Quick Navigation

Report Overview

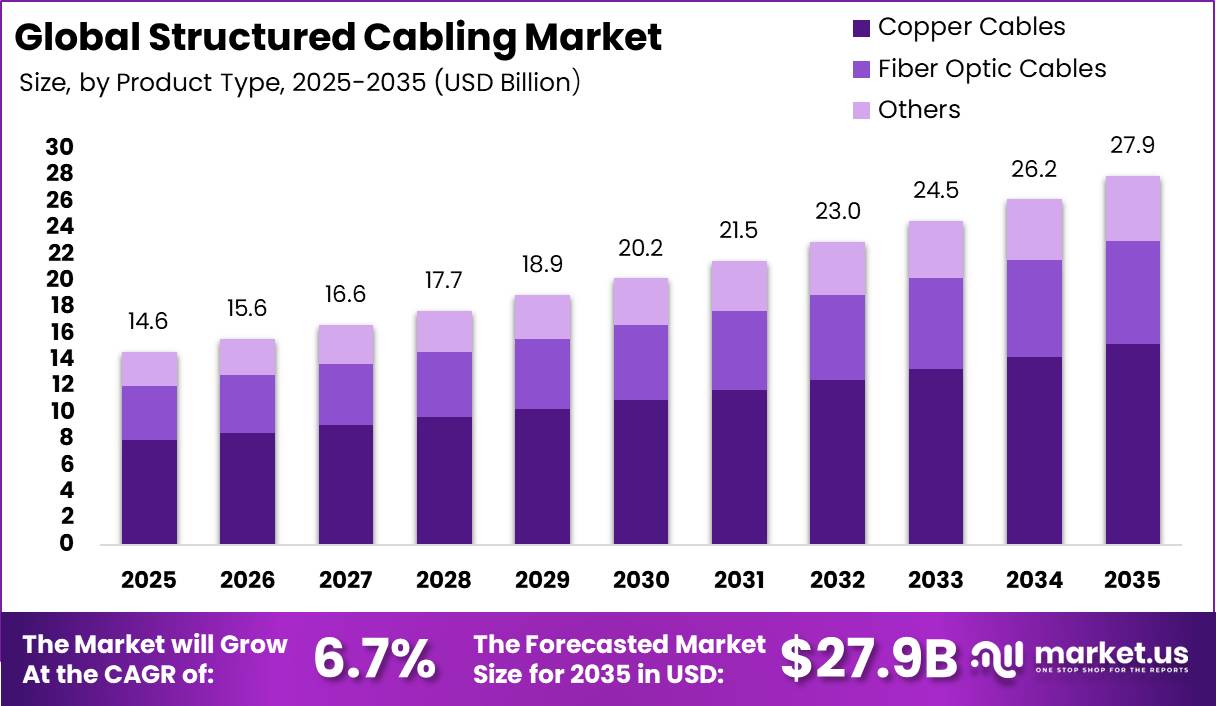

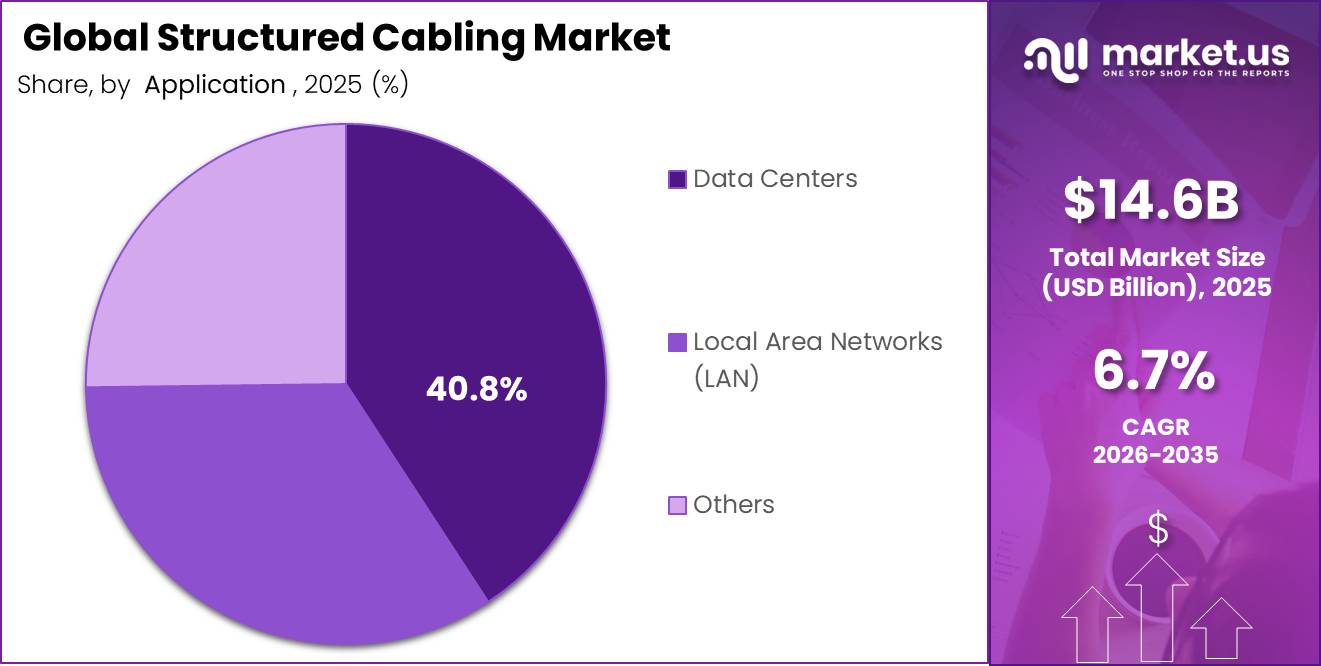

Global Structured Cabling Market size is expected to be worth around USD 27.9 Billion by 2035 from USD 14.6 Billion in 2025, growing at a CAGR of 6.7% during the forecast period 2026 to 2035. This trajectory reflects sustained capital allocation toward physical network infrastructure across data centers, enterprise campuses, and public sector facilities worldwide.

The structured cabling market covers the complete physical layer of network infrastructure, including copper cabling systems, fiber optic assemblies, patch panels, cable management hardware, and connectivity components. The market serves data centers, enterprise LAN environments, government facilities, industrial sites, and residential and commercial buildings. Vendors compete across product supply, system design, and installation services.

Key Takeaways

- The global Structured Cabling Market was valued at USD 14.6 Billion in 2025 and is forecast to reach USD 27.9 Billion by 2035.

- The market is growing at a CAGR of 6.7% during the forecast period 2026 to 2035.

- By Product Type, Copper Cables dominate with a 54.4% share in 2025.

- By Application, Data Centers hold the largest share at 40.8% in 2025.

- By End-Use Industry, the Government segment leads with a 39.0% share in 2025.

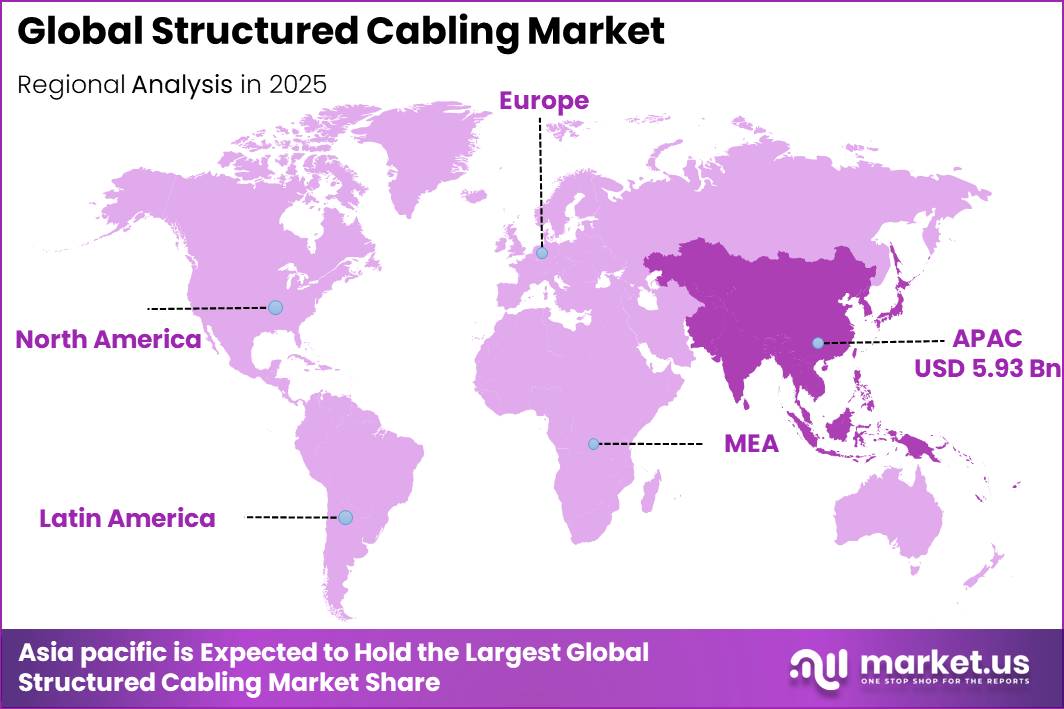

- Asia Pacific is the dominant region with a 40.5% market share, valued at USD 5.93 Billion in 2025.

As per our research, the AI data center build-out driver carries a +2.4% impact on the CAGR forecast. Hyperscale operators are redirecting capital into GPU-intensive campuses that require denser east-west connectivity and lower-loss backbone architectures. This creates a direct revenue shift toward higher-value fiber assemblies and pre-terminated trunk systems for cabling vendors.

As per our research, 400G and 800G migration adds a further +1.9% to the CAGR outlook for structured cabling. Enterprise and carrier networks upgrading to these speeds require Category 6A, Category 8, and high-performance fiber refresh cycles. Vendors positioned in high-grade copper and fiber segments will capture the bulk of this upgrade spend.

In August 2025, Amphenol Corporation announced a definitive agreement to acquire CommScope’s Connectivity and Cable Solutions business for USD 10.5 Billion. This transaction significantly expands Amphenol’s structured cabling, fiber-optic connectivity, and data center infrastructure capabilities. This signals continued consolidation among Tier 1 players, raising barriers to entry for smaller regional vendors.

Product Type Analysis

Copper Cables dominates with 54.4% due to widespread enterprise LAN deployment legacy.

In 2025, Copper Cables held a dominant market position in the By Product Type segment of the Structured Cabling Market, with a 54.4% share. Copper infrastructure remains the default choice for horizontal LAN cabling in enterprise, government, and commercial buildings due to lower upfront cost and compatibility with Power over Ethernet applications. This entrenched installed base means copper replacement cycles, not only new builds, will sustain volume for the forecast period.

Fiber Optic Cables account for 28% of the product type segment. Fiber adoption is accelerating in backbone links, data center interconnects, and new builds requiring higher bandwidth density. This segment commands higher per-port revenue than copper, making it the primary margin-expansion lever for vendors investing in pre-terminated and high-fiber-count assembly capabilities.

The Others segment, covering patch panels, cable management systems, and connectivity hardware, holds a 17.6% share. These ancillary components generate recurring revenue through upgrades, replacements, and compliance-driven recertification projects. In November 2025, Business Communications, Inc. acquired NetLink Cabling Systems, expanding its integrated low-voltage and infrastructure solutions portfolio, signaling that bundled product and service models are becoming a competitive requirement in this sub-segment.

Application Analysis

Data Centers dominate with 40.8% due to hyperscale and AI infrastructure build programs.

In 2025, Data Centers held a dominant market position in the By Application segment of the Structured Cabling Market, with a 40.8% share. Hyperscale and colocation operators are deploying dense fiber backbone and high-speed copper cabling to support AI and cloud workloads. This segment offers the highest average revenue per project, making it the most strategically valuable application for structured cabling vendors targeting volume and margin simultaneously.

Local Area Networks account for 34.0% of the application segment. Enterprise LAN deployments span office buildings, campuses, hospitals, and educational institutions, generating steady replacement and upgrade demand. Category 6A and fiber LAN projects tied to 10G desktop and smart building PoE rollouts represent the primary growth vectors within this sub-segment over the forecast period.

The Others segment covers industrial networks, building automation, and telecom access infrastructure, holding a 25.2% combined share. Industrial Ethernet integration across smart factories and automated warehouses is expanding cabling density in this tier. Vendors that develop standardized cabling kits for industrial and edge environments can capture project volume that traditional enterprise-focused players are not yet equipped to serve.

End-Use Industry Analysis

Government dominates with 39.0% due to public digital infrastructure modernization programs.

In 2025, the Government segment held a dominant market position in the By End-Use Industry segment of the Structured Cabling Market, with a 39.0% share. Public sector agencies are modernizing campus networks, security systems, and administrative IT infrastructure through multi-year capital programs. This creates predictable, large-contract procurement cycles that favor certified vendors with compliance credentials and national-scale delivery capacity.

The IT and Telecommunication segment holds a 35.4% share. Telecom operators and IT service providers are upgrading backbone and access-layer cabling to support 400G and 800G network migrations. This end-use tier generates the highest fiber-to-copper revenue ratio, directly benefiting vendors with strong fiber assembly and pre-terminated product lines.

The Industrial segment accounts for 29.0% of end-use demand. Smart factory deployments and automated warehouse buildouts are integrating industrial Ethernet and ruggedized structured cabling into production environments. The Residential and Commercial segment holds 9.0%, while the Others category accounts for the remaining share, representing niche verticals including healthcare, hospitality, and higher-education campuses currently at earlier stages of structured cabling adoption.

Key Market Segments

By Product Type

- Copper Cables

- Fiber Optic Cables

- Others

By Application

- Data Centers

- Local Area Networks (LAN)

- Others

By End-Use Industry

- Government

- Industrial

- IT and Telecommunication

- Residential and Commercial

- Others

Market Dynamics

Market Opportunity Analysis - Underserved verticals and emerging regions offer structured entry points for vendors outside the hyperscale tier

The Industrial end-use segment holds a 29% share but remains structurally underserved by vendors optimized for enterprise and hyperscale environments. Smart factory and automated warehouse deployments require ruggedized cabling solutions that standard horizontal copper products do not address. Vendors that develop certified industrial Ethernet cabling systems can enter this segment without competing directly against Tier 1 players on price.

The Residential and Commercial segment accounts for only 9% of end-use demand, which signals early-stage penetration rather than low potential. Healthcare, hospitality, and higher-education campuses are expanding fiber-to-the-room infrastructure and PoE-enabled building systems at a pace that current structured cabling supply chains have not fully calibrated to serve. This segment offers above-average contract margins for vendors that position as integrated solution providers rather than product-only suppliers.

Latin America and the Middle East and Africa remain at earlier stages of infrastructure maturity relative to Asia Pacific and North America. GCC smart city programs and Brazil-Mexico enterprise LAN buildouts represent well-defined project pipelines that are not yet dominated by global Tier 1 vendors. New entrants with local installer partnerships and regionally certified product lines can establish first-mover positions in these markets before consolidation tightens competitive access.

Technology and Innovation Landscape - Pre-termination, automated infrastructure management, and fiber transition define the next competitive layer

Pre-terminated plug-and-play cabling solutions are reducing installation time and labor requirements across hyperscale and enterprise deployments. These factory-tested assemblies shift quality control from the job site to the manufacturing environment, lowering rework rates and accelerating project commissioning timelines. Vendors with pre-termination manufacturing capacity gain a cost and speed advantage over those relying on field-terminated installations for large-scale builds.

Automated Infrastructure Management platforms are enabling real-time network and cabling asset visibility across active installations. These systems integrate physical layer monitoring with IT management software, allowing operators to track port utilization, identify unauthorized changes, and plan capacity upgrades from a single interface. This technology layer converts structured cabling from a passive asset into a managed service opportunity, supporting higher-margin recurring revenue models for vendors and integrators.

The transition from copper backbone networks to end-to-end fiber structured cabling systems is progressing across data center and campus environments. Fiber delivers higher bandwidth density, lower signal loss over distance, and immunity to electromagnetic interference that copper cannot match in backbone applications. This shift benefits vendors with fiber assembly, pre-termination, and high-fiber-count trunk manufacturing capabilities, while putting pressure on copper-dominant portfolios to accelerate product line evolution.

Power over Ethernet utilization is expanding beyond phones and cameras into lighting control, occupancy sensing, and broader smart building automation endpoints. As per our research, 2025 industry guidance confirms PoE usage is extending to a wider range of building systems endpoints. This expansion increases cabling density per floor and creates demand for Category 6A and higher-rated horizontal runs that support PoE++ load requirements, giving vendors with certified high-performance copper products a direct revenue pathway into building upgrade budgets.

Drivers

The AI data center build-out is the primary near-term volume driver for the structured cabling market. As per our research, one 2026 industry estimate places infrastructure spending by the top five hyperscalers above USD 600 Billion, up 36% from 2025, with approximately USD 450 Billion directed at AI infrastructure. This capital concentration directly increases demand for dense fiber backbone systems, pre-terminated trunk assemblies, and high-speed copper upgrades at the rack level.

Component lead times for fiber-related categories have stretched to approximately 40 weeks, reflecting how tightly AI infrastructure demand is straining the physical network supply chain. This supply tightness benefits vendors with secured allocations and regional manufacturing presence. Distributors without multi-quarter fiber supply agreements face order delays that translate directly into project slippage and lost revenue on time-sensitive hyperscale builds.

Enterprise migration to 400G and 800G Ethernet networks is accelerating structured cabling refresh cycles across North America, Europe, and advanced Asia Pacific corridors. These speed upgrades require Category 6A, Category 8, and high-performance fiber installations that cannot be served by legacy horizontal cabling. Vendors aligned to high-grade copper and fiber product lines capture replacement revenue that legacy-only suppliers will lose as refresh timelines compress.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI data center build-out lifting fiber-dense backbone demand | +2.4% | North America core, EU hubs, India, Middle East clusters | Short term (≤ 2 years) |

| 400G/800G migration accelerating high-performance fiber refresh cycles | +1.9% | North America core, EU, APAC corridors | Medium term (2-4 years) |

| Smart buildings and PoE retrofits expanding LAN cabling intensity | +1.6% | North America, EU, GCC, urban APAC | Short term (≤ 2 years) |

| TIA/ISO/BICSI compliance upgrades raising replacement and certification spend | +1.2% | North America core, EU, multinational APAC sites | Medium term (2-4 years) |

| Edge and distributed computing increasing secondary-site cabling density | +1.1% | APAC corridors, secondary North America metros, Latin America spill-over | Medium term (2-4 years) |

| Public digital infrastructure and campus modernization supporting baseline volume | +0.9% | India, EU public sector, Middle East, Southeast Asia | Long term (≥ 4 years) |

Restraints

Copper cost volatility is the clearest restraint on structured cabling market growth. As per our research, the U.S. producer price index for copper wire and cable reached 570.382 in May 2026 after 531.667 in April 2026. A quarterly move of 6 to 10% in copper benchmarks flows into 3 to 7% revisions in passive infrastructure quotations, forcing contractors to shorten quote validity from roughly 60 to 90 days down to 15 to 30 days on large tenders.

This pricing instability reduces bid confidence for enterprise LAN refreshes, hospital projects, and multi-building campus installations running fixed capital envelopes. Owners defer non-critical recabling by two to four quarters when quotations become unreliable. Channel partners typically absorb part of the inflation through discounts rather than passing the full increase to end users, compressing margins at the distributor and installer tier.

As per our research, copper cost volatility alone warrants approximately a 1.0 percentage point deduction from the market’s addressable CAGR. This suppresses order conversion even when underlying connectivity requirements remain intact. Vendors that hedge copper exposure through long-term supply contracts or accelerate fiber substitution in backbone applications hold a structural advantage over those relying on spot procurement in this environment.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper cost volatility | -1.0% | Global, India import-linked | Short term |

| Price-led procurement pressure | -0.8% | India metros, ASEAN, MEA | Short to Medium term |

| Installation skill shortages | -0.6% | India Tier 1 and Tier 2 cities | Short to Medium term |

| Building retrofit delays | -0.5% | North America, EU, India core cities | Medium term |

| Standards and compliance complexity | -0.4% | India, EU, GCC | Medium term |

| Wireless and fiber substitution | -0.3% | India edge sites, APAC emerging | Long term |

Challenges

Fiber input tightness is constraining structured cabling deployment capacity in 2026. As per our research, new glass preform capacity cycles require 18 to 24 months, and meaningful supply easing is more likely from late 2027 into 2028. This lag keeps procurement teams exposed to high input volatility and extended sourcing uncertainty on non-contracted volumes exceeding 30 to 45 days on average.

Project-level financial effects are material. As per our research, realistic fiber-heavy builds face 8 to 15% material cost variance, while mid-sized integrators without long-term supply agreements absorb 150 to 300 basis points of gross-margin compression. These pressures force recurring redesign cycles, supplier substitution, and phased installation sequencing across active projects, reducing execution efficiency across the supply chain.

As per our research, fiber input tightness reduces the market’s practical growth path by approximately 1.3 percentage points versus unconstrained execution. This challenge is not evenly distributed: manufacturers and EPC-linked distributors with regionalized sourcing and multi-quarter preform allocations absorb far less disruption than open-market buyers. This creates a structural gap between large integrated vendors and smaller regional installers competing on the same project pipeline.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Fiber input tightness | -1.3% | APAC supply base, global installs | Long term (≥ 4 years) |

| Installer talent deficit | -1.0% | North America core, India, ASEAN | Medium term (2-4 years) |

| High-density design burden | -0.9% | North America hyperscale, APAC metros | Medium term (2-4 years) |

| Multi-standard migration complexity | -0.7% | Global enterprise, EU telecom backbone | Long term (≥ 4 years) |

| Cross-border delivery slippage | -0.8% | APAC logistics corridors, Middle East, EU | Short term (≤ 2 years) |

| Budget phasing pressure | -0.6% | Global commercial, data center, campus builds | Medium term (2-4 years) |

Opportunities

AI-ready fiber densification carries a +2.4% potential CAGR upside for the structured cabling market. Hyperscale and colocation operators building GPU-intensive halls require ultra-high-density fiber connectivity that exceeds conventional enterprise cabling specifications. Vendors that develop pre-terminated, high-fiber-count assemblies certified for AI workload environments can capture this upside before it becomes a commodity offering.

Smart-building Power over Ethernet retrofits represent a +2.1% potential CAGR upside, with medium-term execution windows across the EU, North America, and developed Asia Pacific. As per our research, a mid-size commercial retrofit can raise connected endpoint counts by 2 to 4 times and increase cabling density per floor by 30 to 60%. Solution-led PoE projects can expand operating margins by 200 to 350 basis points compared with traditional bid-based LAN contracts.

Edge micro-DC cabling kits carry a +1.9% potential CAGR upside across APAC emerging markets, North America, GCC, and EU industrial hubs. Standardized cabling kit formats reduce engineering complexity and installation time at distributed edge sites. Vendors that productize edge cabling solutions with pre-configured pathways and tested assemblies can enter this segment at scale without the project-by-project design overhead of traditional enterprise deployments.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| AI-ready fiber densification | +2.4% | North America core, EU, advanced APAC | Short term (≤ 2 years) |

| Edge micro-DC cabling kits | +1.9% | APAC emerging, North America, GCC, EU industrial hubs | Short term (≤ 2 years) |

| Smart-building PoE retrofits | +2.1% | EU, North America, developed APAC | Medium term (2-4 years) |

| Managed lifecycle cabling | +1.6% | North America, EU, APAC enterprise markets | Short term (≤ 2 years) |

| Security and compliance overlays | +1.3% | Regulated EU, US federal and healthcare, Middle East critical infrastructure | Medium term (2-4 years) |

| Installer roll-up platforms | +1.8% | North America fragmented metros, India, Southeast Asia, EU local markets | Long term (≥ 4 years) |

Regional Analysis

Asia Pacific Dominates the Structured Cabling Market with a Market Share of 40.5%, Valued at USD 5.93 Billion

Asia Pacific holds a 40.5% share of the global Structured Cabling Market, valued at USD 5.93 Billion in 2025. China, Japan, South Korea, and India are driving volume through hyperscale data center construction, 5G network backhaul cabling, and government-led smart city programs. This regional leadership reflects both the density of new construction activity and the scale of enterprise LAN refresh programs across manufacturing and financial services sectors.

North America represents the second-largest regional market. The United States is the primary contributor, supported by sustained hyperscale data center investment, enterprise campus upgrades, and federal digital infrastructure programs. In December 2025, Beacon Communications launched a dedicated structured cabling solutions service focused on fiber-optic and copper deployments across healthcare, education, government, and commercial facilities, illustrating the breadth of active end-market demand across this region.

Europe is a significant structured cabling market driven by enterprise network compliance upgrades and public sector digitization programs. The EU’s building renovation and digitization directives are pushing non-residential facilities to upgrade physical network infrastructure by defined deadlines. This regulatory pressure creates a structured replacement cycle that benefits vendors with certified product portfolios aligned to TIA and ISO standards.

Latin America and the Middle East and Africa represent emerging regional markets. GCC countries are executing large-scale smart city and data center projects that require standardized structured cabling frameworks. Brazil and Mexico anchor Latin American demand through financial services and manufacturing sector LAN upgrades. Both regions are earlier in their infrastructure maturity cycle, offering entry opportunities for vendors willing to invest in local installer partnerships and certified distribution channels.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

ABB Ltd operates across power and automation infrastructure, positioning its structured cabling offerings within broader building and industrial connectivity solutions. This integrated approach gives ABB access to multi-system project budgets spanning energy, automation, and data networks. However, its diversified portfolio means structured cabling competes internally for engineering and sales resources against higher-margin segments.

In October 2025, CommScope announced the global availability of its evolved SYSTIMAX Constellation platform, designed to support scalable 10G connectivity and hybrid power and data fiber networks. This launch reinforces CommScope’s position in high-performance enterprise and hyperscale environments. However, Amphenol’s announced acquisition of CommScope’s Connectivity and Cable Solutions business for USD 10.5 Billion introduces strategic uncertainty around product roadmap continuity and channel relationships during the transition period.

Key Players

- ABB Ltd

- Belden Inc.

- CommScope Holding Company, Inc.

- Corning Incorporated

- Furukawa Electric Co., Ltd.

- Legrand SA

- Nexans

- Schneider Electric

- Siemens AG

- TE Connectivity Ltd.

- STL Tech

- Computec Engineering, Ltd.

- RIAM Enterprises

- KFP Total IT Solutions

- Star Networking Services

- Other Key Players

Recent Developments

- June 2025 – Prysmian completed the acquisition of Channell Commercial Corporation for a base purchase price of USD 950 Million, strengthening its fiber connectivity, FTTH, data center, and structured cabling infrastructure portfolio.

- March 2025 – Prysmian announced an agreement to acquire Channell Commercial Corporation for USD 950 Million plus a potential USD 200 Million earn-out, expanding its connectivity solutions business serving fiber-optic networks, data centers, and digital infrastructure markets.

- December 2025 – Prysmian confirmed a USD 200 Million earn-out payment related to the Channell acquisition after the company achieved specified 2025 performance targets, reinforcing its long-term commitment to connectivity and structured cabling solutions.

- November 2025 – Uniserve Communications entered into agreements to acquire Megawire Inc., a provider of managed IT and structured cabling solutions, for approximately USD 6.5 Million, to strengthen its infrastructure services portfolio.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 14.6 Billion |

| Forecast Revenue (2035) | USD 27.9 Billion |

| CAGR (2026-2035) | 6.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Copper Cables, Fiber Optic Cables, Others); By Application (Data Centers, Local Area Networks, Others); By End-Use Industry (Government, Industrial, IT and Telecommunication, Residential and Commercial, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | ABB Ltd, Belden Inc., CommScope Holding Company, Inc., Corning Incorporated, Furukawa Electric Co. Ltd., Legrand SA, Nexans, Schneider Electric, Siemens AG, TE Connectivity Ltd., STL Tech, Computec Engineering Ltd., RIAM Enterprises, KFP Total IT Solutions, Star Networking Services, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |