Quick Navigation

Report Overview

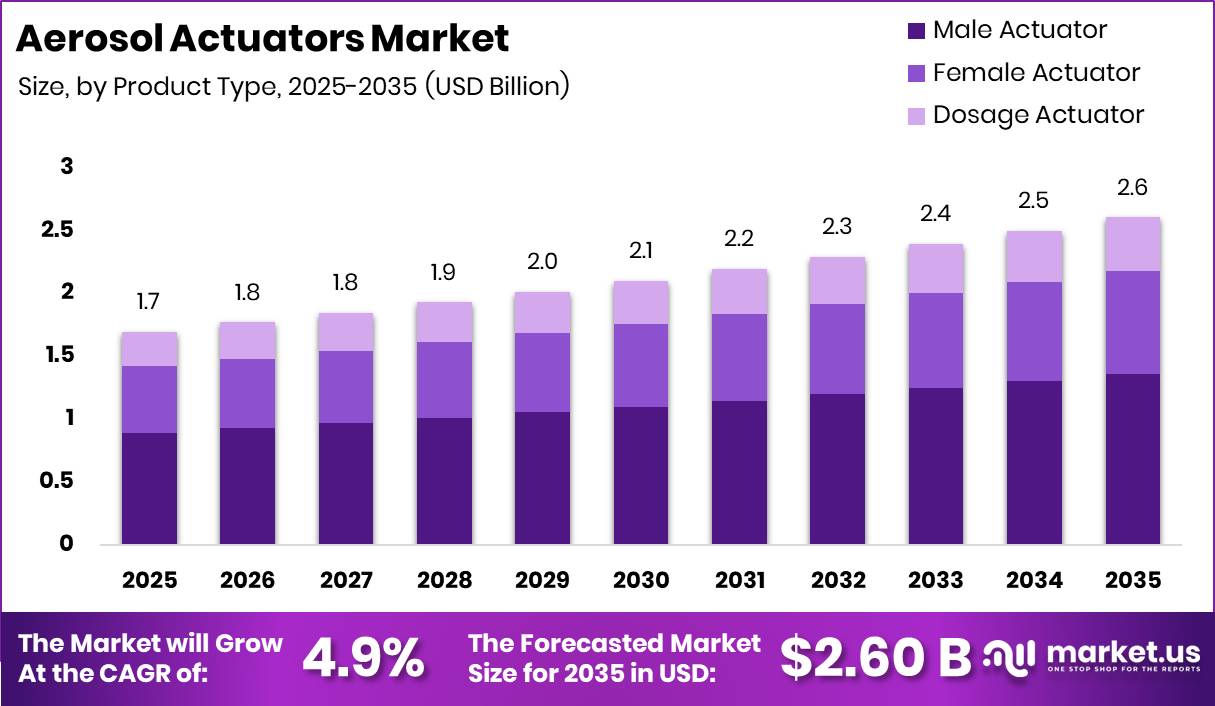

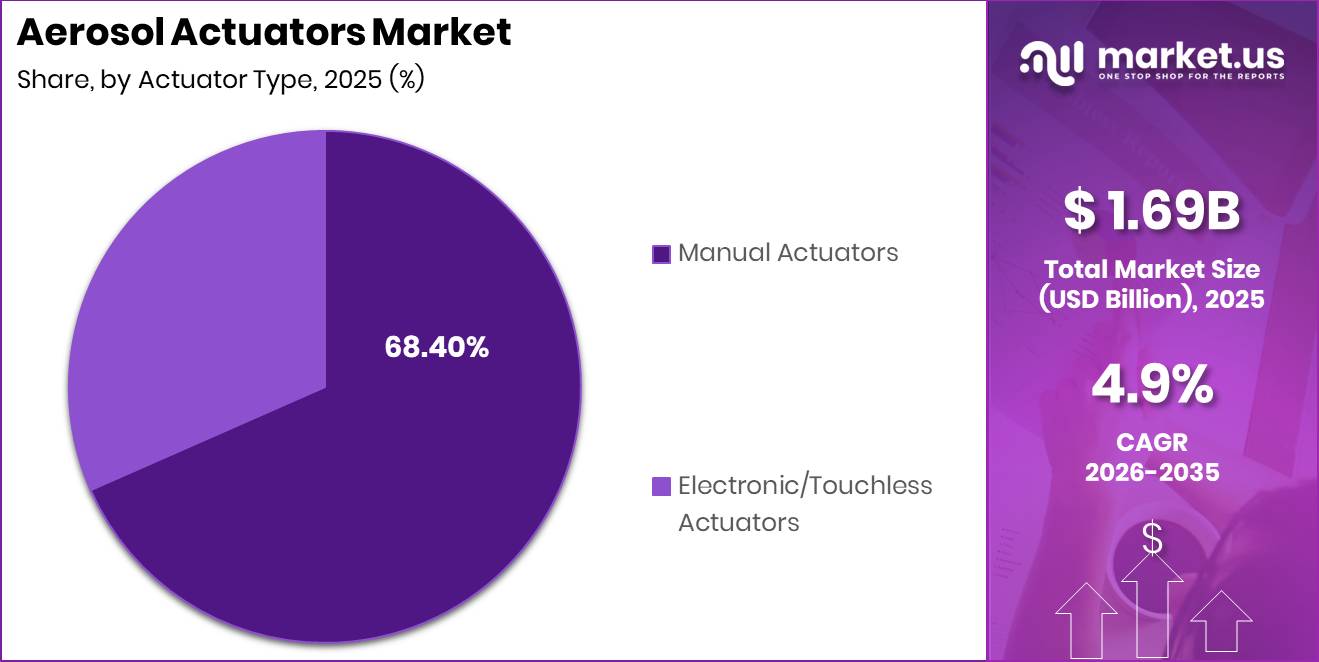

Global Aerosol Actuators Market size is expected to be worth around USD 2.60 Billion by 2035 from USD 1.70 Billion in 2025, growing at a CAGR of 4.9% during the forecast period 2026 to 2035.

Aerosol actuators are the dispensing components mounted on pressurized aerosol containers that control spray direction, droplet size, and dose release. The market spans manual and electronic actuator formats across personal care, household, pharmaceutical, automotive, food, and industrial end-use sectors. Products are segmented by product type, actuator mechanism, material, application, and sales channel.

Key Takeaways

- Market value in 2025 stands at USD 1.70 Billion, forecast to reach USD 2.60 Billion by 2035 at a CAGR of 4.9%.

- Male Actuator dominates the By Product Type segment with a 52.30% share.

- Manual Actuators lead the By Actuator Type segment with a 68.40% share.

- Plastics (PP, PE) dominate the By Material segment with a 71.20% share.

- Personal Care and Cosmetics leads the By Application segment with a 35.70% share.

- Direct Supply to Brand Owners and Fillers dominates By Sales Channel with a 73.50% share.

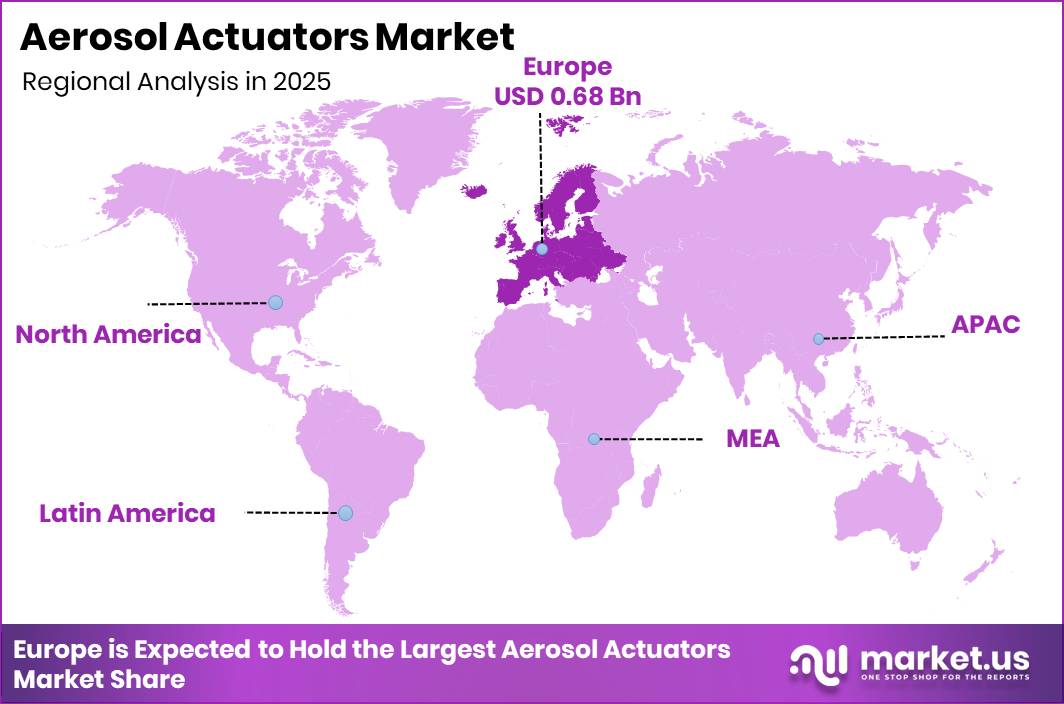

- Europe is the dominant region with a 40.57% market share, valued at USD 0.68 Billion.

Government mandates around packaging recyclability and propellant phase-down are reshaping actuator design requirements across all major markets. The EU Packaging and Packaging Waste Regulation and UK circular economy commitments are pushing brands toward mono-material and recyclable actuator architectures. Aluminium accounted for 67% of UK aerosol cans in 2025, while tinplate represented 33%, directly influencing actuator compatibility and interface design standards across the supply chain.

European aerosol production reached 5.2 billion units in 2024, rising 4.2% versus 2023. This volume scale translates into direct procurement demand for billions of actuator-valve assemblies annually. More than 300 aerosol filling companies operated across 17 European countries in 2024, creating a fragmented but large installed buyer base for actuator suppliers seeking multi-country distribution agreements.

More than 300 million salbutamol metered-dose inhalers are sold globally every year. This volume creates a durable, specification-driven demand channel for precision pharmaceutical actuators. As a result, manufacturers that secure regulatory-cleared actuator designs for inhaler applications access a sticky revenue stream with high switching costs and extended qualification cycles that protect margins.

Type Analysis

Male Actuator dominates with 52.30% due to universal compatibility with standard aerosol valve stems.

In 2025, Male Actuator held a dominant market position in the By Product Type segment of the Aerosol Actuators Market, with a 52.30% share. Male actuators press directly onto valve stems and work across virtually every aerosol container format. Their design simplicity lowers tooling costs and accelerates qualification timelines. Personal care aerosols represented 75% of the UK aerosol market in 2024, and the vast majority of those products use male actuator formats, confirming the segment’s structural depth.

Female Actuator holds a 31.40% share, serving applications that require enclosed valve stem connections for tamper resistance or controlled directional spray. These formats appear most frequently in pharmaceutical and premium personal care formats where spray precision and child-resistance features command higher per-unit prices. UK antiperspirant aerosol sales increased by 5% in 2024, supporting continued volume in female actuator-compatible personal care SKUs.

Dosage Actuator accounts for 16.30% of the market, serving metered-dose inhaler and regulated pharmaceutical spray applications. These components require tighter dimensional tolerances and validated dose repeatability compared to cosmetic or household formats. UK deodorant aerosol sales increased by 2.9% in 2024, and parallel growth in pharmaceutical aerosol volumes reinforces dosage actuator procurement across regulated supply chains.

Actuator Type Analysis

Manual Actuators dominate with 68.40% due to lower cost and broad cross-application compatibility.

In 2025, Manual Actuators held a dominant market position in the By Actuator Type segment of the Aerosol Actuators Market, with a 68.40% share. Manual actuators remain the default format across household, personal care, and industrial aerosol categories because they require no power source, no pairing, and no electronics qualification. Personal care products represented 56.4% of all aerosol fillings in Europe in 2023, and nearly all of those fillings use manual actuator systems, confirming the segment’s volume leadership.

Electronic and Touchless Actuators hold a 31.60% share and address hygiene-sensitive environments such as hospitals, food service facilities, and high-traffic public spaces. These units eliminate contact-based actuation and enable dose programming. In April 2025, LINDAL Group launched FlipStraw™, a dual-spray actuator combining precision and broad-area spraying in a single manual unit, demonstrating that innovation is also advancing within manual formats rather than shifting entirely toward electronic systems.

Material Analysis

Plastics (PP, PE) dominate with 71.20% due to low cost, moldability, and chemical resistance.

In 2025, Plastics (PP, PE) held a dominant market position in the By Material segment of the Aerosol Actuators Market, with a 71.20% share. Polypropylene and polyethylene offer the processing consistency and chemical resistance required across the widest range of aerosol formulations. Household aerosol products represented 19.4% of total European aerosol fillings in 2023, and the cleaning and disinfectant formats within that segment depend overwhelmingly on plastic actuator components for chemical compatibility and cost control.

Application Analysis

Personal Care and Cosmetics dominates with 35.70% due to high-frequency consumer use and SKU proliferation.

In 2025, Personal Care and Cosmetics held a dominant market position in the By Application segment of the Aerosol Actuators Market, with a 35.70% share. Consumer spending on grooming and skincare aerosols sustains continuous actuator procurement cycles across deodorants, hair sprays, and suncare formats. UK tanning and suncare aerosol products recorded 22.5% growth in 2024, one of the fastest-expanding personal care aerosol sub-categories, pulling specialized spray actuator demand with it.

Household and Institutional Cleaning represents a structurally stable application segment anchored by surface cleaners, air fresheners, and pest control aerosols. UK starch and fabric spray aerosol fillings rose by 22% in 2025, making it one of the fastest-growing household aerosol categories and generating direct demand for specialized spray actuators. Air freshener aerosol fillings in the UK increased by 0.3% in 2025, signaling a category stabilization after previous declines.

Automotive and Industrial Maintenance covers lubricants, coatings, adhesives, and technical spray formats that require directional actuators with chemical resistance to solvents and propellants. UK insecticide aerosol fillings increased by nearly 10% in 2025, supporting growth in directional and high-dispersion actuator formats used in pest control. Paint and lacquer aerosol fillings in the UK declined by 16% in 2025, creating a volume headwind for actuators deployed in the coatings sub-segment of industrial maintenance.

Sales Channel Analysis

Direct Supply to Brand Owners and Fillers dominates with 73.50% due to volume scale and specification control.

In 2025, Direct Supply to Brand Owners and Fillers held a dominant market position in the By Sales Channel segment of the Aerosol Actuators Market, with a 73.50% share. Brand owners and contract fillers place large-volume, specification-driven orders that allow actuator manufacturers to run high-cavitation molds at full utilization. UK shaving preparation aerosols increased by 10% in 2025, adding further direct procurement volume from personal care fillers sourcing ergonomic foam-dispensing actuator systems.

Key Market Segments

By Product Type

- Male Actuator

- Female Actuator

- Dosage Actuator

By Actuator Type

- Manual Actuators

- Electronic/Touchless Actuators

By Material

- Plastics (PP, PE)

- Others

By Application / End Use Industry

- Personal Care and Cosmetics

- Deodorants and Antiperspirants

- Hair Sprays and Hair Care

- Skincare Sprays and Sunscreens

- Household and Institutional Cleaning

- Surface Cleaners and Disinfectants

- Air Fresheners

- Pest Control Sprays

- Automotive and Industrial Maintenance

- Lubricants and Corrosion Inhibitors

- Paints, Coatings and Adhesives

- Technical Sprays

- Healthcare and Pharmaceuticals

- Medical Inhalers (MDI)

- Disinfectant and Wound Care Sprays

- Nasal Sprays

- Food and Beverage

- Culinary Sprays

- Whipped Cream Dispensers

- Paints and Coatings

- Others (Agriculture, Veterinary, etc.)

By Sales / Supply Channel

- Direct Supply to Brand Owners and Fillers

- Global OEM / System Integrator Supply

Drivers

The shift toward PET-compatible and lightweight aerosol dispenser architectures requires fundamental actuator redesign to maintain pressure integrity, neck-fit precision, and chemical resistance while improving recyclability. Brand owners are signaling demand for scalable solutions deployable across mainstream portfolios, not isolated eco-products. Validated lightweight actuator platforms can be rolled out across multiple product lines, locking in multi-year supplier relationships and raising barriers to entry through tighter material compatibility requirements, supporting a +0.6 percentage-point long-term CAGR uplift.

Industry direction toward recyclable aerosol systems pushes suppliers to reduce metal content, simplify polymer blends, and rework the interface between actuator, valve, cap, and container so components do not disrupt PET stream recovery. This redesign pressure creates a technical differentiation window. Actuator manufacturers that validate compliant lightweight platforms ahead of regulatory deadlines secure preferred supplier status with brand owners managing large SKU portfolios across EU and UK markets.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Personal care aerosol premiumization and grooming spray mix expansion | +1.4% | Europe core, North America core, urban APAC | Short term (≤ 2 years) |

| EU/UK circular-packaging compliance pushing recyclable actuator redesign | +1.1% | EU core, UK, spill-over to global export hubs | Medium term (2-4 years) |

| Healthcare aerosol delivery shift, especially inhalation and dose-control formats | +0.9% | North America core, EU, Japan | Medium term (2-4 years) |

| Brand-led packaging differentiation through ergonomics, spray precision, and omnichannel shelf impact | +0.8% | North America, Western Europe, premium APAC | Short term (≤ 2 years) |

| Manufacturing localization and component resiliency after resin/logistics volatility | +0.7% | China, India, Southeast Asia, Mexico, Eastern Europe | Medium term (2-4 years) |

| PET/lightweight dispenser architecture and compatibility innovation | +0.6% | EU first, then North America and APAC corridors | Long term (≥ 4 years) |

Restraints

Trade-policy instability acts as a direct commercial restraint because actuator supply chains frequently span Asian molded parts, metal containers, valve systems, and final filling regions, making landed cost sensitive to overlapping duties on plastics, steel, and aluminum derivatives. In the US, 2025 tariff actions included a 20% tariff on imports from China by March 2025, a baseline 10% tariff on imported goods from April 2025, and a rise in steel and aluminum tariffs to 50% effective 4 June 2025.

Even where actuators themselves are plastic-dominant, higher can and valve costs reduce total aerosol system competitiveness. Procurement teams face pressure to dual-source, rebuild molds in alternate countries, or absorb 4–8% landed-cost inflation during transition periods. This lifts working capital, stretches qualification lead times, and slows volume awards in North America, supporting an estimated −0.8 percentage-point CAGR deduction.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Packaging compliance cost | -1.1% | EU, UK, North America core, India | Short term (≤ 2 years) |

| Resin and small-part inflation | -0.9% | EU, North America, APAC export hubs | Short term (≤ 2 years) |

| Tariff and trade disruption | -0.8% | North America core, China-linked supply chains, EU exporters | Short term (≤ 2 years) |

| Qualification delays in pharma | -0.7% | EU, North America, Japan | Medium term (2-4 years) |

| Substitution by pumps/triggers | -0.6% | Europe, North America, developed APAC | Medium term (2-4 years) |

| Freight and lead-time volatility | -0.5% | APAC-Europe lanes, APAC-North America lanes, MENA corridors | Short term (≤ 2 years) |

Challenges

The aerosol actuator manufacturing sector faces a structural shortage of skilled injection molding talent, with demand for specialized roles outpacing supply across mature and emerging manufacturing regions. In the US, more than 30,000 injection molding positions remain unfilled as of 2026, particularly in process technicians, mold maintenance engineering, CNC programming, and automation control. Over 40% of European plastics-processing firms identify labor shortages as a primary operational risk.

In Southeast Asia, approximately 60% of manufacturers report difficulty retaining skilled workers, with only about 30% of vocational graduates meeting technical expectations. This gap is especially critical in high-precision aerosol actuator production, where tooling requires micro-tolerances of ±0.01 mm or tighter. Under-skilled operations increase variability in mold temperature control and injection pressure stability, translating into 8–15% higher scrap rates compared to optimized production lines.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Propellant Transition and HFC Phase-Down Pressure | ~−0.8% | EU regulatory hubs; North America (AIM Act corridors); Pharma MDI value chains globally | Medium term (2–4 years) |

| Polypropylene and Resin Input Volatility | ~−0.6% | North America; Northeast Asia (China/South Korea); EU import corridors | Short term (≤ 2 years) |

| EU PPWR and Mono-Material Recyclability Re-engineering | ~−0.7% | EU market core; UK export corridors; global OEMs with EU-destined supply | Medium term (2–4 years) |

| Precision Tooling Talent Deficit in Injection Molding | ~−0.5% | North America; Western Europe; APAC (selective upskilling gaps) | Long term (≥ 4 years) |

| Geopolitical Tariff and Logistics Cost Volatility | ~−0.6% | APAC–EU transit corridors; US import supply chains; Middle East air freight hubs | Short to Medium term (1–3 years) |

| Pharmaceutical MDI Actuator Regulatory Complexity | ~−0.4% | EU (F-Gas quota integration); North America (FDA combination product pathway); Global pharma supply chains | Long term (≥ 4 years) |

Opportunities

Smart aerosol actuators represent an upgrade path rather than a baseline demand driver, as most of the current market still relies on standard mechanical dispensing systems. The value shift comes from integrating dose counting, lockout protection, usage feedback, and improved spray consistency into actuator design, especially in pharma and regulated personal care applications. These features can support 20% to 40% higher pricing versus conventional components.

In metered-dose systems, where typical delivery volumes sit in the 25 to 100 µL range, better actuation precision directly improves dose consistency and user compliance. This strengthens OEM differentiation and raises switching costs across pharmaceutical supply chains. Scale is supported by large installed aerosol volumes of about 3.7 billion units in the US and 5.2 billion units in Europe, creating a strong penetration base for premium actuator formats.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Smart dose-indicating actuators | +1.6% | North America core, EU, Japan | Short term (≤ 2 years) |

| Premium low-footprint actuator systems | +1.3% | EU, UK, North America | Short term (≤ 2 years) |

| APAC mass-premium personal care expansion | +2.1% | India, ASEAN, China | Medium term (2-4 years) |

| Pharma-adjacent nasal and topical platforms | +1.8% | North America, EU, select APAC | Medium term (2-4 years) |

| Industrial and technical spray conversion | +1.2% | North America, EU, LatAm | Medium term (2-4 years) |

| Roll-up of regional actuator molders | +1.5% | EU, North America, APAC | Long term (≥ 4 years) |

Regional Analysis

Europe Dominates the Aerosol Actuators Market with a Market Share of 40.57%, Valued at USD 0.68 Billion

Europe holds the largest regional position in the aerosol actuators market, supported by one of the world’s highest aerosol production volumes and a mature consumer goods manufacturing base. Personal care aerosols represented 56.4% of all European aerosol fillings in 2023. The UK produced 1.4 billion aerosol units in 2023, accounting for 26.9% of total European aerosol output, making it the single largest national contributor to regional actuator demand.

Germany produced 920 million aerosol units in 2023, representing 17.4% of European aerosol output. Germany’s scale as an aerosol manufacturer reflects its dominant position in household, automotive, and industrial aerosol categories, each requiring distinct actuator specifications. This diversity of end-use formats gives German actuator procurement a broader portfolio footprint than most other national markets.

France produced 723 million aerosol dispensers in 2024, up from 657.9 million units in 2023, representing nearly 10% annual production growth. French hair-care aerosol production increased by 13% in 2024, and body-care aerosol production rose by 4% in the same period. This growth positions France as the fastest-expanding major European actuator-consuming market based on recent production data.

North America represents a substantial actuator market driven by personal care, healthcare, and household aerosol volumes. UK aerosol filling declined by only 2% year-over-year in 2025, demonstrating continued stability in actuator-consuming aerosol packaging despite broader economic pressures. Personal care aerosols represented 75% of the UK aerosol market in 2024, confirming personal care as the dominant demand driver within the Anglo-American market context.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Aptar Beauty holds a strong competitive position in the premium aerosol actuator segment through continuous mechanism innovation. In April 2025, LINDAL Group showcased FlipStraw™ at the Aerosol Dispensers Forum in Paris, marking the first commercial presentation to aerosol fillers and brand owners. GSK’s next-generation low-carbon Ventolin inhaler could reduce greenhouse-gas emissions by approximately 92% per inhaler, creating actuator redesign requirements that precision-capable suppliers like Aptar are positioned to fulfill.

LINDAL Group competes through a modular product architecture that covers both standard and specialty aerosol actuator formats across multiple valve compatibility standards. The FlipStraw™ system launched in April 2025 combines precision and broad-area spray from a single actuator and supports both LI male valves and LIB one-inch ball valves, addressing a wide band of household and industrial filling customers. This dual-compatibility design reduces qualification complexity for fillers managing multiple SKU formats simultaneously.

Key Players

- Aptar Beauty

- LINDAL Group

- Rieke Packaging Systems

- Coster Tecnologie Speciali

- Summit Packaging Systems

- Salvalco

- MRX Packaging

- Precision Valve Corporation

- Nussbaum Matzingen

- SKS Bottle and Packaging

Recent Developments

- May 2026 – Aptar Beauty launched Double Click™ Technology for its Twist-to-Lock aerosol actuator portfolio, introducing an audible double-click confirmation when the actuator reaches the locked or unlocked position to improve accessibility, transport security, and e-commerce performance.

- May 2026 – Aptar Beauty expanded its Twist-to-Lock actuator range by integrating Double Click™ Technology into hoodless aerosol actuators, making the platform compliant with Amazon ISTA-6 e-commerce transport requirements and reducing accidental actuation during shipment.

- April 2025 – LINDAL Group introduced FlipStraw™ with compatibility for both LI male valves and LIB one-inch ball valves, allowing use in standard and inverted aerosol dispensing applications.

- April 2025 – LINDAL Group commercialized FlipStraw™ featuring top-load resistance and a molded tear-away safety tab, specifically designed to prevent accidental spraying during stacking, storage, and transportation.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.70 Billion |

| Forecast Revenue (2035) | USD 2.60 Billion |

| CAGR (2026-2035) | 4.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Male Actuator, Female Actuator, Dosage Actuator), By Actuator Type (Manual Actuators, Electronic/Touchless Actuators), By Material (Plastics (PP, PE), Others), By Application / End Use Industry (Personal Care and Cosmetics, Household and Institutional Cleaning, Automotive and Industrial Maintenance, Healthcare and Pharmaceuticals, Food and Beverage, Paints and Coatings, Others), By Sales / Supply Channel (Direct Supply to Brand Owners and Fillers, Global OEM / System Integrator Supply) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Aptar Beauty, LINDAL Group, Rieke Packaging Systems, Coster Tecnologie Speciali, Summit Packaging Systems, Salvalco, MRX Packaging, Precision Valve Corporation, Nussbaum Matzingen, SKS Bottle and Packaging |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

The Global Aerosol Actuators Market Size size is USD 1.7 Billion in 2023.

The Global Aerosol Actuators Market is expected to grow at a CAGR of 4.80% (2024-2033).

Market.US has segmented the Global Aerosol Actuators Market by geographic (North America, Europe, APAC, South America, and Middle East and Africa). By Product Type(Metered Valve, Continuous Valve), By End-Use(Cosmetics & Personal Care, Healthcare, Homecare, Automotive, Food & Beverage, Paint & Coating, Others)

Aptar Group, Mitani Valve Co. Ltd., Lindal Group, Coster Group, RРС Group plc., Rасkоw Polymers Corp., Cobra Plastics Inc., Plasticap, Сlауtоn Corp., Меdіа Маnоеuvrе Pvt. Ltd., Аѕріrе Industries, Summit Packaging Systems Inc.

The Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, Rest of Western Europe, Eastern Europe, Russia, Poland, The Czech Republic, Greece, Rest of Eastern Europe leading key areas of operation for Global Aerosol Actuators Market.