Quick Navigation

Report Overview

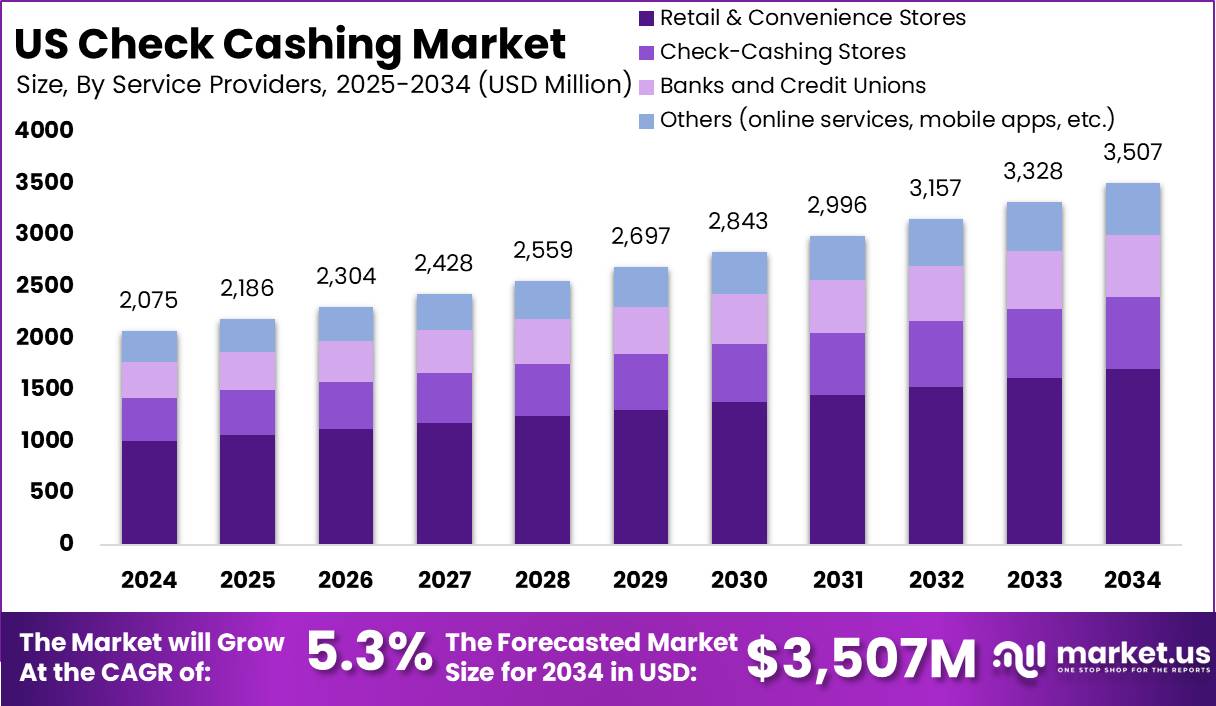

The US Check Cashing Market size is expected to be worth around USD 3,507 Million By 2034, from USD 2,075 Million in 2024, growing at a CAGR of 5.3% during the forecast period from 2025 to 2034.

The US check cashing market is driven by a significant portion of the population that remains unbanked or underbanked. These individuals often rely on check cashing services to access their funds quickly. The market includes various service providers, from small local shops to large retail chains offering check cashing as part of a broader array of financial services.

In the United States, there are approximately 13,000 check-cashing outlets that collectively process over $58 billion in checks annually. The market size is substantial, with expectations for continued growth driven by the need for convenient access to financial services, especially among populations less served by traditional banks.

The primary drivers of the US check cashing market include the high prevalence of unbanked and underbanked individuals, the convenience and immediacy of check cashing services, and the steady demand from workers receiving payroll checks who require immediate access to funds. Payroll check cashing remains dominant, reflecting the critical role these services play in the distribution of employee earnings.

The demand in the check cashing market is largely fueled by individuals, making up a significant portion of the market usage. These services are crucial for people who need quick access to cash to manage daily financial needs. Small businesses also contribute to market demand, utilizing these services for effective cash flow management.

For businesses operating within this market, the primary benefits include a broad customer base of repeat users who require regular access to check cashing services. Additionally, businesses can leverage technological advancements to offer differentiated services such as online and mobile platforms, which can attract a younger demographic and those preferring digital transactions over traditional methods.

Key Takeaways

- The U.S. Check Cashing Market is projected to reach USD 3,507 million by 2034, growing from USD 2,075 million in 2024 at a CAGR of 5.3% during the forecast period. This growth is driven by the continued reliance on alternative financial services, particularly among unbanked and underbanked populations.

- The Payroll Checks segment dominated the market in 2024, accounting for over 36.73% of the market share, as many individuals continue to rely on check cashing services for quick access to wages without needing a traditional bank account.

- Retail & Convenience Stores held a significant 48.6% share in 2024, highlighting their role as key service providers for check cashing. Their accessibility, extended operating hours, and convenience contribute to their dominance in the market.

- The Personal segment captured more than 68.6% of the market share in 2024, reflecting the widespread use of check cashing services for personal financial transactions, including government-issued checks, tax refunds, and insurance settlements.

Analysts’ Viewpoint

Investment opportunities within the check cashing industry are promising due to the market’s expansion and the ongoing integration of technological solutions such as app-based services. The sector’s growth potential is buoyed by increasing financial inclusion initiatives and consumer awareness, making it an attractive area for investors looking at service innovations.

Technological advancements are significantly shaping the check cashing industry. The introduction of mobile check cashing apps and online services has allowed companies to extend their reach and offer convenient solutions that meet the needs of a changing consumer base. These innovations provide faster service and added convenience, thereby enhancing customer satisfaction and competitiveness in the market.

The check cashing industry is subject to stringent regulatory oversight, which includes compliance with AML and KYC regulations. Recent changes have seen regulatory thresholds adjusted, impacting the operational costs and administrative burden for businesses within the market. Despite these challenges, compliance ensures reliability and safety in transactions, which is critical for maintaining consumer trust and market stability.

Types Analysis

In 2024, the Payroll Checks segment held a dominant position within the U.S. Check Cashing Market, capturing more than a 36.73% share. This significant market share can be attributed to the widespread reliance on payroll checks for employee compensation across diverse sectors.

Payroll checks remain a staple in financial transactions, particularly in industries where direct deposit systems are not fully implemented or preferred by employees. The persistence of this method of payment underscores its importance in the financial landscape, catering to a broad demographic that includes both large corporations and small businesses.

US Check Cashing Market Revenue, By Type, 2019-2024 (USD Million)

| By Type | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|---|

| Government Checks | 284.9 | 280.0 | 286.3 | 292.6 | 302.6 | 315.5 |

| Payroll Checks | 662.7 | 657.1 | 678.0 | 699.0 | 729.4 | 767.2 |

| Cashier’s Checks | 155.6 | 151.6 | 153.6 | 155.6 | 159.5 | 164.7 |

| Insurance Checks | 138.6 | 134.8 | 136.4 | 138.0 | 141.2 | 145.6 |

| Retirement Checks | 84.4 | 81.6 | 82.2 | 82.6 | 84.0 | 86.1 |

| Personal Checks | 170.3 | 166.7 | 169.9 | 173.0 | 178.3 | 185.3 |

The prominence of the Payroll Checks segment is further bolstered by the consistent demand for accessible and immediate cashing services that cater to workers who require instant access to their earnings. This need is particularly pronounced among populations that are either unbanked or underbanked.

These individuals often depend on check cashing services to bridge their liquidity gaps efficiently, avoiding potential delays associated with traditional banking procedures. Moreover, the security features inherent in payroll checks, coupled with the stringent regulations governing their issuance, enhance their reliability and trustworthiness as a form of payment.

Additionally, the integration of technology in the check cashing industry has played a pivotal role in maintaining the relevance of payroll checks. Innovations such as mobile applications and automated check cashing machines have streamlined the process, reducing the time and effort required to access funds. These technological advancements not only improve user experience but also expand the reach of services to a wider audience, ensuring the sustained growth of this market segment.

Overall, the Payroll Checks segment’s leadership in the U.S. Check Cashing Market is driven by its critical role in employee compensation, the necessity for immediate financial liquidity among key demographics, and the ongoing technological enhancements that simplify transactions.

Service Providers Analysis

In 2024, the Retail & Convenience Stores segment held a dominant position within the U.S. Check Cashing Market, capturing more than a 48.6% share. This significant market share is primarily driven by the widespread accessibility and convenience offered by these establishments.

Retail and convenience stores are strategically located across both urban and rural areas, providing easy access for a diverse range of customers who may not be in close proximity to traditional banking facilities. Their extended hours of operation, including weekends and holidays, further enhance their appeal as reliable points for financial transactions.

US Check Cashing Market Revenue, By Service Providers Analysis, 2019-2024 (USD Million)

| By Service Providers | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|---|

| Retail & Convenience Stores | 878.5 | 870.5 | 897.9 | 925.3 | 965.1 | 1014.7 |

| Check-Cashing Stores | 587.8 | 577.6 | 590.8 | 603.8 | 624.5 | 651.2 |

| Banks and Credit Unions | 186.4 | 180.6 | 182.1 | 183.4 | 186.9 | 191.9 |

The leadership of the Retail & Convenience Stores segment is also reinforced by the minimal requirements and quick service associated with cashing checks at these venues. Unlike banks or credit unions, retail and convenience stores often do not require account openings or lengthy processing times, which appeals to customers seeking immediate cash.

This is particularly advantageous for individuals who need urgent access to funds and cannot afford the delay typical of more formal banking environments. Moreover, the integration of advanced technological solutions such as point-of-sale systems and automated check verification has increased the efficiency and security of transactions in these stores.

These technological enhancements help in mitigating risks associated with check fraud, thereby boosting consumer confidence in using these services. Additionally, many retail and convenience stores have started offering additional financial services like money transfers and bill payments, making them a one-stop solution for various financial needs.

End User Analysis

In 2024, the Personal segment held a dominant market position within the U.S. Check Cashing Market, capturing more than a 68.6% share. This predominance is largely attributed to the extensive use of check cashing services by individuals for managing personal finances, especially among those who prefer not to engage with traditional banking institutions or lack access to such services.

Personal users typically include those in need of immediate cash flow to meet daily expenses, highlighting the segment’s role in facilitating access to financial resources for a significant portion of the population. The leadership of the Personal segment is further solidified by the simplicity and convenience offered by check cashing services.

US Check Cashing Market Revenue, By End User Analysis, 2019-2024 (USD Million)

| By End User | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|---|

| Personal | 1263.5 | 1246.2 | 1279.3 | 1312.2 | 1362.3 | 1425.6 |

| Commercial | 591.3 | 580.0 | 592.1 | 604.0 | 623.6 | 648.9 |

For many individuals, cashing checks through conventional banks can be cumbersome and time-consuming, involving longer wait times for fund clearance. In contrast, check cashing services provide instant access to cash, which is crucial for users who rely on these funds for urgent financial obligations such as rent, utilities, and other living expenses.

Additionally, the rising number of underbanked and unbanked individuals in the U.S. continues to drive demand within this segment. These individuals often find check cashing services to be a more viable and accessible option for their financial transactions.

The personal check cashing market is also bolstered by the trust and familiarity users have with local service providers, such as retail stores and dedicated check cashing outlets, which often offer personalized service that further attracts personal segment users.

Overall, the Personal segment’s dominance in the U.S. Check Cashing Market is maintained through its critical role in providing rapid, reliable, and accessible financial services to individuals, particularly those who are excluded from or choose not to participate in the traditional banking system.

Key Market Segments

By Types

- Government Checks

- Payroll Checks

- Cashier’s Checks

- Insurance Checks

- Retirement Checks

- Personal Checks

- Others (Business Checks, etc.)

By Service Providers

- Retail & Convenience Stores

- Check-Cashing Stores

- Banks and Credit Unions

- Others (online services, mobile apps, etc.)

By End User

- Personal

- Commercial

Driver

Increasing Reliance on Non-Banking Financial Services

One of the main drivers of the US check cashing market is the increasing reliance on non-banking financial services by a significant portion of the population. An estimated 5.4% of the US population is unbanked, and many more are underbanked, relying heavily on alternative financial services like check cashing facilities.

These services are particularly crucial for individuals and households facing financial instability or who lack access to traditional banking due to issues like poor credit history or the absence of necessary documentation. The convenience, immediacy, and minimal requirement for these services continue to drive their popularity, ensuring sustained market growth.

Restraint

High Regulatory Compliance Costs

The check cashing industry faces significant challenges due to the stringent regulatory environment designed to prevent money laundering and fraud. Compliance with Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations is both complex and costly, requiring businesses to invest heavily in compliance infrastructure and processes.

These regulations, while necessary for the security and integrity of financial transactions, increase the operational costs for check cashing businesses, thereby restraining market growth. The financial burden is particularly heavy on smaller operators who might lack the resources to effectively meet these regulatory demands.

Opportunity

Technological Advancements and Digital Integration

There is a significant opportunity for growth in the US check cashing market through technological advancements and digital integration. The increasing adoption of technologies like mobile check cashing, biometric authentication, and artificial intelligence for enhancing service efficiency presents a major growth avenue.

These technologies not only streamline operations but also improve customer experience by offering convenient, quick, and secure service options. Mobile platforms, in particular, are gaining traction, enabling users to cash checks through smartphones, thus broadening the market reach and appealing to a tech-savvy younger demographic.

Challenge

Maintaining Customer Trust and Managing Fraud

A major challenge in the check cashing industry is maintaining customer trust while managing the risks associated with fraud. Check cashing services must constantly evolve their fraud detection and prevention strategies to combat the risk of counterfeit checks and identity theft.

Additionally, any incidents of fraud or breaches of customer data can severely damage a service provider’s reputation, leading to loss of customer trust and business. Thus, businesses need to invest in robust security measures and customer service to build and maintain trust, ensuring customer retention and market stability.

Growth Factors

The US check cashing market is driven by several compelling factors that sustain its growth. A significant driver is the continued reliance on physical checks for business transactions, which provides a steady stream of customers to check cashing facilities. This is particularly relevant for businesses that prefer checks due to their ability to provide clear transaction records and for personal use where banks are not an option.

Additionally, the prevalence of unbanked and underbanked populations who lack adequate access to traditional banking services underpins the demand for check cashing services. This segment finds check cashing services invaluable for accessing their funds promptly and conveniently, without the hurdles of traditional banking systems.

Emerging Trends

Emerging trends in the check cashing industry are largely driven by technological advancements. The integration of digital technologies in check cashing services, such as mobile applications that allow for remote depositing of checks, is becoming increasingly popular.

These mobile platforms are not only enhancing the convenience but also expanding access, making it easier for users to manage their transactions from anywhere. Moreover, there is a growing trend towards the integration of fintech solutions within the check cashing sector.

Innovations such as blockchain for secure and fast transactions and partnerships with digital wallet providers are expected to increase efficiency and security, making these services more attractive to a broader demographic.

Business Benefits

The check cashing industry offers significant business benefits, particularly due to its wide customer base and the essential nature of its services. For many customers, especially those in lower-income brackets or with irregular income patterns, check cashing services are often the only financial services accessible. This creates a stable and recurring customer base reliant on these services.

Furthermore, the ability of check cashing businesses to offer immediate access to funds is a critical advantage that aligns with the urgent financial needs of their customers, including covering daily expenses or emergency costs. This immediacy and reliability in transactions foster customer loyalty and continuous patronage, which are beneficial for the sustained profitability of businesses within this market.

Key Player Analysis

Amscot Financial operates as one of the leading check-cashing service providers in the U.S. The company has expanded its presence primarily in Florida, with over 230 locations. Amscot has focused on customer convenience by integrating additional financial services such as money orders, bill payments, and payday loans.

Money Mart, formerly known as Dollar Financial Group, has a strong presence in North America, including the U.S. and Canada. The company operates hundreds of check-cashing locations and offers various financial services, such as short-term lending, prepaid cards, and money transfers.

ACE Cash Express is another major player in the U.S. check cashing industry, operating over 850 locations nationwide. The company provides a broad range of financial services, including payday loans, prepaid debit cards, and bill payment services.

Top Key Players in the Market

- Walmart

- ACE Cash Express

- PayPal

- Western Union

- MoneyGram International, Inc.

- Pay-O-Matic

- PLS Financial Services, Inc.

- Speedy Cash

- United Check Cashing

- Moneytree, Inc.

- The Check Cashing Store

- CFSC (Community Financial Service Centers)

- Friendly Check Cashing, Inc.

Recent Developments

- In February 2025, Shift4, a U.S. payment processing firm, signed a definitive agreement to acquire Global Blue, a Swiss paytech company, for approximately $2.5 billion. This acquisition expands Shift4’s international presence and enhances its payment processing capabilities, which could influence competition in the financial services sector.

- In March 2024, MoneyGram expanded its partnership with Walmart, enabling customers to send money internationally to over 200 countries and territories through Walmart’s MoneyCenter services. This collaboration aims to provide affordable and accessible money transfer options to a broader customer base.

- In February 2025, shareholders of both Capital One and Discover approved Capital One’s proposed acquisition of Discover Financial Services. This merger is expected to create a more comprehensive suite of financial products and services, potentially affecting the competitive landscape of the check cashing and broader financial services industry.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 2,075 Bn |

| Forecast Revenue (2034) | USD 3,507 Bn |

| CAGR (2025-2034) | 5.3% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Types (Government Checks, Payroll Checks, Cashier’s Checks, Insurance Checks, Retirement Checks, Personal Checks, Others (Business Checks, etc.)), By Service Providers (Retail & Convenience Stores, Check-Cashing Stores, Banks and Credit Unions, Others (online services, mobile apps, etc.)), By End User (Personal, Commercial) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Walmart, ACE Cash Express, PayPal, Western Union, MoneyGram International Inc., Pay-O-Matic, PLS Financial Services Inc., Speedy Cash, United Check Cashing, Moneytree Inc., The Check Cashing Store, CFSC (Community Financial Service Centers), Friendly Check Cashing Inc., |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |