Quick Navigation

Report Overview

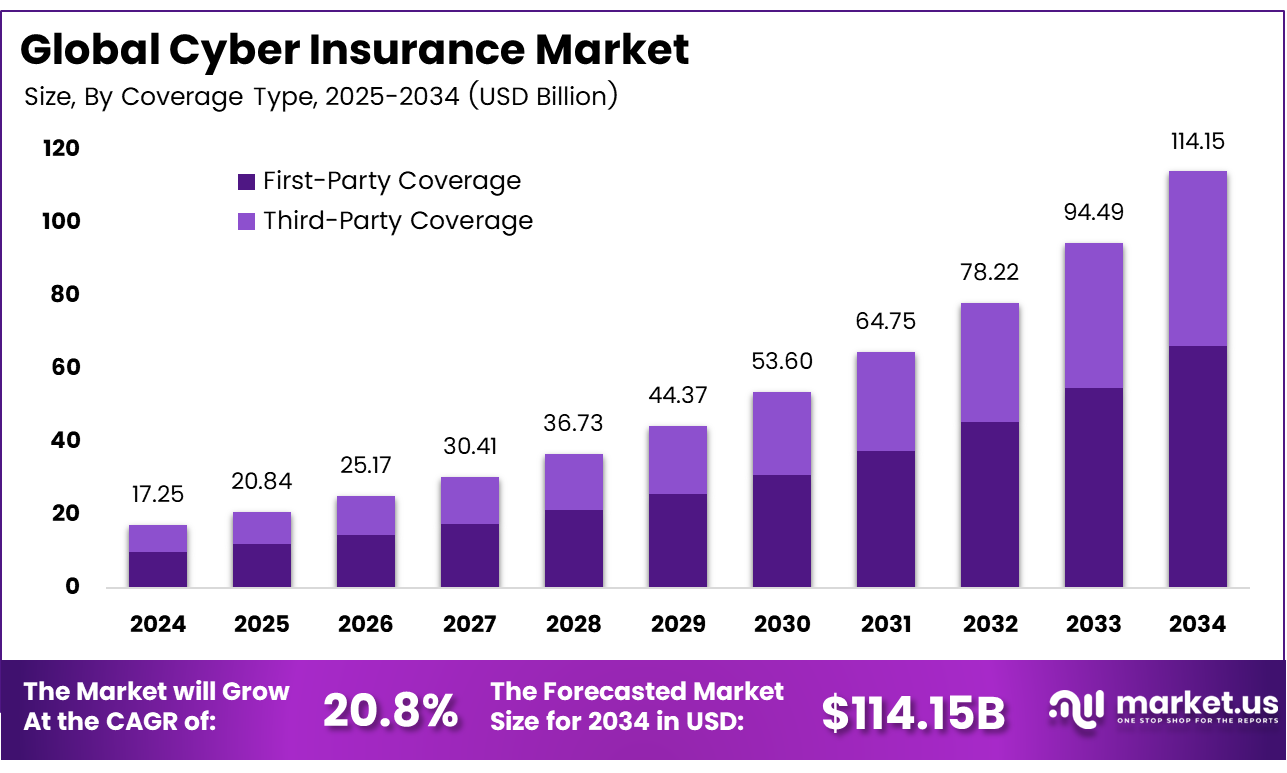

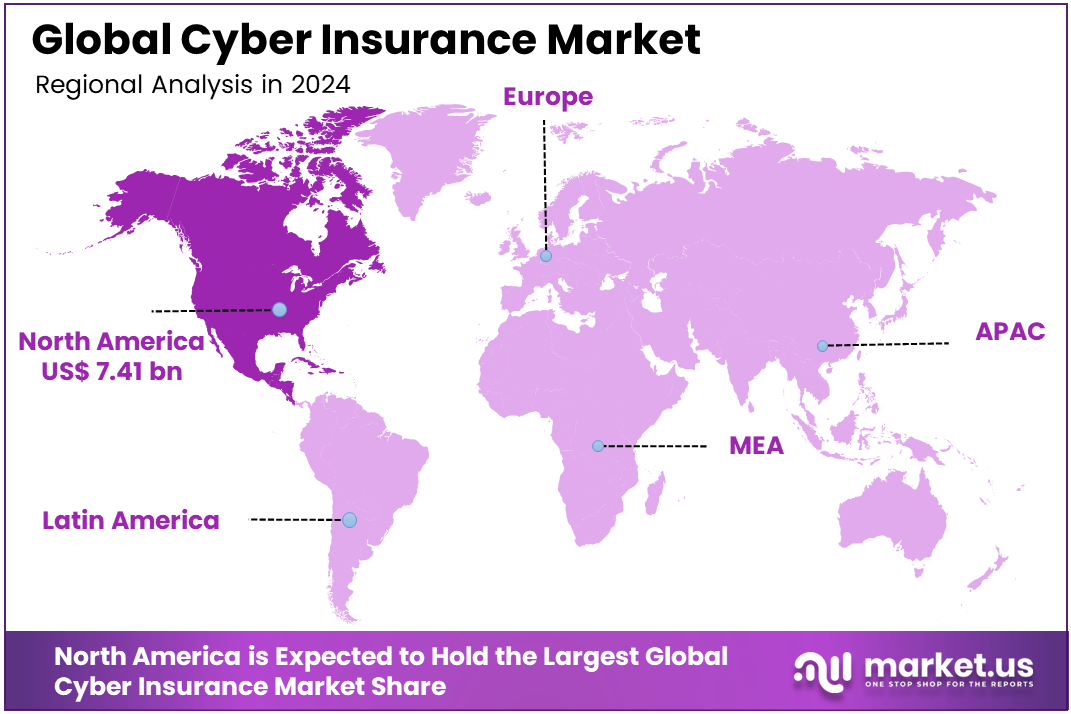

The Global Cyber Insurance Market size is expected to be worth around USD 114.15 billion by 2034, from USD 17.25 billion in 2024, growing at a CAGR of 20.8% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 43% share, holding USD 7.41 billion in revenue.

The market for cyber insurance is primarily driven by the rising frequency and sophistication of cyberattacks, such as ransomware, data breaches, and phishing. As businesses increasingly rely on digital infrastructures, the need to mitigate financial and reputational risks associated with cyber threats grows.

Additionally, regulatory pressures, such as GDPR and CCPA, compel organizations to adopt cyber insurance to comply with data protection laws. The growing awareness of cyber risks, alongside the expansion of digital transformation across industries, further accelerates the demand for comprehensive cyber insurance solutions to safeguard against evolving cyber threats.

For instance, in April 2025, Chubb partnered with SentinelOne to expedite access to cyber insurance for small and medium-sized businesses (SMBs). This collaboration aims to provide SMBs with streamlined access to affordable cyber insurance, coupled with advanced cybersecurity solutions.

Scope and Forecast

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 17.25 Bn |

| Forecast Revenue (2034) | USD 114.15 Bn |

| CAGR (2025-2034) | 20.8% |

| Largest market in 2024 | North America [43% market share] |

Key Takeaways

- In 2024, the First-Party Coverage segment held a dominant market position, capturing a 58% share of the Global Cyber Insurance Market.

- In 2024, the Large Enterprises segment held a dominant market position, capturing a 66% share of the Global Cyber Insurance Market.

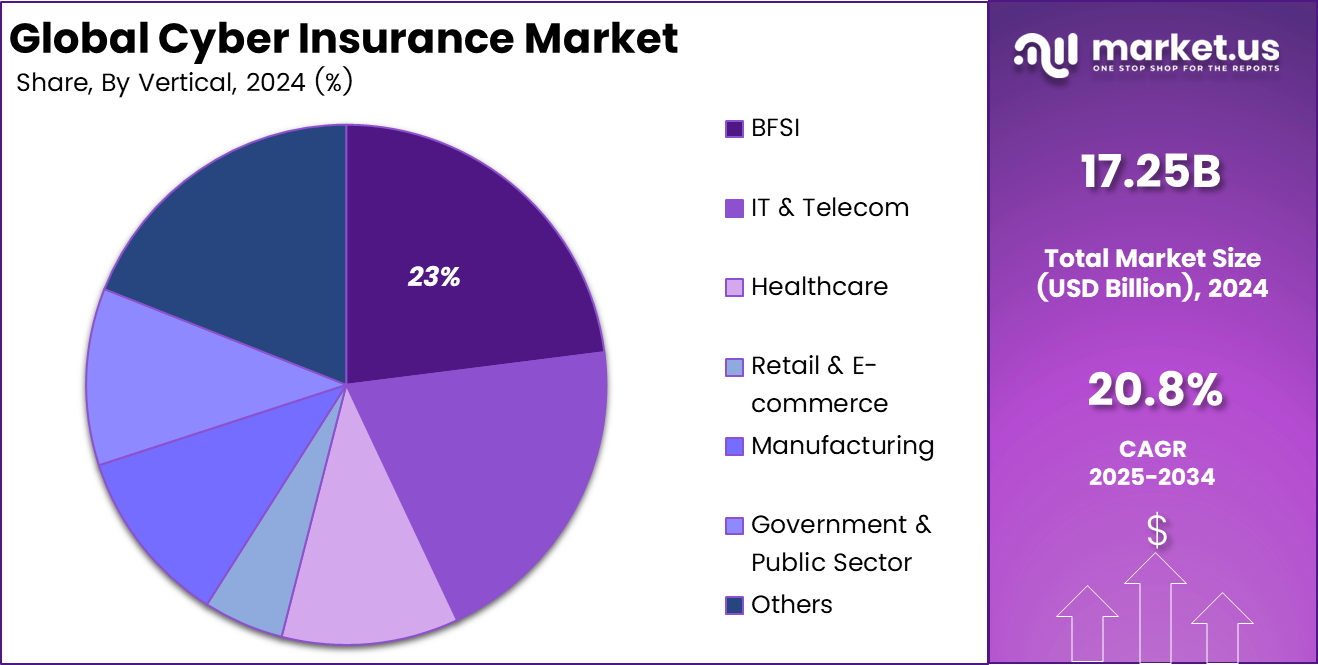

- In 2024, the BFSI segment held a dominant market position, capturing a 23% share of the Global Cyber Insurance Market.

- In 2024, the Brokers & Agents segment held a dominant market position, capturing a 40% share of the Global Cyber Insurance Market.

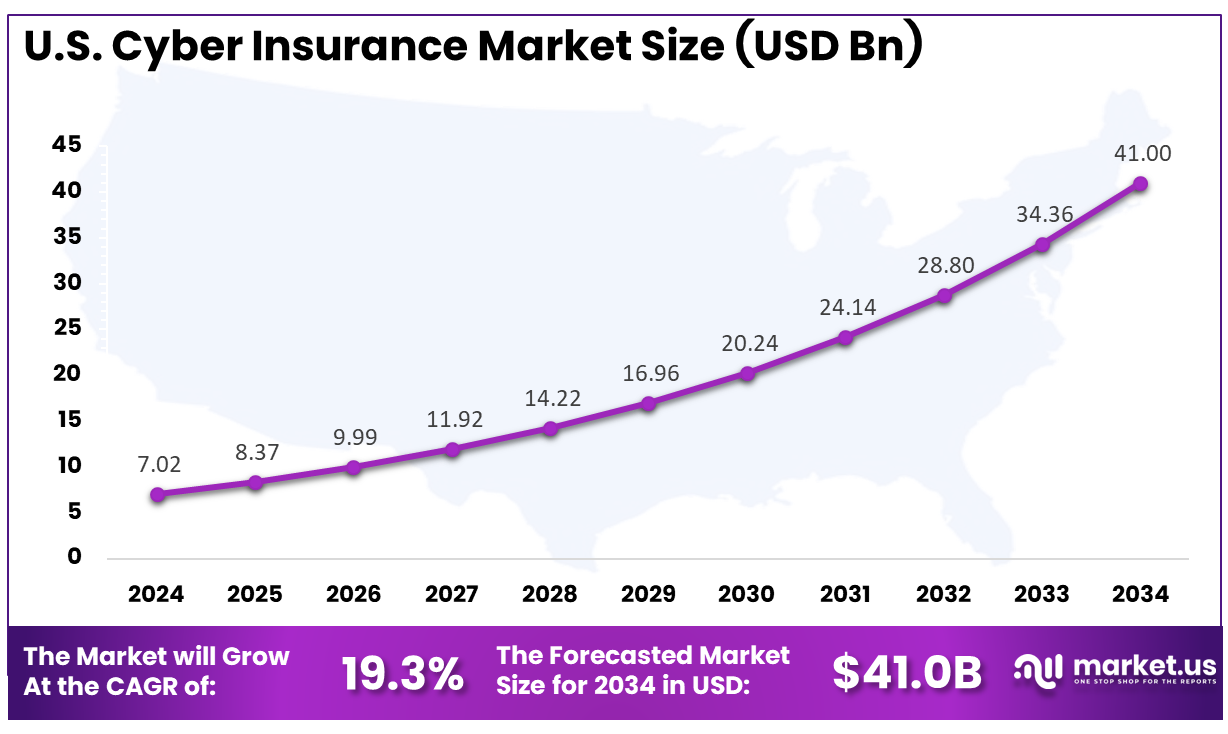

- The U.S. Cyber Insurance Market was valued at USD 7.02 Billion in 2024, with a robust CAGR of 19.3%.

- In 2024, North America held a dominant market position in the Global Cyber Insurance Market, capturing more than a 43% share.

Regional Analysis

In 2024, North America held a dominant market position in the Global Cyber Insurance Market, capturing more than a 43% share, holding USD 7.41 billion in revenue. North America leads the market due to its advanced digital infrastructure, widespread adoption of emerging technologies, and a high frequency of cyberattacks. The region hosts numerous businesses in industries like finance, healthcare, and technology, all of which are particularly vulnerable to cyber risks. Furthermore, stringent regulations like the CCPA and heightened awareness of cyber threats have significantly increased demand for comprehensive cyber insurance, reinforcing North America’s dominant position in the market.

For instance, in April 2025, AXA XL extended its cyber insurance offerings to small and midsize businesses (SMEs) in North America with a new strategic appointment. This move aims to address the increasing demand for cyber coverage among SMEs, a sector that has been increasingly vulnerable to cyberattacks.

U.S. Cyber Insurance Market Size

The market for Cyber Insurance within the U.S. is growing tremendously and is currently valued at USD 7.02 billion; the market has a projected CAGR of 19.3%. The market is expanding rapidly due to the rise in sophisticated cyberattacks, tougher regulations, and growing awareness of cyber risks among businesses. As industries such as healthcare, finance, and retail embrace digital transformation, the need for effective cyber risk management has become critical. Furthermore, regulations like GDPR and CCPA are driving companies to secure insurance coverage to manage compliance risks. This combination of factors is fueling the rapid growth of the cyber insurance market across sectors.

For instance, in April 2025, Munich Re highlighted the untapped potential in the $15.3 billion U.S. cyber insurance market, driven by rising cyber threats. The U.S. remains the market leader due to its advanced digital infrastructure and increasing cyberattacks. Munich Re expects growing demand for comprehensive cyber insurance solutions as businesses face heightened risks, offering significant opportunities for insurers to expand and address emerging vulnerabilities.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Coverage Type Analysis

In 2024, the First-Party Coverage segment held a dominant market position, capturing a 58% share of the Global Cyber Insurance Market. The dominance of the segment is driven by the rising frequency of direct cyberattacks, such as data breaches, ransomware, and system outages. This coverage offers immediate financial support, covering recovery costs, legal fees, and reputational damage.

As cyber threats evolve, businesses are prioritizing first-party coverage to mitigate financial risks and minimize operational disruptions. The increasing frequency and financial consequences of cyberattacks have made first-party protection crucial for safeguarding digital assets, fueling higher demand for comprehensive cyber insurance policies globally.

For instance, in November 2024, Parametrix launched a new cyber insurance solution specifically designed to address digital interruption, enhancing first-party coverage for businesses. This innovative offering focuses on providing immediate financial support to organizations facing operational disruptions caused by cyberattacks, such as ransomware or system outages.

Organization Size Analysis

In 2024, the Large Enterprises segment held a dominant market position, capturing a 66% share of the Global Cyber Insurance Market. The demand in this sector has been driven primarily by the increasing complexity and scale of cyber threats targeting large organizations, along with their substantial digital infrastructures. To minimize potential money losses, companies must have complete cyber insurance, as they are more vulnerable to issues like data breaches, ransomware attacks, and the theft of ideas.

For instance, in October 2024, Beazley launched ‘Beazley Quantum’, a new cyber insurance consortium designed to provide comprehensive coverage for large corporations, offering limits up to $100 million. This initiative enhances Beazley’s cyber insurance capabilities, addressing the full spectrum of risks faced by organizations in sectors like finance and technology.

Vertical Analysis

In 2024, the BFSI segment held a dominant market position, capturing a 23% share of the Global Cyber Insurance Market. The dominance is due to its high vulnerability to cyber threats, such as data breaches, fraud, and ransomware, in the BFSI industry. Handling sensitive customer information and financial transactions makes it a prime target for cyberattacks. To safeguard against financial losses, regulatory penalties, and reputational harm, BFSI firms are increasingly investing in cyber insurance.

For instance, in June 2025, WireX Systems and Brown & Brown announced a strategic collaboration aimed at advancing cyber risk management and improving insurance outcomes for the BFSI sector. The partnership combines WireX’s advanced cybersecurity solutions with Brown & Brown’s expertise in cyber insurance to offer tailored risk management services to financial institutions.

Distribution Channel Analysis

In 2024, the Brokers & Agents segment held a dominant market position, capturing a 40% share of the Global Cyber Insurance Market. This dominance is attributed to brokers and agents’ crucial role in helping businesses navigate the complexities of cyber insurance policies. Due to their expertise in identifying risks, providing tailored insurance options, and supporting businesses with the necessary coverage, they have become indispensable links for those seeking appropriate protection. Furthermore, brokers and agents provide valuable insights into emerging risks, making them essential in the growing cyber insurance industry.

For instance, in December 2024, CyberCube partnered with St. Andrews Insurance Brokers to enhance the cyber insurance offerings for businesses. This collaboration aims to leverage CyberCube’s advanced data analytics and risk modeling tools to provide more accurate cyber risk assessments for clients.

Key Market Segments

By Coverage Type

- First-Party Coverage

- Third-Party Coverage

By Organization Size

- Large Enterprises

- SMEs

By Vertical

- BFSI

- IT & Telecom

- Healthcare

- Retail & E-commerce

- Manufacturing

- Government & Public Sector

- Others

By Distribution Channel

- Direct Sales

- Brokers & Agents

- Bancassurance

- Digital Platforms

Latest Trends

Insurers are increasingly adopting advanced technologies such as artificial intelligence (AI), machine learning, and data analytics to refine their cyber insurance offerings. These technologies enhance risk assessment and pricing models by enabling insurers to analyze vast amounts of data in real time, leading to more accurate underwriting. Additionally, AI and machine learning help optimize claims management by detecting fraud, predicting future risks, and streamlining claims processes. This integration not only improves operational efficiency but also strengthens the overall reliability of the insurance market.

For instance, in April 2025, Cork, a cybersecurity firm, launched an AI-powered tool designed to quickly analyze and assess cyber insurance policies. This innovative tool helps businesses understand the terms and coverage of their policies more efficiently, ensuring they are adequately protected against emerging cyber threats.

Market Dynamics

Drivers - Regulatory Compliance and Legal Mandates

As GDPR and CCPA become more stringent, companies in sectors such as healthcare, finance, and essential services are increasingly turning to cyber insurance to ensure compliance with legal requirements. Companies benefit from cyber insurance to safeguard themselves against financial losses caused by data leaks, such as fines and legal costs, or reputational harm. The implementation of these laws is leading to a surge in the demand for specialized insurance plans, which help businesses stay protected from shifting legal regulations.

For instance, in July 2025, BlueClone Networks launched advanced cyber insurance and compliance assurance services aimed at helping businesses mitigate risks and meet regulatory requirements. The new services address the increasing pressure on organizations to comply with stringent regulations, such as GDPR and CCPA, which are driving demand for cyber insurance.

Restraint - High Premiums and Pricing Uncertainty

The high cost of cyber insurance premiums remains a significant barrier, especially for small and medium-sized enterprises (SMEs). Insurance companies are beginning to set prices based on factors such as the size of a company, cyber risks, and past claims history. The lack of clarity in the calculation process makes it difficult for businesses to predict what will happen. This unpredictability in costs often leads businesses to reconsider their insurance options, limiting widespread adoption and making it difficult for SMEs to afford comprehensive cyber coverage.

For instance, in July 2022, the GAO highlighted that rising cyber threats have led to increased premiums and reduced availability in the cyber insurance market. Insurers are grappling with the unpredictable nature of cyber risks, making it challenging to set stable pricing models. This uncertainty is particularly burdensome for small and medium-sized businesses, which face higher costs and limited access to coverage.

Opportunities - Development of Tailored Insurance Products

The increasing complexity of cyber threats presents insurance companies with an opportunity to develop more targeted cyber insurance solutions for diverse industries. Insurance companies can adapt their insurance policies to meet specific needs in areas like healthcare, financial technology, and essential services. Personalized insurance plans facilitate risk reduction, enhance coverage options, increase choice, and establish stronger connections between insurers and customers seeking more comprehensive protection.

For instance, in January 2025, Vouch introduced Corix, a Managing General Agent (MGA) designed to empower brokers with tailored cyber insurance products. Corix aims to address the evolving needs of businesses by offering customizable coverage options that cater to the unique cyber risks faced by different industries. By providing brokers with more flexible solutions and streamlined processes, Corix is set to enhance accessibility to cyber insurance, making it easier for organizations to secure comprehensive protection.

Challenges -Fraudulent Claims and Cybersecurity Gaps

Fraudulent claims pose a significant challenge to the integrity of the cyber insurance market, especially as cyber incidents become increasingly complex. Underreporting or exaggerating claims can inflate costs and undermine the claims process. Furthermore, many policyholders do not have adequate cybersecurity measures in place, leading to higher-than-anticipated claims. In addition to the safety vulnerabilities, insurance companies are also unable to continue operating as they become overwhelmed, making it necessary to implement better risk management and verification processes.

For instance, in March 2025, a nationwide cybersecurity drill revealed significant gaps in cybersecurity awareness, with 17% of employees falling for phishing scams daily. This highlights a major challenge for the cyber insurance market, as businesses continue to face lapses in security measures. The lack of robust cybersecurity practices increases the frequency of fraudulent claims and exposes organizations to greater risk.

Key Players Analysis

One of the leading players in the market, in July 2025, Zurich Insurance announced the acquisition of BOXX Insurance, a Canadian-based cyber insurance and risk management insurtech. This strategic acquisition strengthens Zurich’s cyber insurance portfolio and enhances its ability to provide tailored solutions for small and medium-sized businesses (SMBs) globally. The move is part of Zurich’s ongoing efforts to expand its cyber insurance offerings and improve access to affordable, comprehensive coverage for businesses facing growing cyber risks, further solidifying its presence in the evolving cyber insurance market.

Top Key Players in the Market

- AIG (American International Group)

- Chubb Ltd.

- AXA XL (AXA Group)

- Munich Re

- Beazley Group

- Zurich Insurance Group

- Hiscox Ltd.

- Allianz SE

- CNA Financial Corporation

- Coalition Inc.

- Others

Recent Developments

- In October 2024, AXA XL unveiled a new cyber insurance endorsement aimed at helping businesses manage emerging risks associated with Generative AI (Gen AI). This coverage extension addresses specific threats related to data poisoning, compliance challenges, and other risks associated with the growing use of AI technologies in business operations.

- In May 2025, Zurich Insurance (Hong Kong) launched “CyberSide,” a personal cyber insurance solution designed to offer comprehensive protection for individuals and families against the rising threat of cyberattacks. The product integrates both preventative technology and coverage for cyber risks, addressing issues like online fraud, identity theft, and data breaches.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 17.25 Billion |

| Forecast Revenue (2034) | USD 114.15 Billion |

| CAGR (2025-2034) | 20.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Coverage Type (First-Party Coverage, Third-Party Coverage), By Organization Size (Large Enterprises, SMEs), By Vertical (BFSI, IT & Telecom, Healthcare, Retail & E-commerce, Manufacturing, Government & Public Sector, Others), By Distribution Channel (Direct Sales, Brokers & Agents, Bancassurance, Digital Platforms) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | AIG (American International Group), Chubb Ltd., AXA XL (AXA Group), Munich Re, Beazley Group, Zurich Insurance Group, Hiscox Ltd., Allianz SE, CNA Financial Corporation, Coalition Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |