Quick Navigation

- Report Overview

- Top Market Takeaways

- Drivers Impact Analysis

- Restraints Impact Analysis

- By Component Analysis

- By Deployment Analysis

- By Organization Size Analysis

- By Industry Vertical Analysis

- Investor Type Impact Analysis

- Technology Enablement Analysis

- Key Challenges

- Emerging Trends

- Growth Factors

- Key Market Segments

- Regional Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

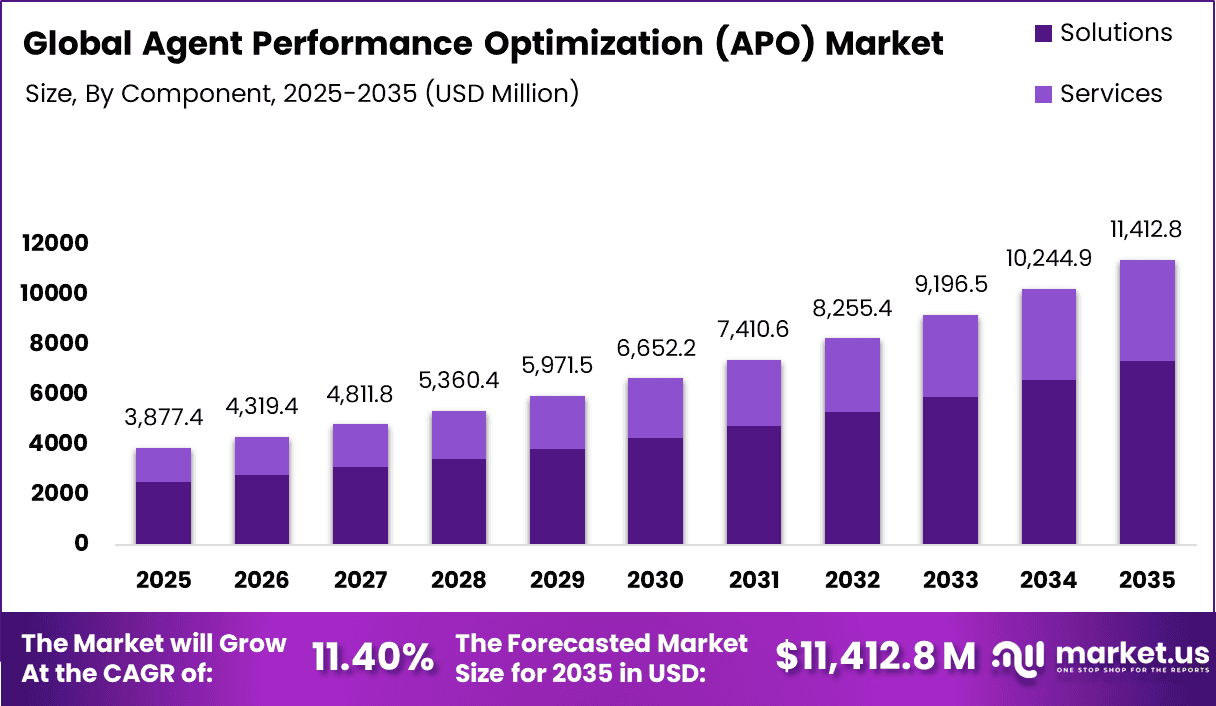

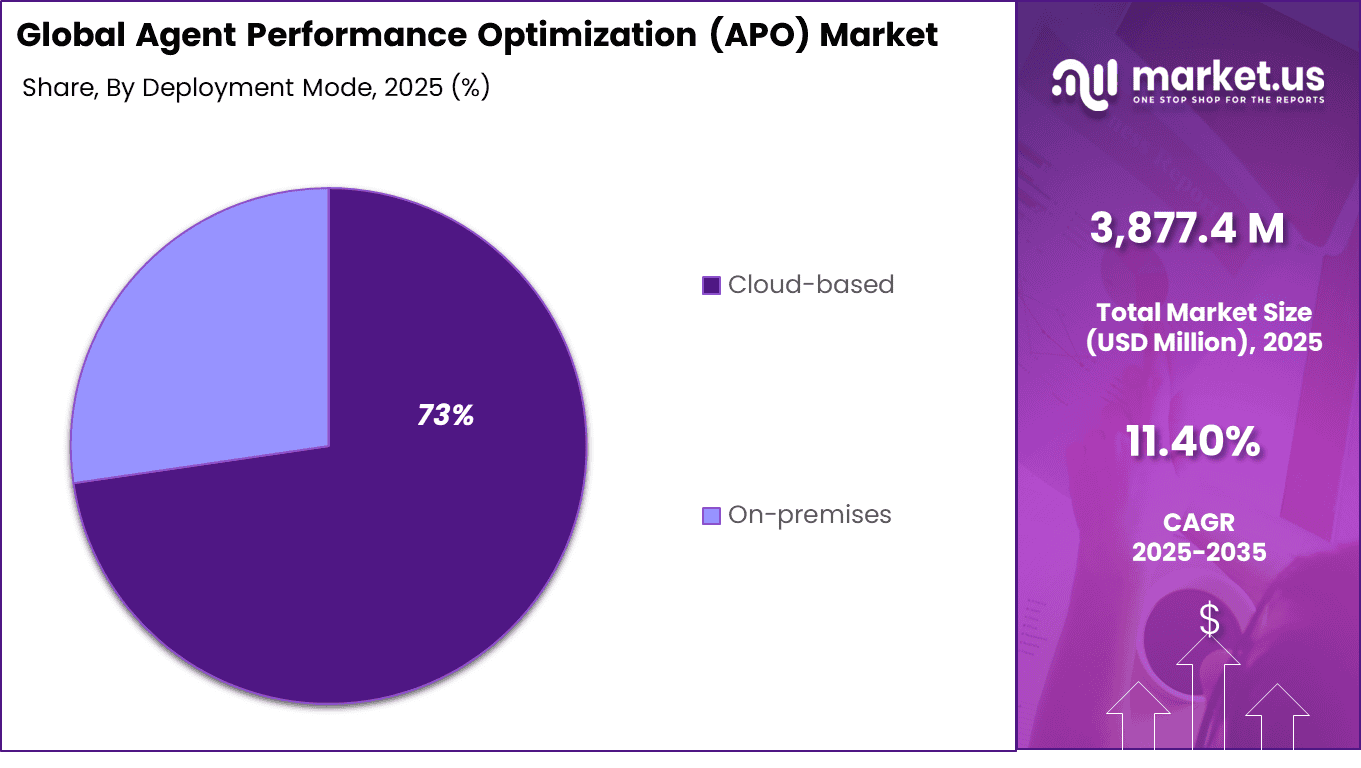

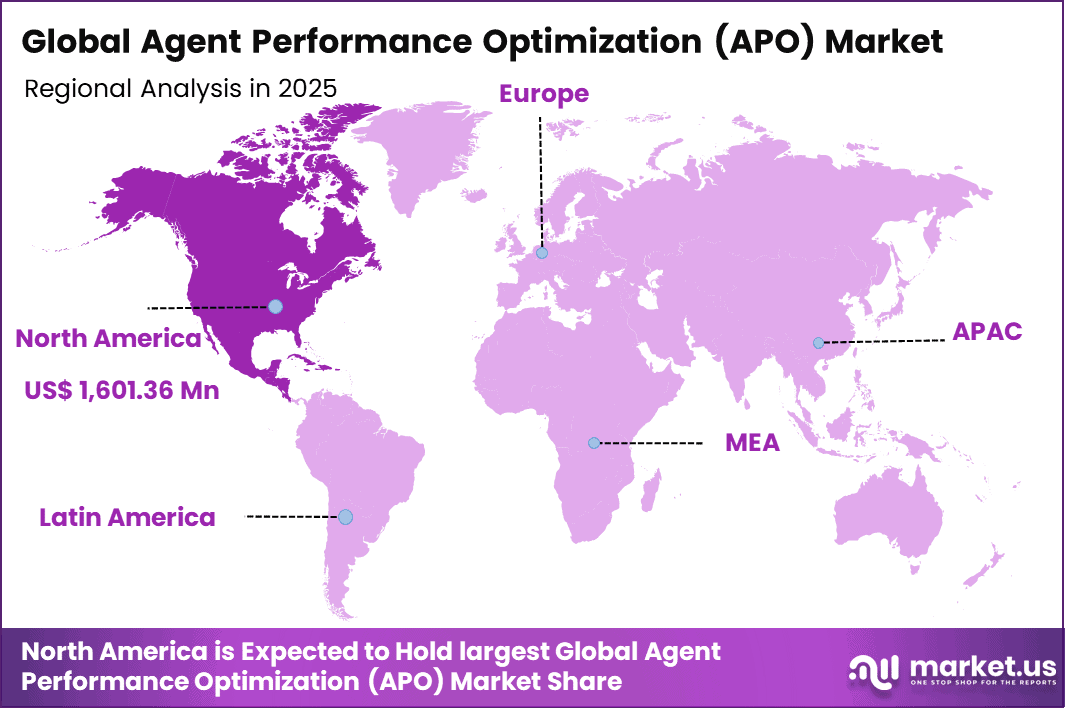

The Global Agent Performance Optimization (APO) Market generated USD 3,877.4 million in 2025 and is predicted to register growth from USD 4,319.4 million in 2026 to about USD 11,412.8 million by 2035, recording a CAGR of 11.40% throughout the forecast span. In 2025, North America held a dominant market position, capturing more than a 41.3% share, holding USD 1,601.36 Million revenue.

Agent performance optimization solutions are used to improve the productivity, efficiency, and service quality of customer facing agents across contact centers, sales teams, and support operations. These platforms combine workforce analytics, coaching tools, quality monitoring, and performance tracking to help organizations manage teams more effectively.

As customer interactions move across voice, chat, email, and digital channels, businesses need better visibility into agent performance and customer outcomes. This is making optimization platforms an important part of modern service operations.

One of the main driving factors is the rising expectation for faster and higher quality customer service. Organizations are under pressure to reduce response times, improve first contact resolution, and maintain consistent service standards.

In addition, remote and hybrid work models have increased the need for digital tools that can monitor productivity and support coaching from any location. The growing use of data analytics is also helping companies identify skill gaps, training needs, and workflow issues more accurately. At the same time, businesses are focusing on employee engagement and retention, which supports investment in tools that provide fair measurement and clear development paths.

Demand for agent performance optimization solutions is increasing as organizations seek measurable improvements in service operations. There is a strong preference for platforms that offer real time dashboards, automated scorecards, and personalized coaching recommendations. Companies are also looking for systems that can integrate with customer relationship management, workforce management, and communication tools.

The demand is particularly strong in industries with high customer interaction volumes such as banking, telecom, healthcare, retail, and business services. As service quality becomes a stronger competitive factor, the need for intelligent and scalable agent optimization solutions is expected to grow steadily.

Top Market Takeaways

- Solutions command 64.3%, delivering real-time coaching, speech analytics, and predictive performance metrics to boost agent productivity and first-call resolution rates.

- Cloud-based deployment dominates at 72.7%, enabling scalable AI integration, multi-channel monitoring, and remote workforce management across distributed operations.

- Large enterprises hold 70.1% by organization size, leveraging enterprise-grade platforms for compliance tracking, gamification, and ROI analytics in high-volume environments.

- BFSI vertical captures 26.5%, powering fraud detection, customer onboarding, and collections optimization through sentiment analysis and automated quality assurance.

- North America drives 41.3% global value, with U.S. market at USD 1,433.5 million and 9.7% CAGR, fueled by regulatory pressures and omnichannel banking evolution.

Drivers Impact Analysis

| Key Driver | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| Rising focus on contact center productivity and efficiency | +3.3% | North America, Europe, Asia Pacific | Short to medium term | Businesses seek higher agent output |

| Growing demand for improved customer experience management | +3.0% | Global | Medium term | Better service drives APO adoption |

| Increasing use of remote and hybrid customer service teams | +2.7% | Global | Medium to long term | Distributed teams need performance tools |

| Expansion of BPO and outsourcing operations | +2.5% | Asia Pacific, Latin America, North America | Medium term | Outsourcing growth supports demand |

| Need for workforce analytics and KPI monitoring | +2.2% | Global | Medium to long term | Data insights improve agent performance |

Restraints Impact Analysis

| Key Restraint | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| High implementation and integration costs | -2.6% | Emerging markets | Short to medium term | Costs slow adoption |

| Resistance to employee monitoring systems | -2.3% | North America, Europe | Medium term | Privacy concerns create pushback |

| Complexity in integrating with legacy CRM systems | -2.0% | Global | Medium term | Legacy systems delay deployment |

| Limited awareness among small enterprises | -1.7% | Developing regions | Medium term | Smaller firms adopt slowly |

| Data privacy and compliance requirements | -1.5% | Global | Medium to long term | Regulations affect analytics usage |

By Component Analysis

The solutions segment accounted for 64.3% of the market share, reflecting its central role in improving workforce productivity, monitoring agent efficiency, and enhancing customer interaction outcomes. This dominance is supported by the growing demand for platforms that provide analytics, workflow automation, coaching tools, and performance dashboards. Organizations are increasingly adopting dedicated solutions to optimize agent operations and improve service quality.

Another factor driving this segment is the need for measurable performance insights across contact centers and service teams. APO solutions help businesses identify skill gaps, track key metrics, and improve resource utilization. Their ability to integrate with customer service systems and communication platforms further strengthens adoption across industries.

By Deployment Analysis

The cloud-based segment held 73% share, driven by the increasing preference for scalable and flexible deployment models. Cloud platforms allow organizations to access performance tools remotely, deploy updates quickly, and manage multiple teams from centralized environments. This approach reduces infrastructure burden and supports faster implementation.

In addition, cloud-based systems are well suited for hybrid and remote work models where agents operate from different locations. Businesses benefit from real-time visibility, easier collaboration, and lower maintenance requirements. These advantages have significantly increased the adoption of cloud deployment in the APO market.

By Organization Size Analysis

The large enterprises segment captured 70.1% of the market, reflecting their strong need to manage extensive customer service operations and distributed agent teams. These organizations handle high interaction volumes and require advanced optimization tools to maintain service consistency, productivity, and compliance standards. APO platforms help streamline operations at scale.

Moreover, large enterprises have greater capacity to invest in advanced analytics, automation, and workforce management technologies. They focus on improving customer experience while controlling operational costs. This has strengthened demand for APO solutions among large organizations across multiple sectors.

By Industry Vertical Analysis

The BFSI segment accounted for 26.5% of the market share, driven by the need for efficient customer support, regulatory compliance, and service accuracy in banking and financial institutions. These organizations manage large volumes of customer inquiries related to accounts, payments, loans, and security, making agent performance highly important. APO tools help improve response quality and operational efficiency.

Furthermore, the increasing use of digital banking channels has raised customer expectations for fast and reliable support. BFSI companies are adopting optimization platforms to monitor agent productivity, reduce handling time, and improve satisfaction levels. This has reinforced the importance of APO solutions within the BFSI sector.

Investor Type Impact Analysis

| Investor Type | Growth Sensitivity | Risk Exposure | Geographic Focus | Investment Outlook |

|---|---|---|---|---|

| Venture capital firms | High | High | US, Europe | Investing in workforce analytics startups |

| Private equity firms | Moderate to high | Moderate | North America and Europe | Scaling enterprise software providers |

| Corporate investors | High | Moderate | Global | Strategic investments in CX technologies |

| Institutional investors | Moderate | Low to moderate | Developed markets | Prefer stable SaaS and enterprise firms |

| Government and public funding bodies | Low to moderate | Low | Global | Supporting digital workforce initiatives |

Technology Enablement Analysis

| Technology | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| AI-driven agent coaching and recommendations | +3.5% | US, Europe | Medium to long term | Improves real-time performance |

| Cloud-based APO platforms | +3.1% | Global | Short to medium term | Enables scalable deployment |

| Speech analytics and sentiment analysis | +2.8% | Global | Medium term | Enhances customer interaction insights |

| Integration with CRM and workforce management tools | +2.5% | Global | Medium to long term | Creates unified operations view |

| Predictive analytics for staffing and productivity | +2.2% | Developed markets | Medium term | Supports smarter resource planning |

Key Challenges

- High implementation cost makes adoption difficult for small businesses.

- Integration challenges with existing CRM and contact center systems.

- Poor data quality reduces the accuracy of performance insights.

- Resistance from employees who feel closely monitored.

- Need for skilled staff to manage analytics and optimization tools.

- Difficulty in measuring performance across different channels.

- Data privacy concerns related to employee and customer information.

- Frequent updates needed to match changing business needs.

- Dependence on stable internet and system performance.

- Limited customization in some software solutions.

Emerging Trends

The agent performance optimization market is evolving toward more intelligent and employee focused solutions that improve productivity, service quality, and operational efficiency. One of the key emerging trends is the use of AI driven coaching tools that analyze customer interactions in real time and provide immediate guidance to agents during calls, chats, or emails. This is helping improve response quality and consistency.

Another important trend is the integration of performance management, workforce engagement, and analytics into unified platforms, allowing managers to monitor outcomes from a single dashboard. There is also growing adoption of sentiment analysis tools that evaluate customer tone and agent behavior to identify training needs and service gaps. In addition, gamification features such as rewards, rankings, and achievement tracking are being used to increase motivation and engagement among frontline teams. Cloud based deployment is also expanding, making APO solutions easier to scale across remote and hybrid workforces.

Growth Factors

The growth of this market is driven by the rising need to improve customer experience and agent productivity across service driven industries. Organizations are recognizing that agent performance directly affects customer satisfaction, retention, and brand perception, which is encouraging investment in optimization tools. The expansion of contact centers and digital support channels is also increasing demand for platforms that can manage performance across voice, chat, and messaging environments.

Another major factor is the shift toward remote and hybrid work models, where managers need better visibility into agent activity and outcomes. Businesses are also focusing on reducing training time, improving first contact resolution, and lowering employee turnover, which further supports adoption. Additionally, the growing use of data driven management practices is encouraging companies to deploy APO solutions that provide measurable insights and continuous improvement opportunities.

Key Market Segments

By Component

- Solutions

- Quality & Interaction Analytics

- Workforce Engagement Management

- Real-Time Guidance & Coaching

- Performance Management

- Others

- Services

- Implementation & Integration

- Consulting & Advisory

- Managed Services

By Deployment

- Cloud-based

- On-Premises

By Organization Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By Industry Vertical

- BFSI

- IT & Telecom

- Retail & E-commerce

- Healthcare & Life Sciences

- Travel & Hospitality

- Others

Regional Analysis

North America accounted for 41.3% of the Agent Performance Optimization (APO) market, supported by strong adoption of workforce analytics and customer experience management solutions across enterprises. The region has a mature contact center ecosystem where organizations are increasingly focused on improving agent productivity, service quality, and operational efficiency.

APO platforms are widely used to monitor performance metrics, optimize scheduling, enhance coaching programs, and improve customer interactions. In addition, growing demand for data-driven decision making and automation in customer service operations is strengthening market growth across industries such as banking, telecom, healthcare, and retail.

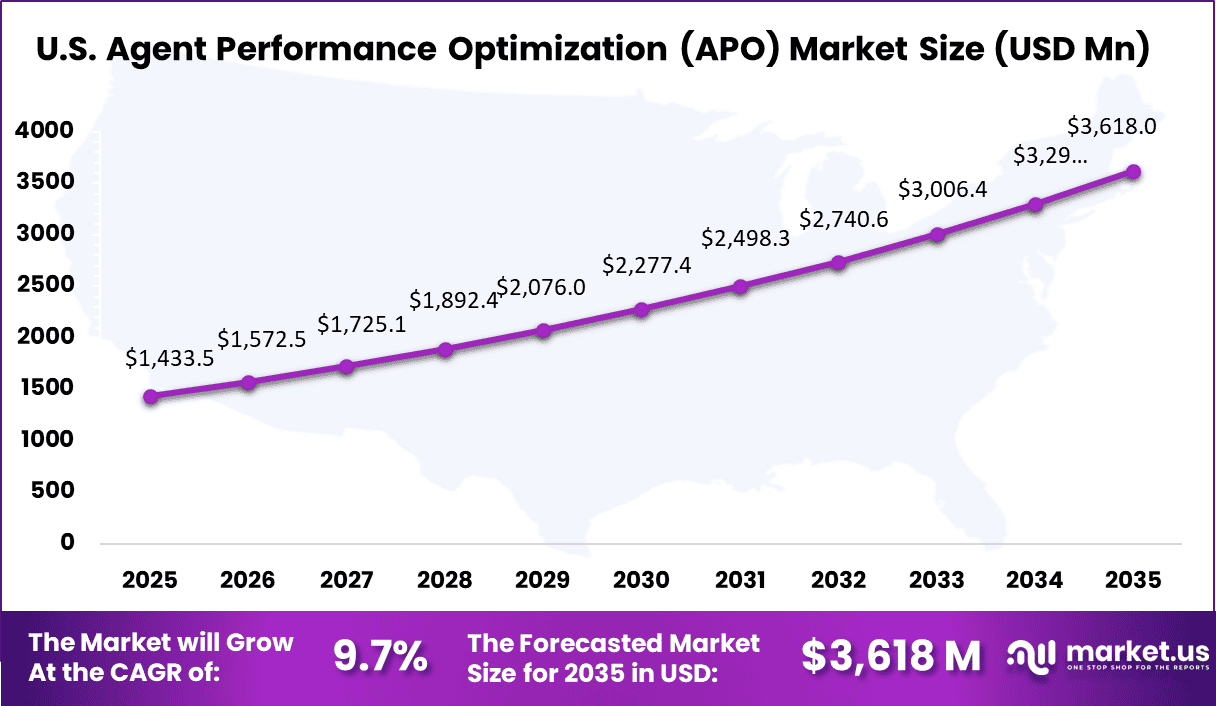

The U.S. market reached USD 1,433.5 Million and is projected to grow at a CAGR of 9.7%, driven by rising investments in modern contact center technologies and employee performance tools. Businesses are adopting APO solutions to improve first-call resolution, reduce handling time, and increase customer satisfaction.

The shift toward hybrid work models has also increased the need for cloud-based monitoring, training, and engagement platforms that support distributed agent teams. Continuous focus on service excellence and efficient workforce management is expected to support steady growth in the US market over the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

The competitive landscape of the Agent Performance Optimization (APO) Market is led by established contact center technology providers and workforce management specialists. Companies such as NICE Ltd, Genesys Cloud Services, Inc., Verint Systems Inc., Cisco Systems, Inc., and Avaya Holdings Corp. focus on comprehensive APO solutions that combine workforce optimization, quality monitoring, analytics, and performance management.

These players serve large enterprises with scalable cloud and on-premise platforms, helping organizations improve agent productivity, customer experience, and operational efficiency. Their strong global presence and broad product portfolios support their leading position in the market.

At the same time, companies such as Aspect, Calabrio Inc., Five9 Inc., Teleopti AB, ZOOM International, InVision AG, Upstream Works Software, Envision Telephony, CallMiner Inc., CallFinder, and HigherGround, Inc. compete by offering specialized solutions in workforce scheduling, speech analytics, compliance recording, and coaching tools.

These players focus on flexibility, user-friendly dashboards, and faster deployment for mid-sized and large contact centers. Competition in this market is driven by AI-based analytics, cloud adoption, and the ability to deliver measurable improvements in agent performance and customer service outcomes.

Top Key Players in the Market

- NICE Ltd

- Genesys Cloud Services, Inc.

- Verint Systems Inc.

- Aspect

- Calabrio Inc.

- Five9 Inc.

- Teleopti AB

- ZOOM International

- InVision AG

- Upstream Works Software

- Envision Telephony

- CallMiner Inc.

- CallFinder

- HigherGround, Inc.

- Cisco Systems, Inc.

- Avaya Holdings Corp.

- Others

Future Outlook

The future outlook for the Agent Performance Optimization (APO) Market looks strong as businesses continue to focus on improving customer service efficiency and workforce productivity. The market is expected to grow with increasing demand for tools that monitor agent performance, analyze customer interactions, and improve service quality. Companies are anticipated to adopt AI-driven solutions for coaching, scheduling, and real-time guidance to support better outcomes. In the coming years, integration with cloud contact centers, advanced analytics, and automation is expected to make APO platforms more effective, helping organizations improve customer satisfaction and operational performance.

Recent Developments

- April, 2026 – Genesys Cloud CX releases telephony permissions and agent ownership for callbacks. Predictive Engagement scores interactions live while Perform handles WFM across 10K agents seamlessly. Cloud CCaaS leader.

- March, 2026 – Verint Open Platform enhances Da Vinci AI with model-agnostic bots. Speech analytics processes 1M hours/day while WFM depth scores 7.8/10 on G2. Open telephony architecture.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3,877.4 Million |

| Forecast Revenue (2035) | USD 11,412.8 Million |

| CAGR(2025-2035) | 11.40% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2024 |

| Forecast Period | 2025-2035 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Solutions (Quality & Interaction Analytics, Workforce Engagement Management, Others), Services (Implementation & Integration, Consulting & Advisory)), By Deployment (Cloud-based, On-Premises), By Organization Size (Large Enterprises, Small & Medium Enterprises (SMEs)), Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | NICE Ltd, Genesys Cloud Services, Inc., Verint Systems Inc., Aspect, Calabrio Inc., Five9 Inc., Teleopti AB, ZOOM International, InVision AG, Upstream Works Software, Envision Telephony, CallMiner Inc., CallFinder, HigherGround, Inc., Cisco Systems, Inc., Avaya Holdings Corp., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Market")