Quick Navigation

Report Overview

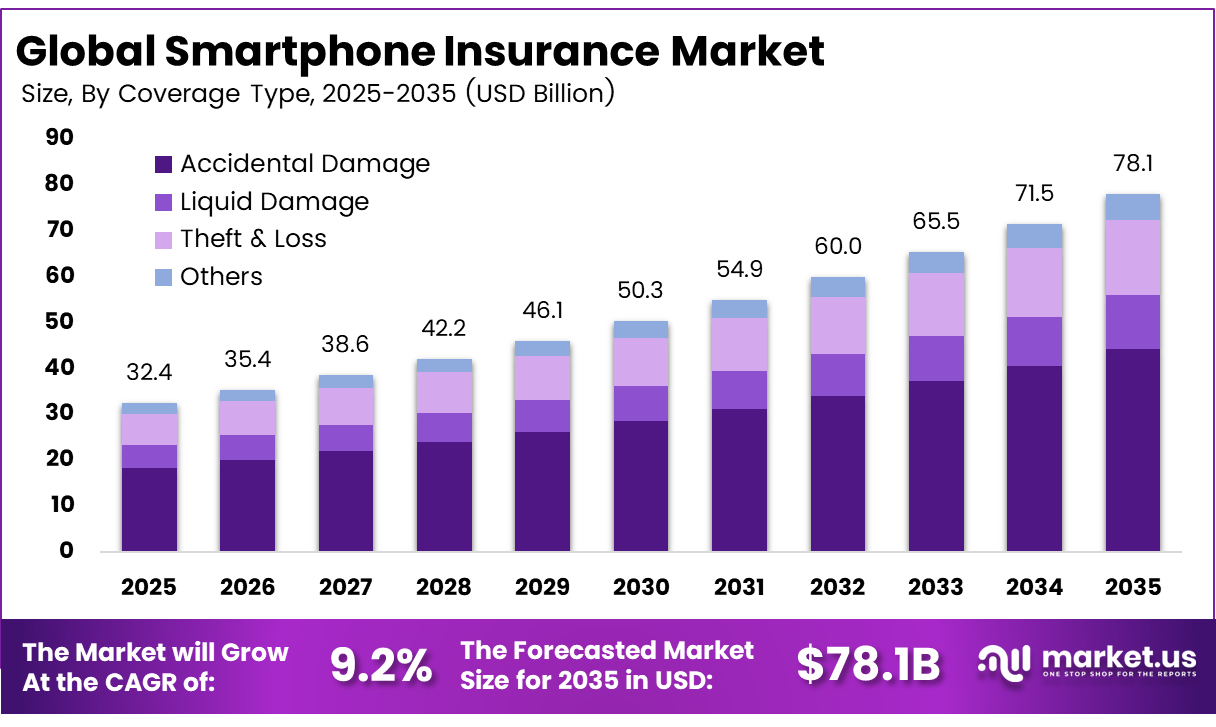

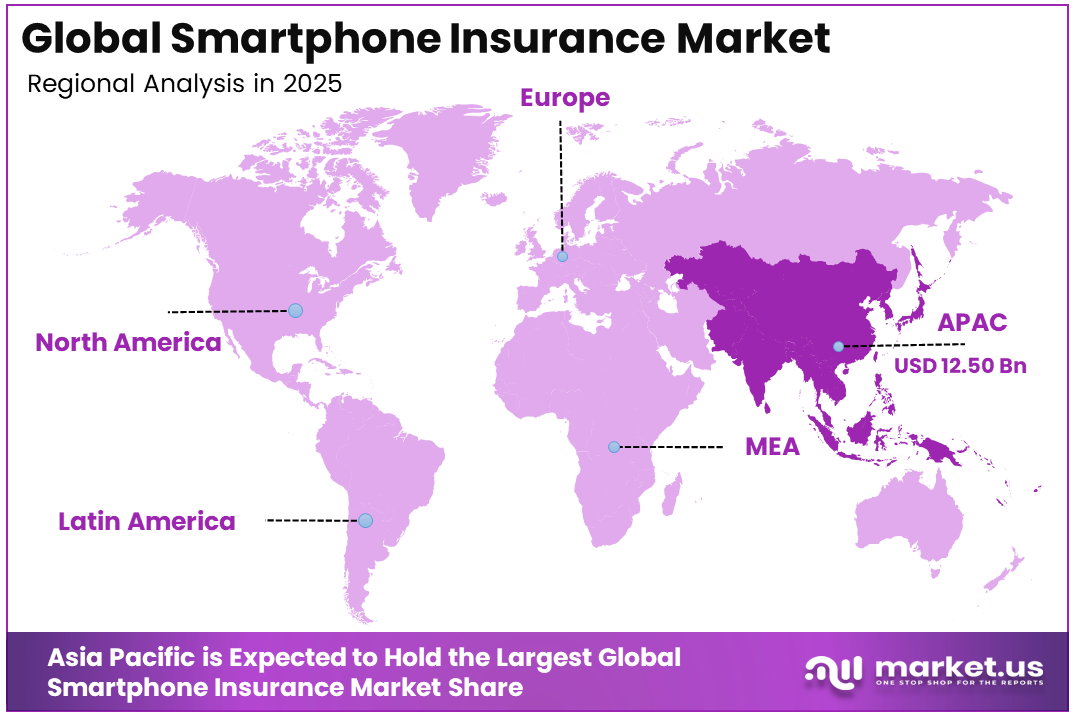

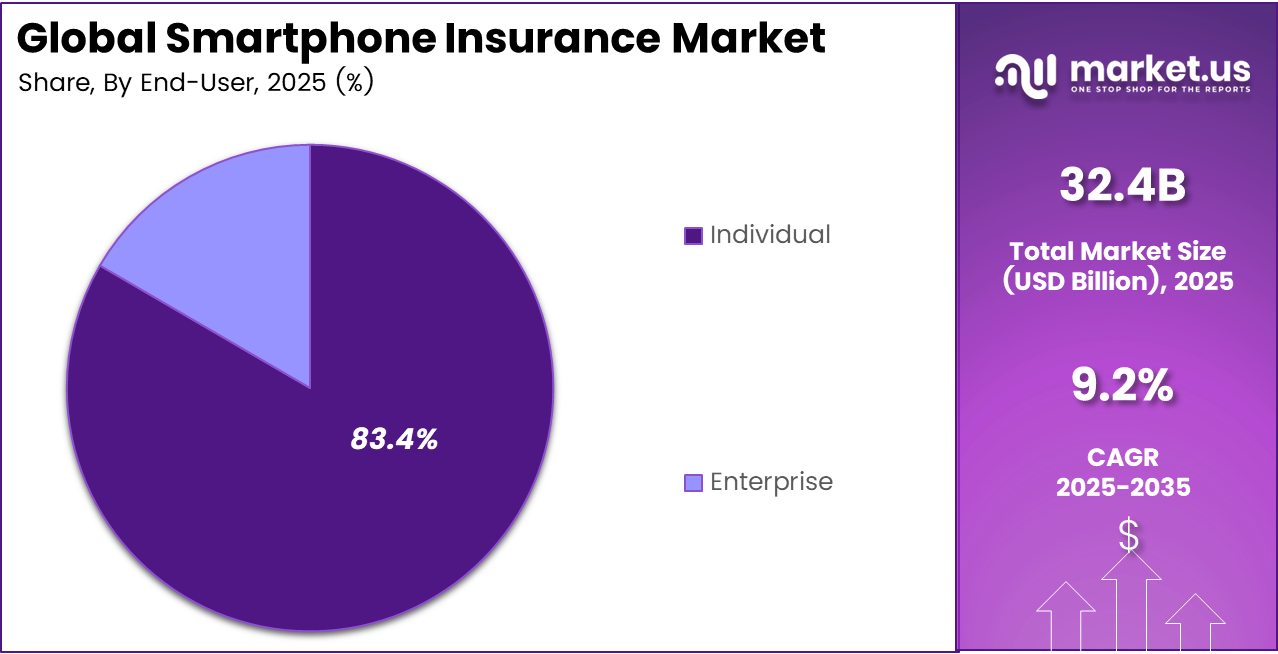

The Global Smartphone Insurance Market size is expected to be worth around USD 78.1 billion by 2035, from USD 32.4 billion in 2025, growing at a CAGR of 9.2% during the forecast period from 2025 to 2035. Asia Pacific held a dominant market position, capturing more than a 38.6% share, holding USD 12.50 billion in revenue.

Smartphone insurance refers to a protection plan that covers financial loss or damage to mobile devices. It helps users manage risks such as accidental damage, theft, or technical faults. These plans offer repair, replacement, or compensation support, ensuring users can continue using their devices without facing high unexpected costs or disruptions.

Rising repair costs continue to push consumers toward insurance, especially as screens crack easily during daily use. Around 70% of phone damage is caused by accidental drops, which increases the need for protection. High smartphone prices further strengthen this trend, as users prefer coverage instead of bearing large replacement expenses after unexpected damage.

The market for smartphone insurance is driven by rising device prices, costly repairs, and growing dependence on smartphones for daily activities. Consumers use their phones for work, banking, shopping, and communication, so any damage or loss creates immediate inconvenience. This is increasing demand for protection plans that offer financial support, quick repairs, and replacement services, making insurance a practical choice for many smartphone users.

Demand is increasing as smartphones have become essential for banking, communication, and personal data storage. Losing or damaging a device now creates both financial and functional disruption. More than 60% of users experience damage within two years, which drives interest in plans that cover theft, water damage, and technical failures beyond standard warranties.

For instance, in January 2025, Apple expanded its AppleCare+ coverage with a new $99 annual plan that includes theft and loss protection for iPhones across North America. This move taps into growing consumer demand for comprehensive device security, making premium protection more accessible while boosting subscriber retention through seamless claims via the My iPhone app.

Key Takeaway

- In 2025, the Accidental Damage segment held a dominant market position, capturing a 56.8% share of the Global Smartphone Insurance Market.

- In 2025, the Repair segment held a dominant market position, capturing a 41.3% share of the Global Smartphone Insurance Market.

- In 2025, the Mobile Operators segment held a dominant market position, capturing a 49.7% share of the Global Smartphone Insurance Market.

- In 2025, the Individual segment held a dominant market position, capturing a 83.4% share of the Global Smartphone Insurance Market.

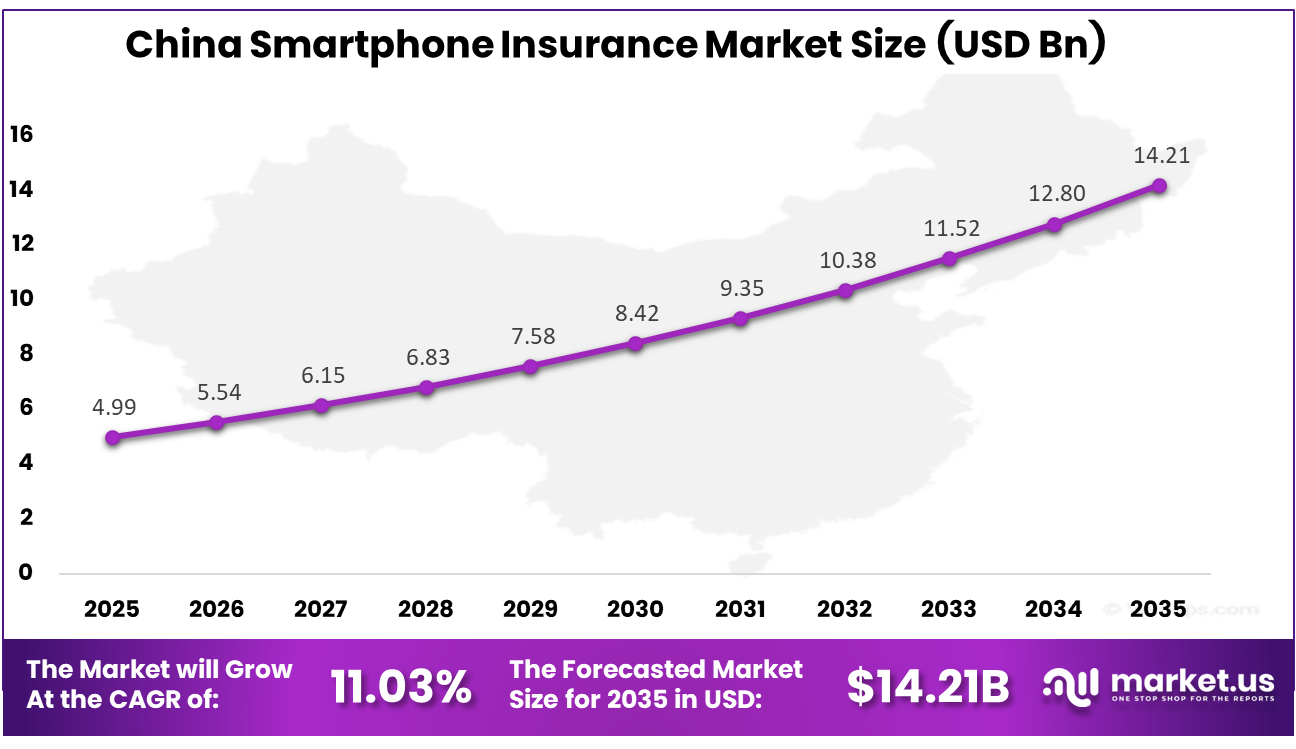

- The China Smartphone Insurance Market was valued at USD 4.99 Billion in 2025, with a robust CAGR of 11.03%.

- In 2025, the Asia Pacific held a dominant market position in the Global Smartphone Insurance Market, capturing more than a 38.6% share.

Role of Generative AI

Generative AI is transforming how insurers evaluate risks in smartphone insurance. It analyzes user behavior and device usage to predict possible damage more accurately. Early pilots show claim processing time reduced by 30%, improving efficiency and customer satisfaction while helping insurers design more precise and flexible policy offerings.

It also plays a strong role in fraud detection by simulating fake claim scenarios to train advanced systems. With insurance fraud reaching $308 billion yearly in some regions, this approach strengthens verification processes. As a result, insurers can maintain fair pricing while reducing losses linked to fraudulent claims.

Investment and Business Benefits

Investment potential is expanding through bundled offerings and targeted insurance plans. The rise of premium smartphone purchases by 50% supports demand for customized protection solutions for high-value devices. Companies are also focusing on partnerships with repair service providers, creating stable revenue streams as claim volumes increase and service ecosystems strengthen.

Insurance offerings support business growth by improving customer retention and increasing additional sales opportunities. Repeat purchases are 25% higher among insured users, which reflects stronger brand loyalty. Organizations also benefit from reduced operational disruptions, as quick claim processing ensures minimal downtime and helps maintain employee productivity with uninterrupted device access.

Regional Analysis

In 2025, the Asia Pacific held a dominant market position in the Global Smartphone Insurance Market, capturing more than a 38.6% share, holding USD 12.50 billion in revenue. This dominance is due to the large smartphone user base and rapid digital adoption across countries such as China, India, and Southeast Asia. Rising sales of mid and premium devices have increased the need for protection against damage and theft. Expanding mobile operator networks and strong e-commerce growth also support easy access to insurance. In addition, growing awareness and affordable plans are encouraging more consumers to adopt smartphone insurance across the region.

For instance, in March 2025, Acko deepened its smartphone-insurance dominance across Asia-Pacific by launching a low-cost, app-native mobile-protection plan bundled with handset purchases on major Indian e-commerce platforms, significantly expanding its reach among first-time and mid-tier smartphone users in India, one of the region’s fastest-growing insurance markets.

China Smartphone Insurance Market Size

The market for Smartphone Insurance within China is growing tremendously and is currently valued at USD 4.99 billion. The market has a projected CAGR of 11.03%. The market is growing strongly due to high smartphone ownership, rising use of premium devices, and increasing repair costs. Consumers are becoming more aware of the financial risk linked to screen damage, theft, and hardware failure. Rapid growth in e-commerce and digital payment use also increases dependence on smartphones. In addition, easy policy access through mobile operators, online platforms, and retail channels is helping expand insurance adoption across urban consumers.

For instance, in April 2025, Xiaomi Insurance expanded its smartphone protection footprint in China by bundling low-premium accidental-damage and theft coverage directly into Xiaomi phone sales on its e-commerce platform and offline stores, leveraging its high-volume user base to capture a leading share of the mobile-insurance wallet-capture channel in urban China.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Coverage Type Analysis

In 2025, the Accidental Damage segment held a dominant market position, capturing a 56.8% share of the Global Smartphone Insurance Market. This dominance is due to the frequent physical risks faced by smartphones during daily use. Users commonly experience drops, spills, and screen cracks, which create a strong need for protection. Insurance plans focusing on accidental damage provide peace of mind and reduce unexpected repair costs for consumers.

Consumers prefer coverage that directly addresses everyday risks rather than rare events. Accidental damage protection is easy to understand and widely offered at the time of purchase. This makes it the most chosen option, as users aim to protect their devices from common incidents that happen without warning.

For instance, in January 2025, Apple expanded its AppleCare+ offering to include broader accidental-damage coverage and more flexible subscription options, allowing customers to buy protection beyond the initial purchase window. This move reflects a shift toward long-term device protection that aligns with how people use and upgrade their phones over time.

Claim Type Analysis

In 2025, the Repair segment held a dominant market position, capturing a 41.3% share of the Global Smartphone Insurance Market. This dominance is due to the practical and cost-effective nature of repair services. Most smartphone issues can be fixed quickly without replacing the entire device. Users benefit from shorter waiting times and lower service disruption, which repairs the preferred claim option in many cases.

Repair services are widely available through authorized centers and service networks. Quick turnaround times and reliable fixes encourage users to choose repair over replacement. This approach also supports sustainability by extending device life, which aligns with growing awareness around reducing electronic waste.

For instance, in March 2025, Asurion enhanced its device-protection platform to speed up repairs and streamline claims for accidental damage, partnering with a wider network of service centers. This improves turnaround for screen, port, and battery repairs, which makes repair-based claims more attractive than full device replacements.

Distribution Channel Analysis

In 2025, the Mobile Operators segment held a dominant market position, capturing a 49.7% share of the Global Smartphone Insurance Market. This dominance is due to the convenience offered by mobile operators at the point of sale. Customers often purchase insurance while buying a new phone or activating a plan. This integrated approach simplifies decision-making and increases adoption among users seeking immediate device protection.

Mobile operators also provide bundled services, including billing, support, and claims management. This creates a seamless experience for customers, reducing the effort in managing multiple service providers. Strong customer relationships and wide retail presence further support operator-led distribution channels in maintaining their leading position.

For instance, in February 2026, AT&T expanded its device-protection offering by adding more flexible tiers and better transparency around repair versus replacement options. By embedding these plans into online and retail purchase flows, AT&T is making it simpler for subscribers to insure their phones without leaving the carrier ecosystem.

End-User Analysis

In 2025, the Individual segment held a dominant market position, capturing a 83.4% share of the Global Smartphone Insurance Market. This dominance is due to the personal importance of smartphones in everyday life. Individuals rely heavily on their devices for communication, payments, entertainment, and work-related activities. Protecting these devices becomes essential as any damage or loss directly impacts daily routines and personal data access.

Rising smartphone usage across all age groups continues to expand the individual user base. Consumers are becoming more aware of the financial risks linked to device damage or theft. This awareness drives higher adoption of insurance plans among individuals who seek reliable and continuous device usage.

For instance, in December 2025, Samsung expanded its consumer-facing device-protection plans in several Asian markets, tailoring coverage to mid-range and premium smartphones used by individual buyers. By offering simple monthly or annual plans, Samsung is making insurance more accessible to non-corporate users.

Key Market Segments

By Coverage Type

- Accidental Damage

- Liquid Damage

- Theft & Loss

- Others

By Claim Type

- Repair

- Replacement

- Others

By Distribution Channel

- Mobile Operators

- Device OEMs

- Retailers

- Online

- Banks

By End-User

- Individual

- Enterprise

Emerging Trends

On-demand insurance is gaining traction, allowing users to activate coverage only when required, such as during travel. Mobile applications support this shift, enabling 40% faster sign-ups. At the same time, digital platforms and AI-driven personalization are helping insurers create policies that match individual usage patterns and lifestyle needs.

Integration of IoT sensors in smartphones enables real-time monitoring and early alerts for potential issues. These systems connect with 5G networks for quick diagnostics and faster response. Blockchain technology is also being adopted to secure claim records, improving transparency and strengthening customer trust in digital insurance ecosystems.

Growth Factors

The rising cost of smartphones is a key growth driver, as repair expenses often exceed 50% of the device value. Consumers are increasingly choosing insurance to avoid high out-of-pocket costs. Frequent device upgrades and bundled insurance offers through e-commerce platforms further encourage adoption across a wider customer base.

Increasing incidents of theft and accidental damage, especially in urban areas, continue to support market expansion. Growing smartphone dependence for daily tasks amplifies the need for protection. Awareness campaigns and faster digital claim processes enhance user experience, leading to higher retention and repeat purchases in the smartphone insurance segment.

Market Dynamics

Drivers - Costly Repairs and Daily Dependence

Rising smartphone repair costs are encouraging more users to choose insurance for financial protection. Modern devices are expensive to fix, especially when screens, cameras, or internal parts are damaged. This makes insurance more appealing for users who want to avoid sudden spending after accidental damage or technical problems.

Daily dependence on smartphones is also supporting market growth. People use their phones for communication, banking, shopping, work, and entertainment throughout the day. When a device stops working, it affects routine activities quickly. Insurance gives users a sense of security by helping them restore access with less disruption.

For instance, in February 2026, Samsung teamed up with Hartford Steam Boiler to launch Smart Home Savings, tying device protection into home insurance to offset rising repair bills for Galaxy phones. With people glued to their smartphones all day, this partnership highlights how dependence drives demand for bundled fixes that ease wallet strain. Early pilots proved it cuts costs effectively.

Restraint - Trust and Policy Complexity

One major restraint in this market is the lack of trust many users have in insurance terms. Consumers often worry about hidden conditions, claim limits, and unclear exclusions. When policy details are difficult to understand, many buyers hesitate to purchase coverage even if they see the value of protection.

Complex claim procedures add to this issue. Some users feel that policy benefits appear simple at first, but become confusing during actual claim filing. Delays, documentation requirements, and approval uncertainty can reduce confidence. This makes transparency and simple communication important for improving customer acceptance in smartphone insurance.

For instance, in July 2025, Asurion powered growth for partners like Cricket Wireless with new trade-in programs, but complex policy terms slowed some uptake as customers questioned coverage details. Building trust remains key when daily users worry about hidden clauses in protection plans. Their retail expansions aim to simplify explanations face-to-face.

Opportunities - Digital and Embedded Sales

A strong opportunity in this market comes from digital and embedded sales channels. Insurance can be offered during online smartphone purchases, mobile app checkouts, or device activation. This makes the buying process easier and more natural, helping providers reach users at the exact moment they are ready to protect a device.

Embedded sales also improve convenience for customers who prefer simple digital journeys. Instead of searching for insurance later, users can add protection in one smooth step. This approach supports higher adoption and creates room for tailored plans based on device type, usage habits, and customer preferences.

For instance, in October 2025, Samsung Fire wrapped up a big investment in Lloyd’s insurer Canopius to strengthen digital reinsurance ties, embedding mobile coverage into global sales channels. Digital platforms make it simple to add protection at purchase, opening doors for embedded deals worldwide. Stronger partnerships fuel this growth.

Challenges - Fraud and Claim Verification

Fraud remains a serious challenge for smartphone insurance providers. False damage reports, duplicate claims, and dishonest documentation can increase operating pressure. These issues raise costs for insurers and make the system harder to manage fairly. As fraud risks grow, claim processes often become stricter and less convenient for genuine users.

Claim verification is also becoming more difficult in fast digital environments. Insurers must balance quick service with careful checks on ownership, damage history, and policy eligibility. If this balance is weak, customer trust may decline. Strong verification systems are needed to protect both service quality and long-term market stability.

For instance, in January 2026, Verizon leaned on Asurion’s platform innovations to tackle fraud in claims, with new verification tech slowing fake submissions but delaying honest payouts. Balancing quick checks against scams frustrates users who need fast device replacements. Tighter processes aim to cut losses overall.

Key Players Analysis

One of the leading players, in March 2025, Asurion partnered with Walmart to offer instant smartphone insurance activation at checkout for 1,200+ stores, reaching underserved rural markets. This retail expansion added 2 million policies in Q1, leveraging Walmart’s foot traffic to solidify Asurion’s lead in accessible, affordable device protection across America.

Top Key Players in the Market

- Apple

- Samsung

- Asurion

- Assurant

- Allianz

- AXA

- Liberty Mutual

- Verizon

- AT&T

- T-Mobile

- Sprint

- SquareTrade

- Protect Your Bubble

- Gadget Cover

- Insurance2go

- Others

Recent Developments

- In February 2025, Samsung launched Samsung Care+ 360, a $15/month flexible insurance tier covering Galaxy devices with same-day screen repairs at 5,000+ authorized centers nationwide. The program targets U.S. millennials, bundling accessory coverage and software support to compete directly with carrier plans while driving ecosystem loyalty.

- In May 2025, Allianz introduced a bundled smartphone-family plan covering up to 5 devices for $25/month, emphasizing cyber protection alongside physical damage. Targeted at U.S. households, this innovation grew their market share by 12% through aggressive digital marketing and partnerships with Best Buy.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 32.4 Billion |

| Forecast Revenue (2035) | USD 78.1 Billion |

| CAGR (2026-2035) | 9.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Coverage Type (Accidental Damage, Liquid Damage, Theft & Loss, Others), By Claim Type (Repair, Replacement, Others), By Distribution Channel (Mobile Operators, Device OEMs, Retailers, Online, Banks), By End-User (Individual, Enterprise) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Apple, Samsung, Asurion, Assurant, Allianz, AXA, Liberty Mutual, Verizon, AT&T, T-Mobile, Sprint, SquareTrade, Protect Your Bubble, Gadget Cover, Insurance2go, Others |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |