Quick Navigation

Report Overview

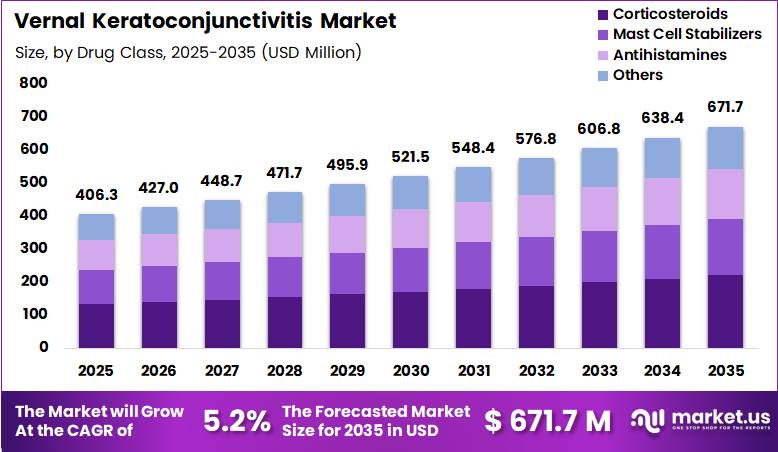

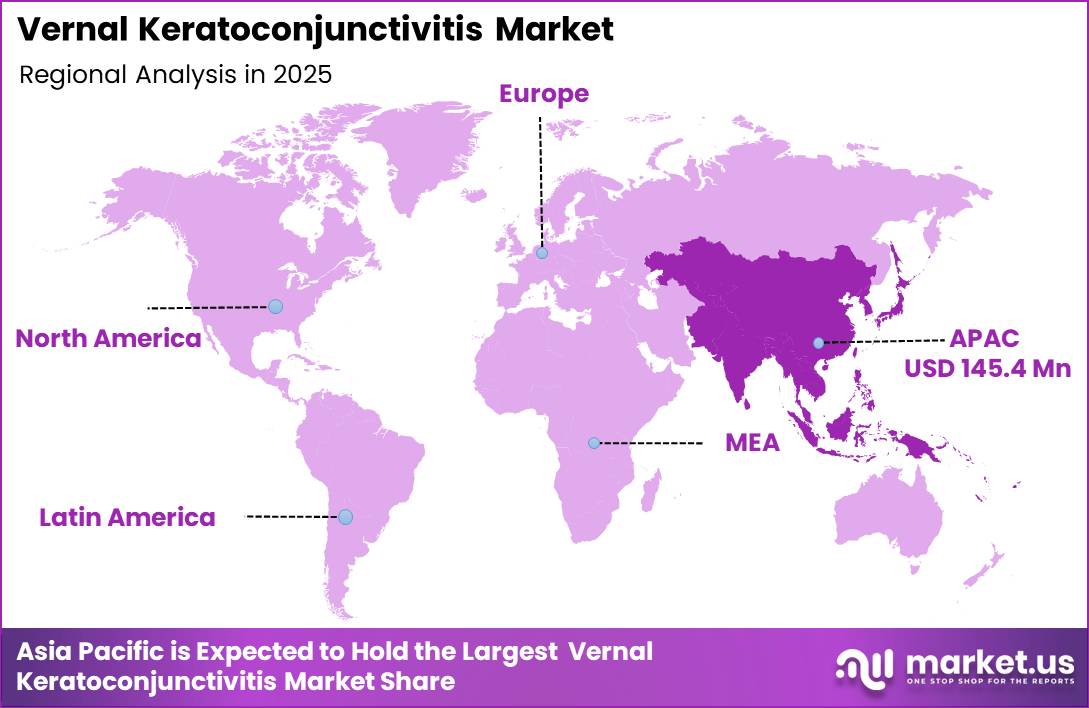

Global Vernal Keratoconjunctivitis Market size is expected to be worth around US$ 671.7 Million by 2035 from US$ 406.3 Million in 2025, growing at a CAGR of 5.2% during the forecast period from 2026 to 2035. In 2025, Asia Pacific led the market, achieving over 35.8% share with a revenue of US$ 145.4 Million.

Vernal keratoconjunctivitis (VKC) is a chronic, recurrent, and severe form of allergic eye disease that primarily affects children and adolescents, particularly in tropical and subtropical regions. The condition is characterized by inflammation of the conjunctiva and cornea, leading to symptoms such as intense ocular itching, redness, tearing, photophobia, and mucous discharge.

If left untreated, VKC may result in corneal complications, scarring, and permanent visual impairment, thereby increasing the need for effective long-term therapeutic management.

According to the U.S. National Center for Biotechnology Information (NCBI), VKC occurs more frequently in males than females, with reported male-to-female ratios ranging from 2:1 to 3:1, and most cases are diagnosed between 5 and 10 years of age. Approximately 95% of affected patients experience remission by late adolescence, although severe cases may persist into adulthood.

The increasing global burden of ocular allergies is a major factor supporting demand for VKC therapeutics. A review published in Allergology International reported that the prevalence of allergic rhinoconjunctivitis reached 14.6% among adolescents across 98 countries, while several regions reported prevalence rates exceeding 18%, highlighting the growing incidence of allergic eye disorders worldwide.

Furthermore, VKC prevalence is considerably higher in warm-climate regions, with studies reporting prevalence rates ranging from 2% to 37% in parts of Africa and up to 12.6 cases per 10,000 population in Europe.

The VKC market encompasses a broad range of treatment options, including topical antihistamines, mast cell stabilizers, corticosteroids, calcineurin inhibitors such as cyclosporine and tacrolimus, lubricating eye drops, and emerging biologic therapies. Growing concerns regarding steroid-associated adverse effects, including glaucoma and cataracts, have accelerated the adoption of steroid-sparing immunomodulatory therapies.

Additionally, advancements in ophthalmic drug delivery systems, preservative-free formulations, and increasing awareness programs for allergic eye diseases are improving diagnosis and treatment rates. Rising investments in ophthalmic healthcare infrastructure and ongoing clinical research focused on safer and more effective therapies are expected to support the continued expansion of the vernal keratoconjunctivitis market globally.

Key Takeaways

- Market Size: Global Vernal Keratoconjunctivitis Market size is expected to be worth around US$ 671.7 Million by 2035 from US$ 406.3 Million in 2025.

- Market Share: The market growing at a CAGR of 5.2% during the forecast period from 2026 to 2035.

- Drug Class Analysis: Corticosteroids are expected to dominate the market, accounting for 32.8% of the total market share in 2025.

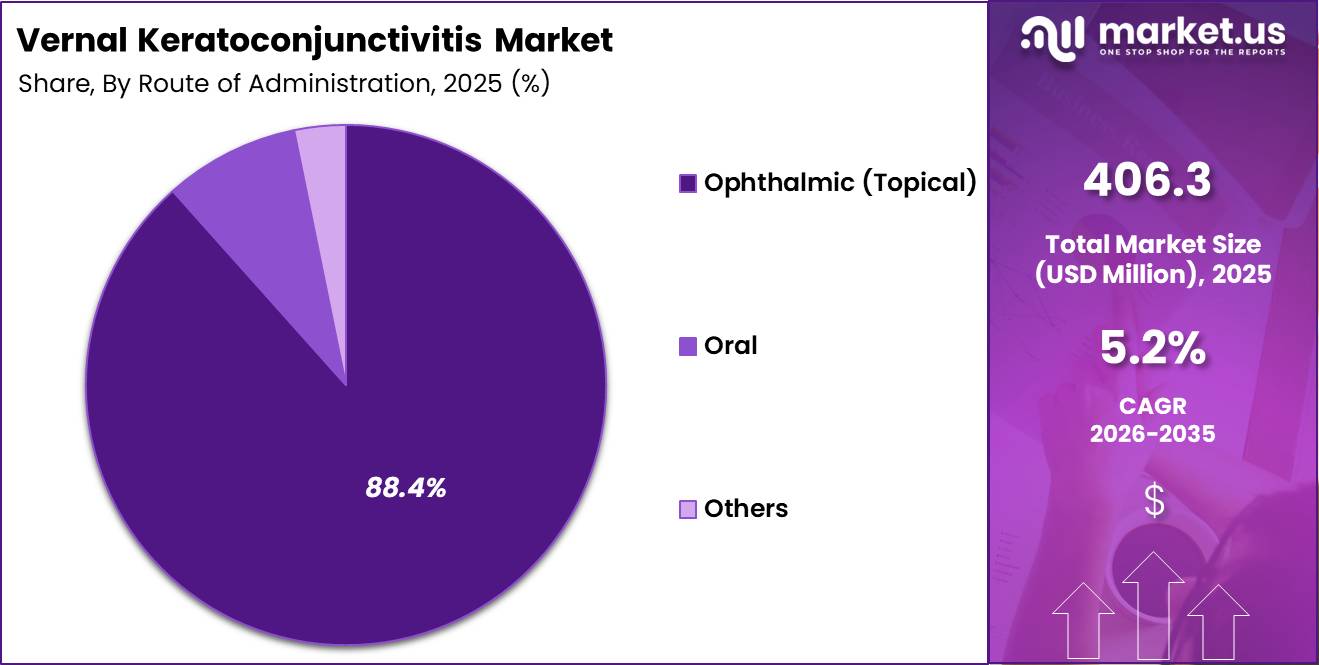

- Route of Administration Analysis: The Ophthalmic (Topical) segment dominates the market with an estimated 88.4% share in 2025.

- End-User Analysis: The Hospitals segment is projected to account for 52.8% of the market share in 2025, making it the leading end-user category.

- Market Regional Analysis: In 2025, Asia Pacific led the market, achieving over 35.8% share with a revenue of US$ 145.4 Million.

Market Dynamics

Driving Factors - Increasing Focus on Early Diagnosis and Long-Term Disease Management

The growing emphasis on early identification and proactive management of chronic ocular disorders is supporting the growth of the vernal keratoconjunctivitis (VKC) market. Healthcare providers are increasingly recognizing the importance of timely intervention to prevent disease progression and reduce the risk of corneal complications that may affect visual function.

Improved access to ophthalmic specialists, expanding pediatric eye care services, and greater awareness among caregivers have contributed to higher diagnosis rates and earlier treatment initiation.

In addition, the need for sustained disease control has encouraged the adoption of advanced therapeutic approaches that can effectively manage recurrent symptoms while minimizing treatment-related complications. These factors continue to support demand for VKC therapies across healthcare settings.

Trending Factors - Advancements in Patient-Centric Ophthalmic Treatment Approaches

A key trend shaping the VKC market is the growing focus on improving patient experience and treatment adherence through innovative ophthalmic solutions. Manufacturers are increasingly investing in advanced drug delivery technologies designed to enhance ocular bioavailability and reduce dosing frequency. The development of preservative-free formulations is also gaining attention as healthcare providers seek to improve tolerability during long-term treatment.

In parallel, digital health tools, teleophthalmology platforms, and remote follow-up solutions are gradually being incorporated into disease management practices, enabling more efficient monitoring of treatment response. These developments are contributing to a more personalized and patient-centered approach to VKC management.

Restraining Factors - Limited Availability of Specialized Ophthalmic Care

The availability of specialized ophthalmic services remains a challenge in several regions, particularly in underserved and rural areas. Effective management of VKC often requires regular clinical evaluation and ongoing follow-up, which may not be readily accessible to all patients. Variations in clinical expertise and treatment practices can also result in inconsistent disease management.

Furthermore, the long-term nature of therapy may create financial and logistical burdens for patients and caregivers, potentially affecting treatment continuity. These factors can hinder optimal disease control and limit the broader adoption of advanced therapeutic interventions.

Opportunity - Expansion of Research and Innovation in Ocular Immunology

Growing research activity in ocular immunology is creating new opportunities within the VKC market. Increasing understanding of the inflammatory pathways involved in ocular allergic diseases is supporting the development of more targeted therapeutic approaches with improved safety and efficacy profiles.

Collaboration among pharmaceutical companies, research institutions, and ophthalmology centers is accelerating innovation in this field. Additionally, investments in pediatric ophthalmology programs and specialized eye care facilities are expanding the potential patient base for advanced treatments. As research continues to advance, opportunities are expected to emerge for next-generation therapies that address unmet clinical needs and improve long-term patient outcomes.

Drug Class Analysis

The drug class segment of the Vernal Keratoconjunctivitis (VKC) market is categorized into Corticosteroids, Mast Cell Stabilizers, Antihistamines, and Others. Corticosteroids are expected to dominate the market, accounting for 32.8% of the total market share in 2025.

Their strong market position is attributed to their rapid anti-inflammatory action and high efficacy in managing moderate-to-severe VKC symptoms, including intense ocular itching, redness, photophobia, and corneal inflammation. Ophthalmologists frequently prescribe corticosteroids during acute disease exacerbations, particularly in patients requiring immediate symptom control.

Mast Cell Stabilizers represent a significant segment due to their preventive mechanism of action, which inhibits mast cell degranulation and reduces the release of inflammatory mediators. These agents are widely utilized for long-term disease management and prophylactic treatment, especially among pediatric patients with recurrent allergic episodes.

Antihistamines also hold a notable market share owing to their effectiveness in relieving itching and allergic symptoms. The availability of dual-action formulations combining antihistaminic and mast cell-stabilizing properties has further strengthened segment growth.

The Others segment, including immunomodulators such as cyclosporine and tacrolimus, continues to gain traction. Increasing adoption of steroid-sparing therapies and growing awareness regarding the long-term adverse effects associated with corticosteroid use are expected to support segment expansion throughout the forecast period.

Route of Administration Analysis

Based on route of administration, the Vernal Keratoconjunctivitis market is segmented into Ophthalmic (Topical), Oral, and Others. The Ophthalmic (Topical) segment dominates the market with an estimated 88.4% share in 2025.

The segment’s leadership is primarily driven by the localized delivery of medications directly to the ocular surface, resulting in rapid therapeutic effects, enhanced bioavailability at the target site, and reduced systemic side effects. Topical formulations, including eye drops, suspensions, and ointments, remain the standard treatment approach for VKC management and are widely prescribed across all disease severities.

The Oral segment accounts for a smaller but important share of the market. Oral antihistamines are commonly recommended for patients experiencing concomitant systemic allergic conditions such as allergic rhinitis, asthma, or atopic dermatitis. These therapies provide additional symptom control, particularly during seasonal allergic flare-ups.

The Others segment includes emerging and specialized administration approaches utilized in severe or refractory cases. Growth within this category is supported by ongoing research into advanced ocular drug delivery systems designed to improve patient compliance and therapeutic outcomes.

The increasing preference for non-invasive treatment options, coupled with continuous innovations in ophthalmic formulations, is expected to sustain the dominance of the topical administration segment over the forecast period.

End-User Analysis

Based on end users, the Vernal Keratoconjunctivitis market is segmented into Hospitals, Ophthalmic Clinics, and Others. The Hospitals segment is projected to account for 52.8% of the market share in 2025, making it the leading end-user category.

Hospital dominance is attributed to the availability of specialized ophthalmology departments, advanced diagnostic capabilities, multidisciplinary care teams, and comprehensive treatment options for moderate-to-severe VKC cases. Hospitals also serve as primary referral centers for patients experiencing complications such as corneal involvement, vision impairment, or recurrent disease episodes requiring intensive management.

Ophthalmic Clinics represent the second-largest segment and play a crucial role in the diagnosis, monitoring, and treatment of mild-to-moderate VKC cases. The growing number of specialized eye care centers, shorter waiting times, and increasing accessibility to ophthalmology services have contributed significantly to segment growth. These facilities are increasingly adopting advanced diagnostic technologies and personalized treatment protocols to improve patient outcomes.

The Others segment includes ambulatory surgical centers, community healthcare facilities, and academic research institutions involved in ocular allergy management. Rising awareness of allergic eye disorders and expanding access to specialized eye care services are supporting the growth of this segment.

Overall, increasing disease prevalence, improved healthcare infrastructure, and greater availability of specialized ophthalmic services are expected to drive demand across all end-user categories during the forecast period.

Key Market Segments

By Drug Class

- Corticosteroids

- Mast Cell Stabilizers

- Antihistamines

- Others

By Route of Administration

- Ophthalmic (Topical)

- Oral

- Others

By End User

- Hospitals

- Ophthalmic Clinics

- Others

Regional Analysis

In 2025, Asia Pacific dominated the Vernal Keratoconjunctivitis (VKC) market, accounting for over 35.8% of the global market share and generating revenue of approximately US$ 145.4 million.

The region’s leadership can be attributed to its large pediatric population, increasing prevalence of allergic eye disorders, and rising exposure to environmental allergens such as dust, pollen, and air pollution. Countries including India, China, and Japan represent major contributors to market growth due to their expanding healthcare infrastructure and growing awareness regarding early diagnosis and treatment of ocular allergies.

North America held a significant share of the market, supported by advanced healthcare systems, high healthcare expenditure, and widespread availability of innovative ophthalmic treatments. Increased adoption of prescription therapies and strong presence of leading pharmaceutical companies further strengthened regional market growth.

Europe also represented a notable portion of the market, driven by rising incidence of allergic conjunctival diseases and favorable reimbursement policies in several countries. Growing investments in ophthalmology research and increasing patient awareness supported market expansion across the region.

Meanwhile, Latin America and the Middle East & Africa are expected to witness steady growth during the forecast period. Improving access to healthcare services, expanding diagnostic capabilities, and increasing awareness of allergic eye conditions are anticipated to create new opportunities for market participants in these emerging regions.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The Vernal Keratoconjunctivitis (VKC) market is characterized by the presence of both established pharmaceutical companies and emerging biotechnology firms focused on developing innovative ophthalmic therapies. Key players are strengthening their market positions through product innovation, clinical research, strategic collaborations, and geographic expansion.

Major companies such as Novartis, Santen Pharmaceutical, Alcon, and Bausch + Lomb offer a range of anti-inflammatory and immunomodulatory treatments used in VKC management. In addition, companies are investing in advanced formulations that improve efficacy, reduce dosing frequency, and enhance patient compliance.

Emerging players are actively evaluating novel biologics and targeted therapies to address unmet clinical needs in severe and refractory VKC cases. The competitive landscape is further influenced by increasing regulatory approvals, partnerships with research institutions, and growing awareness of allergic eye disorders.

As demand for effective long-term treatment options increases, market participants are expected to focus on expanding product portfolios and strengthening their presence across high-growth regional markets.

Market Key Players

- Novartis AG

- Allergan plc (AbbVie)

- Santen Pharmaceutical Co., Ltd.

- Bausch Health Companies Inc.

- F. Hoffmann-La Roche Ltd

- Johnson & Johnson Vision

- Alcon Inc.

- Ocular Therapeutix, Inc.

- Regeneron Pharmaceuticals, Inc.

- Teva Pharmaceutical Industries Ltd.

- Sun Pharmaceutical Industries Ltd.

- Cipla Inc.

- Lupin Limited

- Apotex Inc.

- Mylan N.V. (Viatris)

- Others

Recent Developments

- April 2026 – AbbVie Inc. (Allergan Eye Care) announced continued advancement of its ophthalmology pipeline and eye-care research programs as part of its long-term growth strategy. The company reported ongoing investments across ocular surface disorders and retinal disease research, reinforcing its commitment to expanding innovative eye-care solutions globally.

- May 2025 – Regeneron Pharmaceuticals, Inc. entered into an asset purchase agreement to acquire substantially all assets of 23andMe Holding Co. for approximately USD 256 million. The acquisition is intended to enhance Regeneron’s genetics-driven research platform and support the development of innovative therapies across multiple disease areas, including ophthalmology and immune-mediated disorders.

- August 2025 – Ocular Therapeutix, Inc. continued significant investment in its ophthalmology portfolio, reporting research and development expenditure of approximately USD 93.9 million during the first half of 2025. The increased investment was primarily directed toward advancing late-stage clinical programs for retinal and ocular diseases, reflecting the company’s expansion strategy in ophthalmic therapeutics.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 406.3 Million |

| Forecast Revenue (2035) | US$ 671.7 Million |

| CAGR (2026-2035) | CAGR of 5.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Class (Corticosteroids, Mast Cell Stabilizers, Antihistamines, Others) By Route of Administration ( Ophthalmic (Topical), Oral, Others) By End User (Hospitals, Ophthalmic Clinics, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Novartis AG, Allergan plc (AbbVie), Santen Pharmaceutical Co., Ltd., Bausch Health Companies Inc., F. Hoffmann-La Roche Ltd, Johnson & Johnson Vision, Alcon Inc., Ocular Therapeutix, Inc., Regeneron Pharmaceuticals, Inc., Teva Pharmaceutical Industries Ltd., Sun Pharmaceutical Industries Ltd., Cipla Inc., Lupin Limited, Apotex Inc., Mylan N.V. (Viatris), Others, |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |