Global Wine Packaging Market Size, Share, Growth Analysis, Packaging Type (Bottles, Cans, Bag-in-Box, Tetra Pak / Cartons, Pouches, Kegs, Others), Material Type (Glass, Plastic, Metal, Others), Wine Type (Red Wine, White Wine, Rosé Wine, Sparkling Wine, Fortified Wine, Others), Packaging Size (Standard, Small, Large, Bulk), Closure Type (Natural Cork, Synthetic Cork, Screw Cap, Crown Cap, Others), Distribution Channel (Offline Retail, Online Retail), Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 178666

- Number of Pages: 211

- Format:

-

keyboard_arrow_up

Quick Navigation

- Wine Packaging Market Overview

- Key Takeaways

- Packaging Type Analysis

- Material Type Analysis

- Wine Type Analysis

- Packaging Size Analysis

- Closure Type Analysis

- Distribution Channel Analysis

- Key Market Segments

- Drivers

- Restraints

- Growth Factors

- Emerging Trends

- Regional Analysis

- Key Regions and Countries

- Key Company Insights

- Recent Developments

- Report Scope

Wine Packaging Market Overview

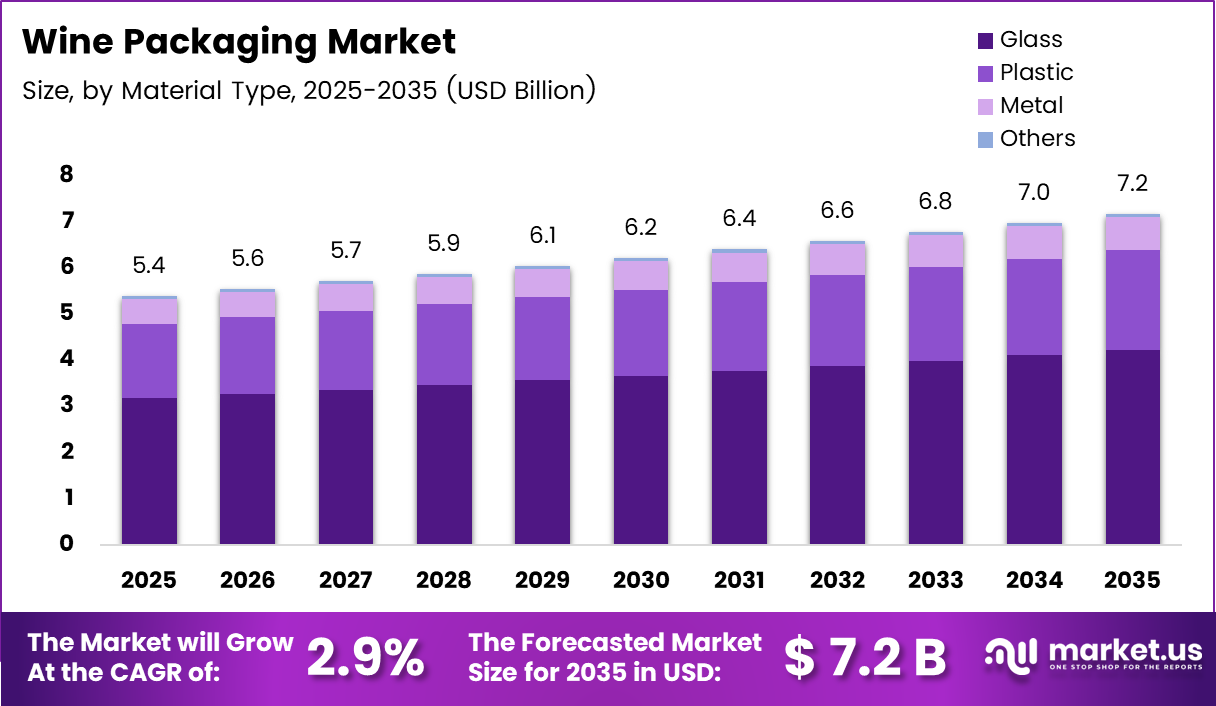

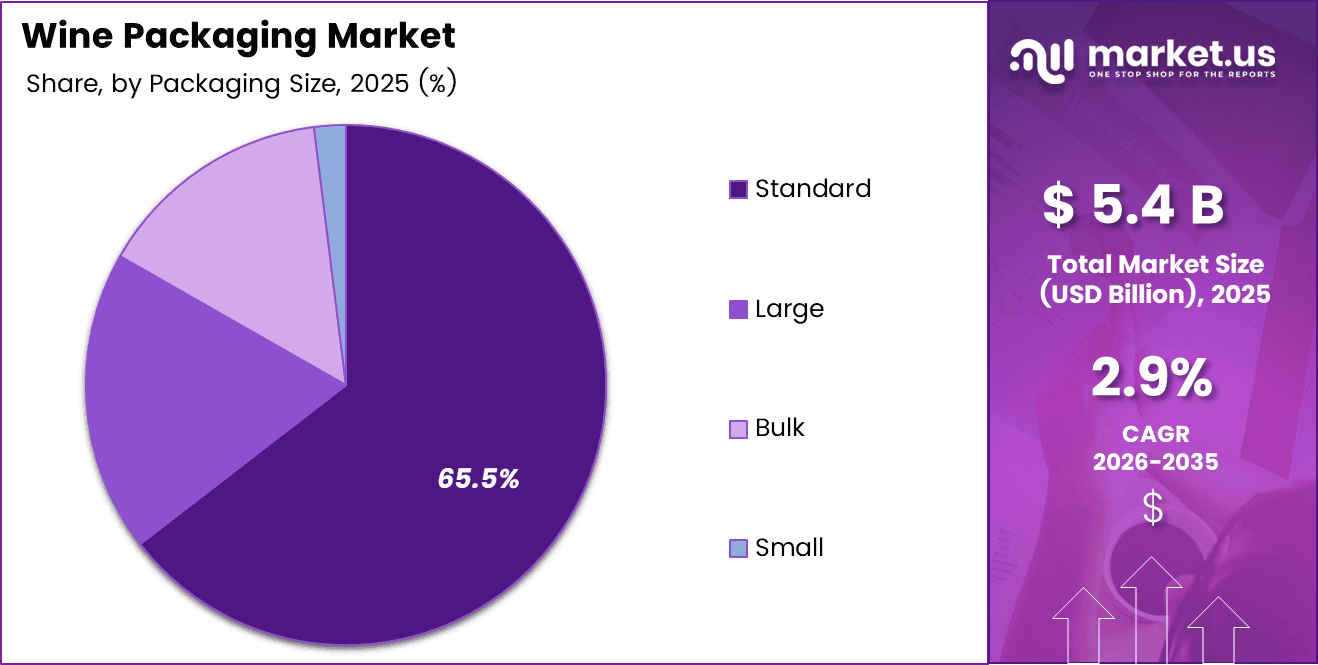

Global Wine Packaging Market size is expected to be worth around USD 35.4 Billion by 2035 from USD 7.2 Billion in 2025, growing at a CAGR of 2.9% during the forecast period 2026 to 2035.

The wine packaging market encompasses a broad range of materials, formats, and closure solutions used to store, protect, and present wine products. It includes glass bottles, cans, bag-in-box formats, pouches, and cartons. Moreover, closures such as natural cork, screw caps, and synthetic options are integral components of this market.

Wine packaging plays a critical role beyond simple containment. It directly influences shelf appeal, brand perception, and consumer purchasing decisions. Therefore, producers invest significantly in packaging design to differentiate their products in a highly competitive global market.

Growth in global wine consumption across both premium and mass segments is a key driver of this market. Additionally, the expansion of organized retail and wine e-commerce distribution channels has created new demand for durable, attractive, and transport-friendly packaging formats.

Governments across major wine-producing regions are introducing regulations around labeling, recycling, and material safety. Consequently, packaging manufacturers are adapting to meet compliance requirements while also aligning with broader sustainability mandates that encourage recyclable and eco-friendly solutions.

Sustainable packaging innovation is reshaping the industry. According to Smurfit Kappa, 69% of consumers say packaging should be paper-based, and 71% of customers want packaging that is easy to dispose of. These preferences are pushing brands toward lightweight and compostable formats.

Additionally, according to Smurfit Kappa, 59% of consumers prefer parcels that are easy to open without tools, and 74% want packaging that supports easy returns. These behavioral trends highlight the growing importance of consumer-centric design in wine packaging decisions.

Key Takeaways

- The global Wine Packaging Market is valued at USD 7.2 Billion in 2025 and is projected to reach USD 35.4 Billion by 2035.

- The market is growing at a CAGR of 2.9% during the forecast period 2026 to 2035.

- By Packaging Type, Bottles dominate with a 65.4% market share in 2025.

- By Material Type, Glass holds the leading position with a 58.9% share.

- By Wine Type, Red Wine accounts for the largest share at 55.4%.

- By Packaging Size, Standard size leads with a 65.5% share.

- By Closure Type, Natural Cork dominates with a 52.1% share.

- By Distribution Channel, Offline Retail holds an 80.8% share.

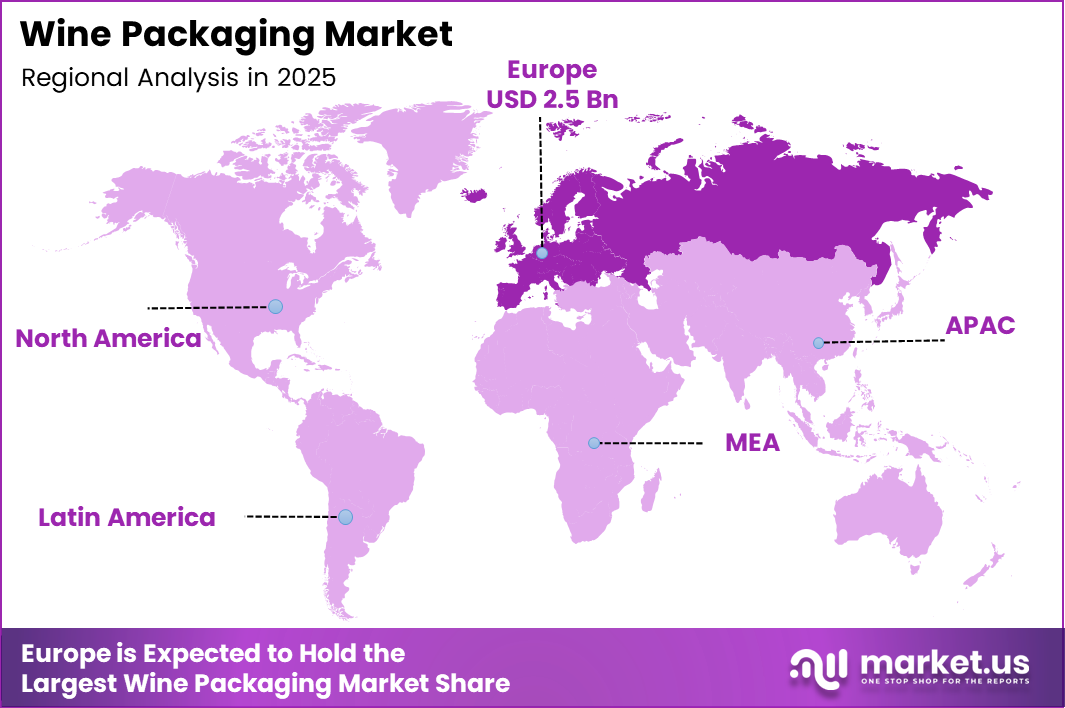

- Europe dominates the regional landscape with a 46.8% market share, valued at USD 2.5 Billion.

Packaging Type Analysis

Bottles dominate with 65.4% due to widespread consumer preference and established supply chain infrastructure.

In 2025, Bottles held a dominant market position in the Packaging Type segment of the Wine Packaging Market, with a 65.4% share. Bottles remain the most widely used format globally due to their strong association with wine quality and tradition. Their established supply chain infrastructure makes them the default choice for producers across all price segments.

Glass Bottles are the premium standard in wine packaging, preferred for their ability to preserve flavor and project a high-quality brand image. They dominate retail shelves and are deeply embedded in consumer expectations worldwide. Moreover, their full recyclability aligns with growing sustainability mandates across key wine markets.

Plastic (PET) Bottles serve the value-oriented and casual wine segment, offering a lightweight and cost-efficient alternative to glass. They are particularly popular in outdoor, travel, and single-serve consumption occasions. However, increasing environmental concerns are pushing producers to explore more sustainable material substitutions.

Cans are gaining rapid traction among younger consumers seeking convenience and portability in wine consumption. They are well-suited for on-the-go occasions and are expanding across retail and e-commerce channels. Additionally, their recyclability makes them an attractive option for eco-conscious brands.

Bag-in-Box is a popular format for bulk and casual wine consumption, offering extended shelf life after opening. It is cost-effective and easy to transport, making it widely used in households and foodservice settings. Furthermore, its paper-based outer structure supports sustainability goals for brands and retailers.

Tetra Pak / Cartons are seeing growing adoption in markets focused on sustainability and portability. They offer a lightweight, paper-based solution that appeals to environmentally conscious consumers. Their versatility in shape and size makes them suitable for both single-serve and multi-serve wine formats.

Pouches offer a lightweight and flexible packaging solution suited for outdoor, travel, and casual wine occasions. They are compact, shatterproof, and easy to dispose of after use. Moreover, advances in barrier technology are improving their ability to preserve wine quality over longer periods.

Kegs are widely used in hospitality, restaurant, and foodservice channels as a high-volume wine dispensing solution. They reduce packaging waste significantly compared to individual bottles and support cost efficiency in commercial settings. Additionally, their use is growing in wine bars and venues focused on sustainable service practices.

Others in this segment include emerging and regionally specific packaging formats that continue to evolve with market innovation. These formats often cater to niche consumer preferences or experimental brand positioning strategies. Consequently, they represent an area of ongoing development for packaging manufacturers seeking differentiation.

Material Type Analysis

Glass dominates with 58.9% due to its premium perception and superior preservation properties.

In 2025, Glass held a dominant market position in the Material Type segment of the Wine Packaging Market, with a 58.9% share. It remains the preferred material for wine packaging due to its ability to preserve flavor integrity and project a premium brand image. Moreover, its full recyclability aligns with sustainability expectations among producers and consumers globally.

Plastic materials, primarily PET, provide a lightweight and cost-efficient alternative for value-oriented wine categories. They are favored in casual consumption and single-serve formats where portability is a priority. However, tightening environmental regulations are prompting producers to reduce plastic use and explore greener material options.

Metal, primarily aluminum used in cans, is growing rapidly as a format for ready-to-drink and sparkling wine products. Its full recyclability and strong barrier properties make it an increasingly preferred sustainable choice. Additionally, the rising popularity of canned wine among younger consumers continues to drive demand for metal packaging.

Others in this category include paper-based composites, multi-material laminates, and bio-based alternatives gaining interest from eco-conscious brands. These materials are being explored as producers seek packaging innovations that reduce environmental impact. Consequently, investment in this segment is expected to grow as sustainability regulations tighten across major markets.

Wine Type Analysis

Red Wine dominates with 55.4% due to its global popularity and strong consumer demand across all price segments.

In 2025, Red Wine held a dominant market position in the Wine Type segment of the Wine Packaging Market, with a 55.4% share. It consistently leads global consumption, supported by deep cultural traditions and a broad range of accessible price points. Consequently, packaging demand for red wine remains the highest across all categories and geographies.

White Wine holds the second-largest share and is particularly strong across European and North American markets. It is commonly packaged in standard glass bottles and is increasingly appearing in cans and bag-in-box formats. Moreover, its broad consumer appeal supports steady packaging demand across both premium and entry-level segments.

Rosé Wine is experiencing steady growth, driven by younger demographics and strong seasonal consumption trends globally. It is gaining shelf space in retail and on-trade channels across multiple regions. Additionally, its visual appeal makes it a strong candidate for premium and design-forward packaging formats.

Sparkling Wine requires specialized packaging including thicker glass and wire-caged corks to safely manage carbonation pressure. This technical requirement increases packaging complexity and cost compared to still wine formats. Therefore, suppliers serving this segment must maintain strict quality and engineering standards.

Fortified Wine demands airtight and durable closure solutions to maintain quality and stability over extended storage periods. It is typically packaged in heavier glass bottles with premium closures to reflect its higher price positioning. Consequently, packaging suppliers must deliver both functional reliability and aesthetic excellence for this category.

Others represent regional and niche wine varieties that contribute incrementally to overall packaging demand. These include orange wines, natural wines, and locally produced varieties expanding in emerging markets. However, their growing popularity is gradually creating new packaging customization opportunities for producers and suppliers alike.

Packaging Size Analysis

Standard size dominates with 65.5% due to universal consumer acceptance and widespread retail availability.

In 2025, Standard packaging size held a dominant market position in the Packaging Size segment of the Wine Packaging Market, with a 65.5% share. The standard 750ml format is the global benchmark accepted across all retail, hospitality, and gifting channels. It remains the default choice for the vast majority of wine producers worldwide.

Small packaging formats, including 187ml and 250ml sizes, are gaining popularity for single-serve occasions, airline service, and trial purchases. They reduce waste and align with on-the-go consumption patterns increasingly common among urban consumers. Moreover, small formats support premiumization strategies when paired with high-quality closures and refined label design.

Large formats such as magnums and double magnums appeal to special occasions, celebrations, and the gifting market. They command higher price points and are often associated with luxury wine experiences. Additionally, their visual impact at retail and on dining tables makes them a preferred choice for premium brand positioning.

Bulk packaging is used primarily in hospitality, commercial foodservice, and institutional channels where cost efficiency and high volume are the priority. It typically takes the form of large bag-in-box or kegs suited for on-premise wine service. Consequently, this segment plays an important role in reducing per-unit packaging costs for high-volume operators.

Closure Type Analysis

Natural Cork dominates with 52.1% due to its traditional association with premium wine quality and aging potential.

In 2025, Natural Cork held a dominant market position in the Closure Type segment of the Wine Packaging Market, with a 52.1% share. It is deeply embedded in wine culture and remains the preferred closure for premium and aged wines. Its micro-oxygenation properties support wine development over time, making it both a functional and symbolic choice.

Synthetic Cork offers a cost-effective and consistent alternative that eliminates the risk of cork taint found in natural cork. It is widely adopted across entry-level and mid-range wine categories globally. Moreover, advances in material science are improving the performance and sustainability profile of synthetic cork options.

Screw Caps are increasingly popular, particularly in New World wine markets such as Australia, New Zealand, and the United States. They provide a reliable airtight seal and are favored for wines intended for near-term consumption. Additionally, their ease of use and tamper-evident properties are driving acceptance among younger and convenience-focused consumers.

Crown Caps are predominantly used for sparkling wines and are also popular among natural and pét-nat wine producers seeking a casual aesthetic. They provide a secure seal and are cost-efficient for high-volume production. Consequently, their use is expanding beyond traditional applications into boutique and artisan wine segments.

Others include glass closures and emerging alternatives gaining traction in premium boutique wine segments. These options offer a distinctive and modern aesthetic that appeals to design-conscious producers. Furthermore, their strong airtight properties and reusability are attracting interest from producers prioritizing both quality and sustainability.

Distribution Channel Analysis

Offline Retail dominates with 80.8% due to the predominance of in-store wine purchasing behavior globally.

In 2025, Offline Retail held a dominant market position in the Distribution Channel segment of the Wine Packaging Market, with an 80.8% share. Physical retail remains the primary channel for wine sales globally, spanning supermarkets, specialty wine stores, and duty-free outlets. Consumers continue to prefer in-store selection for its tactile experience and immediate product availability.

Online Retail is the fastest-growing channel, accelerated by shifting consumer habits and rapid digital commerce expansion. E-commerce platforms and direct-to-consumer winery websites are capturing a growing share of wine purchases globally. Consequently, packaging must now meet higher durability standards to withstand shipping and last-mile delivery without compromising presentation quality.

Key Market Segments

Packaging Type

- Bottles (Glass Bottles, Plastic (PET) Bottles)

- Cans

- Bag-in-Box

- Tetra Pak / Cartons

- Pouches

- Kegs

- Others

Material Type

- Glass

- Plastic

- Metal

- Others

Wine Type

- Red Wine

- White Wine

- Rosé Wine

- Sparkling Wine

- Fortified Wine

- Others

Packaging Size

- Standard

- Small

- Large

- Bulk

Closure Type

- Natural Cork

- Synthetic Cork

- Screw Cap

- Crown Cap

- Others

Distribution Channel

- Offline Retail

- Online Retail

Drivers

Rising Wine Consumption and Brand Differentiation Needs Drive Wine Packaging Market Growth

Global wine consumption is rising steadily across both premium and mass market segments. As more consumers explore wine globally, demand for varied and well-designed packaging increases. Producers require packaging solutions that maintain product quality while meeting the diverse expectations of consumers across different income levels and regional markets.

Packaging has become a powerful brand differentiation tool in the wine industry. Attractive label design, closure type, and bottle shape directly influence purchasing decisions at the point of sale. Moreover, as retail shelves grow more competitive, producers are investing more in distinctive packaging to capture consumer attention and reinforce their brand identity.

The expansion of organized retail and e-commerce wine distribution channels is also fueling packaging demand. Online retail requires durable and protective formats to prevent breakage during transit. Additionally, growth in modern retail formats creates opportunities for innovative packaging that supports shelf display, marketing communication, and consumer convenience simultaneously.

Restraints

High Material Costs and Strict Regulatory Requirements Restrain Wine Packaging Market Growth

Premium and custom wine packaging materials, particularly high-quality glass and specialty closures such as natural cork, carry significant costs. Small and mid-size wine producers often struggle to absorb these expenses while maintaining competitive pricing. Consequently, cost pressures limit their ability to invest in advanced packaging formats or premium design enhancements.

Strict alcohol packaging and labeling regulations vary significantly across regions and markets. Producers and packaging suppliers must comply with rules covering material safety, label content, language requirements, and environmental standards. Therefore, navigating multi-jurisdictional compliance adds complexity and cost to packaging operations, particularly for brands selling across international markets simultaneously.

Regulatory changes can also disrupt established supply chains. When new rules mandate material substitutions or labeling updates, producers face additional time and financial investments to adapt. Moreover, the lack of harmonized global standards means that packaging designed for one market may require modification before it can be used in another, increasing overall operational burden.

Growth Factors

Sustainability Adoption and Emerging Market Expansion Accelerate Wine Packaging Market Growth

Rising adoption of sustainable and eco-friendly wine packaging solutions presents a significant growth opportunity. Brands are increasingly switching to recyclable glass, paper-based materials, and biodegradable closures. Moreover, consumer demand for environmentally responsible packaging is pushing producers to innovate, creating new product categories and expanding the addressable market for sustainable packaging suppliers.

Demand for lightweight packaging is growing as producers seek to reduce transportation costs and carbon emissions. Lighter formats such as PET bottles, pouches, and bag-in-box reduce shipping weight significantly. Consequently, logistics savings are encouraging broader adoption, particularly among value-oriented brands and exporters managing long-distance supply chains across multiple international markets.

The growth of ready-to-drink and single-serve wine formats is opening new packaging avenues. Cans, small pouches, and compact cartons are well-suited to these formats. Additionally, expanding wine production in emerging markets across Asia, Africa, and Latin America is increasing local packaging demand, creating new revenue streams for global and regional packaging manufacturers.

Emerging Trends

Alternative Formats and Smart Packaging Innovation Reshape the Wine Packaging Market

A significant shift toward alternative packaging formats such as cans and bag-in-box is transforming the wine packaging landscape. These formats appeal to younger, convenience-driven consumers and are gaining retail shelf space rapidly. Moreover, their lower environmental footprint compared to traditional glass aligns with the sustainability values increasingly prioritized by both producers and consumers.

Increasing use of recyclable glass and paper-based closures reflects the industry’s commitment to circular economy principles. Producers are replacing traditional plastic elements with compostable or fully recyclable alternatives. Consequently, innovations in closure technology, including paper-pulp corks and plant-based synthetic options, are being adopted across a growing range of premium and mid-tier wine brands.

Integration of smart labels and QR codes is enabling direct consumer engagement from the packaging itself. Producers are using these technologies to share product stories, sustainability credentials, and food pairing suggestions. Additionally, minimalist and premium aesthetic design trends are influencing label and bottle formats, as brands seek elegant, modern packaging that resonates with discerning consumers globally.

Regional Analysis

Europe Dominates the Wine Packaging Market with a Market Share of 46.8%, Valued at USD 2.5 Billion

Europe leads the global Wine Packaging Market with a dominant share of 46.8%, valued at USD 2.5 Billion in 2025. The region’s dominance is driven by its status as the world’s largest wine-producing and consuming region, home to established industries in France, Italy, Spain, and Germany. Moreover, strong retail infrastructure and premium packaging demand reinforce Europe’s leadership position.

North America Wine Packaging Market Trends

North America represents a significant and growing market for wine packaging, led by the United States. Strong consumer demand for premium wines and the rapid growth of e-commerce wine retail are driving packaging innovation. Additionally, the popularity of canned and ready-to-drink wine formats is accelerating adoption of alternative packaging materials across the region.

Asia Pacific Wine Packaging Market Trends

Asia Pacific is emerging as a high-growth region in the wine packaging market, driven by rising wine consumption in China, Australia, and India. Growing middle-class populations and increasing exposure to Western lifestyle trends are fueling demand. Consequently, both imported and domestically produced wines are driving packaging demand across premium and entry-level categories in the region.

Latin America Wine Packaging Market Trends

Latin America, led by Brazil, Argentina, and Chile, presents solid growth opportunities in wine packaging. The region is a significant wine producer with growing export activity, requiring robust and export-grade packaging solutions. Furthermore, rising domestic wine consumption and expanding modern retail channels are creating new demand for diverse packaging formats and closure types.

Middle East and Africa Wine Packaging Market Trends

The Middle East and Africa region shows moderate but expanding participation in the wine packaging market, primarily driven by South Africa’s established wine industry. Export-oriented production requires durable and internationally compliant packaging solutions. Additionally, growing hospitality and tourism sectors in certain GCC countries are creating incremental demand for premium wine packaging formats.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Owens-Illinois Inc. (O-I) is a global leader in glass container manufacturing, serving the wine industry across multiple continents. The company’s extensive production network and strong relationships with major wine producers position it as a critical supply chain partner. Its focus on lightweighting and sustainable glass innovation aligns well with current packaging trends and regulatory requirements.

Verallia SA is one of Europe’s largest producers of glass bottles and jars for the wine and spirits sector. The company operates numerous facilities across Europe and South America, enabling regional supply flexibility. Moreover, Verallia’s ongoing investment in furnace efficiency and recycled glass content positions it as a sustainability leader within the premium wine packaging segment.

Ardagh Group SA operates across both glass and metal packaging, giving it a diversified presence in the wine packaging market. Its glass division supplies bottles to leading wine producers, while its metal segment is benefiting from rising demand for canned wine products. Additionally, the group’s broad geographic footprint supports its capacity to serve producers across multiple international markets.

Amcor plc brings a flexible and diversified packaging portfolio to the wine market, including pouches, closures, and specialty films. The company’s strong focus on recyclable and responsible packaging aligns with global sustainability mandates. Consequently, Amcor is well-positioned to capture growing demand from wine producers seeking alternative formats that balance cost efficiency, performance, and environmental responsibility.

Key Players

- Owens-Illinois Inc. (O-I)

- Verallia SA

- Ardagh Group SA

- Saverglass SAS

- Vetropack Holding AG

- BA Glass Group

- Consol Glass Pty Ltd

- Guala Closures Group

- Amorim Cork, S.A.

- Vinventions LLC (Nomacorc)

- Amcor plc

- Ball Corporation

- TricorBraun Inc.

- SIG Combibloc Group AG

- Sealed Air

- Other Key Players

Recent Developments

- August 2025 – The Wine Group announced its acquisition of wine brands and production facilities from Constellation Brands, marking a significant consolidation move in the global wine industry. This transaction is expected to expand The Wine Group’s production capacity and strengthen its portfolio across multiple price segments.

- June 2025 – Berlin Packaging, recognized as the world’s largest Hybrid Packaging Supplier, completed its acquisition of Sarom Packaging and Romgallia. This strategic move enhances Berlin Packaging’s European footprint and broadens its product offering for wine and beverage packaging clients across the region.

Report Scope

Report Features Description Market Value (2025) USD 7.2 Billion Forecast Revenue (2035) USD 35.4 Billion CAGR (2026-2035) 2.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered Packaging Type (Bottles, Cans, Bag-in-Box, Tetra Pak / Cartons, Pouches, Kegs, Others), Material Type (Glass, Plastic, Metal, Others), Wine Type (Red Wine, White Wine, Rosé Wine, Sparkling Wine, Fortified Wine, Others), Packaging Size (Standard, Small, Large, Bulk), Closure Type (Natural Cork, Synthetic Cork, Screw Cap, Crown Cap, Others), Distribution Channel (Offline Retail, Online Retail) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Owens-Illinois Inc. (O-I), Verallia SA, Ardagh Group SA, Saverglass SAS, Vetropack Holding AG, BA Glass Group, Consol Glass Pty Ltd, Guala Closures Group, Amorim Cork S.A., Vinventions LLC (Nomacorc), Amcor plc, Ball Corporation, TricorBraun Inc., SIG Combibloc Group AG, Sealed Air, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Owens-Illinois Inc. (O-I)

- Verallia SA

- Ardagh Group SA

- Saverglass SAS

- Vetropack Holding AG

- BA Glass Group

- Consol Glass Pty Ltd

- Guala Closures Group

- Amorim Cork, S.A.

- Vinventions LLC (Nomacorc)

- Amcor plc

- Ball Corporation

- TricorBraun Inc.

- SIG Combibloc Group AG

- Sealed Air

- Other Key Players

Our Clients

- 178666

- Feb 2026