Quick Navigation

Report Overview

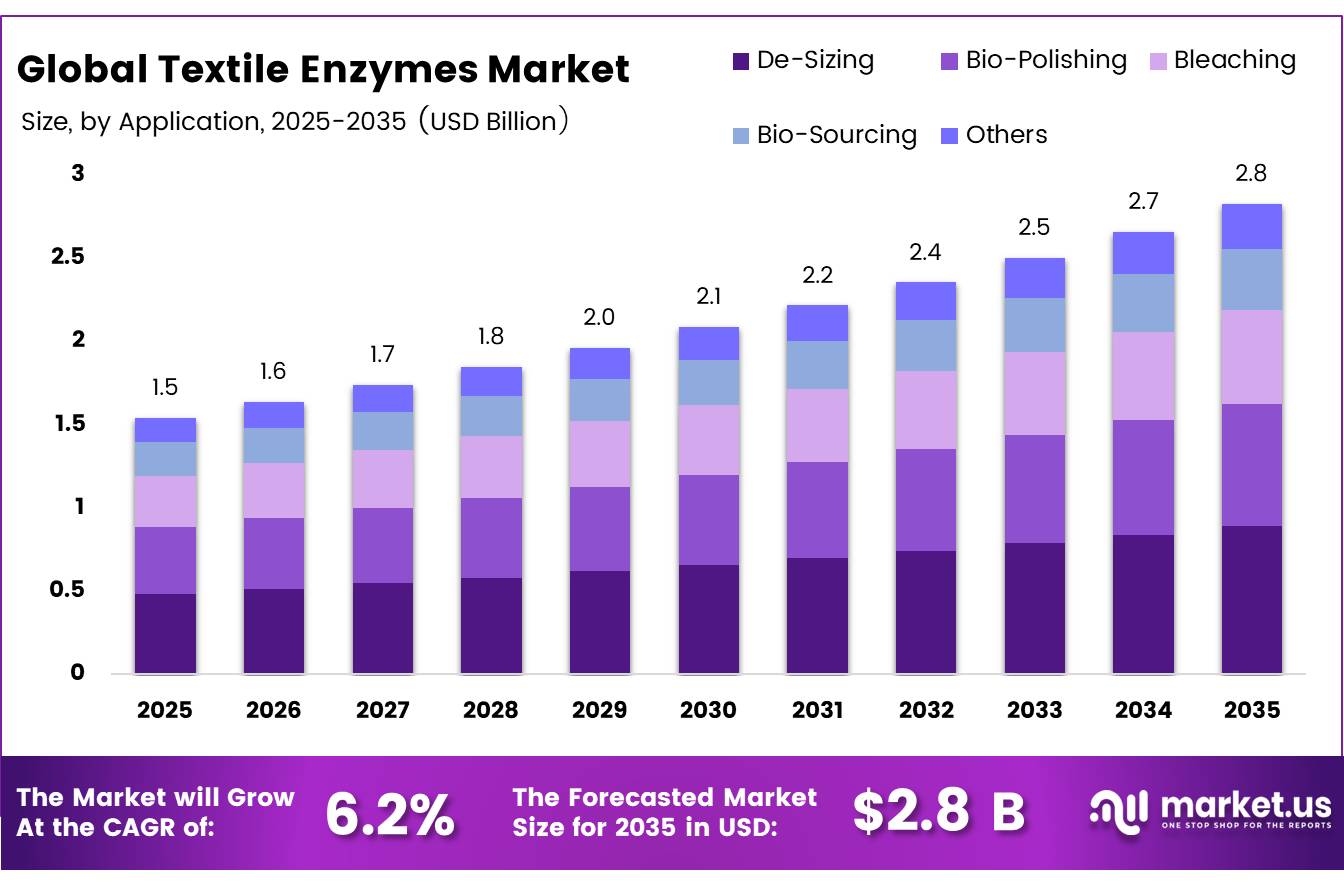

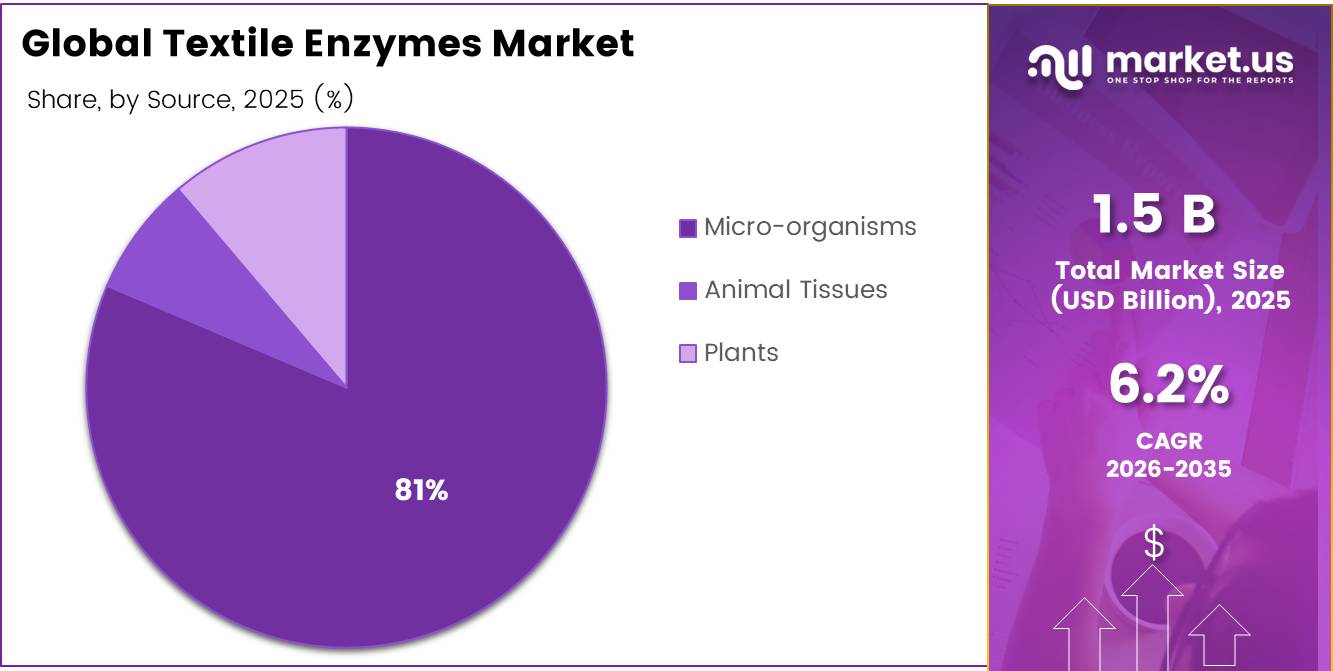

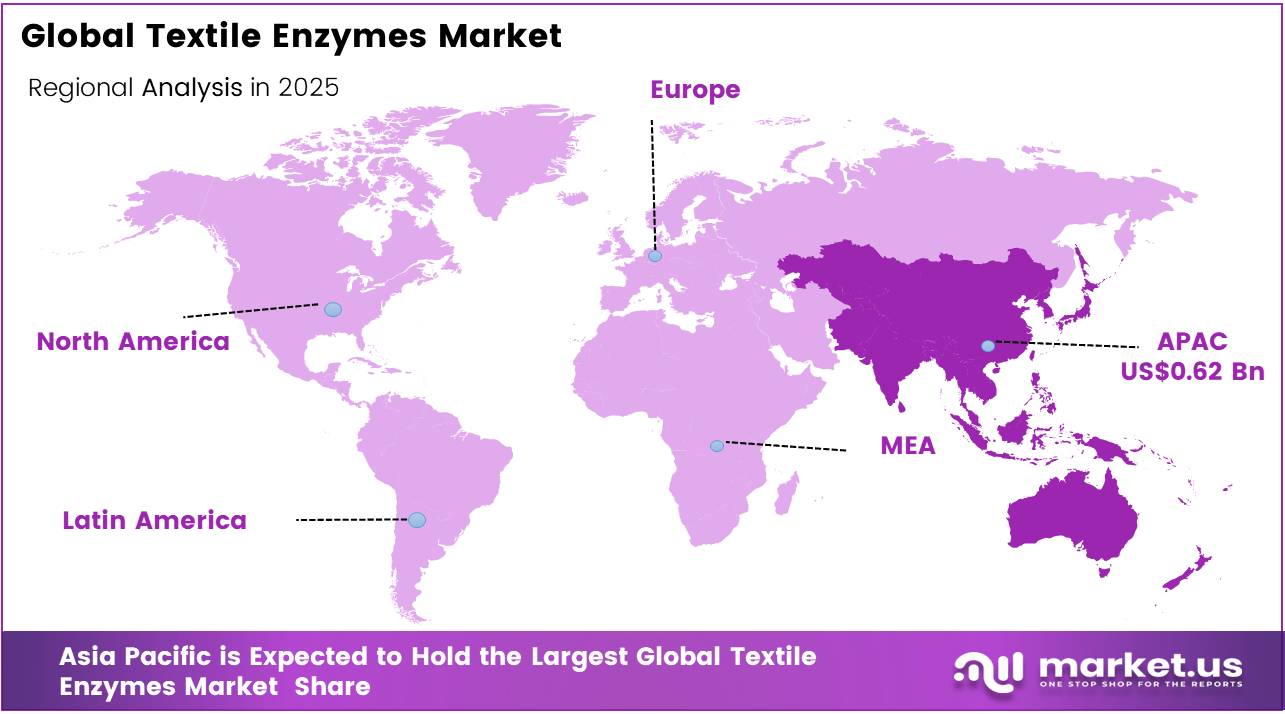

In 2025, the Global Textile Enzymes Market was valued at USD 1.5 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 6.2%, reaching about USD 2.8 billion by 2035. In 2025, Asia Pacific led the market, achieving over 40.5% share with a revenue of USD 0.62 Billion.

The textile enzyme is a vital component of the industrial biotechnology value chain, facilitating sustainability and efficiency in desizing, bio-polishing, scouring, bleaching, and dyeing processes by substituting traditional chemically intensive processes. The demand is highly dependent on the growth of textile and apparel manufacturing worldwide with an ever-increasing emphasis on the performance of fabric qualities, efficient use of water, and environmental compliance.

- As per United Nations Environment Programme, the textile industry is responsible for 2-8% annual greenhouse gas emissions globally and uses 215 trillion liters of water per year, a majority of which is used in water-intensive chemical processes.

Key Takeaways

- The Textile Enzymes market was valued at USD 1.5 billion in 2025.

- The global Textile Enzymes market is projected to grow at a CAGR of 6.2% and is estimated to reach USD 2.8 billion by 2035.

- On the basis of source, Micro-organisms dominated the market, constituting 81.4% of the total market share.

- Based on the type, the Cellulase dominated the Textile Enzymes market, with a substantial market share of around 28.6%.

- Based on the Application, De-Sizing led the market, comprising 31.5% of the total market.

- In 2025, the Asia Pacific was the most dominant region in the global textile enzymes, accounting for 40.5% of the total global consumption.

According to World Trade Organization the production and consumption of textile enzymes are largely centered in the Asia Pacific region, where the share of China’s textile exports rose to 43.3% in 2024. Europe and North America have made progress in enzyme technology development and regulation. Next-generation innovations involve the development of thermostable, pH-stable, and multienzyme technologies.

- Law No. 2025-188 of France introduced in February 2025 banning PFAS-containing textiles and footwear starting 2026 and later all textiles in 2030, thus pushing the demand for enzymes globally. Eurofins

Textile Enzymes Market Segmentation

Source Analysis

Micro Organisms represents dominant Segment in the Market.

Micro-organisms are the dominant sources segment, with an 81.4% share, owing to excellent scalability, economical costs, and adaptability across processes like desizing, bio-polishing, scouring, and bleaching. Their capability of being quickly cultivated, genetically engineered to provide more specific functionality, and manufactured on a large scale make them the ideal sources for textile wet processing operations.

Many regional authorities in the Asia Pacific are now supporting the use of microbial biotechnologies and clean manufacturing, such as the Indian government with its BioE3 policy launched in August 2024. These policies have directly led to investment in facilities manufacturing microbial enzymes in significant textile-producing nations.

Plants Are the Fastest Growing Sources Segment in the Textile Enzymes Market , plant enzymes have emerged as the fastest-growing sources due to their growing adoption in specialty fabrics and natural fibers, where environmental and purity benefits matter greatly under stringent export regulations.

Type Analysis

Cellulases a significant type.

The market shares for cellulases accounts largest among all types of textile enzymes, occupying a 28.6% share due to their heavy use in various bio-polishing, bio-finishing, and bio-stoning processes used in the processing of cotton and cellulosic fibers. With their high effectiveness in producing smooth surfaces on fabrics, preventing pilling, and replicating stone-washed effects without the need for any pumice stones, cellulases are considered an essential product in producing both general and high-end denims. Based on USDA reports, there was a growth of 1% in India’s textile production and 5% increase in India’s apparel production in December 2024 compared to the previous year.

Pectinases was the fastest growing type in the textile enzymes. The total volume and showing the fastest growth as they gain rapid popularity in bio scouring processes where pectinases replace chemical scouring of cotton substrates. Based on USDA Foreign Agricultural Services reports, India is expected to consume 25 million 480 lb. bales of cotton mills in the marketing year 2024-25, two percent more than what had been previously projected due to robust global demand for yarns and textiles.

Application Analysis

Desizing Are the Most Widely Used Application.

Desizing leads as the dominant application segment in the textile enzymes market with a 31.5% share due to its essential role in removing starch-based sizing agents from fabrics before dyeing and finishing. Enzymatic desizing improves fabric absorbency, reduces harsh chemical use, lowers water consumption, and supports smoother processing, making it widely preferred by textile manufacturers seeking efficient and sustainable pretreatment.

Bio-Scouring Is the Fastest-Growing Application Segment in the Textile Enzymes Market, bio-scouring segment has become the fastest-growing in the market, reflecting the increasing shift away from the use of chemicals that require alkalis in the scouring process. New EU environmental regulations for textile wet processing target three processes are bleaching, dyeing, and finishing and regulate the emission of 20 pollutants, both air and water, including formaldehyde and metal, thus forcing the manufacturers to replace chemical with bio scouring (pectinase based).

Key Market Segments

By Source

- Animal Tissues

- Plants

- Micro-organisms

By Type

- Amylases

- Cellulase

- Lipases

- Proteases

- Pectinases

- Laccases

- Others

By Application

- De-Sizing

- Bio-Polishing

- Bleaching

- Bio-Sourcing

- Others

Driver Analysis

Water-energy cost savings in pretreatment and finishing

In 2026, textile mills are adopting enzymes mainly to lower operating costs and improve production efficiency. Industry evaluations indicate that fully enzymatic processing can reduce water use by about 70%, steam consumption by 33%, energy use by 27%, and combined input costs by nearly 66%. Processing time may also fall by 23%–30%, depending on fabric shade and process conditions. These savings are encouraging mills to use enzymes not only as specialty chemicals, but also as practical tools for reducing utility costs, shortening production cycles, and improving margins in mainstream cotton and blended-fabric processing.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance shift to low-residue wet processing | +1.4% | EU core, North America compliance lanes, Turkey, China export hubs | Short term (≤ 2 years) |

| Water-energy cost savings in pretreatment and finishing | +1.2% | South Asia core, China, Southeast Asia, MENA processing clusters | Short term (≤ 2 years) |

| PFAS and restricted chemistry replacement in textile value chains | +0.9% | EU, France, California-linked supply chains, technical textile spill-over | Medium term (2-4 years) |

| Export competitiveness of Bangladesh-India-Pakistan wet processing | +0.8% | South Asia core, EU and US sourcing corridors | Short term (≤ 2 years) |

| Traceability and product data requirements under textile sustainability rules | +0.7% | EU-led value chains, global brands, APAC supplier networks | Medium term (2-4 years) |

| Natural fiber quality upgrading and fabric performance differentiation | +0.6% | India, Pakistan, China, Turkey, Latin America spill-over | Medium term (2-4 years) |

Restraint Analysis

Weak apparel demand

Weak downstream apparel and home-textile offtake remains the largest restraint because textile enzymes are consumed only when mills are running enough pretreatment, desizing, biopolishing, and finishing volume to justify recipe conversion and technical trials. In practical terms, when retailer replenishment is weak and export orders are placed closer to season, mills cut batch experimentation, delay chemistry substitution, and preserve working capital, which can defer enzyme adoption by 6 to 12 months and trim approximately 1.4 percentage points from baseline sector CAGR in 2026–2028 across EU-linked and US-linked sourcing corridors.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weak apparel demand | -1.4% | EU core, North America, China, South Asia export lanes | Short term (≤ 2 years) |

| High enzyme cost base | -1.1% | EU core, China, India, Southeast Asia | Short term (≤ 2 years) |

| Long mill approvals | -1.0% | South Asia core, China, Turkey, MENA | Medium term (2-4 years) |

| Tight mill margins | -0.9% | Bangladesh, India, Pakistan, Vietnam | Short term (≤ 2 years) |

| Trade-policy shocks | -0.7% | EU, APAC corridors, China-linked supply chains | Medium term (2-4 years) |

| Compliance proof burden | -0.6% | EU, North America, global brand networks | Medium term (2-4 years) |

Opportunity Analysis

Enzymes for textile recycling

Textile recycling represents a future opportunity for enzyme suppliers rather than a major current demand driver. The EU’s revised Waste Framework Directive took effect in October 2025, giving member states 20 months to transpose the rules and 30 months to establish textile EPR schemes. If 3%–5% of separately collected EU textile waste enters enzyme-supported recycling by 2030, suppliers could create a new mid-double-digit million-dollar market. Enzymes may support cotton-blend separation, cellulose recovery, and contaminant removal while delivering gross margins around 300–600 basis points above conventional textile auxiliaries.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Enzymes for textile recycling | +1.7% | EU core, North America, Japan, South Korea, China | Medium term (2-4 years) |

| Traceability-linked premium platforms | +1.3% | EU, premium APAC exporters, North America brands | Short term (≤ 2 years) |

| Technical textiles expansion | +1.1% | India, China, Germany, Turkey, Southeast Asia | Medium term (2-4 years) |

| Denim finishing system bundles | +0.9% | Bangladesh, Pakistan, India, Turkey, Mexico | Short term (≤ 2 years) |

| Asset-light contract fermentation | +0.8% | India, China, Southeast Asia, EU spill-over | Short term (≤ 2 years) |

| Private-label roll-up channels | +0.7% | India, Bangladesh, Vietnam, Indonesia, MENA | Medium term (2-4 years) |

Challenges Analysis

Logistics and cold-chain complexity

Logistics remains a continuing challenge for textile enzyme suppliers because temperature-sensitive products require tighter storage, tracking, and delivery controls than standard textile chemicals. Port congestion, 3–5°C temperature deviations, or delivery delays of 5–7 days can reduce shelf life and product consistency. Suppliers therefore need larger regional inventories, better packaging, and real-time monitoring, which may add 1–2 percentage points to logistics costs and increase working-capital requirements. Until cold-chain infrastructure and tracking systems improve, these pressures could reduce the market’s achievable CAGR by around 1 percentage point.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Mill capability gap | -1.2% | South Asia core, China, Turkey, MENA | Long term (≥ 4 years) |

| Logistics and cold-chain complexity | -1.0% | APAC logistics corridors, EU hubs, North America | Medium term (2-4 years) |

| Regulatory maze and overlap | -0.9% | EU regulatory hubs, UK, North America brands | Long term (≥ 4 years) |

| Application talent bottleneck | -0.8% | India, Bangladesh, Vietnam, China, EU | Medium term (2-4 years) |

| Integration with recycling flows | -0.7% | EU, North America, Japan, South Korea | Long term (≥ 4 years) |

| ESG data and greenwashing risk | -0.6% | EU, US, UK, global brand networks | Medium term (2-4 years) |

Geopolitical Impact Analysis

Geopolitical Realignment and Supply Chain Fragmentation Reshaping Textile Enzymes Manufacturing.

Current geopolitical tensions are reshaping the textile enzymes market through supply chain concentration risks, trade restrictions, and accelerated sourcing diversification across global textile manufacturing ecosystems. According to World Trade Organization (WTO) data, China’s share in global textile exports rose to 43.3% in 2024, maintaining dominant positions across upstream fiber, yarn spinning, and wet processing input supply chains. Since enzyme consumption is closely integrated with textile wet processing, disruptions in cotton supply and chemical inputs directly affect enzyme procurement and investment planning.

- As per the USDA Foreign Agricultural Service, Cotton and Products Annual, April 2025, Xinjiang accounted for approximately 92.3% of China’s total cotton production in MY 2024-25 a record high compelling global textile manufacturers to accelerate supply chain diversification toward India, Bangladesh, and Vietnam, where enzyme-based sustainable processing adoption is intensifying under both export compliance requirements and domestic environmental mandates

Escalating tariff measures are accelerating sourcing realignment. In 2024, the U.S. imported approximately USD 107.72 billion in textiles and apparel, with China accounting for USD 26.07 billion or 24.2% total imports, a supply base now subject to rising tariff and compliance pressures compelling manufacturers to diversify toward India, Vietnam, and Bangladesh markets where enzyme-based sustainable processing adoption is accelerating under export compliance and domestic environmental mandates. However, concentrated control over cotton and chemical processing infrastructure continues to expose enzyme supply chains to raw material volatility and regulatory uncertainty globally.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Textile Enzymes Market.

The Asia Pacific is considered as the leading region with the market share of 40.5% in the textile enzymes market owing to the largest concentration of textile manufacturing facilities located in China, India, Bangladesh, and Vietnam. Additionally, India reported total textile and garment exports of USD 36.6 billion in FY 2025 aided by a national budget of USD 635.2 million for a five-year cotton mission aimed at increasing productivity and tracing supply chains. Large-scale cotton wet processing in this region contributes significantly towards enzyme usage in desizing, bio polishing, and scouring processes.

Latin America Is the Fastest Growing Region in the Textile Enzymes Market and holds 18% of the market share as investments in textile manufacturing continue to rise across the country including Brazil, Mexico, and Colombia. In 2024, Mexico and Brazil were the leaders in the production of textile finishing agents which made up most of the 852,000 tonnes produced in Latin America and the Caribbean. In June 2024, Brazil announced its National Circular Economy Strategy that aims to transform the textile industry into a sustainable and low-carbon business environment.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Enzyme manufacturers in the textile industry concentrate on enhancing their competitive edge through technological differentiation, production efficiency, and supply chain coordination. One of the crucial objectives is to innovate enzymes regularly and create thermophilic, pH-resistant, and multienzyme cocktails that enhance operational efficiency, fabric quality, and water savings in simultaneous desizing, scouring, and biological polishing processes. Asian governments are increasingly encouraging biotechnological applications and environmentally friendly manufacturing methods. In India, the BioE3 policy launched in August 2024 aims at expanding specialty chemicals and enzyme-based manufacturing in an industrially significant way.

Capacity expansion in Asia Pacific creates a basis for the alignment of demand for the textile industry. The investment under India’s PLI scheme in 14 sectors, including the textile industry, totaled approximately USD 18.72 billion up until November 2024, leading to production and sales of about USD 162.84 billion. Press Information Bureau

IP management becomes imperative in establishing customer loyalty through patents and long-term cooperation with major textile manufacturers. As per India’s Union Budget 2025-26, more than 80% of textile capacity utilization belongs to MSMEs, indicating an enormous opportunity for enzyme providers with cost-effective and scalable products.

The Major Players in The Industry

- Novozymes

- BESTZYME BIO-ENGINEERING CO., LTD.

- AB Enzymes

- BASF SE

- DENYKEM

- DSM

- Kemin Industries, Inc.

- Advanced Enzyme Technologies

- Ultreze

- EPYGEN LABS LLC.

- Sunsong Industry Group Co., Ltd.

- Noor Enzymes

- Antozyme Biotech Pvt. Ltd.

- Nature BioScience Pvt. L.T.D.

- Tex Biosciences (P) Ltd.

- Infinita Biotech Private Limited

- Other Key Players

Key Development

- In January 2025, the merger between Novozymes and Chr. Hansen was successfully executed resulting in the formation of Novonesis. The merger immediately enhances the capability of Novonesis in the textile enzymes market due to increased R&D capacity and wider application areas like cellulases, proteases, and amylases.

- In February 2025, Novonesis unveiled its novel enzyme-based carbon capture technology in industries such as textile production. It uses biodegradable enzymes in place of chemicals to capture over 90% of carbon emissions produced in flue gases.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.5 Bn |

| Forecast Revenue (2035) | USD 2.8 Bn |

| CAGR (2026-2035) | 6.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Source (Animal Tissues, Plants, Micro-organisms), By Type (Amylases, Cellulase, Lipases, Proteases, Pectinases, Laccases, Others), By Application (De-Sizing, Bio-Polishing, Bleaching, Bio-Sourcing, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Novozymes, BESTZYME BIO-ENGINEERING CO., AB Enzymes, BASF SE, DENYKEM, DSM, Kemin Industries, Inc., Advanced Enzyme Technologies, Ultreze, EPYGEN LABS LLC., Sunsong Industry Group Co., Ltd., Noor Enzymes, Antozyme Biotech Pvt. Ltd., Nature BioScience Pvt. L.T.D., Tex Biosciences (P) Ltd., Infinita Biotech Private Limited, Other Key Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |