Global Transfer Switch Market Size, Share, Growth Analysis By Type (Automatic Transfer Switch, Manual Transfer Switch), By Mode (Open Transition Mode, Closed Transition Mode, Soft Load Transition Mode, Delayed Transition Mode), By Voltage Rating (Low, Medium, High), By Application (Industrial, Residential, Commercial), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181451

- Number of Pages: 219

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

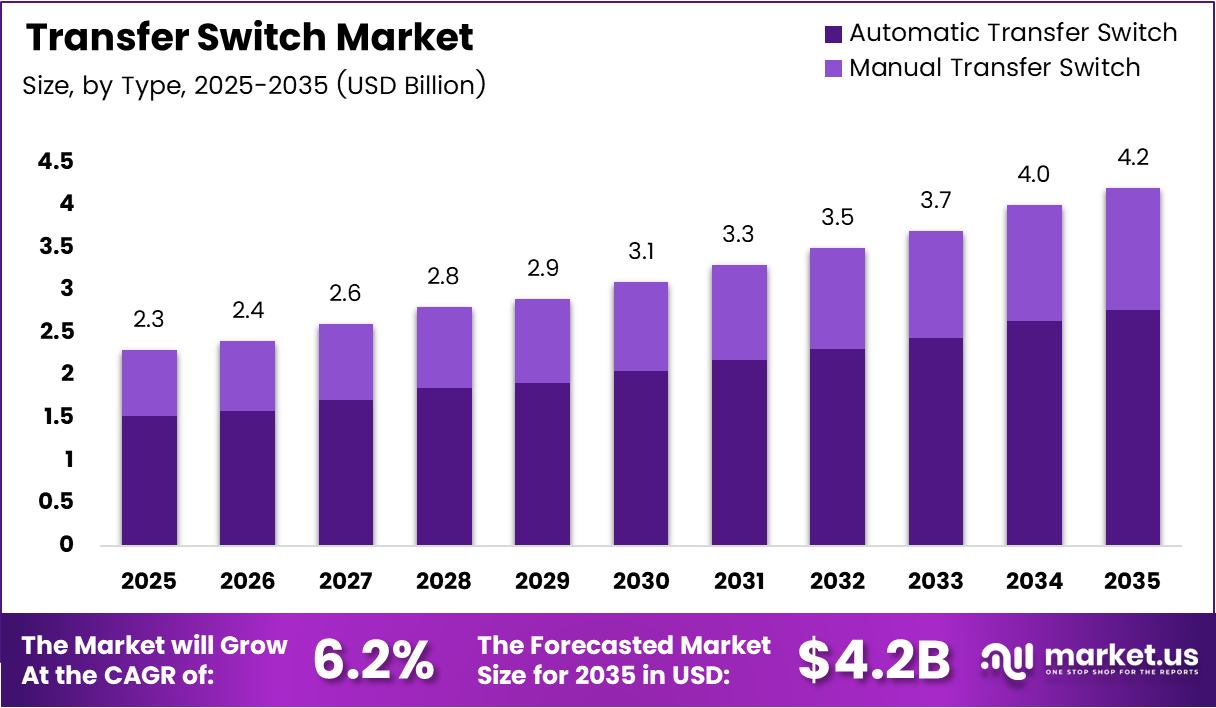

Global Transfer Switch Market size is expected to be worth around USD 4.2 Billion by 2035 from USD 2.3 Billion in 2025, growing at a CAGR of 6.2% during the forecast period 2026 to 2035.

Transfer switches form the backbone of power continuity infrastructure across industries. These devices detect power supply failures and redirect electrical loads to backup sources — generators, battery storage, or renewable systems — without manual intervention. Their role spans data centers, hospitals, manufacturing plants, and residential backup systems worldwide.

The market’s steady expansion reflects real structural pressure on power infrastructure. Grid instability, aging utility networks, and higher uptime expectations from commercial and industrial operators are pushing facility managers to treat backup power switching as a non-negotiable investment rather than an optional upgrade.

Automatic transfer switches dominate adoption, commanding 65.4% of the market by type. This concentration signals that buyers prioritize speed and reliability over cost savings — operators simply cannot afford manual intervention during a power failure in data centers or hospitals.

Industrial applications account for 45.6% of demand by end use. Continuous manufacturing processes, where even seconds of downtime translate to measurable production losses, are the core driver behind this share. Consequently, industrial buyers consistently select higher-specification systems with faster transfer times.

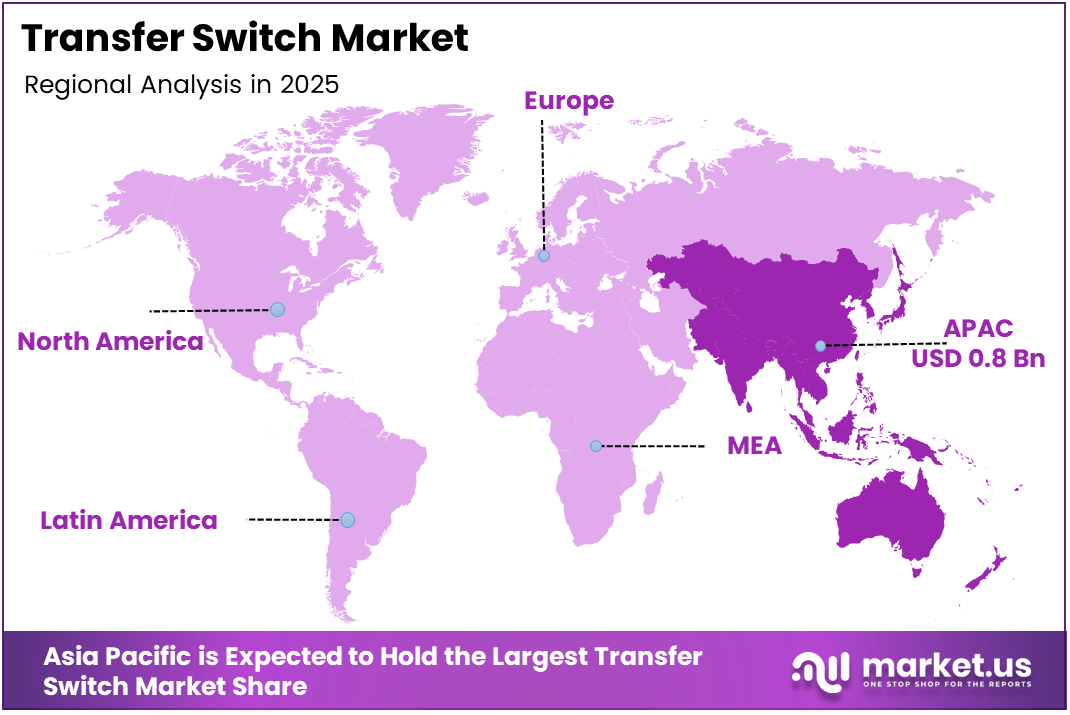

Asia Pacific leads the global transfer switch market with a 38.6% share, valued at approximately USD 0.8 Billion. Rapid industrialization across China, India, and Southeast Asia, combined with unreliable grid infrastructure in emerging economies, creates persistent structural demand for reliable power transfer solutions in the region.

According to the Borri-Legrand STS brochure published in January 2025, the STS 16-32 models achieve an AC/AC efficiency of 99%. This efficiency level matters because it directly reduces operational energy costs in large-scale data center deployments, where even fractional efficiency gains translate to significant annual savings.

According to E3S Web of Conferences, Volume 601, Article 00088, published January 2025, in an ATS-managed hybrid PV-generator system with 6 batteries, the PV source covers 7.88 hours of an 8-hour operational requirement, reducing generator runtime to just 0.12 hours. This finding confirms that ATS technology is now a critical enabler of hybrid renewable energy deployment, not merely a backup power accessory.

Key Takeaways

- The global Transfer Switch Market was valued at USD 2.3 Billion in 2025 and is forecast to reach USD 4.2 Billion by 2035, at a CAGR of 6.2%.

- By Type, Automatic Transfer Switch leads with a 65.4% market share in 2025.

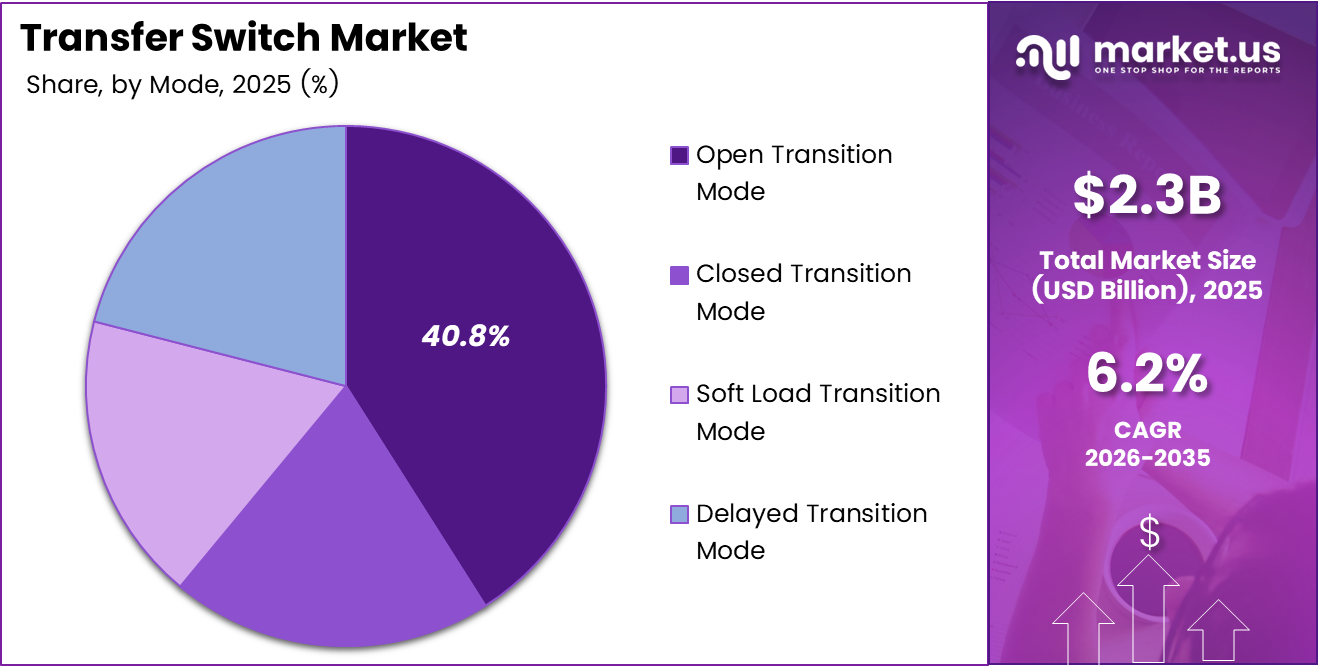

- By Mode, Open Transition Mode holds the largest share at 40.8%.

- By Voltage Rating, Medium (300A–1600A) accounts for 45.6% of the market.

- By Application, Industrial segment dominates with 45.6% share.

- Asia Pacific leads all regions with a 38.6% share, valued at USD 0.8 Billion.

Type Analysis

Automatic Transfer Switch dominates with 65.4% due to zero-intervention failover capability.

In 2025, Automatic Transfer Switch held a dominant market position in the By Type segment of the Transfer Switch Market, with a 65.4% share. Facilities managing critical loads — data centers, hospitals, telecom towers — cannot rely on personnel to manually restore power during outages. This operational requirement locks in ATS adoption across high-stakes applications.

Manual Transfer Switch serves as the cost-accessible entry point for residential and small commercial buyers. Operators with lower uptime requirements and budget constraints choose manual systems to reduce installation costs. However, as building automation expands into mid-market commercial properties, manual systems face displacement pressure from increasingly affordable ATS alternatives.

Mode Analysis

Open Transition Mode dominates with 40.8% due to cost efficiency and straightforward installation.

In 2025, Open Transition Mode held a dominant market position in the By Mode segment of the Transfer Switch Market, with a 40.8% share. This mode briefly disconnects the load before switching to the backup source, eliminating the need for synchronization hardware. For most commercial and light industrial applications, this momentary interruption is acceptable, making open transition the default choice for cost-conscious buyers.

Closed Transition Mode differentiates through momentary source paralleling, enabling a seamless transfer with zero interruption. This mode carries a higher price point but addresses the requirements of sensitive electronic equipment and process-critical loads where even milliseconds of power gap cause equipment faults or data corruption.

Soft Load Transition Mode allows load to be gradually transferred between sources, reducing the mechanical and electrical stress on connected equipment. This mode appeals most to facilities operating precision machinery or large motor loads, where sudden source transitions create damaging current spikes.

Delayed Transition Mode introduces a timed pause between source disconnection and reconnection. This approach protects equipment in environments where voltage residuals need time to decay before the new source engages, particularly relevant in motor-heavy industrial settings with legacy rotating equipment.

Voltage Rating Analysis

Medium (300A–1600A) dominates with 45.6% due to broad commercial and industrial applicability.

In 2025, Medium Voltage Rating (300A–1600A) held a dominant market position in the By Voltage Rating segment of the Transfer Switch Market, with a 45.6% share. This range aligns with the power requirements of most commercial buildings, mid-size industrial facilities, and institutional campuses. The segment captures the largest addressable base of buyers, making it the volume leader by a wide margin.

Low Voltage Rating (less than 300A) carries the highest margin within the residential and small commercial sub-market. Simpler installation requirements and compatibility with standard electrical panels drive adoption among homeowners adding standby generator capability. The residential retrofit opportunity continues to grow as home backup power systems become more mainstream.

High Voltage Rating (more than 1600A) serves as the solution layer for large industrial plants, utility substations, and hyperscale data center campuses. These systems require specialized engineering and longer procurement cycles, which limits volume but supports premium pricing. Buyers in this segment prioritize transfer speed and reliability over cost, driving specification-led purchasing decisions.

Application Analysis

Industrial dominates with 45.6% due to zero-downtime production requirements.

In 2025, Industrial held a dominant market position in the By Application segment of the Transfer Switch Market, with a 45.6% share. Manufacturing lines, processing plants, and mining operations face direct financial losses from unplanned outages. This operational exposure makes transfer switch investment non-discretionary for industrial operators managing continuous or near-continuous production cycles.

Residential applications represent the fastest-expanding buyer category outside the industrial base. Homeowners in regions with frequent grid disruptions are investing in standby generator systems, creating consistent demand for residential-grade automatic transfer switches. In January 2025, Generac introduced a new automatic transfer switch design with integrated surge protection for home standby generator systems, directly targeting this growth segment.

Commercial applications span office buildings, retail centers, hotels, and healthcare facilities requiring reliable emergency power management. Building code requirements for emergency lighting, life safety systems, and data continuity mandate transfer switch installation in most new commercial construction. This regulatory floor supports steady baseline demand even during economic slowdowns.

Key Market Segments

By Type

- Automatic Transfer Switch

- Manual Transfer Switch

By Mode

- Open Transition Mode

- Closed Transition Mode

- Soft Load Transition Mode

- Delayed Transition Mode

By Voltage Rating

- Low (less than 300A)

- Medium (300A–1600A)

- High (more than 1600A)

By Application

- Industrial

- Residential

- Commercial

Drivers

Grid Instability and Data Center Expansion Force Rapid Deployment of Automatic Transfer Switch Systems

Power outages in commercial and industrial facilities no longer represent occasional disruptions — they represent measurable revenue losses and operational liabilities. Data centers, hospitals, and telecom networks require uninterrupted power delivery, making automatic transfer switch systems a procurement priority rather than a capital planning afterthought. This operational imperative directly expands the addressable market for high-specification switching solutions.

According to the Vertiv PowerIT Rack Transfer Switch Installer/User Guide (2025), the Vertiv PowerIT Rack Transfer Switch delivers a typical total transfer time of 4 to 8 ms using hybrid switching topology. This millisecond-range response is what makes modern ATS systems viable for data center infrastructure, where connected servers and storage arrays cannot tolerate longer interruptions without triggering automatic shutdowns.

Commercial building construction — including hospitals and office campuses — adds a structural demand layer on top of data center growth. Emergency power transfer requirements embedded in building codes mandate ATS installation in new construction across most developed markets. Consequently, every new commercial build creates a guaranteed procurement event, providing vendors with predictable pipeline volume regardless of macro conditions.

Restraints

High Installation Costs and Technical Complexity Slow Adoption in Price-Sensitive Market Segments

Advanced automatic transfer switch systems require not just hardware investment but also engineering assessment, electrical panel upgrades, and integration with existing generator or renewable backup infrastructure. For small commercial operators and residential buyers, this total installed cost creates a meaningful adoption barrier that keeps many facilities on older manual switching solutions.

Technical complexity compounds the cost issue. Proper ATS integration requires qualified electrical contractors familiar with load calculation, transfer timing parameters, and compliance standards. According to the Borri-Legrand STS brochure published January 2025, STS 16-32 models support overload capacity of 125% for 1 minute, 150% for 30 seconds, and 200% for 5 seconds — specifications that demand precise installation and commissioning to function safely and reliably.

The shortage of trained technicians capable of correctly installing and maintaining high-specification transfer switch systems restricts deployment velocity, particularly in developing markets. This skills gap benefits established vendors with certified installer networks but creates a real ceiling on how quickly the market can absorb new deployments across the mid-market and emerging economy segments.

Growth Factors

Renewable Energy Integration and Smart Infrastructure Investment Open New Revenue Streams for Transfer Switch Vendors

Solar, wind, and battery storage installations create a direct need for transfer switch systems capable of managing multiple power sources simultaneously. As renewable energy adoption accelerates across commercial and industrial facilities, the demand for advanced switching solutions that can arbitrate between grid, generator, and stored energy sources grows in parallel. This dynamic fundamentally expands the transfer switch use case beyond traditional backup power.

According to E3S Web of Conferences, Volume 601, Article 00088 (January 2025), in a hybrid PV-generator system managed by ATS with 6 batteries, fuel consumption drops to 0.032 liters compared to a full-generator baseline of 2.147 liters, delivering 2.115 liters of fuel savings per 8-hour operation. This efficiency outcome makes ATS technology a business-grade energy cost management tool, not merely a safety device — a repositioning that expands the buyer base significantly.

Microgrid infrastructure investment and EV charging network expansion add further revenue opportunities. Vertiv’s hot-standby controller, which enables zero downtime during firmware updates and processor resets, exemplifies how smart transfer switch functionality now addresses the uptime requirements of complex distributed energy environments. Vendors offering IoT-enabled, remotely monitored switching systems are positioned to capture premium pricing in these next-generation infrastructure segments.

Emerging Trends

Digital Controls, Modular Designs, and Smart Grid Integration Redefine Transfer Switch Performance Standards

Transfer switch buyers now expect real-time monitoring, remote diagnostics, and predictive maintenance capability as standard features rather than premium add-ons. Digital control interfaces and IoT connectivity transform transfer switches from passive switching devices into active power management nodes within facility energy systems. This expectation shift rewards vendors who invest in software capability alongside hardware engineering.

According to the Borri-Legrand STS brochure published January 2025, the STS 300 series achieves a transfer time of ≤4 ms, reflecting how hardware improvements now complement digital control advances. Simultaneously, compact and modular transfer switch designs address the space constraints of hyperscale data centers and urban commercial installations, where rack-mounted and front-access systems reduce footprint without sacrificing performance.

In July 2025, ABB introduced the new Zenith T-series Service Entrance Rated Automatic Transfer Switch (30–1200 A) with integrated TruONE Technology and true voltage agnostic design. This product direction signals the industry’s movement toward all-in-one modular systems that simplify installation while meeting the technical demands of mixed-source power environments. Early movers offering such integrated solutions gain specification advantages in commercial and industrial procurement cycles.

Regional Analysis

Asia Pacific Dominates the Transfer Switch Market with a Market Share of 38.6%, Valued at USD 0.8 Billion

Asia Pacific commands 38.6% of the global transfer switch market, valued at USD 0.8 Billion. Rapid industrialization in China, India, and Southeast Asia, combined with chronically unreliable grid infrastructure in many developing economies across the region, creates persistent structural demand. High-volume manufacturing expansion and data center construction in tier-two cities further reinforce this regional leadership position.

North America Transfer Switch Market Trends

North America maintains a strong transfer switch base driven by mature data center infrastructure, stringent building code requirements for emergency power, and high per-facility investment capacity. The U.S. market benefits from an established ecosystem of generator manufacturers, electrical contractors, and facility managers familiar with ATS procurement and maintenance. Aging grid infrastructure in several U.S. regions adds urgency to backup power investment.

Europe Transfer Switch Market Trends

Europe’s transfer switch demand reflects its advanced industrial base and tightening energy resilience standards for critical facilities. Germany, the UK, and France lead procurement driven by data center expansion and healthcare facility upgrades. The region’s push toward renewable energy integration also creates new requirements for multi-source transfer switching, supporting demand for more sophisticated switching architectures beyond traditional generator backup.

Latin America Transfer Switch Market Trends

Latin America presents consistent demand anchored in Brazil and Mexico, where grid reliability challenges in industrial zones drive investment in backup power infrastructure. Mining, oil and gas, and food processing facilities in the region represent the core buyer base. Growth in commercial construction in major urban centers adds a secondary demand layer for mid-range automatic transfer switch systems in new building projects.

Middle East and Africa Transfer Switch Market Trends

The Middle East and Africa region sees transfer switch demand concentrated in GCC countries, where large-scale infrastructure projects, data centers, and commercial real estate development require reliable emergency power switching. South Africa’s well-documented grid instability issues generate consistent demand across industrial and commercial segments. Ongoing energy infrastructure investment across the Gulf Cooperation Council creates a durable procurement base for advanced switching systems.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

ABB positions itself at the intersection of power management hardware and digital grid integration. Its July 2025 launch of the Zenith T-series Service Entrance Rated ATS (30–1200 A) with TruONE Technology and voltage-agnostic design reflects a deliberate strategy to capture the modular, all-in-one market segment. This approach reduces installation complexity for commercial buyers and strengthens ABB’s position in specification-led procurement.

AEG Power Solutions builds its competitive base on industrial-grade power continuity systems, targeting facilities where operational continuity directly ties to financial performance. Its engineering focus on heavy-duty applications positions the company in procurement cycles where technical specification depth outweighs price competition. This specialization creates customer stickiness but also limits addressable volume compared to broader-portfolio competitors.

Briggs & Stratton leverages its established generator brand to drive transfer switch adoption in the residential and light commercial segments. The company’s distribution strength through home improvement retail and dealer networks gives it structural reach into buyer categories that larger industrial-focused players do not efficiently serve. This channel advantage supports consistent volume even as the residential backup market matures.

Caterpillar integrates transfer switch solutions within its broader power systems portfolio, enabling bundled procurement for large industrial and infrastructure clients. Caterpillar’s global service network and long-term maintenance contracts create switching system stickiness beyond the initial sale. In June 2025, Advent International’s acquisition of LayerZero Power Systems — a leading U.S. static transfer switch manufacturer — signals that private equity now views the mission-critical power switching segment as a high-value standalone business, intensifying competitive pressure on established players like Caterpillar.

Key Players

- ABB

- AEG Power Solutions

- Briggs & Stratton

- Caterpillar

- Cummins

- Eaton

- General Electric (GE)

- Generac Power Systems

- Kohler

- Midwest Electric Products

- Schneider Electric

- Siemens

- Vertiv Group

- Netrack

- Insel Rectifier (India) Pvt. Ltd.

- Other Key Players

Recent Developments

- January 2025 — Legrand, via Borri, released the new STS 16-32 (1-phase, 16–32 A rackmount) and STS 300 series static transfer switches. Key features include zero switching time, dual redundant power supplies, redundant cooling with fan failure monitoring, real-time SCR fault sensing, and high overload capacity — targeting data center operators requiring maximum power continuity assurance.

- May 2025 — Vertiv launched the enhanced Vertiv PowerSwitch 7000 static transfer switch with internally redundant architecture, compartmentalized high-voltage design, modular SCRs, hot-swappable fans, and a 9-inch color touchscreen with high-sampling waveform capture. The system also carries UL2900-1 cybersecurity certification for remote monitoring, addressing the data center sector’s tightening cybersecurity requirements for networked power infrastructure.

- June 2025 — Advent International signed a definitive agreement to acquire majority shareholding in LayerZero Power Systems, a leading U.S. manufacturer of static transfer switches and power management products for data centers and mission-critical applications. Founders retain minority holdings; deal closing was targeted for Q3 2025, signaling institutional investor confidence in the mission-critical power infrastructure segment.

- July 2025 — ABB introduced the Zenith T-series Service Entrance Rated Automatic Transfer Switch (30–1200 A) featuring integrated TruONE Technology, true voltage agnostic design, and modular all-in-one construction. The product targets commercial and light industrial facilities requiring compact critical power protection with simplified installation and long-term serviceability.

Report Scope

Report Features Description Market Value (2025) USD 2.3 Billion Forecast Revenue (2035) USD 4.2 Billion CAGR (2026-2035) 6.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Automatic Transfer Switch, Manual Transfer Switch), By Mode (Open Transition Mode, Closed Transition Mode, Soft Load Transition Mode, Delayed Transition Mode), By Voltage Rating (Low, Medium, High), By Application (Industrial, Residential, Commercial) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape ABB, AEG Power Solutions, Briggs & Stratton, Caterpillar, Cummins, Eaton, General Electric (GE), Generac Power Systems, Kohler, Midwest Electric Products, Schneider Electric, Siemens, Vertiv Group, Netrack, Insel Rectifier (India) Pvt. Ltd., Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- ABB

- AEG Power Solutions

- Briggs & Stratton

- Caterpillar

- Cummins

- Eaton

- General Electric (GE)

- Generac Power Systems

- Kohler

- Midwest Electric Products

- Schneider Electric

- Siemens

- Vertiv Group

- Netrack

- Insel Rectifier (India) Pvt. Ltd.

- Other Key Players

Our Clients

- 181451

- Mar 2026