Quick Navigation

Overview

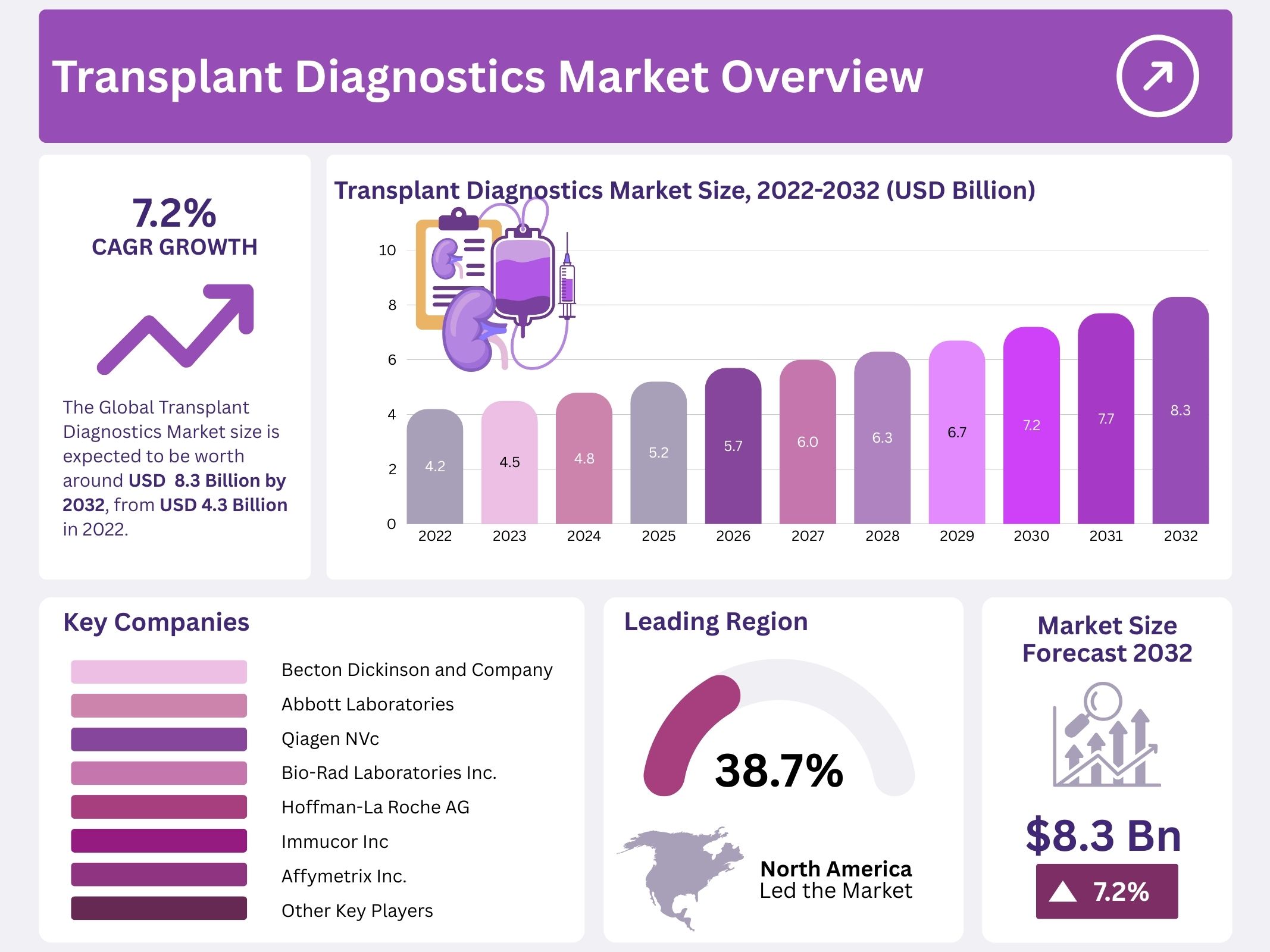

The Global Transplant Diagnostics Market is projected to reach USD 8.3 billion by 2032, up from USD 4.2 billion in 2022, growing at a compound annual growth rate (CAGR) of 7.2% during the forecast period from 2023 to 2032. This growth is primarily driven by several key factors, including the increasing prevalence of chronic diseases, advancements in diagnostic technologies, and rising demand for organ transplants worldwide.

A significant factor contributing to market expansion is the rising number of organ transplant procedures. Chronic diseases such as kidney failure, liver cirrhosis, heart failure, and certain cancers are increasingly prevalent. This has led to a growing need for organ transplants, which directly boosts the demand for reliable transplant diagnostics to ensure successful outcomes and reduce complications.

Technological advancements in molecular diagnostics are also playing a crucial role in market growth. Innovations such as next-generation sequencing (NGS), polymerase chain reaction (PCR), and high-throughput assays have improved the accuracy, speed, and sensitivity of transplant diagnostics. These advancements enable more precise donor-recipient matching, early detection of transplant rejection, and better management of immunosuppressive therapies, thereby enhancing transplant success rates.

Government initiatives and growing public awareness are further accelerating the adoption of transplant diagnostics. Countries are increasingly investing in healthcare infrastructure and launching awareness campaigns to promote organ donation. These efforts are driving higher adoption rates of transplant procedures and the associated diagnostic technologies. As a result, the demand for diagnostic tools that can assess organ compatibility and monitor transplant health is on the rise.

Lastly, the expanding healthcare access and infrastructure in emerging markets are opening new growth opportunities for the transplant diagnostics sector. Regions like Asia-Pacific, Latin America, and the Middle East are witnessing a surge in healthcare investments, improving access to diagnostic technologies. This trend is expected to drive further growth in the transplant diagnostics market, particularly in these developing regions.

Key Takeaways

- In 2022, PCR-based assays accounted for 34% of the transplant diagnostics market’s revenue, highlighting their significant role in molecular diagnostics.

- Reagents generated the highest revenue in the market and are projected to grow at the fastest CAGR in the coming years.

- Solid organ transplants held the largest market share, reflecting their critical role in transplant diagnostics.

- Research laboratories and academic institutions represented the largest share of the market, underscoring their importance in research and development.

- North America remained the largest market in 2022, contributing 38.7% to the overall turnover of the transplant diagnostics industry.

- The Asia Pacific region is expected to experience the fastest CAGR during the forecast period, reflecting its growing significance in the global market.

Regional Analysis

North America dominates the global transplant diagnostics market, holding the largest revenue share of 38.7%. This dominance is driven by factors such as advanced treatment methods, cutting-edge diagnostic technologies, and a strong healthcare system. The region benefits from extensive healthcare infrastructure and the availability of skilled professionals, contributing to its market leadership. Additionally, the high healthcare expenditure in North America further supports market growth.

The United States is the key player in the North American market, contributing significantly to its overall share. With its well-developed healthcare infrastructure, the country leads the market in transplant diagnostics. The availability of specialized healthcare professionals and access to advanced medical technologies play a crucial role in maintaining the nation’s dominant position in this sector.

In the Asia-Pacific region, China and India are experiencing the fastest growth in the transplant diagnostics market. This growth can be attributed to rising healthcare investments, improved infrastructure, and a growing focus on soft tissue transplants, stem cell therapies, and personalized medicines. As the region embraces advanced medical technologies, these markets are expected to expand rapidly during the forecast period, contributing significantly to the global market growth.

Segmentation Analysis

The molecular assay segment holds the largest revenue share, accounting for 59%. Pre-transplant analysis methods ensure the safety and effectiveness of procedures. The market is expected to grow due to factors such as the adoption of advanced technologies and increased awareness among physicians. Molecular assays are preferred over non-molecular assays because of their accuracy, efficacy, and reduced risks. Additionally, HLA typing has largely replaced serological assays. The PCR-based assay segment leads the market due to its wide range of applications.

During the forecast period, the sequencing-based assay segment is expected to experience the fastest growth. However, several challenges may hinder the market’s expansion. These include stringent regulatory protocols, slow approval processes, inadequate reimbursement policies for organ transplants, and ethical controversies. These factors could restrict the growth of the transplant diagnostics market. Despite these hurdles, the market’s potential remains high due to the continuous advancements in transplant diagnostic technologies and the increasing demand for improved organ transplant procedures.

The transplant diagnostics market is segmented into instruments, reagents, software, and others. The reagent segment dominates with a 32% revenue share. Reagents and consumables are often purchased through contracts, contributing to their widespread adoption. This segment is expected to maintain its dominance due to repeat purchases. The services and software market is also growing. The increasing use of advanced instruments has created a higher demand for training and technical support, which drives the expansion of this segment during the forecast period.

Research laboratories and academic institutes hold the largest share of the transplant diagnostics market. This is driven by the rapid modernization and automation of diagnostic laboratories, as well as increased research and development activities. Pharmaceutical and biotechnology companies are increasingly outsourcing their research to independent laboratories. Additionally, the growing number of organ transplant procedures supports the demand for advanced diagnostic tools. This segment is expected to continue dominating the market throughout the forecast period due to these factors.

Key Players Analysis

The transplant diagnostics market experiences moderate competition, with several factors shaping its landscape. Technological advancements, affordability, reagent efficacy, and organ preservation facilities are key challenges and opportunities for businesses. Companies are expected to focus on these areas to enhance decision-making in clinician practices and improve overall market performance during the forecast period. This competition level will drive innovation and operational efficiency across the industry, promoting sustainable growth.

Eurobio Scientific, a France-based biotechnology company, acquired GenDx, a molecular diagnostics startup from the Netherlands. This acquisition enables Eurobio Scientific to enhance its research and development in transplantation diagnostics. By integrating GenDx’s capabilities, Eurobio is positioned to expand its market presence. This strategic move emphasizes the increasing trend of mergers and acquisitions in the biotechnology sector, aimed at strengthening product portfolios and advancing scientific capabilities in transplant diagnostics.

Prominent players in the global transplant diagnostics market include QIAGEN N.V., Thermo Fisher Scientific Inc., Luminex Corporation, and Becton Dickinson and Company. Other major companies such as Olerup SSP AB, Alpha Laboratories, Takara Bio Inc., and CareDx Inc. also contribute significantly to the market’s growth. These companies play a crucial role in shaping market dynamics, advancing technologies, and responding to market demands. Their innovations continue to support the evolution of transplant diagnostics on a global scale.

Market Key Players

- Becton Dickinson and Company

- Abbott Laboratories

- Qiagen NV

- Biomérieux SA

- Bio-Rad Laboratories Inc.

- Hoffman-La Roche AG

- Immucor Inc

- Affymetrix Inc.

- Illumina Inc.

- Omixon Inc.

- Other Key Players

Conclusion

In conclusion, the transplant diagnostics market is poised for significant growth, driven by the increasing demand for organ transplants, advancements in diagnostic technologies, and rising awareness of chronic diseases. The market is benefiting from innovations in molecular diagnostics, particularly PCR-based and sequencing assays, which enhance transplant success rates. As healthcare infrastructure improves, especially in emerging markets, the adoption of transplant diagnostic tools will continue to rise. Key players in the market are focusing on technological advancements and strategic collaborations to meet the growing demand. Despite challenges like regulatory hurdles and ethical concerns, the market holds strong growth potential in the coming years.

Get in Touch with Us:

Market.us (Powered By Prudour Pvt. Ltd.)

Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States.

Contact No: +1 718 874 1545 (International), +91 78878 22626 (Asia).

Email: [email protected]

View More

Hair Transplant Market || Tissue and Organ Transplantation Market || Transplantation Market || Liver Transplantation Market || Organ Transplant Immunosuppressant Drugs Market