe holds the largest regional share in the Agritourism Market, supported by a dense network of formal rural tourism programs, government-backed farm diversification incentives, and mature visitor infrastructure. The region benefits from internationally recognized rural destination frameworks and strong intra-European travel behavior. Italy, France, and Scotland each operate structured agritourism certification programs that convert farm assets into commercially viable visitor experiences.

North America represents a high-value agritourism corridor anchored by direct-booking farm operators and winery tourism across the United States and Canada. The county-level tourism spread model drives short-break and weekend agritourism demand, particularly across peri-urban farm belts. Women-led rural enterprises and farm-stay yield stacking are emerging as structural growth factors with short-term impact on regional revenue.

Asia Pacific is an expanding agritourism region with Australia serving as the most mature sub-market. Figures from Tourism Research Australia show that Victoria and New South Wales each recorded more than 5 million agritourism trips in 2024, together accounting for 59% of all agritourism trips in Australia. This concentration signals that two states alone are driving the bulk of national agritourism output, creating scalable investment targets for accommodation and experience operators.

Latin America holds growth potential through women-led digital village models and rural event monetization platforms, particularly in Brazil and Mexico. The region’s agricultural diversity and cultural heritage support experiential product development. However, infrastructure investment gaps and weak digital capability remain constraints that slow conversion of agricultural assets into structured visitor destinations.

Middle East and Africa represent an early-stage agritourism opportunity with strong untapped agricultural and natural heritage assets. Governance bottlenecks and limited tourism administration capacity restrict the pace of destination formalization. Conservation-linked agritourism and carbon farming experiences are positioned as long-term growth vectors for this region, contingent on credible verification frameworks and international partnership support.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Expedia Group positions agritourism within its broader alternative accommodation strategy, using platform scale to aggregate farm-based listings that individual operators cannot market alone. This distribution reach is a structural advantage over niche booking tools. However, platform commission structures may deter direct-booking-dominant farm operators from listing, limiting inventory depth in rural corridors.

Booking Holdings, through Booking.com, competes on search visibility and price transparency across rural accommodation categories. Its algorithm-driven ranking system favors high-review-volume properties, which disadvantages smaller farm operators with limited guest throughput. In 2025, VisitScotland reported that agritourism businesses welcomed 2.5 million visitors and supported approximately 8,000 full-time equivalent jobs, underscoring the scale that platforms must serve to remain relevant to rural tourism ecosystems.

Key Players

- Expedia Group

- Booking Holdings (Booking.com)

- Airbnb Inc.

- Blackberry Farm LLC

- Farm to Farm Tours

- Field Farm Tours Limited

- Harvest Travel International

- Agrilys Voyages

- Bay Farm Tours

- Agritours Canada

- Domiruth Peru Travel

- Greenmount Travel

- Agricultural Tour Operators International (ATOI)

- Farm Stay US

- Agri Tourism Development Corporation (ATDC)

Recent Developments

- November 2025 – maeva (Pierre and Vacances-Center Parcs Group) acquired Parcel Tiny House, an agritourism accommodation operator with approximately 40 tiny houses located across 30 working farms in France, expanding its farm-based tourism portfolio and sustainable rural travel offerings.

- January 2025 – Harvest Hosts introduced a redesigned membership platform and expanded benefits under its All Access Membership, strengthening direct booking and visitor access to farm-based tourism destinations across North America.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 11.63 Billion |

| Forecast Revenue (2035) | USD 35.97 Billion |

| CAGR (2026-2035) | 13.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Activity Type (Farm Stays and Rural Lodging, Educational and Learning Tourism, Recreational and Adventure Activities, Others); By Traveler Type (Family Groups, Educational Institutions, Millennials and Young Adults, Corporate Groups, Others); By Distribution Channel (Direct Bookings, Online Booking Platforms, Travel Agents) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Expedia Group, Booking Holdings (Booking.com), Airbnb Inc., Blackberry Farm LLC, Farm to Farm Tours, Field Farm Tours Limited, Harvest Travel International, Agrilys Voyages, Bay Farm Tours, Agritours Canada, Domiruth Peru Travel, Greenmount Travel, Agricultural Tour Operators International (ATOI), Farm Stay US, Agri Tourism Development Corporation (ATDC) |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |