Global 3D Printed Hip and Knee Implants Market By Material Type (Metallic Implants, Ceramic Implants, Polymeric Implants, Composite Implants and Others), By Fixation Type (Cemented Fixation, Cementless Fixation and Hybrid Fixation), By End User (Hospitals, Orthopedic Clinics and Ambulatory Surgical Centers (ASCs)), By Surgery Type (Total Hip Replacement, Partial Hip Replacement, Total Knee Replacement, Partial Knee Replacement and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180905

- Number of Pages: 323

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

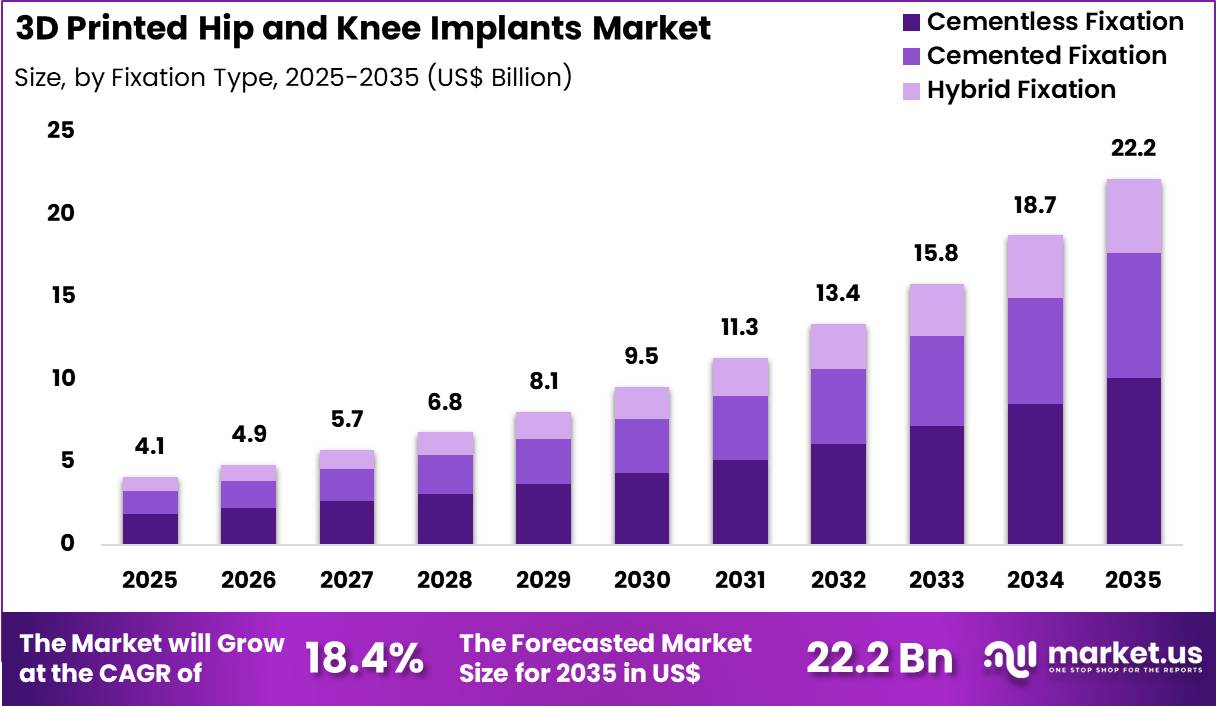

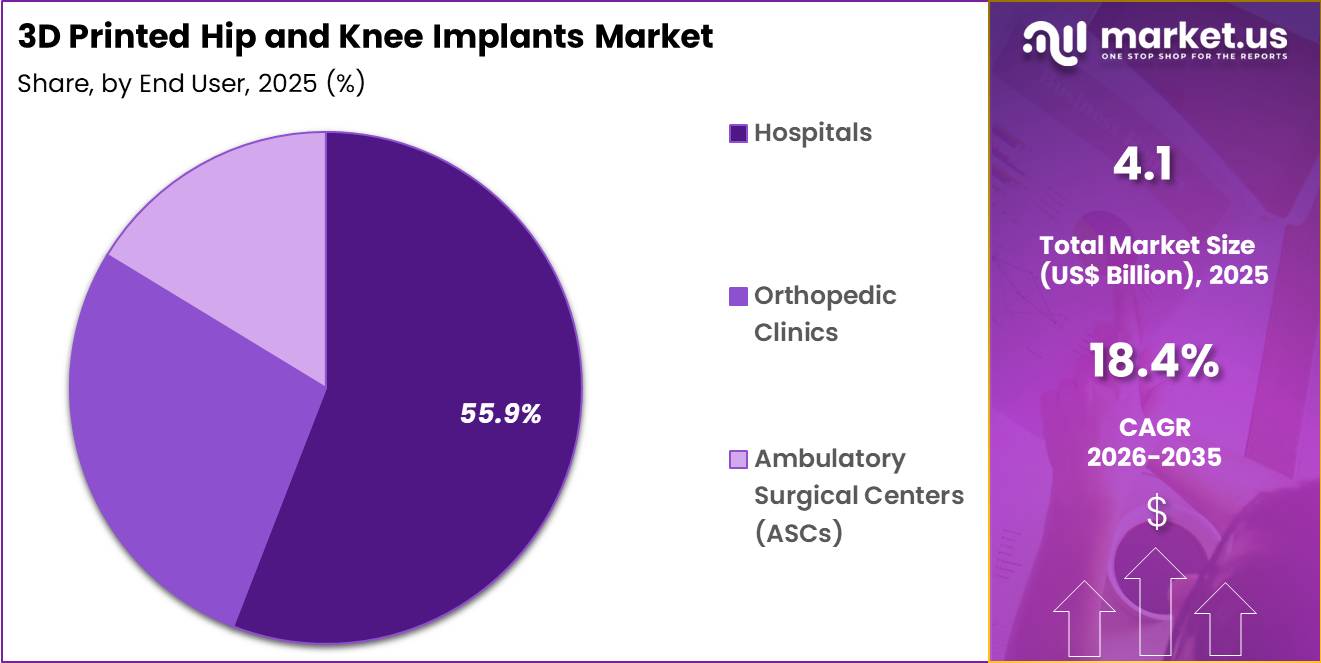

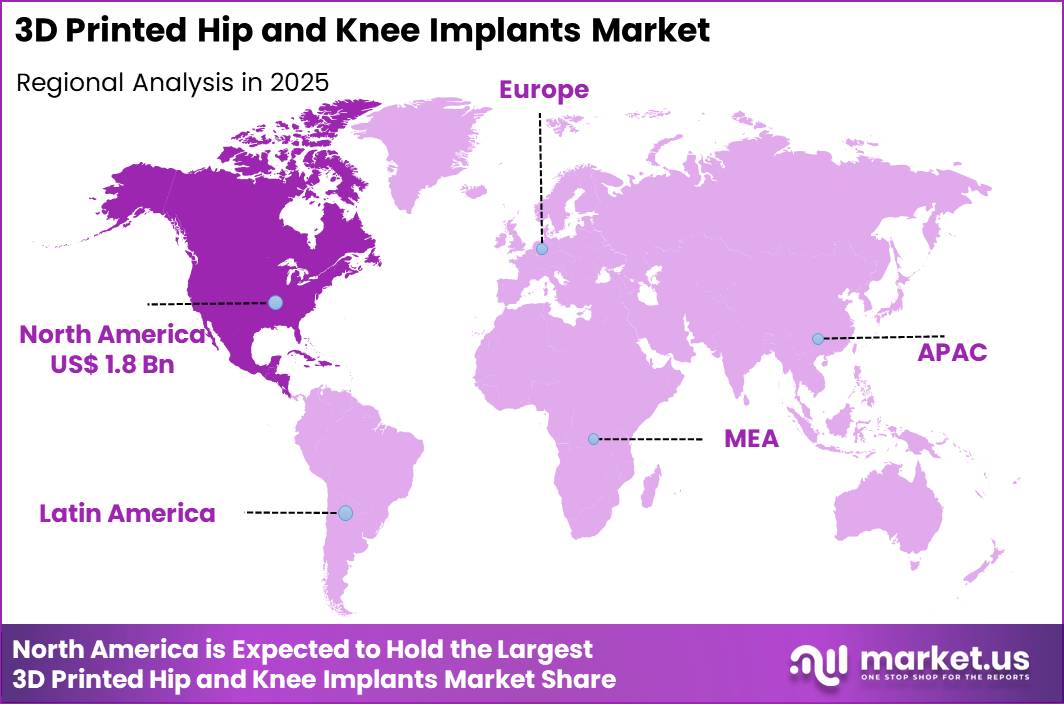

The Global 3D Printed Hip and Knee Implants Market size is expected to be worth around US$ 22.2 Billion by 2035 from US$ 4.1 Billion in 2025, growing at a CAGR of 18.4% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 43.8% share with a revenue of US$ 1.8 Billion.

Increasing demand for personalized orthopedic solutions propels the 3D printed hip and knee implants market as surgeons and manufacturers leverage additive manufacturing to create patient-specific devices that improve fit, function, and long-term performance.

Orthopedic surgeons increasingly utilize 3D-printed acetabular cups and femoral stems in total hip arthroplasty for patients with complex deformities or bone loss, customizing implant geometry to match individual anatomy and optimize load distribution.

These implants support revision hip procedures where standard components fail to address severe acetabular defects, allowing porous, lattice-structured designs that promote osseointegration and reduce stress shielding.

In knee reconstruction, surgeons apply 3D-printed femoral and tibial components in total knee arthroplasty to accommodate unique patellofemoral tracking and ligament balancing needs, particularly in cases of severe varus-valgus deformity or post-traumatic arthritis.

Patient-specific 3D-printed augments and cones fill bone voids in revision knee replacements, restoring joint line anatomy and stability while preserving remaining bone stock. These devices also enable partial knee resurfacing with customized unicompartmental components, preserving healthy cartilage and ligaments in isolated compartment disease.

Manufacturers pursue opportunities to incorporate advanced biomaterials and lattice architectures that enhance osseointegration and reduce implant weight, expanding applications in younger, active patients requiring durable, high-performance joint replacements. Developers advance solvent-free polymers suitable for high-resolution printing, enabling production of biocompatible, biodegradable prototypes that support temporary scaffolding or drug-eluting implants.

These innovations facilitate integration with robotic-assisted surgery systems, improving intraoperative precision in complex primary and revision cases. Opportunities emerge in hybrid implants combining 3D-printed porous surfaces with traditional stems or articulating surfaces, optimizing long-term fixation and wear characteristics.

Companies invest in preoperative planning software that generates models from CT data, streamlining customization and reducing operative time. In March 2025, China’s National Medical Products Administration granted approval for a laser-based 3D-printed total knee implant developed by Naton Biotechnology researchers.

The device was recognized as an innovative medical product, marking the first regulatory clearance of its kind for a 3D-printed knee replacement in the country. In October 2024, researchers at Duke University developed a solvent-free polymer suitable for digital light processing (DLP) 3D printing.

The material was designed to maintain structural strength without shrinkage while supporting biomedical applications, including the development of biodegradable and biocompatible medical device prototypes. Recent trends emphasize regulatory progress for customized implants and material advancements for clinical translation, positioning the market for growth in precision orthopedic reconstruction focused on improved fit, durability, and patient satisfaction.

Key Takeaways

- In 2025, the market generated a revenue of US$ 4.1 Billion, with a CAGR of 18.4%, and is expected to reach US$ 22.2 Billion by the year 2035.

- The material type segment is divided into metallic implants, ceramic implants, polymeric implants, composite implants and others, with metallic implants taking the lead with a market share of 71.3%.

- Considering fixation type, the market is divided into cemented fixation, cementless fixation and hybrid fixation. Among these, cementless fixation held a significant share of 45.6%.

- Furthermore, concerning the end user segment, the market is segregated into hospitals, orthopedic clinics and ambulatory surgical centers (ASCs). The hospitals sector stands out as the dominant player, holding the largest revenue share of 55.9% in the market.

- The surgery type segment is segregated into total hip replacement, partial hip replacement, total knee replacement, partial knee replacement and others, with the total knee replacement segment leading the market, holding a revenue share of 48.2%.

- North America led the market by securing a market share of 43.8%.

Material Type Analysis

Metallic implants accounted for 71.3% of growth within material type and dominate the 3D printed hip and knee implants market due to their superior mechanical strength and long-term durability in load-bearing orthopedic applications. Surgeons widely adopt titanium and cobalt-chromium alloys because these materials support excellent osseointegration and structural stability.

Additive manufacturing technologies allow manufacturers to design porous metal surfaces that promote bone ingrowth and implant fixation. The American Academy of Orthopaedic Surgeons reports that more than 790,000 total knee replacements occur annually in the United States, which drives significant demand for durable implant materials.

Metallic implants are expected to maintain strong adoption as orthopedic surgeons increasingly use patient-specific implant designs created through 3D printing technologies. Continuous improvements in biocompatible metal alloys and implant surface engineering further support segment growth.

Fixation Type Analysis

Cementless fixation accounted for 45.6% of growth within fixation type and dominate the market due to their ability to support natural bone integration without the use of bone cement. Orthopedic surgeons increasingly prefer cementless implants because porous surfaces allow bone tissue to grow directly into the implant structure.

This biological fixation improves long-term stability and reduces complications associated with cement degradation. Advances in 3D printing technology allow manufacturers to create lattice structures that mimic natural bone architecture. These structural designs encourage faster osseointegration and improved implant longevity.

Segment growth is projected to strengthen as surgeons favor implants that promote natural bone healing and long-term performance. The increasing use of advanced porous titanium implants further reinforces the adoption of cementless fixation in joint replacement procedures.

End User Analysis

Hospitals accounted for 55.9% of growth within end users and dominate the 3D printed hip and knee implants market due to their role as primary centers for orthopedic surgical procedures. Hospitals provide specialized orthopedic departments, advanced imaging systems, and multidisciplinary surgical teams required for joint replacement procedures.

Complex orthopedic surgeries often require operating rooms equipped with robotic systems and advanced implant technologies. Hospitals also manage post-operative rehabilitation programs that support patient recovery after joint replacement. Segment growth is expected to accelerate as aging populations increase demand for joint replacement procedures.

The Centers for Disease Control and Prevention reports that arthritis affects more than 58 million adults in the United States, which significantly increases demand for orthopedic treatments. Hospitals continue to invest in advanced surgical technologies that support the adoption of customized 3D printed implants.

Surgery Type Analysis

Total knee replacement accounted for 48.2% of growth within surgery type and dominate the 3D printed hip and knee implants market due to the high global prevalence of degenerative joint diseases. Osteoarthritis remains the primary cause of knee joint damage and mobility loss among older adults.

Patients increasingly seek surgical interventions that restore mobility and reduce chronic pain. Orthopedic surgeons adopt 3D printed implants to improve anatomical fit and surgical precision during knee replacement procedures. Customized implant designs enhance joint alignment and functional outcomes after surgery.

Segment growth is anticipated to strengthen as global populations continue to age and obesity rates increase. Healthcare systems increasingly expand joint replacement programs to address the growing burden of musculoskeletal disorders. Continuous innovation in implant design and surgical planning technologies further supports adoption of total knee replacement procedures.

Key Market Segments

By Material Type

- Metallic Implants

- Ceramic Implants

- Polymeric Implants

- Composite Implants

- Others

By Fixation Type

- Cemented Fixation

- Cementless Fixation

- Hybrid Fixation

By End User

- Hospitals

- Orthopedic Clinics

- Ambulatory Surgical Centers (ASCs)

By Surgery Type

- Total Hip Replacement

- Partial Hip Replacement

- Total Knee Replacement

- Partial Knee Replacement

- Others

Drivers

Increasing revenue in knee implants is driving the market.

Stryker Corporation’s knee implant portfolio, incorporating advanced 3D printed technologies for enhanced fixation and customization, has shown consistent expansion. Net sales for knees reached $2,273 million in 2023. This figure advanced to $2,447 million in 2024, reflecting a 7.6 percent increase. In 2025, revenue climbed to $2,656 million, marking an additional 8.6 percent growth from the prior year.

Such progression highlights surging demand for patient-specific 3D printed components in total knee arthroplasty. Surgeons increasingly select these implants for improved osseointegration and reduced revision rates. The revenue uplift enables sustained R&D investments in porous titanium structures.

Healthcare systems benefit from streamlined inventory through on-demand printing capabilities. This driver correlates with broader adoption of digital surgical planning in orthopedic centers. Overall, it fortifies the market’s foundation for innovative hip and knee solutions.

Restraints

Slow growth in hip implant sales is restraining the market.

Zimmer Biomet’s hip segment, encompassing traditional and emerging 3D printed acetabular cups, encountered tempered performance in recent years. Net sales for hips totaled $1,967 million in 2023. The figure edged up to $1,999 million in 2024, achieving only a 1.6 percent increase. This modest rise underscores challenges in penetrating conservative surgical preferences for hip revisions.

Facilities hesitate to transition from established off-the-shelf designs to customized 3D variants due to familiarity concerns. The restraint manifests in deferred capital expenditures for printing infrastructure. Manufacturers face pressure to demonstrate long-term cost efficiencies against incremental gains.

Such dynamics limit scalability in high-volume hip replacement procedures. Providers must address surgeon training gaps to elevate adoption thresholds. This factor curtails accelerated market maturation during the 2023-2025 period.

Opportunities

FDA clearance for 3D printed porous knee replacement systems is creating growth opportunities.

restor3d received U.S. Food and Drug Administration 510(k) clearance on March 27, 2025, for the iTotal Identity Cruciate Retaining 3DP Porous Knee Replacement System. This approval covers cementless fixation components fabricated via additive manufacturing for primary total knee arthroplasty. Opportunities arise for tailored implants matching patient anatomy to optimize load distribution and longevity.

The porous structure promotes bone ingrowth, potentially lowering aseptic loosening incidences. Developers can extend this technology to revision scenarios with complex defects. The clearance facilitates integration with robotic navigation for precise intraoperative adjustments. Partnerships with ambulatory surgery centers enable faster procedure turnaround.

Such advancements support value-based reimbursement models emphasizing durable outcomes. Stakeholders gain avenues for exporting cleared designs to international registries. This milestone paves the way for diversified portfolios in personalized orthopedics.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the 3D printed hip and knee implants market through hospital capital planning, orthopedic procedure volumes, and reimbursement policies. Inflation raises costs for titanium powders, additive manufacturing equipment, sterilization, and quality testing, which increases production expenses for implant manufacturers.

Higher interest rates limit capital investment in advanced printing facilities and slow expansion of manufacturing capacity. Geopolitical tensions affect global trade in specialty metal powders, precision printing systems, and surgical instrumentation, creating procurement challenges. Current US tariffs on imported additive manufacturing hardware and metal inputs increase equipment and material costs for suppliers serving the US market.

These pressures can delay technology adoption among smaller orthopedic centers and outpatient surgery facilities. At the same time, manufacturers strengthen domestic production networks and invest in local material sourcing to improve supply reliability. Growing demand for customized implants and improved surgical outcomes continues to support steady and confident market growth.

Latest Trends

FDA 510(k) clearance for 3D printed porous titanium tibial baseplate is driving the market.

Maxx Orthopedics obtained U.S. Food and Drug Administration 510(k) clearance on February 19, 2025, for its 3D printed Porous Titanium Tibial Baseplate within the Freedom Total Knee System. The device features a lattice architecture designed to enhance biological fixation without cement. This development addresses unmet needs in active patients requiring stable implant interfaces.

Surgeons appreciate the baseplate’s compatibility with modular polyethylene inserts for versatile sizing. The clearance validates the manufacturing process for consistent porosity gradients. Facilities report potential reductions in operative times through simplified instrumentation. The innovation aligns with trends toward metal additive manufacturing in load-bearing applications.

Early adopters observe improved radiographic integration at six-month follow-ups. Collaborative validations with imaging software refine preoperative templating. Overall, this 2025 authorization accelerates the shift toward fully customized knee reconstructions.

Regional Analysis

North America is leading the 3D Printed Hip and Knee Implants Market

North America accounted for 43.8% of the 3D printed hip and knee implants market in 2025 as orthopedic centers increasingly adopted additive manufacturing technologies to improve implant customization and surgical outcomes. Hospitals across the United States and Canada have expanded joint replacement programs to address rising mobility disorders and age related degeneration.

The American Academy of Orthopaedic Surgeons reported that more than 790000 total knee replacements and over 450000 total hip replacements are performed each year in the United States, illustrating the large procedural base that supports demand for advanced implant technologies.

Orthopedic surgeons are increasingly selecting additively manufactured implants because porous structures produced through advanced printing techniques enhance bone integration and long term stability.

Medical device manufacturers have also accelerated innovation in patient specific implant designs that match anatomical variations more precisely than traditional manufacturing methods. Expanding use of digital surgical planning and robotic assisted orthopedic procedures further complements adoption of advanced implant technologies.

Academic medical centers and orthopedic research institutes continue to collaborate with device manufacturers to refine new implant materials and structural designs. Regulatory approvals for additively manufactured orthopedic implants have strengthened clinical confidence in these technologies. These developments collectively supported robust expansion of advanced orthopedic implant solutions across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to experience strong growth during the forecast period as healthcare systems expand orthopedic care capacity and invest in advanced surgical technologies. Rapid population aging across the region is increasing the prevalence of osteoarthritis and other degenerative joint conditions that require joint replacement surgery.

According to the World Health Organization, the global population aged 60 years and older reached about 1.1 billion people in 2022, and a significant share of this demographic growth is occurring in Asian countries. Hospitals in China, Japan, South Korea, and India are expanding orthopedic surgery programs and introducing advanced digital surgical planning technologies that support patient specific implants.

Medical universities and orthopedic research institutes are strengthening training programs focused on additive manufacturing and advanced implant design. Regional governments are also investing in biotechnology and medical device manufacturing sectors to develop domestic capabilities in advanced implant production.

Private healthcare networks are adopting modern surgical technologies to meet increasing patient expectations for improved mobility and faster recovery. Medical device companies are forming partnerships with local hospitals to introduce innovative orthopedic implant technologies across emerging markets. These factors are expected to drive steady adoption of advanced orthopedic implant manufacturing technologies throughout Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the 3D Printed Hip and Knee Implants market pursue expansion by investing heavily in additive manufacturing platforms, personalized implant design, and advanced porous lattice structures that promote stronger bone integration. Companies collaborate with orthopedic surgeons and research institutes to develop patient-specific implants that improve surgical precision and long-term joint stability.

They also strengthen growth through regulatory approvals, robotic-assisted surgery integration, and continuous product launches that support minimally invasive joint replacement procedures. Three-dimensional printing enables highly customized orthopedic implants and complex geometries that enhance clinical outcomes and implant performance.

Stryker represents a prominent participant in the 3D Printed Hip and Knee Implants market and operates as a global medical technology company headquartered in Michigan that develops orthopedic implants, surgical equipment, and advanced digital surgery systems.

The firm leverages proprietary additive manufacturing technologies such as Tritanium porous structures to produce implants designed to encourage bone growth and improve fixation in joint replacement surgeries. The company has manufactured millions of such implants using additive manufacturing since the early 2010s, demonstrating large-scale commercialization of this technology.

Industry competitors including Zimmer Biomet and Smith & Nephew also expand capabilities through 3D design platforms, surgeon training programs, and partnerships that accelerate adoption of next-generation orthopedic implants.

Top Key Players

- Stryker Corporation

- Zimmer Biomet Holdings Inc.

- Johnson & Johnson (DePuy Synthes)

- Medtronic plc

- Smith & Nephew plc

- Exactech Inc.

- 3D Systems Corporation

- Stratasys Ltd.

Recent Developments

- In February 2025, NextStep Arthropedix expanded its distribution network into the state of Georgia to address growing demand for orthopedic solutions. The company applies 3D-printing technologies in the development and production of advanced materials and components used across areas such as medical ceramics, microelectronics, and antimicrobial applications.

- In January 2025, restor3d’s chief executive officer and co-founder Kurt Jacobus emphasized the company’s strategy of using patient-specific data and additive manufacturing to advance orthopedic care. By combining artificial intelligence with 3D-printed implant design, the company aims to improve patient mobility outcomes while expanding its presence in emerging segments of the orthopedic device market.

Report Scope

Report Features Description Market Value (2025) US$ 4.1 Billion Forecast Revenue (2035) US$ 22.2 Billion CAGR (2026-2035) 18.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Material Type (Metallic Implants, Ceramic Implants, Polymeric Implants, Composite Implants and Others), By Fixation Type (Cemented Fixation, Cementless Fixation and Hybrid Fixation), By End User (Hospitals, Orthopedic Clinics and Ambulatory Surgical Centers (ASCs)), By Surgery Type (Total Hip Replacement, Partial Hip Replacement, Total Knee Replacement, Partial Knee Replacement and Others) Regional Analysis North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Stryker, Zimmer Biomet, Johnson & Johnson, Medtronic, Smith & Nephew, Exactech, 3D Systems, Stratasys Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  3D Printed Hip and Knee Implants MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

3D Printed Hip and Knee Implants MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Stryker Corporation

- Zimmer Biomet Holdings Inc.

- Johnson & Johnson (DePuy Synthes)

- Medtronic plc

- Smith & Nephew plc

- Exactech Inc.

- 3D Systems Corporation

- Stratasys Ltd.

Our Clients

- 180905

- March 2026