Quick Navigation

- Report Overview

- Key Takeaways

- Analysts’ Viewpoint

- U.S. Market Size

- Component Analysis

- Technology Type Analysis

- Application Analysis

- End-User Industry Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Recent Developments

- Report Scope

Report Overview

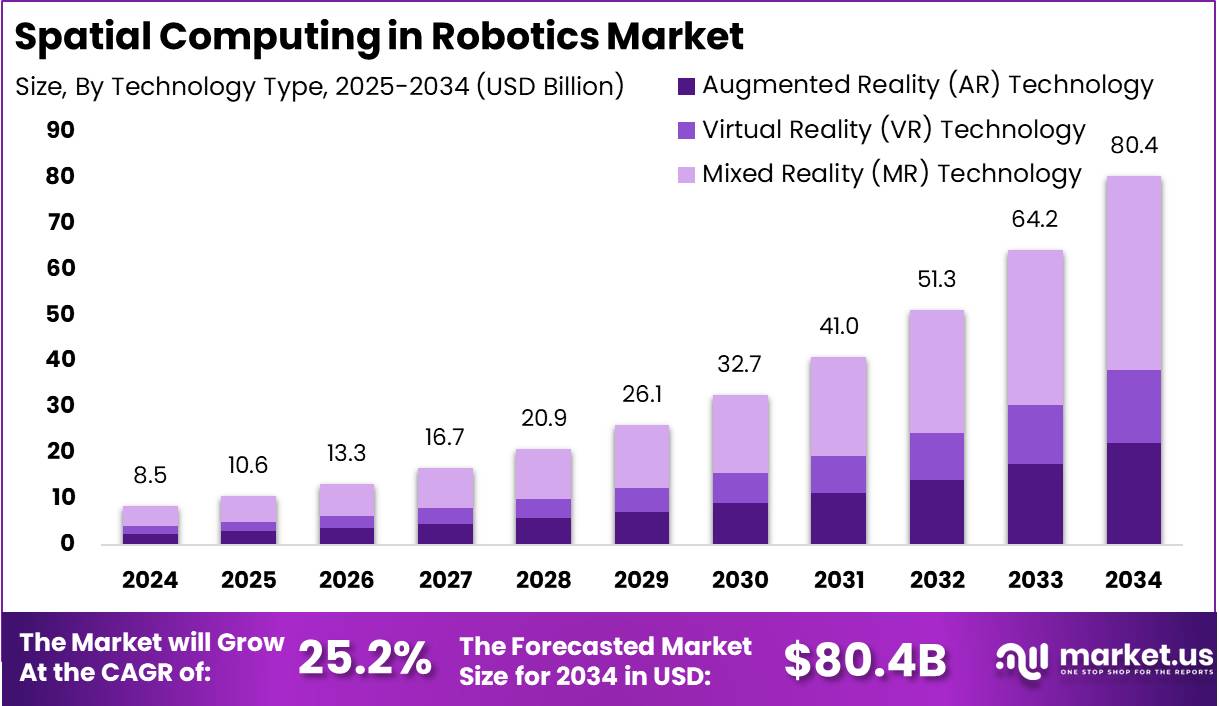

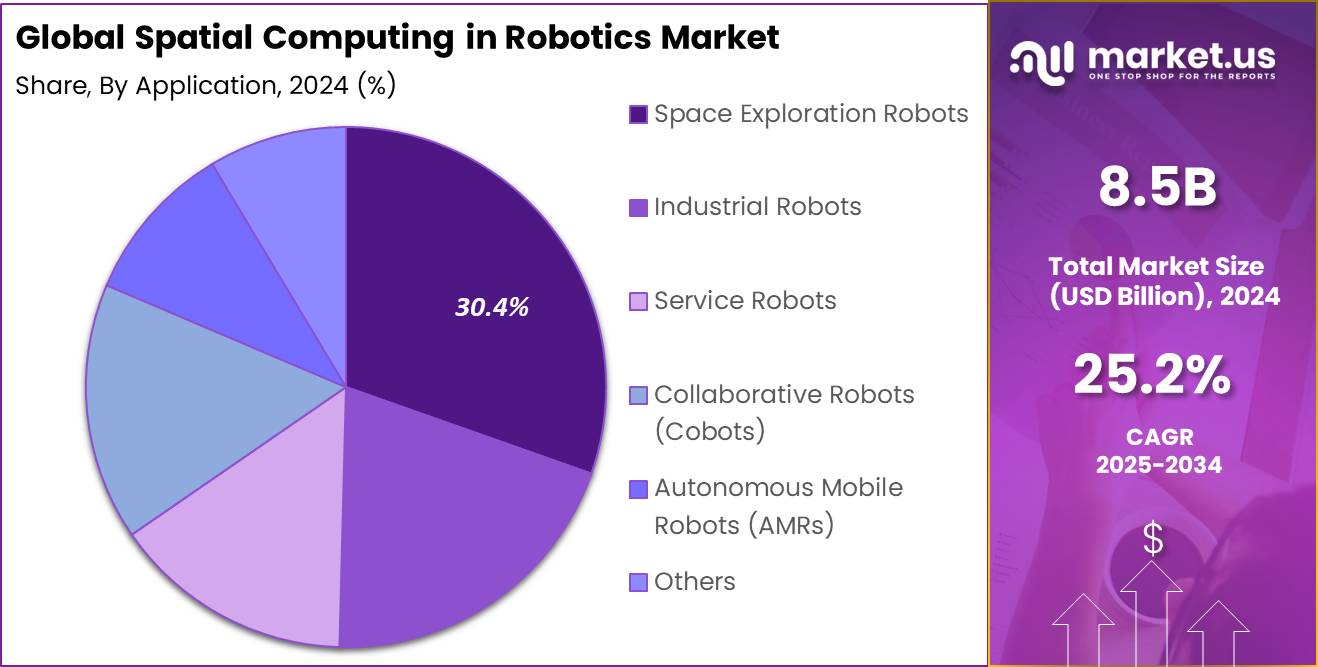

The Spatial Computing in Robotics Market size is expected to be worth around USD 80.4 Billion By 2034, from USD 8.5 billion in 2024, growing at a CAGR of 25.2% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 36.5% share, holding USD 3.1 Billion revenue.

Spatial Computing in Robotics integrates real-world physical environments with computational processes and virtual data, enhancing robotic interaction and operational effectiveness. This technology allows robots to perceive, analyze, and interact with their environments in sophisticated ways, enabling tasks ranging from navigation in autonomous vehicles to precise manipulation in industrial settings.

The market for spatial computing in robotics is evolving rapidly, driven by advances in AI, machine learning, sensor technology, and AR/VR technologies. These advancements enable robots to perform more complex tasks with greater efficiency and precision. The integration of spatial computing in robotics is seeing significant application across diverse sectors including manufacturing, healthcare and logistics, where the ability to interact with and adapt to dynamic environments is critical.

Additionally, the ongoing advancements in AI and machine learning are enabling more sophisticated and context-aware robots, further propelling market growth. There is a robust demand for spatial computing in robotics, particularly in applications requiring high precision and adaptability such as surgical robots, autonomous vehicles, and industrial automation systems.

According to Market.us, The global spatial computing market is projected to reach USD 620.2 billion by 2032, growing from USD 142.6 billion in 2023 at a CAGR of 18.3% during the forecast period from 2024 to 2033. The rapid growth is driven by advancements in augmented reality (AR), virtual reality (VR), artificial intelligence (AI), and IoT, which are transforming industries such as healthcare, retail, automotive, and manufacturing.

Spatial computing in robotics offers numerous business benefits, including increased operational efficiency, reduced costs, and enhanced safety. These technologies enable robots to perform tasks with higher accuracy and less human intervention, leading to streamlined operations and lower operational risks.

Key Takeaways

- The Spatial Computing in Robotics Market is projected to grow significantly, reaching USD 80.4 billion by 2034 from USD 8.5 billion in 2024, expanding at a CAGR of 25.2% between 2025 and 2034.

- North America held a dominant position in 2024, accounting for more than 36.5% of the market share, translating to a revenue of USD 3.1 billion.

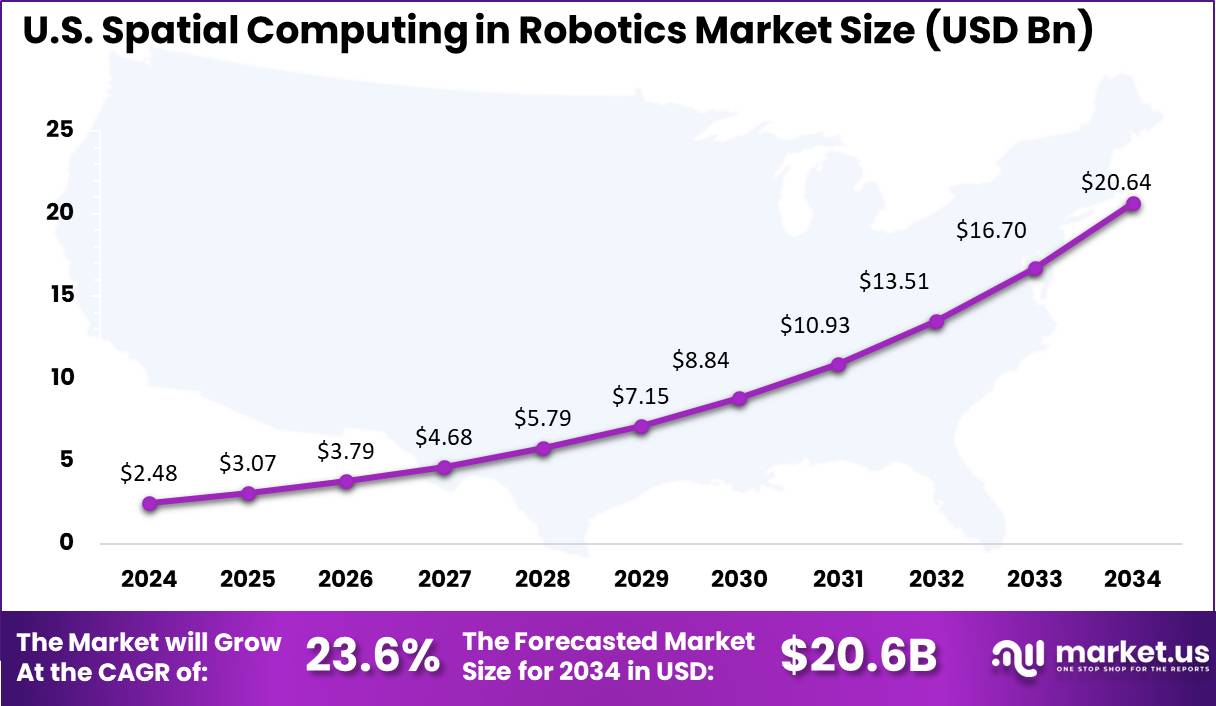

- The U.S. market alone was valued at USD 2.48 billion in 2024, growing at a CAGR of 23.6%, indicating strong demand for spatial computing solutions across robotics applications.

- The hardware segment maintained the largest market share in 2024, contributing over 40.8% of total market revenue. The increasing deployment of AI-powered robotics, LiDAR sensors, and edge computing devices has fueled this growth.

- The MR technology segment dominated with a 52.5% market share in 2024, as industries increasingly integrate augmented and virtual reality to enhance robotic automation and remote operations.

- The space exploration robots segment accounted for 30.4% of the market in 2024. The rising investment in autonomous robotic missions, planetary exploration, and satellite servicing is expected to further accelerate demand.

- The manufacturing industry was a key end-user, holding a 28.4% market share in 2024. Companies are leveraging spatial computing for precision robotics, real-time data analytics, and smart automation to enhance efficiency.

Analysts’ Viewpoint

Investment in spatial computing for robotics presents significant opportunities, especially in sectors poised for rapid technological advancement such as healthcare, automotive, and industrial automation. As businesses seek to leverage these technologies to gain competitive advantages, the potential for growth in this market is substantial.

Investors are particularly interested in startups and companies innovating in AI, sensor technology, and AR/VR applications. AI significantly impacts the spatial computing in robotics market by enabling more complex data analysis and decision-making processes.

AI algorithms enhance the ability of robots to understand and navigate their environments, making them more autonomous and efficient. The integration of AI with spatial computing is leading to innovations such as predictive maintenance, optimized workflow, and enhanced customization capabilities in robotics.

The regulatory landscape for spatial computing in robotics is still developing, as governments and international bodies begin to address the complexities introduced by these technologies. Current regulations are focused on ensuring safety and privacy, particularly in consumer-facing applications.

Recent advancements in spatial computing include improvements in sensor accuracy, AI algorithms, and the development of more sophisticated AR and VR interfaces. These enhancements allow for more detailed and accurate environmental mapping and more intuitive human-robot interactions.

U.S. Market Size

The US Spatial Computing in Robotics Market size was exhibited at USD 2.48 Billion in 2024 with CAGR of 23.6%. The United States leads in the Spatial Computing in Robotics market due to several key factors that interplay to create a robust ecosystem for this advanced technology.

Firstly, the U.S. market benefits significantly from the presence of major technology leaders and innovators such as Google, Apple, and Microsoft. These companies not only invest heavily in research and development but also in the application of spatial computing technologies across various sectors, including healthcare, automotive, and consumer electronics.

Furthermore, the U.S. market is characterized by a high adoption rate of advanced technologies, including augmented reality (AR) and virtual reality (VR), which are integral components of spatial computing. This technological readiness is complemented by a strong venture capital presence that supports startups and new innovations within the field, allowing for rapid development and deployment of new spatial computing solutions.

Another significant driving force behind the U.S. market’s leadership is the comprehensive ecosystem that includes not only technology companies but also educational institutions and government support. These elements collectively facilitate a conducive environment for technological advancement and adoption.

In 2024, North America held a dominant market position in the Spatial Computing in Robotics sector, capturing more than a 40% share, which equated to USD 16.2 billion in revenue. This leadership can be attributed to several pivotal factors that uniquely position North America at the forefront of the spatial computing revolution.

Firstly, North America benefits from the presence of major technology firms that lead innovations in AR, VR, and AI technologies, which are integral components of spatial computing. Companies like Google, Microsoft, and Apple, headquartered in this region, invest heavily in research and development.

These investments propel technological advancements and the adoption of spatial computing solutions across various industries, including automotive, healthcare, and manufacturing. Additionally, the region’s robust financial ecosystem supports startups and innovations through venture capital and a wealth of funding opportunities.

This economic environment encourages continuous growth and innovation in spatial computing technologies, driving further market expansion. Furthermore, North America’s regulatory framework is progressively adapting to new technologies. Governments in the U.S. and Canada are implementing policies that favor the development and safe deployment of AI and robotics technologies. This regulatory support mitigates risks associated with technology adoption, reassuring businesses and consumers alike.

Component Analysis

In 2024, the hardware segment held a dominant market position in the Spatial Computing in Robotics market, capturing more than a 40.8% share. This prominence is largely due to the critical role that hardware components like sensors, processors, displays, and controllers play in enabling the fundamental operations of spatial computing systems.

These components are essential for the accurate capture, processing, and display of spatial data, which is integral to various applications ranging from augmented reality (AR) to virtual reality (VR) and mixed reality (MR). The leadership of the hardware segment is also driven by continual advancements in these technologies.

Innovations in sensor technology, for instance, have significantly enhanced the ability of robots and devices to interact with their environments in more sophisticated ways. This includes improved spatial recognition and more precise tracking of movements within a given space, which are crucial for applications in industries such as healthcare, manufacturing, and automotive.

Furthermore, the integration of advanced processors and high-resolution displays has enabled more complex computations and richer visualizations, thus expanding the potential use cases of spatial computing. These technological improvements not only enhance the functionality and efficiency of spatial computing systems but also drive their adoption across various sectors.

Lastly, the market’s growth is supported by a robust ecosystem involving key technological firms and startups, particularly in regions like North America, where there is a strong focus on R&D and innovation. The presence of major tech companies, coupled with substantial investments in the development and commercialization of new spatial computing solutions, continues to propel the hardware segment forward.

Technology Type Analysis

In 2024, the Mixed Reality (MR) Technology segment held a dominant market position within the Spatial Computing in Robotics market, capturing more than a 52.5% share. This leadership can be attributed to several key factors that distinguish MR from other technologies such as Augmented Reality (AR) and Virtual Reality (VR).

Primarily, MR technology offers a blend of AR and VR, providing a more immersive and interactive experience that combines real-world elements with virtual ones. This hybrid nature allows for applications across various industries, significantly enhancing user interaction and engagement by overlaying digital information onto the physical world in real-time.

This capability makes MR highly valuable in sectors like manufacturing for training and simulation, in healthcare for surgical procedures and diagnostics, and in entertainment for more engaging experiences. The adoption of MR technology has been further facilitated by significant advancements in related hardware and software.

Innovations in sensor technology, graphics processing, and display resolutions have greatly improved the quality and responsiveness of MR applications, making them more practical and effective for professional and consumer use. Companies leading in MR technology, such as Microsoft and Magic Leap, continue to invest heavily in these areas, pushing the boundaries of what’s possible in spatial computing.

Moreover, the integration of MR with other cutting-edge technologies like artificial intelligence (AI) and the Internet of Things (IoT) has expanded its applications and effectiveness, particularly in industrial settings where precision and efficiency are critical. This has led to rapid growth and adoption, setting MR technology apart as a leader in the spatial computing landscape.

Application Analysis

In 2024, the Space Exploration Robots segment held a dominant position in the Spatial Computing in Robotics market, capturing more than a 30.4% share. This leading status can be attributed to several pivotal factors that underscore the segment’s critical importance and expansive potential.

Firstly, space exploration robots equipped with spatial computing capabilities are essential for navigating and operating in the complex, unstructured environment of space. These robots leverage advanced sensors and computing systems to perform tasks such as terrain mapping, autonomous navigation, and scientific experimentation, which are crucial for missions to the moon, Mars, and beyond.

The integration of spatial computing allows these robots to process and interpret vast amounts of environmental data in real time, enhancing their effectiveness and reliability in space exploration tasks. Moreover, significant investments by governments and private entities in space exploration initiatives have propelled the demand for these robots.

Programs aimed at planetary exploration, asteroid mining, and the development of sustainable off-Earth living conditions rely heavily on robotic systems that incorporate spatial computing technologies to extend human reach and capabilities in space.

Additionally, technological advancements in robotics and computing, including improvements in AI algorithms and the miniaturization of hardware, have made these robots more capable and cost-effective. These advancements facilitate more frequent and complex missions, as space agencies and companies push the boundaries of what’s achievable in space exploration.

The ongoing innovation and strategic partnerships among leading aerospace corporations and tech companies also drive the growth of this market segment. Collaborations are aimed at enhancing the technological capabilities of space exploration robots, making them pivotal in the broader strategy of exploring and utilizing space resources.

End-User Industry Analysis

In 2024, the Manufacturing segment in the Spatial Computing in Robotics market held a significant market position, capturing more than a 28.4% share. This dominance is driven by several factors that highlight the critical role of spatial computing in transforming manufacturing processes.

The adoption of spatial computing in manufacturing is largely fueled by the need to enhance precision and efficiency in production lines. These technologies enable more sophisticated automation by providing robots and automated systems with the capability to perceive and understand their environment in three dimensions.

This is crucial for tasks that require high levels of accuracy, such as assembly and quality control, where spatial computing aids in the precise placement and inspection of components. Moreover, the integration of augmented reality (AR) and virtual reality (VR) within manufacturing workflows has revolutionized training and maintenance procedures.

By using AR and VR, manufacturers can simulate different scenarios for training purposes without the need to halt production lines, thereby reducing downtime and increasing worker safety. Maintenance teams can also use AR to receive real-time, step-by-step visual guidance on machinery diagnostics and repair, which enhances the speed and effectiveness of their work.

The growth in this segment is also supported by ongoing industrial advancements and the digital transformation of factories. The push towards Industry 4.0, characterized by the integration of IoT and cyber-physical systems, relies heavily on the capabilities provided by spatial computing to connect and optimize various components of the manufacturing process.

Key Market Segments

By Component

- Hardware

- Sensors

- Processors

- Displays

- Controllers

- Others

- Software

- 3D Mapping and Modeling Software

- Spatial Analytics Software

- Others

- Services

- Integration and Deployment Services

- Maintenance and Support Services

- Training and Education Services

By Technology Type

- Augmented Reality (AR) Technology

- Virtual Reality (VR) Technology

- Mixed Reality (MR) Technology

By Application

- Space Exploration Robots

- Industrial Robots

- Service Robots

- Collaborative Robots (Cobots)

- Autonomous Mobile Robots (AMRs)

- Others

By End-User Industry

- Aerospace and Defense

- Manufacturing

- Healthcare

- Retail and E-commerce

- Education and Training

- Automotive

- IT & Telecom

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Integration of Emerging Technologies

The Spatial Computing in Robotics market is primarily driven by the rapid integration of emerging technologies such as Artificial Intelligence (AI), Machine Learning (ML), and Internet of Things (IoT). These technologies enhance the capability of spatial computing systems to interpret and understand their environment, leading to more efficient and autonomous robotic operations.

For instance, AI and ML algorithms can process spatial data to improve navigation and decision-making processes in robotics, essential for applications ranging from industrial automation to autonomous driving. This integration not only boosts the operational efficiency of robots but also expands their application scope across different industries, fueling market growth.

Restraint

High Implementation Costs

One significant restraint in the Spatial Computing in Robotics market is the high cost associated with implementing and maintaining these systems. The development and deployment of spatial computing technologies involve substantial investments in advanced sensors, software, and skilled personnel.

The initial setup costs and ongoing maintenance expenses can be prohibitive for small and medium-sized enterprises (SMEs), limiting the technology’s adoption to larger organizations with adequate resources. This economic barrier restricts the market’s growth potential, especially in less developed regions where businesses may not have the financial capability to invest in such advanced technologies.

Opportunity

Expansion into Healthcare and Automotive Industries

Spatial computing presents significant opportunities in the healthcare and automotive industries by enhancing precision and efficiency. In healthcare, spatial computing can revolutionize surgical procedures and training through AR and VR, providing real-time, immersive experiences that improve the accuracy and outcomes of medical interventions.

Similarly, in the automotive sector, this technology can be applied in the design and manufacturing processes, as well as in developing advanced driver-assistance systems (ADAS) that require precise spatial awareness. The growing demand for enhanced safety features in vehicles and the increasing need for innovative medical training and treatment methods offer lucrative prospects for the expansion of spatial computing in these industries.

Challenge

Data Privacy and Security Concerns

A major challenge facing the Spatial Computing in Robotics market is addressing data privacy and security concerns. Spatial computing devices collect and process vast amounts of sensitive data, including personal and environmental information, which can be vulnerable to breaches and misuse.

Ensuring the security of this data is paramount, as any compromise could lead to privacy violations and reduce consumer trust in spatial computing technologies. The industry must navigate complex regulatory environments and invest in robust cybersecurity measures to protect user data and comply with global data protection regulations, posing a significant challenge for market players.

Growth Factors

The Spatial Computing in Robotics market is experiencing rapid growth, largely fueled by the integration of augmented reality (AR), virtual reality (VR), and mixed reality (MR) technologies. These technologies enhance the interaction between robots and their operational environments, making them more intuitive and effective for various applications.

The increasing adoption of these technologies in industries such as healthcare, automotive, and manufacturing is a primary growth driver. Specifically, in healthcare, AR and VR are revolutionizing surgical procedures and training by providing simulations that offer realistic, risk-free environments for medical professionals.

Emerging Trends

Emerging trends in spatial computing include the rising use of AI and machine learning to enhance the capabilities of robotics systems. These technologies allow robots to make more autonomous decisions based on the spatial data they collect.

Furthermore, the development of smaller, more efficient sensors and processors is enabling the creation of more agile and less obtrusive robots, which can operate more effectively in a variety of settings. There is also a significant trend towards the use of spatial computing in collaborative robots (cobots), which work alongside humans in shared workspaces, enhancing safety and efficiency.

Business Benefits

The integration of spatial computing in robotics offers substantial business benefits, including increased efficiency and accuracy in robotic tasks. This technology enables robots to better understand and navigate their surroundings, reducing errors and increasing the speed of task completion.

Industries such as manufacturing have seen significant improvements in assembly and quality control processes, while in sectors like retail, spatial computing aids in inventory management and customer service. The ability to improve process accuracy and operational efficiency presents a strong value proposition for businesses across various sectors.

Key Player Analysis

Top Key Players in the Market

- Microsoft Corporation

- Meta Platforms Inc.

- Apple Inc.

- Google LLC

- Nvidia Corporation

- Qualcomm Incorporated

- Sony Group Corporation

- Magic Leap Inc.

- PTC Inc.

- Others

Recent Developments

- In February 2025, Meta established a new division within its Reality Labs unit to develop AI-powered humanoid robots capable of assisting with physical tasks. This initiative signifies Meta’s entry into the robotics arena, positioning it alongside competitors like Nvidia-backed Figure AI and Tesla. The robotics group is led by Marc Whitten, the former CEO of Cruise.

- In January 2025, at CES 2025, Nvidia showcased its latest innovations in robotics and AI, emphasizing the role of spatial computing and its Omniverse platform in training robotics, environmental AI, and self-driving car frameworks.

- In January 2024, Apple launched the Vision Pro headset, a spatial-computing-based device that blends the virtual and physical worlds seamlessly. This launch signifies Apple’s commitment to advancing spatial computing technologies.

- In September 2024, Google introduced Android XR, a new operating system designed explicitly for extended reality (XR) devices and services. Developed in collaboration with Samsung, this initiative aims to enhance the future of AI, AR, and VR experiences on headsets and smart glasses.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 8.5 Bn |

| Forecast Revenue (2034) | USD 80.4 Bn |

| CAGR (2025-2034) | 25.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Hardware (Sensors, Processors, Displays, Controllers, Others), Software (3D Mapping and Modeling Software, Spatial Analytics Software, Others), Services (Integration and Deployment Services, Maintenance and Support Services, Training and Education Services)), By Technology Type (Augmented Reality (AR) Technology, Virtual Reality (VR) Technology, Mixed Reality (MR) Technology), By Application (Space Exploration Robots, Industrial Robots, Service Robots, Collaborative Robots (Cobots), Autonomous Mobile Robots (AMRs), Others), By End-User Industry (Aerospace and Defense, Manufacturing, Healthcare, Retail and E-commerce, Education and Training, Automotive, IT & Telecom, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Microsoft Corporation, Meta Platforms Inc., Apple Inc., Google LLC , Nvidia Corporation, Qualcomm Incorporated , Sony Group Corporation, Magic Leap Inc., PTC Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |