Quick Navigation

Report Overview

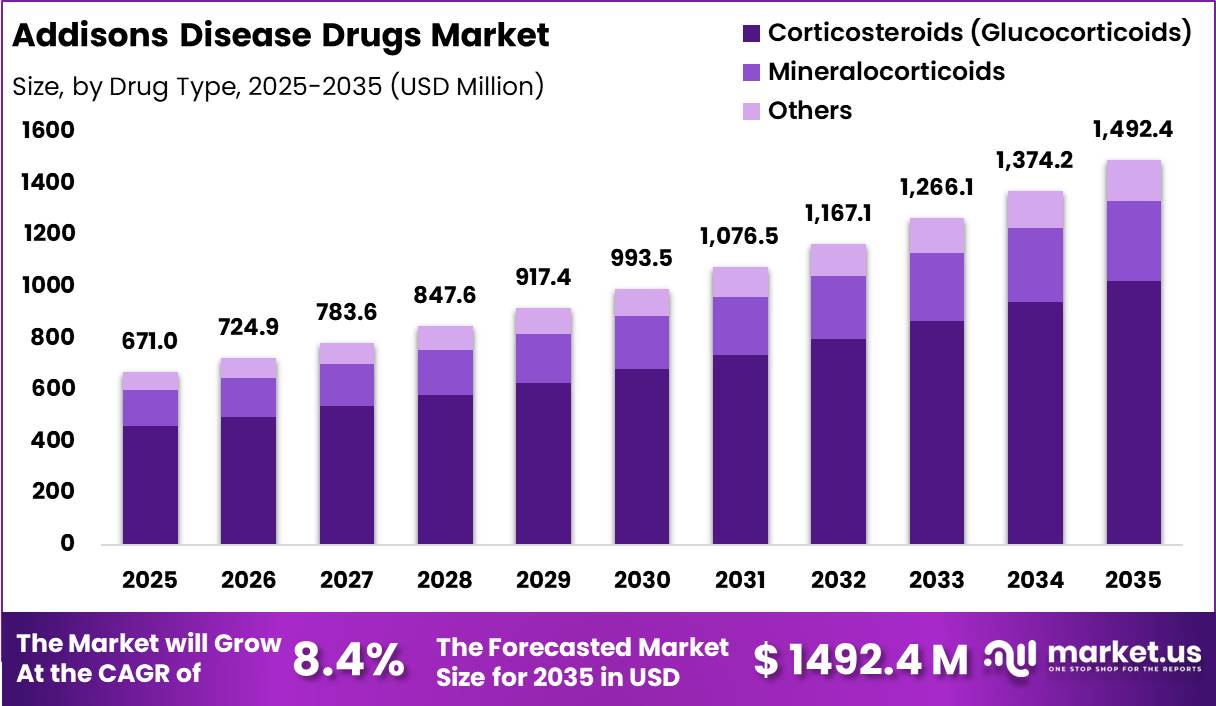

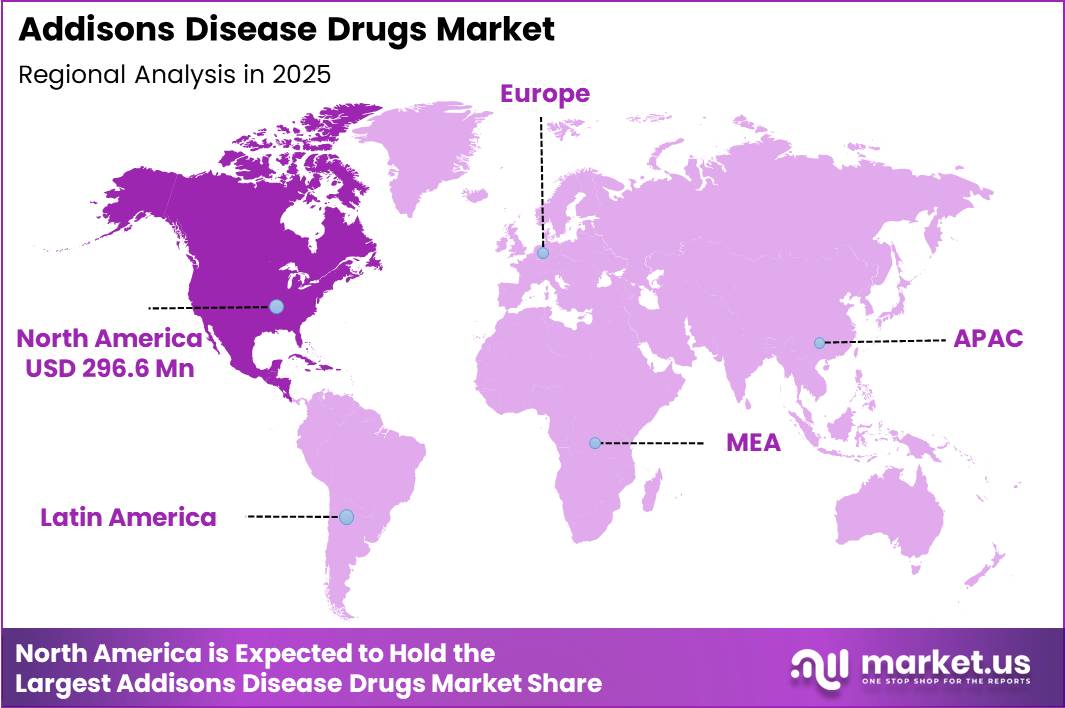

Global Addisons Disease Drugs Market size is expected to be worth around US$ 1,492.4 Million by 2035 from US$ 671.0 Million in 2025, growing at a CAGR of 8.4% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 44.2% share with a revenue of US$ 296.6 Million.

The Addison’s Disease Drugs Market represents a specialized segment of the endocrine therapeutics industry focused on the treatment of primary adrenal insufficiency, commonly known as Addison’s disease. This rare but serious disorder occurs when the adrenal glands fail to produce sufficient amounts of cortisol and, in many cases, aldosterone, hormones that are essential for regulating metabolism, blood pressure, immune response, and the body’s reaction to stress.

As a result, patients require lifelong hormone replacement therapy, creating a sustained demand for corticosteroid-based medications such as hydrocortisone, prednisone, dexamethasone, and fludrocortisone. According to the U.S. National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK), Addison’s disease affects approximately 100–140 individuals per million population in developed countries, while secondary adrenal insufficiency affects 150–280 individuals per million, highlighting a significant patient population requiring long-term treatment.

Market growth is being supported by increasing diagnosis rates, greater awareness of adrenal disorders, and improvements in endocrine care pathways. Autoimmune adrenalitis remains the leading cause of Addison’s disease, accounting for nearly 80–90% of cases in developed nations, while infectious diseases such as tuberculosis continue to contribute to adrenal insufficiency in several regions.

Furthermore, the growing prevalence of tuberculosis remains a relevant factor, as the U.S. Centers for Disease Control and Prevention (CDC) reported 10,388 tuberculosis cases in 2024, reflecting the continued burden of infections that may lead to adrenal gland damage in susceptible individuals.

The market is also benefiting from advancements in modified-release corticosteroid formulations designed to better mimic the body’s natural cortisol rhythm, thereby improving treatment adherence and patient outcomes. Pharmaceutical companies are increasingly investing in patient-centric therapies, novel delivery systems, and precision hormone replacement approaches to reduce the risk of adrenal crises and enhance quality of life.

As healthcare systems place greater emphasis on early diagnosis and long-term disease management, the demand for effective Addison’s disease therapies is expected to remain strong, supporting continued innovation and expansion across the global market.

Key Takeaways

- Market Size: Global Addisons Disease Drugs Market size is expected to be worth around US$ 1,492.4 Million by 2035 from US$ 671.0 Million in 2025.

- Market Share: The market growing at a CAGR of 8.4% during the forecast period from 2026 to 2035.

- Drug Type Analysis: Corticosteroids (Glucocorticoids) accounted for the largest market share of 68.5% in 2025.

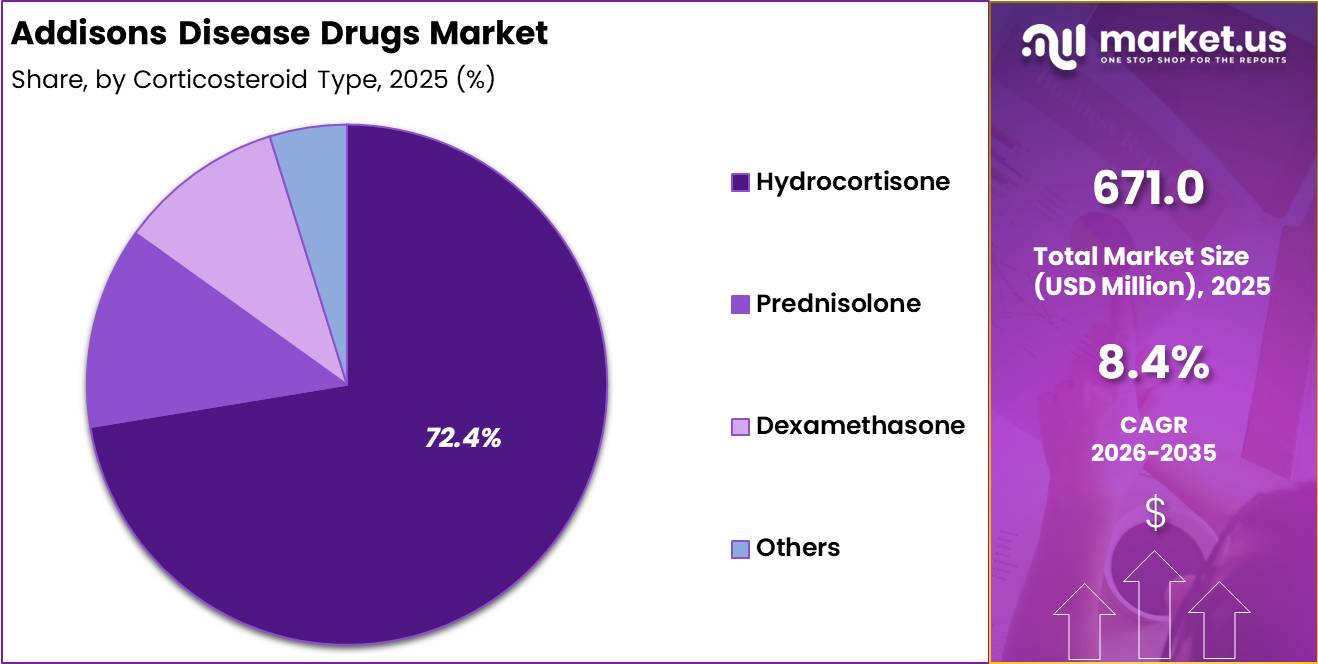

- Corticosteroid Type Analysis: Hydrocortisone dominated the market with a 72.4% share in 2025, owing to its widespread use as the standard first-line therapy for cortisol replacement.

- Route of Administration Analysis: The Oral segment held the dominant market share of 85.6% in 2025.

- End User Analysis: Hospitals emerged as the leading segment, accounting for 52.8% of the market share in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 44.2% share with a revenue of US$ 296.6 Million.

Drug Type Analysis

The drug type segment of the Addison’s disease drugs market is categorized into Corticosteroids (Glucocorticoids), Mineralocorticoids, and Others. Among these, Corticosteroids (Glucocorticoids) accounted for the largest market share of 68.5% in 2025, driven by their essential role in replacing deficient cortisol levels in patients with adrenal insufficiency.

These therapies represent the cornerstone of Addison’s disease management and are widely prescribed for long-term hormone replacement. The strong clinical preference for glucocorticoids is supported by their proven efficacy in controlling fatigue, weight loss, hypotension, and other symptoms associated with cortisol deficiency. Increasing diagnosis rates and growing awareness regarding adrenal disorders are further contributing to segment growth.

The Mineralocorticoids segment represents the second-largest share of the market. These drugs are commonly administered alongside glucocorticoids to restore aldosterone deficiency and maintain electrolyte balance, blood pressure regulation, and fluid homeostasis. Rising adoption of combination hormone replacement therapies is supporting demand for this segment.

The Others category includes adjunctive treatments and supportive medications used for symptom management and specific patient requirements. Although comparatively smaller, this segment is expected to witness steady growth due to ongoing research into improved treatment approaches and personalized disease management strategies.

Corticosteroid Type Analysis

Based on corticosteroid type, the Addison’s disease drugs market is segmented into Hydrocortisone, Prednisolone, Dexamethasone, and Others. Hydrocortisone dominated the market with a 72.4% share in 2025, owing to its widespread use as the standard first-line therapy for cortisol replacement.

Hydrocortisone closely mimics the body’s natural cortisol production, making it the preferred treatment option among healthcare professionals. Its established safety profile, flexible dosing schedules, and strong clinical effectiveness in managing chronic adrenal insufficiency continue to support its leading position. Increasing availability of optimized formulations and improved patient adherence are further enhancing segment growth.

The Prednisolone segment holds a significant share due to its longer duration of action and convenience in reducing dosing frequency. It is often prescribed for patients who require alternative treatment regimens or improved compliance with hormone replacement therapy.

The Dexamethasone segment accounts for a smaller portion of the market but remains important in specific clinical situations where potent and prolonged glucocorticoid activity is required. Its use is generally limited because of a higher risk of overtreatment and adverse effects.

The Others segment includes emerging corticosteroid formulations and specialized therapies that address individual patient needs, contributing to gradual market expansion.

Route of Administration Analysis

The Addison’s disease drugs market is segmented by route of administration into Oral, Injectable, and Others. The Oral segment held the dominant market share of 85.6% in 2025, primarily due to the convenience, effectiveness, and widespread acceptance of oral hormone replacement therapies.

Oral corticosteroids and mineralocorticoids are considered the standard treatment approach for long-term management of Addison’s disease, enabling patients to maintain stable hormone levels with routine daily dosing. The ease of self-administration, lower healthcare costs, and improved patient adherence associated with oral formulations continue to strengthen demand within this segment.

The Injectable segment represents a crucial component of the market, particularly for emergency management of adrenal crises and severe cases where oral administration is not feasible. Injectable hydrocortisone remains an essential treatment option in hospitals, emergency departments, and critical care settings. Increasing awareness regarding emergency preparedness among Addison’s disease patients is supporting segment growth.

The Others segment includes alternative administration methods and specialized delivery systems under development. While currently accounting for a smaller market share, ongoing pharmaceutical innovation aimed at improving treatment outcomes and patient convenience is expected to create new growth opportunities within this category over the forecast period.

End User Analysis

Based on end user, the Addison’s disease drugs market is segmented into Hospitals, Specialty Clinics, Homecare Settings, and Others. Hospitals emerged as the leading segment, accounting for 52.8% of the market share in 2025.

The dominance of hospitals is attributed to their comprehensive diagnostic capabilities, access to endocrinology specialists, and ability to manage both routine treatment and life-threatening adrenal crises. Hospitals serve as primary centers for diagnosis, treatment initiation, emergency care, and monitoring of patients with adrenal insufficiency, supporting their significant market contribution.

Specialty Clinics represent a substantial segment due to the growing preference for specialized endocrine care. These facilities provide focused disease management, personalized treatment plans, and regular follow-up services, which contribute to improved patient outcomes and treatment adherence.

The Homecare Settings segment is witnessing notable growth as long-term hormone replacement therapy increasingly shifts toward self-management. Advancements in patient education, remote monitoring technologies, and convenient oral treatment options are encouraging home-based disease management while reducing healthcare utilization costs.

The Others segment includes ambulatory care centers, research institutions, and community healthcare facilities. Continuous improvements in healthcare infrastructure and increasing awareness of adrenal disorders are expected to support steady growth across these alternative care settings.

Key Market Segments

By Drug Type

- Corticosteroids (Glucocorticoids)

- Mineralocorticoids

- Others

By Corticosteroid Type

- Hydrocortisone

- Prednisolone

- Dexamethasone

- Others

By Route of Administration

- Oral

- Injectable

- Others

By End User

- Hospitals

- Specialty Clinics

- Homecare Settings

- Others

Driving Factors

Rising Prevalence of Autoimmune Disorders Increasing Addison’s Disease Incidence

The increasing prevalence of autoimmune diseases is a significant driver of the Addison’s disease drugs market. Addison’s disease, also known as primary adrenal insufficiency, is most commonly caused by autoimmune destruction of the adrenal cortex.

Several autoimmune disorders, including type 1 diabetes, autoimmune thyroid disease, and autoimmune polyglandular syndromes, are associated with a higher risk of Addison’s disease. The U.S. Centers for Disease Control and Prevention (CDC) reports that approximately 38.4 million Americans were living with diabetes in 2021, with type 1 diabetes representing a significant autoimmune component of the disease burden. Increased monitoring of patients with autoimmune conditions has improved the identification of adrenal insufficiency, supporting earlier treatment initiation.

Since Addison’s disease requires lifelong glucocorticoid and often mineralocorticoid replacement therapy, every newly diagnosed patient contributes to long-term pharmaceutical demand. Growing awareness among endocrinologists regarding autoimmune disease complications, combined with advances in diagnostic testing and routine screening of high-risk populations, is further supporting treatment uptake.

Consequently, the rising burden of autoimmune diseases worldwide continues to strengthen the demand for Addison’s disease therapeutics and remains a key growth driver for the market.

Trending Factors

Adoption of Physiological Cortisol Replacement Approaches

A significant trend in the Addison’s disease drugs market is the shift toward therapies that better mimic the body’s natural cortisol secretion pattern. Conventional hydrocortisone treatment often requires administration two to three times daily, creating challenges related to patient compliance and fluctuations in cortisol levels. Healthcare providers are increasingly focusing on treatment strategies that provide more physiological hormone replacement and improve quality of life.

Clinical management guidelines from endocrine health organizations emphasize individualized dosing and optimized corticosteroid replacement to reduce complications associated with under- or over-treatment. Research efforts are focused on modified-release hydrocortisone formulations and advanced delivery systems designed to replicate circadian cortisol rhythms. These innovations aim to improve fatigue management, metabolic outcomes, and overall patient well-being.

Furthermore, digital health tools and patient monitoring programs are being integrated into chronic disease management, enabling better dose adjustment during illness, surgery, or periods of physical stress. Since Addison’s disease commonly affects adults between 30 and 50 years of age, maintaining long-term treatment adherence and minimizing adverse effects remain key clinical priorities. The increasing emphasis on personalized endocrine care is therefore shaping product development and treatment practices within the market.

Restraining Factors

Limited Patient Population and Diagnostic Challenges

The rarity of Addison’s disease remains a major restraint for the market. According to NIDDK, making it one of the less common endocrine disorders. Such a limited patient pool restricts commercial opportunities for pharmaceutical manufacturers and can reduce incentives for large-scale investment in novel drug development.

In addition, diagnosis is often delayed because symptoms such as chronic fatigue, muscle weakness, weight loss, abdominal discomfort, nausea, and low blood pressure overlap with those of many other medical conditions. NIDDK notes that symptoms frequently develop gradually, resulting in misdiagnosis or delayed recognition of the disease. Patients may remain undiagnosed until an adrenal crisis occurs, which can be life-threatening.

Another limiting factor is the availability of effective generic corticosteroids, including hydrocortisone and fludrocortisone. These established therapies are relatively inexpensive and widely prescribed, creating pricing pressure for manufacturers attempting to introduce premium products.

Furthermore, healthcare systems in several countries prioritize cost-effective treatment options, limiting rapid adoption of newer formulations. Collectively, the small patient population, diagnostic complexity, and strong reliance on generic hormone replacement therapies continue to restrain revenue growth opportunities within the Addison’s disease drugs market.

Opportunity

Expanding Awareness and Improved Endocrine Care Infrastructure

An important opportunity in the Addison’s disease drugs market lies in increasing disease awareness and strengthening endocrine healthcare infrastructure worldwide. Government health agencies and academic institutions are actively promoting awareness of adrenal insufficiency and improving access to diagnostic testing. Greater physician education regarding symptoms and diagnostic pathways can facilitate earlier detection and treatment initiation.

The growing prevalence of autoimmune diseases, which account for approximately 8 to 9 out of every 10 Addison’s disease cases in developed countries, is also expected to support future patient identification. Improved screening among individuals with autoimmune thyroid disease, type 1 diabetes, and other autoimmune disorders may increase diagnosis rates of adrenal insufficiency.

Furthermore, opportunities exist for the development of innovative corticosteroid replacement therapies, emergency injectable products, and patient-centric treatment solutions that improve cortisol control and reduce adrenal crisis risk. NIDDK highlights that patients require higher corticosteroid doses during illness, injury, or surgery, emphasizing the need for flexible and advanced treatment options.

As healthcare systems continue to invest in rare disease management and endocrine specialty services, demand for improved therapeutic approaches is expected to increase. These factors create favorable conditions for innovation and expansion within the Addison’s disease drugs market over the coming years.

Regional Analysis

In 2025, North America dominated the Addison’s Disease Drugs Market, accounting for more than 44.2% of the global market share and generating revenue of approximately US$ 296.6 million. The region’s leadership can be attributed to a well-established healthcare infrastructure, high disease awareness, widespread availability of hormone replacement therapies, and favorable reimbursement policies.

The presence of major pharmaceutical manufacturers, advanced diagnostic capabilities, and increased screening for adrenal insufficiency further support market growth across the United States and Canada. Continuous investments in rare disease research and the adoption of innovative treatment approaches are also contributing to regional market expansion.

Europe represented the second-largest market, driven by strong healthcare systems, growing awareness of endocrine disorders, and supportive government healthcare initiatives. Countries such as Germany, the United Kingdom, France, and Italy continue to witness stable demand for corticosteroid replacement therapies owing to improved diagnosis rates and access to specialized endocrinology services.

The Asia Pacific market is expected to register the fastest growth during the forecast period. Rising healthcare expenditure, improving diagnostic infrastructure, increasing patient awareness, and expanding access to treatment in countries such as China, India, and Japan are supporting market development. Additionally, a large population base and growing investments in healthcare modernization are creating significant growth opportunities.

Latin America and the Middle East & Africa accounted for a comparatively smaller market share. However, gradual improvements in healthcare access, increasing awareness of rare endocrine disorders, and government efforts to strengthen healthcare services are expected to support steady market growth in these regions over the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The Addison’s Disease Drugs Market is characterized by the presence of established pharmaceutical companies with strong capabilities in corticosteroid production, endocrinology therapies, and specialty medicines. Key players such as Pfizer Inc., Novartis AG, Merck & Co., Inc., Viatris Inc., Teva Pharmaceutical Industries Ltd., Sun Pharmaceutical Industries Ltd., Dr. Reddy’s Laboratories Ltd., Cipla Ltd., Lupin Limited, and Hikma Pharmaceuticals PLC focus on maintaining a steady supply of glucocorticoid and mineralocorticoid replacement therapies used in the management of adrenal insufficiency.

Market competition is driven by product quality, regulatory compliance, geographic expansion, and pricing strategies. Generic drug manufacturers play a significant role by improving treatment accessibility and affordability across emerging economies. Companies are also investing in research activities aimed at developing improved corticosteroid formulations that enhance patient adherence and treatment outcomes.

Strategic acquisitions, partnerships, and portfolio expansion initiatives are further strengthening market positions. With growing awareness of rare endocrine disorders and increasing diagnosis rates, leading players are expected to focus on expanding their specialty and rare disease portfolios to capture future growth opportunities.

Market Key Players

- Pfizer Inc.

- Novartis AG

- Merck & Co., Inc.

- Mylan N.V. (Viatris)

- Teva Pharmaceutical Industries Ltd.

- Sun Pharmaceutical Industries Ltd.

- Dr. Reddy’s Laboratories Ltd.

- Cipla Inc.

- Lupin Limited

- Hikma Pharmaceuticals PLC

- Bayer AG

- Eli Lilly and Company

- Fresenius Kabi AG

- Amphastar Pharmaceuticals Inc.

- Endo International plc

- Others

Recent Developments

- March 2025 – Sun Pharmaceutical Industries Ltd. announced the acquisition of Checkpoint Therapeutics for approximately USD 355 million. The transaction expanded Sun Pharma’s specialty pharmaceutical portfolio and reinforced its presence in regulated markets, strengthening its long-term capabilities in specialty and rare disease therapeutics.

- July 2025 – Merck & Co., Inc. entered into a definitive agreement to acquire Verona Pharma in a deal valued at approximately USD 10 billion. The acquisition was aimed at expanding Merck’s specialty medicines portfolio and enhancing its pipeline diversification strategy through the addition of innovative respiratory therapies.

- September 2025 – Pfizer Inc. signed a definitive agreement to acquire Metsera, a clinical-stage biotechnology company focused on next-generation metabolic disease therapies. The transaction, valued at approximately USD 4.9 billion, was designed to strengthen Pfizer’s innovative medicine pipeline and expand its presence in high-growth therapeutic areas.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 671.0 Million |

| Forecast Revenue (2035) | US$ 1,492.4 Million |

| CAGR (2026-2035) | 8.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Type (Corticosteroids (Glucocorticoids), Mineralocorticoids, Others) By Corticosteroid Type (Hydrocortisone, Prednisolone, Dexamethasone, Others) By Route of Administration (Oral, Injectable, Others) By End User (Hospitals, Specialty Clinics, Homecare Settings, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Pfizer Inc., Novartis AG, Merck & Co., Inc., Mylan N.V. (Viatris), Teva Pharmaceutical Industries Ltd., Sun Pharmaceutical Industries Ltd., Dr. Reddy’s Laboratories Ltd., Cipla Inc., Lupin Limited, Hikma Pharmaceuticals PLC, Bayer AG, Eli Lilly and Company, Fresenius Kabi AG, Amphastar Pharmaceuticals Inc., Endo International plc, Others, |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |