Global Weapon Release System Market Size, Share, Growth Analysis By Weapon Type (Missiles, Bombs, Torpedoes, Rocket), By Platform (Fighter Aircraft, Combat Support Aircraft, Helicopters, UAVs), By End User (OEM, Aftermarket), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Apr 2026

- Report ID: 183785

- Number of Pages: 339

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

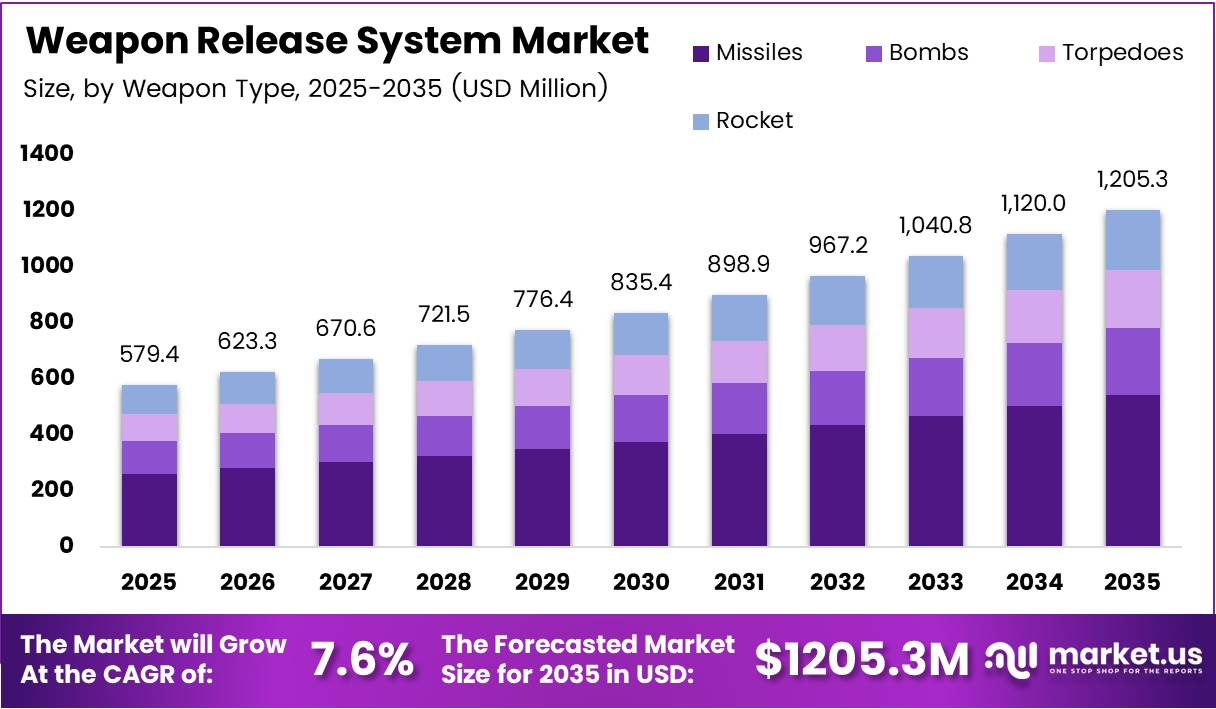

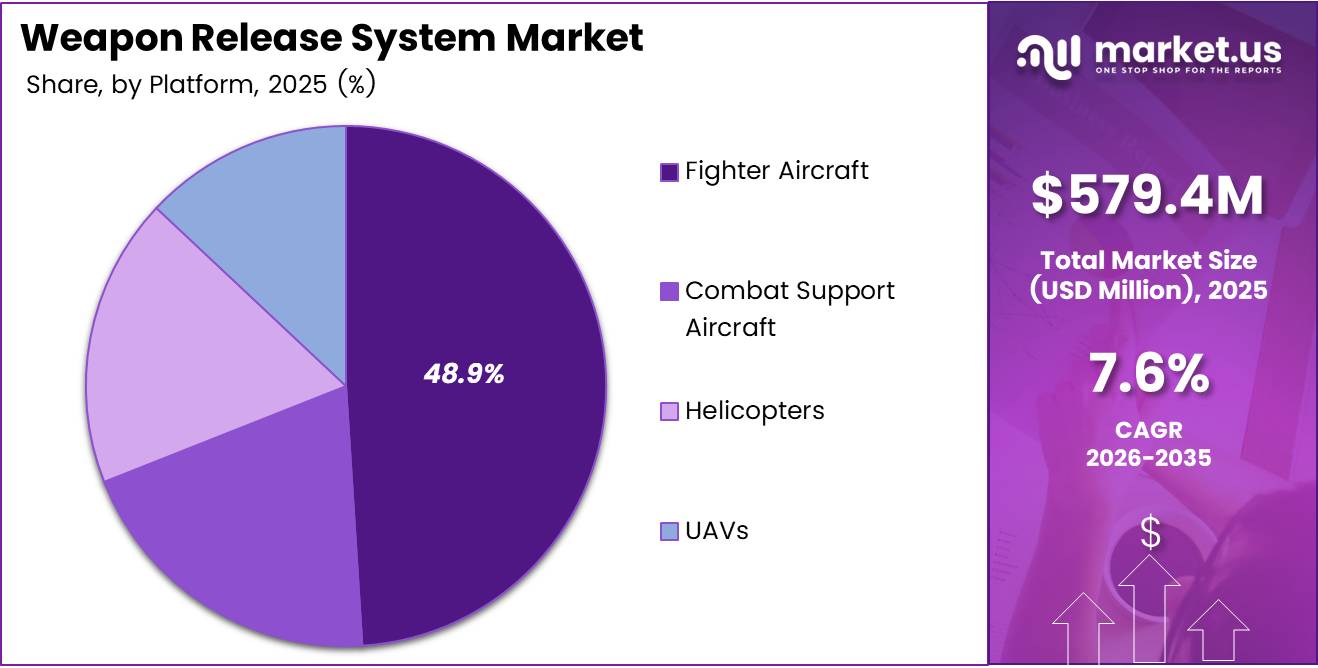

Global Weapon Release System Market size is expected to be worth around USD 1,205.3 Million by 2035 from USD 579.4 Million in 2025, growing at a CAGR of 7.6% during the forecast period 2026 to 2035.

Weapon release systems are the mechanical, electromechanical, and digital mechanisms that enable aircraft, helicopters, and UAVs to carry, manage, and deploy munitions. These systems include ejector racks, bomb release units, missile launchers, store management systems, and associated control interfaces. They connect directly to mission success, because a precision weapon is only as effective as the platform that releases it.

The market spans multiple platform types, from frontline fighter aircraft to combat support aircraft, rotary-wing platforms, and unmanned aerial vehicles. Each platform type places distinct mechanical, software, and certification demands on weapon release hardware. This diversity means vendors must maintain broad engineering capabilities rather than single-product solutions — a structural advantage for established defense contractors.

Military aircraft modernization programs across NATO and Indo-Pacific nations are the primary structural force behind this market’s expansion. Defense budgets in the United States, Europe, and Asia have committed to multi-decade platform upgrades, each requiring updated or new weapon release hardware. These procurement cycles create multi-year revenue visibility for qualified suppliers.

Precision strike capability has become the defining requirement of modern air combat doctrine. Guided bombs, smart missiles, and network-linked munitions each require release systems with tighter tolerances, digital interfaces, and real-time store management. This shift from dumb to smart munitions pushes the bill-of-materials complexity upward and raises the average contract value per aircraft system.

UAV proliferation is opening an entirely new procurement channel. Unmanned platforms require lighter, electrically actuated release mechanisms that differ substantially from traditional crewed-aircraft systems. This creates a parallel product development track and a new buyer category — both of which expand the total addressable market beyond legacy fleet upgrades.

According to the F-35 program data, the global fleet has surpassed one million cumulative flight hours with nearly 1,300 aircraft in service. This scale confirms that next-generation fighter procurement is moving from pilot program to mass deployment, directly driving replacement and new-install demand for compatible weapon release hardware across allied air forces.

In 2024, Lockheed Martin reported large U.S. Air Force and allied orders for JASSM and LRASM long-range precision munitions, driving additional demand for aircraft store management and release systems across multiple platforms. This signals that munitions procurement and release system demand move in lockstep — making munitions order trends a reliable leading indicator for this market.

Key Takeaways

- The global Weapon Release System Market was valued at USD 579.4 Million in 2025.

- The market is forecast to reach USD 1,205.3 Million by 2035, at a CAGR of 7.6%.

- By Weapon Type, Missiles led with a 44.8% share in 2025.

- By Platform, Fighter Aircraft dominated with a 48.9% share in 2025.

- By End User, OEM held the largest share at 69.1% in 2025.

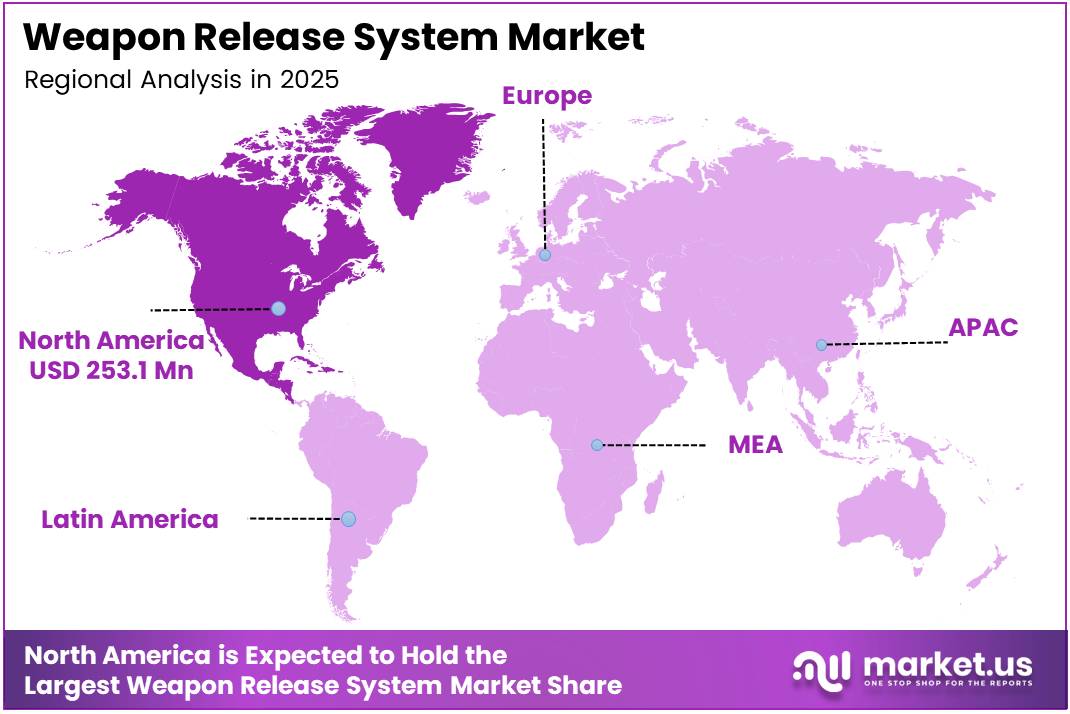

- North America was the dominant region with 43.70% market share, valued at USD 253.1 Million in 2025.

Product Analysis

Missiles dominate with 44.8% due to precision strike doctrine prioritization.

In 2025, Missiles held a dominant market position in the By Weapon Type segment of the Weapon Release System Market, with a 44.8% share. Air forces worldwide have shifted procurement toward guided missile systems because they reduce collateral risk and extend standoff range. This doctrinal shift directly increases the per-aircraft investment in missile launcher rails, ejection mechanisms, and store management software.

Bombs remain the most cost-effective weapon type for high-sortie close air support missions. Unguided and precision-guided bomb delivery systems require mechanically robust ejector racks capable of handling high release loads. However, the shift toward precision-guided munitions is steadily increasing the electronics content within bomb release hardware, raising unit value even as volume plateaus.

Torpedoes serve a specialized but strategically critical role in anti-submarine warfare platforms. Maritime patrol aircraft and naval helicopters require dedicated torpedo release mechanisms with water-entry sequencing and safe-separation logic. This niche demands specialized engineering, limiting competition and sustaining higher margin potential for qualified vendors.

Rockets are primarily deployed from rotary-wing platforms and close air support aircraft. Rocket launcher pods use relatively simpler release mechanisms, but integration with digital fire control systems has increased their complexity. Helicopter-based rocket systems are seeing renewed investment as armies modernize light attack platforms for asymmetric warfare environments.

Platform Analysis

Fighter Aircraft dominate with 48.9% due to concentrated high-value procurement cycles.

In 2025, Fighter Aircraft held a dominant market position in the By Platform segment of the Weapon Release System Market, with a 48.9% share. The F-35, Eurofighter, and Rafale programs each require sophisticated multi-station weapon management systems capable of handling mixed weapon loads. High unit cost and multi-decade service lives make fighter aircraft the most intensive per-platform buyers of release system hardware.

Combat Support Aircraft serve as force multipliers by delivering heavy payloads over extended ranges. Platforms such as the B-52 and A-10 require high-capacity multiple ejector racks and digital store management upgrades as part of service-life extension programs. Their lower procurement volumes are offset by the complexity and value of each system integration contract.

Helicopters represent a structurally distinct buyer segment driven by rotary-wing operational requirements. Attack helicopters and naval helicopters use lightweight, vibration-resistant release mechanisms for rockets, missiles, and torpedoes. Army modernization programs across Europe and Asia are generating steady replacement demand within this platform category.

UAVs are the fastest-growing platform segment, because they impose entirely different engineering constraints on weapon release hardware. Unmanned systems require electrically actuated, low-weight mechanisms with remote arming and release logic integrated into autonomous control architectures. In July 2024, Raytheon received a contract supporting AIM-9X Sidewinder Block II missile integration across multiple fighters and emerging launcher formats, signaling that compatible release interface standards are now extending to unmanned platforms as well.

End-User Analysis

OEM dominates with 69.1% due to new-build platform procurement volumes.

In 2025, OEM held a dominant market position in the By End User segment of the Weapon Release System Market, with a 69.1% share. Original equipment manufacturers integrate weapon release systems during aircraft production, capturing revenue at the point of highest procurement certainty. Multi-year fighter and helicopter build programs create predictable order pipelines, allowing OEM-aligned suppliers to plan capacity and secure long-term framework agreements.

Aftermarket serves the installed base through upgrade kits, replacement components, and retrofit integration. As legacy aircraft like the F-16 and F/A-18 undergo service-life extensions, aftermarket providers gain access to substantial modification budgets. This segment grows more valuable over time as fleets age and require digital interface upgrades to carry newer generations of smart munitions.

Key Market Segments

By Weapon Type

- Missiles

- Bombs

- Torpedoes

- Rocket

By Platform

- Fighter Aircraft

- Combat Support Aircraft

- Helicopters

- UAVs

By End User

- OEM

- Aftermarket

Drivers

Fighter Aircraft Modernization Programs and Precision Strike Mandates Accelerate Weapon Release System Procurement

Global fighter aircraft procurement and modernization programs are the single most powerful demand engine for weapon release systems. Nations across NATO, the Indo-Pacific, and the Middle East are replacing fourth-generation fleets with fifth-generation platforms, each requiring new multi-station release hardware. These procurement cycles run for decades, creating long-term revenue certainty for qualified system integrators.

Precision weapon deployment has become an operational requirement rather than a capability option. Air forces now demand release systems that can manage mixed weapon loads — missiles, guided bombs, and electronic warfare pods — across a single sortie. According to airandspaceforces.com, the F-35A carries up to 22,000 lb of weapons across 10 stations, combining internal bays and external pylons. This multi-station architecture requires sophisticated store management systems, raising the average contract value per aircraft.

In July 2024, RTX’s Raytheon received a contract for AIM-9X Sidewinder Block II missiles for the U.S. Navy and allies, reinforcing demand for compatible rail launchers and smart weapon release interfaces across multiple fighter types. Each new munitions contract of this scale creates a downstream requirement for certified release hardware, making munitions procurement a reliable forward indicator for this market’s order pipeline.

Restraints

High Integration Complexity and Military Certification Requirements Create Entry Barriers and Program Delays

Weapon release systems must meet some of the most stringent certification and safety standards in any defense subsystem category. Each system must demonstrate safe separation across the full flight envelope, with certification processes that can extend program timelines by years. These requirements increase development costs substantially and make qualification a structural barrier that limits competition to a small pool of established defense suppliers.

Next-generation combat aircraft such as the F-35 use deeply integrated avionics and software architectures that require weapon release systems to interface with multiple aircraft subsystems simultaneously. Adapting existing release hardware to these digital environments requires significant re-engineering investment. Vendors that lack software integration capabilities find themselves excluded from the most valuable new-build contracts, narrowing the competitive field further.

Strict military compliance also slows the adoption of commercially derived technologies. Innovations in electromechanical actuation or lightweight materials that are mature in commercial aerospace face multi-year re-certification processes before qualifying for military use. This lag between commercial readiness and military adoption creates a persistent gap between what is technically possible and what is currently deployable, constraining the pace of product evolution in this market.

Growth Factors

Advanced Electromechanical Systems and UAV Expansion Create New Revenue Streams Beyond Legacy Platform Upgrades

The shift from hydraulic to electromechanical weapon release mechanisms represents a fundamental product upgrade cycle across both new-build and retrofit markets. Electromechanical systems offer lower maintenance burden, higher precision, and digital integration capability — all requirements that modern combat aircraft programs demand. Vendors that develop qualified electromechanical solutions position themselves to capture a share of every active aircraft modernization contract.

According to navalnews.com, F-35 Block 4 incorporates more than 80 capability upgrades, including integration of AGM-158C LRASM, GBU-53/B StormBreaker, AIM-260 JATM, and AGM-88G AARGM-ER. Each of these weapon integrations requires validated release hardware and updated store management software. This breadth of new weapon types creates multiple parallel integration contracts, each representing incremental revenue for certified release system providers.

In November 2024, the U.S. Army awarded Lockheed Martin a contract to increase PAC-3 MSE production capacity, supporting the integration of launcher canisters and fire-control interfaces that manage the safe release and firing sequence of interceptors. This expansion of ground-based missile release infrastructure illustrates how next-generation defense investment extends weapon release system demand well beyond airborne platforms alone.

Emerging Trends

Digital Weapon Management, Modular Architectures, and Network-Centric Control Systems Redefine Platform Compatibility Standards

Digital weapon management systems are replacing analog and semi-digital store management units across active fleets. Modern systems offer real-time weapon status monitoring, automatic release sequencing, and encrypted communication with mission computers. According to navalnews.com, annual F-35 production runs at a pace roughly five times faster than any other allied fighter currently in production — meaning digital management standards established on this platform will propagate across the largest active production line in Western defense.

Modular weapon release platforms are reshaping how air forces configure multi-role aircraft. Rather than platform-specific hardware, modular architectures allow a single release system to accommodate different weapon types through software updates and interchangeable mechanical interfaces. This reduces lifecycle cost for operators while concentrating design authority — and recurring upgrade revenue — with the modular platform provider.

In 2024, contracts under the U.S. Army’s FWS-I program required integration of thermal sights with weapon rails and mounting interfaces, reflecting how network-centric systems now extend weapon management logic beyond traditional airborne platforms into ground and dismounted applications. This cross-domain integration trend signals that weapon release system vendors with software-layer expertise will find addressable markets expanding into new platform categories.

Regional Analysis

North America Dominates the Weapon Release System Market with a Market Share of 43.70%, Valued at USD 253.1 Million

North America holds a 43.70% share of the Weapon Release System Market, valued at USD 253.1 Million in 2025. The United States drives this leadership through the world’s largest defense procurement budget, including the F-35 program, B-21 development, and multi-year munitions contracts. In 2026, the U.S. Pentagon is allocating approximately USD 153 Billion in accelerated military funding, including roughly USD 24 Billion for munitions, directly sustaining demand for advanced weapon release systems.

Europe Weapon Release System Market Trends

Europe represents the second-largest regional market, supported by NATO modernization commitments and active programs across Germany, France, and the UK. European nations are upgrading Eurofighter and Rafale fleets while simultaneously procuring F-35s, creating parallel demand channels for both domestic and U.S.-standard release hardware. Germany’s USD 1.2 Billion Patriot system order in July 2024 demonstrates the scale of European missile defense investment that drives compatible release system procurement.

Asia Pacific Weapon Release System Market Trends

Asia Pacific is the fastest-growing regional demand center, driven by active territorial disputes and fleet expansion programs in China, India, Japan, South Korea, and Australia. Japan and South Korea are among the largest F-35 customers outside North America, creating immediate demand for compatible weapon release and store management systems. India’s domestic fighter production programs add a localization dimension that favors vendors with in-country manufacturing or offset partnerships.

Middle East and Africa Weapon Release System Market Trends

The Middle East sustains steady procurement activity through long-standing U.S. and European defense partnerships and active operational requirements. Gulf nations continue to upgrade their fighter fleets with advanced precision munitions, each requiring certified release hardware. Africa presents limited near-term volume but represents a developing procurement base as several nations invest in counter-insurgency air capabilities.

Latin America Weapon Release System Market Trends

Latin America represents a smaller but stable market segment, with Brazil and Mexico driving the majority of regional defense spending. Fleet recapitalization programs and the need to replace aging aircraft release hardware provide incremental procurement opportunities. Regional buyers generally favor proven systems with established support infrastructure over unproven new entrants, making existing supplier relationships the primary competitive advantage in this geography.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

RUAG Group positions itself as a European-based specialist in airborne weapon carriage, release systems, and aircraft systems integration. Its advantage lies in proximity to European NATO customers and established qualification history on platforms including Eurofighter and F/A-18. This geographic and platform alignment gives RUAG a structural bid advantage on European fleet upgrade contracts that require offset or in-region industrial participation.

Marotta Controls focuses on precision fluid and motion control systems for defense applications, with direct relevance to electromechanical weapon release and store management hardware. Its engineering depth in custom actuation components positions it as a critical subsystem supplier to prime integrators. As the industry shifts toward digital electromechanical release mechanisms, Marotta’s component-level expertise becomes more strategically valuable within prime contractor supply chains.

Harris Corporation brings electronic systems integration capability that extends weapon release functionality into broader mission and communication systems architectures. Its ability to integrate store management systems with aircraft avionics and data links addresses the growing demand for network-centric weapon control. This cross-system integration capability is a differentiated advantage as air forces move toward connected, software-defined weapon management architectures.

ALKAN is a French manufacturer with deep expertise in aircraft weapon suspension, release, and jettison systems. Its long-standing relationship with Dassault Aviation and established NATO qualification history make it a preferred supplier for Rafale-equipped nations. As France expands Rafale exports across Europe, Asia, and the Middle East, ALKAN’s platform-specific expertise creates a durable competitive position tied directly to Rafale fleet growth.

Key Players

- RUAG Group

- Marotta Controls

- Harris Corporation

- ALKAN

- Ultra Electronics

- Moof Inc.

- Marvin Group

- Raytheon Company

- Cobham plc

- RAFAUT

Recent Developments

- January 2026 — The F-35 program surpassed one million cumulative flight hours with a global fleet of nearly 1,300 aircraft. A 2025 U.S. Marine Corps F-35B deployment recorded nearly 5,000 mishap-free flight hours, and NATO F-35s engaged and eliminated Russian drones over Poland, confirming operational readiness of the program’s release and weapons integration architecture.

- 2025 — Annual F-35 production ran at a pace roughly five times faster than any other allied fighter currently in production. The program completed Technology Refresh 3 (TR-3) software, enabling integration of next-generation weapons and significantly expanding the certified weapons envelope for existing fleet aircraft.

- March 2025 — Lockheed Martin introduced the Sidekick rack on Lot 17 F-35s, enabling internal carriage of six AMRAAM-sized missiles and increasing the internal air-to-air payload from four to six missiles for F-35A and F-35C variants without compromising the aircraft’s low-observable stealth configuration.

- December 2025 — The U.S. Air Force and Northrop Grumman flight-tested the Stand-In Attack Weapon (SiAW) from an F-16 to validate safe separation and flight characteristics prior to integration on the F-35, advancing the certified weapon envelope for one of the program’s highest-priority new munitions additions.

- 2026 — The U.S. Pentagon allocated approximately USD 153 Billion in accelerated new military funding, including roughly USD 24 Billion for munitions such as medium-range missiles. This direct munitions investment creates immediate downstream demand for compatible aircraft weapon release systems across active and forthcoming platforms.

Report Scope

Report Features Description Market Value (2025) USD 579.4 Million Forecast Revenue (2035) USD 1,205.3 Million CAGR (2026-2035) 7.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Weapon Type (Missiles, Bombs, Torpedoes, Rocket), By Platform (Fighter Aircraft, Combat Support Aircraft, Helicopters, UAVs), By End User (OEM, Aftermarket) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape RUAG Group, Marotta Controls, Harris Corporation, ALKAN, Ultra Electronics, Moof Inc., Marvin Group, Raytheon Company, Cobham plc, RAFAUT Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Weapon Release System MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample

Weapon Release System MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- RUAG Group

- Marotta Controls

- Harris Corporation

- ALKAN

- Ultra Electronics

- Moof Inc.

- Marvin Group

- Raytheon Company

- Cobham plc

- RAFAUT

Our Clients

- 183785

- Apr 2026